|

市場調查報告書

商品編碼

1851028

軟體定義廣域網路:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)Software-Defined Wide Area Network - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

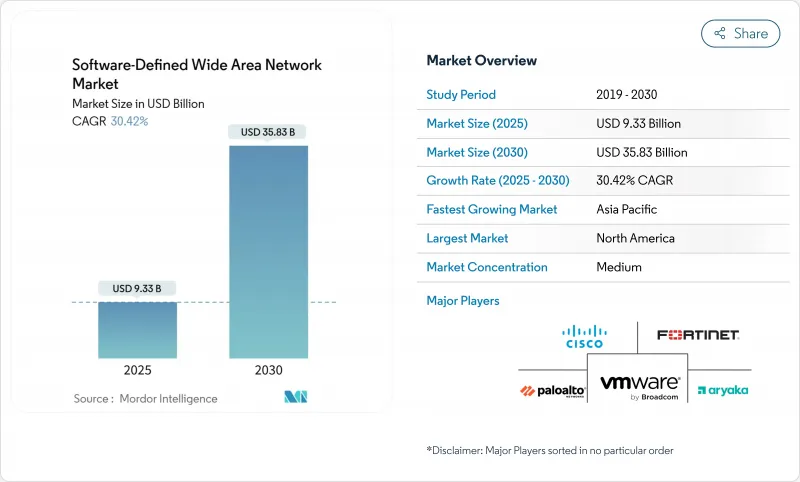

軟體定義廣域網路市場規模預計在 2025 年達到 93.3 億美元,預計到 2030 年將達到 358.3 億美元,預測期(2025-2030 年)複合年成長率為 30.42%。

這一前景反映了從傳統 MPLS 向雲端原生架構的重大轉變,後者能夠支援分散式辦公室、AI主導的工作負載和 5G 流量。企業決策者正在優先考慮直連雲端、整合安全性和應用程式感知路由,這促使供應商在其產品中嵌入自動化和機器學習功能。雲端超大規模資料中心業者與通訊業者之間的夥伴關係,透過將高容量存取、網路切片和託管安全服務捆綁在基於結果的服務模式中,正在加速雲端原生架構的普及。同時,儘管人才短缺和資料平面安全問題在短期內限制了雲端原生架構的普及,但隨著企業追求頻寬效率和營運敏捷性,其長期發展勢頭依然強勁。

全球軟體定義廣域網路市場趨勢與洞察

雲端中心應用程式的爆炸性成長

向SaaS和雲端原生工作負載的快速轉型正促使企業重新設計其廣域網,以實現對分散式應用程式的零延遲存取。 Salesforce採用Prisma SD-WAN後,在不增加通訊成本的情況下,可用頻寬提高了五倍。如今,企業需要能夠即時識別、分類和確定數千種雲端服務的優先順序的策略引擎,從而將商業模式從基於容量的協定轉向基於體驗的協定。超大規模資料中心業者正在積極回應:Google雲端與Lumen合作,為5萬個地點提供400Gbps光纖,並整合雲端廣域網路和SD-WAN編配,以支援AI工作負載。隨著買家傾向於選擇能夠跨多重雲端連接運算、儲存和廣域網路的單一供應商解決方案,整合進程正在加速。軟體定義廣域網路市場將繼續受益於雲端策略和網路策略的這種整合。

混合/遠距辦公主導的廣域網路敏捷性

持續的混合辦公模式需要彈性鏈路、零接觸配置和整合安全功能,將企業網路架構擴展到任何終端。儘管在許多市場,MPLS 配置仍然需要 40 週或更長時間,但 SD-WAN 能夠利用寬頻、4G 和衛星網路,透過主動-主動路徑選擇,在幾天內完成分支機構的部署。 T-Mobile 正與 Palo Alto Networks 合作推出託管式 SASE,將 5G 高階存取與雲端安全相結合,為企業提供從總部到家庭辦公室的彈性頻寬和一致的策略。這種對敏捷性的需求正在推動軟體定義廣域網路 (SD-WAN) 市場快速成長,尤其是在擁有多個分支機構的跨國企業中。

資料平面安全與控制平面攻擊面

分店直接遭受網路入侵會擴大威脅面。 IFIC銀行將新一代防火牆與SD-WAN邊緣結合,降低了40%的監控成本,並且能夠滿足嚴格的監管審核。控制平面遭到破壞仍然是一個重大風險,因為單一配置錯誤就可能在整個網路中傳播。因此,供應商正在跨編排通道整合零信任狀態檢查、安全硬體模組和雙向TLS。安全審查可能會延緩一些部署進程,但最終會透過增強人們對編配定義廣域網路市場的信心來推動其普及。

