|

市場調查報告書

商品編碼

1850980

持續測試:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)Continuous Testing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

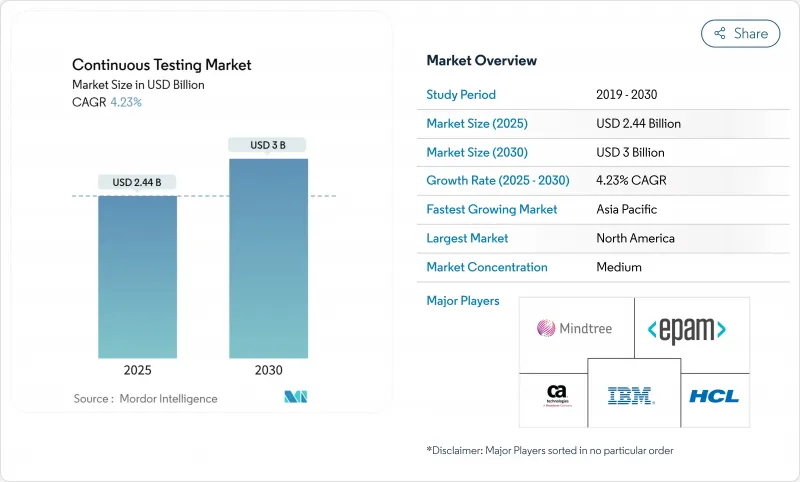

預計到 2025 年,連續測試市場規模將達到 24.4 億美元,到 2030 年將達到 30 億美元,年複合成長率為 4.2%。

這是由於持續測試市場正從傳統的品質保證工作流程轉向以人工智慧支援、以合規性為中心的生態系統。超過68%的公司已將生成式人工智慧融入其品質工程流程。這一成長勢頭得益於DevOps以20.1%的複合年成長率持續成長,儘管只有大約一半的DevOps採用者完全整合了測試自動化。隨著技能短缺推動測試環境編配的外部化,託管服務夥伴關係關係蓬勃發展,同時,為了響應歐洲新《網路彈性法案》的里程碑,功能測試和安全測試的組合也在重新平衡。雖然北美在地理上佔據領先地位,但隨著製造業、銀行業和零售業的快速數位化,亞太地區正以5.0%的複合年成長率縮小差距。

全球連續測試市場趨勢與洞察

採用敏捷和DevOps方法

儘管DevOps實踐如今已成為主流,但測試方面的差距仍然巨大,因為持續測試所需的技能仍然短缺。在受監管的銀行環境中,結合DevOps和持續測試的公司報告稱,生產力提高了20%,因為人工智慧產生的測試案例縮短了發布週期,同時保留了審核追蹤。隨著向品質工程模式的轉變,傳統QA職能的角色正在縮小,測試覆蓋率的責任轉移到了整個開發團隊。分析師預測,到2027年,90%的測試工作流程將自動化,這將增加對人工智慧保障工程師和模型訓練人員的需求。像Nationwide Building Society這樣的機構指出,在敏捷迭代早期階段引入測試的好處在於,可以加快變更交付速度並提高客戶滿意度。

新冠疫情後加速數位轉型勢在必行

快速向數位化管道轉型迫使企業以前所未有的速度發佈軟體,這往往突破了品質保障的底線。由於程式碼未經完整的回歸測試週期就被推送,拉丁美洲企業正面臨缺陷發布數量增加的問題。一家全球連鎖企業在維持「五個九」運轉率的同時,每天處理 1 萬個訂單,但轉換率卻提高了 4.5 個百分點。製造業領導者表示,智慧工廠的競爭優勢取決於軟體質量,但當人工智慧試點計畫無法擴展時,其雄心壯志往往停滯不前,這凸顯了平台級測試框架的必要性,該框架能夠彌合概念驗證和企業部署之間的差距。

缺乏端到端測試環境編配技能

美國勞動市場數據顯示,到2032年,品質保證(QA)職缺將成長17%,如果這些職缺持續空缺,每年可能造成1,620億美元的產出損失。目前,能夠整合持續整合/持續交付(CI/CD)管線、雲端基礎設施和人工智慧主導的測試自動化的專家嚴重短缺。為了填補人手不足,企業正在採購託管服務和無程式碼測試平台,從而降低了技術水平較低的人員的准入門檻。雖然自動化消除了重複性工作,但對能夠建立人工智慧模型、進行偏見審核以及保護管線免受資料外洩的架構師的需求卻在不斷成長。