細分市場分析

預計2024年,雲端託管覆蓋網路將佔據軟體定義廣域網路(SWAN)市場48%的佔有率,屆時SWAN市場規模將達到45億美元,到2030年將以33.2%的複合年成長率成長。企業傾向於採用按需付費模式,以降低資本支出,並提供與IaaS和SaaS環境的無縫連接。自建平台在嚴格監管的行業中佔據主導地位,但其普及受到硬體更新周期和生態系統規模有限的限制。混合架構將本機控制器執行個體與公共雲端結合,既滿足資料駐留需求,又能利用全球存取點(POP)實現規模化擴充。

隨著雲端部署密度和 API 整合深度的不斷提升,廠商之間的競爭日益激烈。博通公司將 VMware VeloCloud 與賽門鐵克邊緣節點整合,體現了向分散式、雲端優先架構的轉型,這種架構能夠以線速實現安全性和服務品質保障。買家正在尋找能夠自動發現雲端應用、透過 Terraform 編排策略並與服務網格整合的解決方案。這些功能使得雲端採用成為軟體定義廣域網路市場的關鍵成長引擎。

2024年,軟體定義廣域網路(SD-WAN)市場規模將達61億美元,其中解決方案營收佔高達65%。早期採用者正從概念驗證硬體套裝轉向全面託管的SD-WAN部署。整合、策略設計和全天候監控需要許多企業缺乏的專業技能。因此,諮詢和生命週期管理在合約總價值中所佔的佔有率越來越大。

Zayo等供應商已與SSE領導者Netskope合作,在單一服務等級協定(SLA)下提供安全邊緣和連線服務。這種成長趨勢表明,長期差異化將更多地取決於平台開放性和服務創新,而非專有硬體,從而強化軟體定義廣域網路市場的混合價值獲取模式。

軟體定義廣域網路市場報告按部署類型(本地部署、雲端部署、混合部署)、組件(解決方案和服務)、組織規模(大型企業和中小企業)、最終用戶行業垂直領域(醫療保健、銀行、金融服務和保險、零售和消費者服務、製造業、運輸和物流、IT 和通訊等)以及地區進行細分。

區域分析

到2024年,北美將佔據軟體定義廣域網路(SWAN)市場規模的55%,這反映出雲端運算的日益普及、風險資金籌措的活躍以及網路安全法規的日益嚴格。 Verizon 59億美元的MPLS減損損失表明,軟體主導的疊加網路正在加劇傳統傳輸方式的經濟困境。美國補貼安全網路閘道的計畫將進一步刺激市場需求,而加拿大和墨西哥也將受益於跨國汽車和零售公司的跨國整合。目前,該地區正轉向SASE融合,促使供應商將防火牆即服務和零信任認證整合到所有SWAN產品中。

亞太地區是成長最快的地區,預計到2030年將以32.6%的複合年成長率成長。積極的5G部署為企業提供了全新的選擇,可以將蜂窩網路和寬頻網路整合到一個可程式設計的疊加網路中。新加坡電信將於2024年在其企業級SD-WAN邊緣之上擴展消費級5G網路切片功能,凸顯了通訊業者推動該地區5G普及的雄心。中國的智慧製造群、印度的IT外包中心以及東協高速成長的數位經濟將匯聚一堂,創造數十億美元的需求。本地系統整合商將與全球OEM廠商合作,提供合規性和語言本地化服務,從而拓展軟體定義廣域網路的市場。

儘管監管體系較為分散,歐洲仍展現出巨大的市場潛力。歐盟委員會的「數位十年」計畫旨在2030年向下一代連接技術投入2000億歐元,其中軟體定義廣域網路(SD-WAN)將成為跨境資料流的核心要素。技能短缺問題依然嚴峻,光是德國預計到2026年就將面臨78萬名資訊通訊技術(ICT)專業人員的缺口。沃達豐英國等業者正透過諮詢服務來應對這項挑戰,將碳排放報告與安全邊緣設計結合。因此,歐洲的監管法規和永續性要求正在發揮成熟供應商的優勢,推動軟體定義廣域網路市場的穩定成長。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 以雲端為中心的應用程式爆發式成長

- 混合/遠距辦公主導的廣域網路敏捷性

- MPLS成本削減和頻寬最佳化

- 人工智慧驅動的自修復路線最佳化

- 5G網路切片與SD-WAN融合

- 與環境、社會和治理 (ESG) 相關的碳排放最佳化路線的需求

- 市場限制

- 資料平面安全與控制平面攻擊面

- SD-WAN架構人才短缺

- 專有疊加的鎖定風險

- CPE供應鏈瓶頸

- 價值/供應鏈分析

- 監管環境

- 技術展望

- 波特五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 透過部署模式

- 前提

- 雲

- 混合

- 按組件

- 解決方案

- 服務

- 按組織規模

- 主要企業

- 小型企業

- 按最終用戶行業分類

- 衛生保健

- BFSI

- 零售和消費者服務

- 製造業

- 運輸與物流

- 資訊科技和電信

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 歐洲

- 英國

- 德國

- 法國

- 西班牙

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 亞太其他地區

- 中東和非洲

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Cisco Systems

- Fortinet

- VMware(Broadcom)

- Aryaka Networks

- Versa Networks

- HPE Aruba

- Nokia(Nuage Networks)

- Huawei

- Tata Communications

- Ericsson

- Cato Networks

- Palo Alto Networks

- Silver Peak(HPE)

- Masergy(Comcast)

- Juniper Networks

- Citrix Systems

- Zscaler

- Riverbed Technology

- Check Point Software

- Barracuda Networks

- ATandT Business

- Telstra

第7章 市場機會與未來展望

The Software-Defined Wide Area Network Market size is estimated at USD 9.33 billion in 2025, and is expected to reach USD 35.83 billion by 2030, at a CAGR of 30.42% during the forecast period (2025-2030).

This outlook reflects the decisive shift from legacy MPLS to cloud-native architectures that sustain distributed workforces, AI-driven workloads, and 5G traffic. Enterprise decision makers are prioritizing direct-to-cloud connectivity, integrated security, and application-aware routing, pushing vendors to embed automation and machine learning across offerings. Partnerships between cloud hyperscalers and telecom carriers accelerate adoption by bundling high-capacity access, network slicing, and managed security under outcome-based service models. Meanwhile, talent shortages and data-plane security concerns temper near-term rollouts, yet the long-run trajectory remains strong as enterprises pursue bandwidth efficiency and operational agility.

Global Software-Defined Wide Area Network Market Trends and Insights

Cloud-centric Application Explosion

Rapid migration to SaaS and cloud-native workloads reshapes WAN design as enterprises target latency-free access to distributed applications. Salesforce increased available bandwidth fivefold after adopting Prisma SD-WAN without raising telecom costs. Enterprises now demand policy engines that identify, classify, and prioritise thousands of cloud services in real time, shifting commercial models from capacity-based to experience-level agreements. Hyperscalers are responding: Google Cloud teamed with Lumen to deliver 400 Gbps fibre to 50,000 locations, embedding Cloud WAN and SD-WAN orchestration for AI workloads. Consolidation accelerates as buyers favour single-vendor stacks that bridge compute, storage, and wide-area connectivity across multi-cloud estates. The Software-Defined Wide Area Network market continues to benefit from this alignment of cloud and network strategies.

Hybrid/Remote-work-driven WAN Agility

Permanent hybrid work models require resilient links, zero-touch provisioning, and integrated security that extend corporate fabrics to any endpoint. MPLS provisioning still runs 40-plus weeks in many markets, whereas SD-WAN enables branch turn-ups in days using broadband, 4G, and satellite for active-active path selection. T-Mobile collaborated with Palo Alto Networks to launch a managed SASE offer that marries 5G Advanced access with cloud security, giving enterprises elastic bandwidth and consistent policy from headquarters to home offices. Demand for such agility keeps the Software-Defined Wide Area Network market on a steep adoption curve, especially among multinational corporations with volatile site counts.

Data-plane Security and Control-plane Attack Surface

Direct internet breakouts at branch sites enlarge the threat canvas. IFIC Bank mitigated exposure by combining next-generation firewalls with its SD-WAN edge, lowering monitoring costs by 40% while satisfying strict regulatory audits. Control-plane compromise remains a material risk because a single misconfiguration can propagate network-wide. Vendors are therefore integrating zero-trust posture checks, secure hardware modules, and mutual TLS across orchestration channels. Security diligence slows some rollouts, yet ultimately lifts adoption by increasing confidence in the Software-Defined Wide Area Network market.