細分市場分析

到2024年,託管服務將佔持續測試市場的67.8%,到2030年將以5.8%的複合年成長率成長。企業對外部合作夥伴的依賴日益增強,主要原因是其內部運作複雜、人工智慧驅動的測試環境的能力有限,而這些環境必須滿足日益嚴格的監管標準。服務供應商正在重新定位自身,聘用人工智慧保障工程師和模型治理人員,而不是傳統的手動負責人。諮詢和專業服務業務是外包業務的補充,並引導客戶完成向品質工程和雲端運維方向的文化轉變。

如今,託管服務模式已不再局限於基礎測試執行,而是涵蓋了全面的品質智慧分析,服務提供者致力於確保快速發布、風險分析和高效的測試調度。在澳洲和紐西蘭,一些公司將雲端遷移和資料現代化工作流程打包在一起,並重新聘請專家來處理混合工作負載。這種服務範圍的擴大使現有企業能夠在成長加速的同時保持市場佔有率,從而使託管服務成為持續測試市場的重要組成部分。

到2024年,Web應用程式仍將以58.2%的市佔率成為最大的介面類別,但行動測試預計在2030年前實現5.5%的最高複合年成長率。預計到2027年,智慧型手機主導的商務將佔據全球零售額的大部分,這對分散式設備環境提出了更高的效能和可用性要求。為了在數千種行動裝置組合上保持品牌的一致性,企業正在採用雲端託管設備集群、網路狀況模擬和基於人工智慧的視覺檢驗。

瀏覽器標準正朝著融合區塊鏈和邊緣服務的分散式 Web 4.0 架構演進,這需要新的狀態持久化和 API 層容錯方法。桌面測試對於傳統業務流程平台仍然至關重要,但相關資金投入仍然不足。總體而言,介面的多樣化強化了對統一編配的需求,該編排能夠透過單一介面管理跨通道的測試資料、交付物和分析結果。

持續測試市場報告按服務類型(託管服務和專業服務)、介面(Web、桌面、行動)、部署類型(本地和雲端)、測試類型(功能測試、效能和負載測試、其他)、組織規模(大型企業和中小企業)、垂直行業(銀行、金融服務和保險、IT 和電信、其他)以及地區進行細分。

區域分析

北美地區預計佔2024年營收的26.5%,這得益於DevOps的早期應用、強大的雲端基礎設施以及對高品質工程平台的大力創業投資資金。生成式人工智慧的應用十分廣泛,96%的公司正在測試產生和最佳化工作流程中試點或擴展人工智慧的應用。儘管該地區在技術上處於領先地位,但仍面臨嚴重的人才短缺問題,導致對託管服務協議和自動化工具鏈的依賴性增強。美國銀行報告稱,透過引入能夠推薦基於風險的回歸測試包的人工智慧代理,其生產力實現了兩位數的成長。

亞太地區是成長最快的區域,預計到2030年將以5.0%的複合年成長率成長。中國、印度和東南亞國家正在為其智慧製造和金融科技生態系統注入資金,為持續品質自動化創造了新的待開發區機會。隨著企業尋求SAP S/4HANA升級、API現代化和部門特定合規性報告的專業知識,澳洲和紐西蘭的外包測試業務正在復甦。預計到2033年,該地區將需要新增380萬製造業員工,將推動可擴展、低成本測試框架的需求。

歐洲依然是產業巨頭,這得益於其法規環境,該環境有效地強制推行持續測試。 《網路韌性法案》(Cyber Resilience Act,簡稱CRA)將於2024年通過,《數位營運韌性法案》(Digital Operational Resilience Act,簡稱DORA)將於2025年生效,這兩項法案分別要求製造商和金融機構證明其持續的安全檢驗。德國、法國和英國在企業人工智慧驅動的合規自動化方面的支出處於領先地位,這些自動化系統既能滿足CRA和DORA的指標要求,又能最大限度地減少人工干預。諸如歐盟產品責任指令修正案等配套立法,加強了對軟體缺陷的問責,並促進了持續測試的市場滲透,將品質視為董事會層面的責任,而非工程上的事後考慮。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 採用敏捷和DevOps方法