Other drivers and restraints analyzed in the detailed report include:

- MPLS Cost-out and Bandwidth Optimisation

- AI-driven Self-healing Route Optimisation

- Shortage of SD-WAN Architecture Talent

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud-hosted overlays captured 48% of the Software-Defined Wide Area Network market share in 2024, equal to USD 4.5 billion of the Software-Defined Wide Area Network market size, and are set to expand at 33.2% CAGR to 2030. Enterprises favour consumption-based models that remove capex and provide frictionless links into IaaS and SaaS environments. Premise-based platforms persist in highly regulated sectors but face slower uptake due to hardware refresh cycles and smaller ecosystems. Hybrid designs blend controller instances on-premises with public cloud to satisfy data residency while leveraging global POPs for scale.

Vendor competition increasingly revolves around cloud footprint density and API integration depth. Broadcom's unification of VMware VeloCloud with Symantec edge nodes exemplifies the pivot to distributed, cloud-first fabrics capable of enforcing security and quality of service at line-rate. Buyers seek solutions that auto-discover cloud apps, adjust policies via Terraform, and integrate with service meshes. These capabilities keep cloud deployment the primary growth engine in the Software-Defined Wide Area Network market.

Solutions generated 65% of revenue in 2024, equating to USD 6.1 billion of Software-Defined Wide Area Network market size, while services posted the steeper 32.45% CAGR outlook. Early adopters have transitioned from proof-of-concept hardware bundles to full-scale managed SD-WAN estates. Integration, policy design, and 24 X 7 monitoring demand specialist skills that many enterprises lack. Consulting and lifecycle management, therefore, account for a rising share of total contract value.

Providers like Zayo partner with SSE leader Netskope to deliver secure edge plus connectivity as a single SLA, illustrating how services envelop technology to deliver outcomes. The growth trajectory signals that long-term differentiation will hinge on platform openness and service innovation more than on proprietary hardware, reinforcing hybrid value capture in the Software-Defined Wide Area Network market.

The Software-Defined Wide Area Network Market Report is Segmented by Deployment Mode (Premise, Cloud, Hybrid), Component (Solutions and Services), Organisation Size (Large Enterprises and Small and Medium Enterprises), End-User Industry (Healthcare, BFSI, Retail and Consumer Services, Manufacturing, Transport and Logistics, IT and Telecom, and Others), and Geography.

Geography Analysis

North America accounted for 55% of the Software-Defined Wide Area Network market size in 2024, reflecting advanced cloud adoption, robust venture funding, and proactive cyber regulations. Verizon's USD 5.9 billion MPLS impairment illustrates how software-driven overlays cannibalise legacy transport economics. US federal programs that subsidise secure internet gateways further stimulate demand, while Canada and Mexico benefit from cross-border integrations by auto and retail multinationals. The region now pivots to SASE convergence, pushing vendors to bundle firewall-as-a-service and zero-trust authentication into every Software-Defined Wide Area Network market offer.

Asia Pacific represents the fastest expanding theatre, pacing at 32.6% CAGR to 2030. Aggressive 5G rollouts give enterprises clean-sheet options to bond cellular with broadband under programmable overlays. Singtel extended consumer-grade 5G network slicing on top of its enterprise SD-WAN edge in 2024, underscoring how carrier ambition propels regional uptake. China's smart-manufacturing clusters, India's IT outsourcing hubs, and ASEAN's hyper-growth digital economy converge to create multi-billion-dollar incremental demand. Local system integrators partner with global OEMs to tailor compliance and language localisation, broadening the Software-Defined Wide Area Network market footprint.

Europe delivers a sizeable volume despite fragmented regulations. The European Commission's Digital Decade aims to channel EUR 200 billion into next-gen connectivity by 2030, making SD-WAN a core element for cross-border data flow. Skills shortages remain acute; Germany alone expects a gap of 780,000 ICT professionals by 2026. Operators like Vodafone UK respond with advisory practices that fuse carbon reporting and secure edge design. Consequently, Europe's layered regulatory and sustainability demands play to the strengths of mature vendors, reinforcing steady growth in the Software-Defined Wide Area Network market.

- Cisco Systems

- Fortinet

- VMware (Broadcom)

- Aryaka Networks

- Versa Networks

- HPE Aruba

- Nokia (Nuage Networks)

- Huawei

- Tata Communications

- Ericsson

- Cato Networks

- Palo Alto Networks

- Silver Peak (HPE)

- Masergy (Comcast)

- Juniper Networks

- Citrix Systems

- Zscaler

- Riverbed Technology

- Check Point Software

- Barracuda Networks

- ATandT Business

- Telstra

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cloud-centric application explosion

- 4.2.2 Hybrid/remote-work-driven WAN agility

- 4.2.3 MPLS cost-out and bandwidth optimization

- 4.2.4 AI-driven self-healing route optimisation

- 4.2.5 5G network slicing and SD-WAN convergence

- 4.2.6 ESG-linked carbon-aware routing demand

- 4.3 Market Restraints

- 4.3.1 Data-plane security and control-plane attack surface

- 4.3.2 Shortage of SD-WAN architecture talent

- 4.3.3 Proprietary overlay lock-in risks

- 4.3.4 CPE supply-chain bottlenecks

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Mode

- 5.1.1 Premise

- 5.1.2 Cloud

- 5.1.3 Hybrid

- 5.2 By Component

- 5.2.1 Solutions

- 5.2.2 Services

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By End-user Industry

- 5.4.1 Healthcare

- 5.4.2 BFSI

- 5.4.3 Retail and Consumer Services

- 5.4.4 Manufacturing

- 5.4.5 Transport and Logistics

- 5.4.6 IT and Telecom

- 5.4.7 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Italy

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Cisco Systems

- 6.4.2 Fortinet

- 6.4.3 VMware (Broadcom)

- 6.4.4 Aryaka Networks

- 6.4.5 Versa Networks

- 6.4.6 HPE Aruba

- 6.4.7 Nokia (Nuage Networks)

- 6.4.8 Huawei

- 6.4.9 Tata Communications

- 6.4.10 Ericsson

- 6.4.11 Cato Networks

- 6.4.12 Palo Alto Networks

- 6.4.13 Silver Peak (HPE)

- 6.4.14 Masergy (Comcast)

- 6.4.15 Juniper Networks

- 6.4.16 Citrix Systems

- 6.4.17 Zscaler

- 6.4.18 Riverbed Technology

- 6.4.19 Check Point Software

- 6.4.20 Barracuda Networks

- 6.4.21 ATandT Business

- 6.4.22 Telstra

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

軟體定義廣域網路 (SD-WAN) 市場:按元件、連線類型、部署模式、組織規模和最終用戶產業分類-2026-2032 年全球市場預測政府軟體定義廣域網路市場:按組件、部署、組織規模、安全性、最終用戶和應用分類-2026-2032年全球市場預測

軟體定義廣域網路 (SD-WAN) 市場:按元件、連線類型、部署模式、組織規模和最終用戶產業分類-2026-2032 年全球市場預測政府軟體定義廣域網路市場:按組件、部署、組織規模、安全性、最終用戶和應用分類-2026-2032年全球市場預測 2026年全球軟體定義廣域網路(SD-WAN)市場報告

2026年全球軟體定義廣域網路(SD-WAN)市場報告 軟體定義廣域網路 (SD-WAN) 市場分析及至 2035 年預測:按類型、產品類型、服務、技術、元件、應用程式、部署類型、最終用戶、解決方案和功能分類

軟體定義廣域網路 (SD-WAN) 市場分析及至 2035 年預測:按類型、產品類型、服務、技術、元件、應用程式、部署類型、最終用戶、解決方案和功能分類 軟體定義一切市場-全球產業規模、佔有率、趨勢、機會及預測(依技術、服務、垂直產業、地區及競爭格局分類,2021-2031年)

軟體定義一切市場-全球產業規模、佔有率、趨勢、機會及預測(依技術、服務、垂直產業、地區及競爭格局分類,2021-2031年) 軟體定義廣域網路 (SD-WAN) 市場規模、佔有率和成長分析(按組件、部署模式、組織規模、垂直產業和地區分類)-2026-2033 年產業預測

軟體定義廣域網路 (SD-WAN) 市場規模、佔有率和成長分析(按組件、部署模式、組織規模、垂直產業和地區分類)-2026-2033 年產業預測 全球 SD-WAN 市場(按解決方案、服務、組織規模和最終用戶分類)- 預測至 2030 年

全球 SD-WAN 市場(按解決方案、服務、組織規模和最終用戶分類)- 預測至 2030 年 全球軟體定義廣域網路市場

全球軟體定義廣域網路市場 2025-2029年全球SD-WAN市場

2025-2029年全球SD-WAN市場 SDE(軟體定義一切)的全球市場(2024-2028)

SDE(軟體定義一切)的全球市場(2024-2028)