- 新冠疫情後加速數位轉型勢在必行

- 人工智慧驅動的測試平台日益普及

- 向雲端原生架構與微服務轉型

- 合規壓力促使產品更快、更安全地上市

- 與永續性相關的IT採購優先考慮高效測試

- 市場限制

- 缺乏端到端測試環境編配技能

- 傳統單體架構會降低測試自動化速度。

- 工具鏈碎片化和供應商鎖定問題

- 測試資料隱私法規限制了接近生產環境的資料。

- 價值鏈分析

- 監管環境

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 評估宏觀經濟趨勢對市場的影響

第5章 市場規模與成長預測

- 按服務類型

- 託管服務

- 專業服務

- 透過介面

- Web

- 桌面

- 移動的

- 透過部署模式

- 本地部署

- 雲

- 按測試類型

- 功能測試

- 效能和負載測試

- 安全測試

- API 測試

- UI/UX 測試

- 按組織規模

- 主要企業

- 小型企業

- 按行業

- BFSI

- 資訊科技和通訊

- 零售與電子商務

- 醫療保健和生命科學

- 製造業

- 媒體與娛樂

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 亞太其他地區

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略舉措與發展

- 市佔率分析

- 公司簡介

- IBM Corporation

- Broadcom Inc.(CA Technologies)

- Tricentis GmbH

- Micro Focus International plc

- Sauce Labs Inc.

- Mindtree Ltd(LTIMindtree)

- EPAM Systems Inc.

- HCL Technologies Ltd

- Cigniti Technologies Ltd

- Cognizant Technology Solutions Corp.

- Tech Mahindra Ltd

- Hexaware Technologies Ltd

- Larsen and Toubro Infotech Ltd

- Accenture plc

- Infosys Ltd

- Capgemini SE

- Atos SE

- Keysight Technologies Inc.

- SmartBear Software

- Perfecto(Perforce Software)

- Applitools Ltd

- Parasoft Corporation

- Katalon Inc.

- mabl Inc.

第7章 市場機會與未來展望

The continuous testing market size is valued at USD 2.44 billion in 2025 and is forecast to reach USD 3 billion by 2030, expanding at a 4.2% CAGR.

Behind the measured headline rate, the continuous testing market is shifting from traditional quality-assurance workflows to AI-supported, compliance-centric ecosystems. More than 68% of enterprises have already embedded generative AI into quality-engineering processes. Momentum is reinforced by a wider DevOps backdrop growing at a 20.1% CAGR, although only about half of DevOps adopters have achieved full test-automation integration, signalling untapped headroom inside existing pipelines. Managed service partnerships are thriving as skill shortages drive externalisation of test-environment orchestration, while the functional-to-security testing mix is recalibrating in response to new European Cyber Resilience Act milestones. Geographic leadership remains with North America, yet Asia-Pacific's 5.0% CAGR trajectory suggests a narrowing gap as manufacturers, banks, and retailers digitise at speed.

Global Continuous Testing Market Trends and Insights

Adoption of Agile and DevOps methodologies

DevOps practices are now mainstream, yet sizeable testing gaps persist because continuous testing requires skills that remain scarce. Enterprises that combine DevOps with continuous testing report productivity gains of 20% in regulated banking environments where AI-generated test cases compress release cycles while maintaining audit trails. The role of the traditional QA function is shrinking as companies transition toward quality-engineering models in which responsibility for test coverage shifts to the entire development squad. Analysts expect 90% of all testing workflows to become automated by 2027, elevating demand for AI-assurance engineers and model trainers. Organisations such as Nationwide Building Society illustrate the payoff, citing faster change delivery and higher customer-satisfaction scores after embedding testing earlier in agile increments.

Need for accelerated digital transformation post-COVID

A rapid pivot to digital channels has forced enterprises to release software at unprecedented speed, often stretching quality guardrails. Latin American firms have experienced heightened defect leakage when code is pushed without complete regression cycles. Retailers are scaling AI-guided user-acceptance testing to safeguard 24/7 e-commerce uptime, with one global chain improving conversion by 4.5 percentage points while supporting 10,000 daily orders at "five-nine" availability. Manufacturing leaders say smart-factory competitiveness hinges on software quality, yet ambitions frequently stall when AI pilots cannot be scaled, underscoring the need for platform-level testing frameworks capable of bridging proof-of-concept and enterprise rollout.

Scarcity of end-to-end test-environment orchestration skills

U.S. labour-market data show QA vacancies on course to grow 17% through 2032, potentially placing USD 162 billion of annual output at risk if roles remain unfilled. The gap is acute for specialists who can weave CI/CD pipelines, cloud infrastructure and AI-driven test automation into a cohesive fabric. To offset shortages, enterprises are procuring managed services and codeless test platforms that lower entry barriers for less technical staff. Automation eliminates repetitive tasks but raises demand for architects able to curate AI models, audit bias and safeguard pipelines against data exposure.

Other drivers and restraints analyzed in the detailed report include:

- Rising adoption of AI-augmented testing platforms

- Shift to cloud-native architectures and micro-services

- Legacy monolithic architectures slowing test automation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Managed services captured 67.8% of the continuous testing market in 2024 and are forecast to grow at a 5.8% CAGR through 2030. Heightened reliance on external partners stems from limited in-house capacity to run complex, AI-enabled test estates that must meet tightening regulatory standards. Providers are repositioning, hiring AI-assurance engineers and model governors rather than traditional manual testers. Advisory and professional-services lines complement outsourcing deals, guiding clients through cultural shifts toward quality engineering and CloudOps alignment.

The managed-services model now extends beyond basic test execution to holistic quality intelligence, with providers guaranteeing release velocity, risk analytics, and energy-efficient test scheduling. Renewed demand is visible in Australia and New Zealand, where enterprises bundling cloud migration and data-modernisation workstreams are re-engaging specialists to maintain coverage across hybrid workloads. Such breadth enables incumbents to defend their share even as growth accelerates, making managed services the structural anchor of the continuous testing market.

Web applications remained the largest interface class with a 58.2% share in 2024, but mobile testing is on track for the highest 5.5% CAGR to 2030. Smartphone-led commerce, forecast to comprise a dominant slice of global retail sales by 2027, places rigorous performance and usability demands on distributed device landscapes. Enterprises are adopting cloud-hosted device farms, network-condition emulation, and AI-based visual validation to uphold brand consistency across thousands of handset permutations.

Web testing is hardly static; browser standards are evolving toward decentralized Web 4.0 constructs that blend blockchain and edge services, which in turn mandate new approaches to state persistence and API-layer fault tolerance. Desktop testing remains relevant for legacy business-process platforms, yet receives lower capital allocation. Overall, interface diversification is reinforcing the need for unified orchestration that can manage cross-channel test data, artefacts, and analytics inside a single pane of glass.

The Continuous Testing Market Report is Segmented by Service Type (Managed Services and Professional Services), Interface (Web, Desktop, and Mobile), Deployment Type (On-Premise and Cloud), Testing Type (Functional Testing, Performance and Load Testing, and More), Organization Size (Large Enterprises and Small and Medium Enterprises), Industry Vertical (BFSI, IT and Telecom, and More) and Geography.

Geography Analysis

North America accounted for 26.5% revenue in 2024, benefiting from early DevOps uptake, robust cloud infrastructure, and strong venture funding into quality-engineering platforms. Generative AI adoption is widespread, with 96% of enterprises piloting or scaling AI in test generation and optimisation workflows. Despite technology leadership, the region contends with acute talent shortages, prompting higher reliance on managed-service engagements and automated toolchains. U.S. banks report double-digit productivity gains after embedding AI agents that recommend risk-based regression packs, balancing rapid feature delivery against strict regulatory demands.

Asia-Pacific is the fastest-expanding theatre, registering a projected 5.0% CAGR to 2030. China, India, and Southeast Asian nations are channelling capital into smart manufacturing and fintech ecosystems, creating greenfield opportunities for continuous quality automation. Australia and New Zealand showcase a resurgence in outsourced testing as enterprises hunt for expertise that spans SAP S/4HANA upgrades, API modernisation, and sector-specific compliance reporting. An expected 3.8 million additional manufacturing employees will be required across the region by 2033, magnifying demand for scalable, low-overhead testing frameworks.

Europe remains a heavyweight, shaped by a regulatory environment that effectively mandates continuous testing. The Cyber Resilience Act, adopted in 2024, and the Digital Operational Resilience Act, effective in 2025, oblige manufacturers and financial institutions, respectively, to demonstrate ongoing security validation. Germany, France, and the United Kingdom spearhead enterprise spending on AI-enabled compliance automation that can satisfy both CRA and DORA metrics while minimizing manual effort. Complementary legislation such as the revised EU Product Liability Directive heightens liability for software defects, encouraging continuous testing and market penetration that treats quality as a board-level responsibility rather than an engineering afterthought.

- IBM Corporation

- Broadcom Inc. (CA Technologies)

- Tricentis GmbH

- Micro Focus International plc

- Sauce Labs Inc.

- Mindtree Ltd (LTIMindtree)

- EPAM Systems Inc.

- HCL Technologies Ltd

- Cigniti Technologies Ltd

- Cognizant Technology Solutions Corp.

- Tech Mahindra Ltd

- Hexaware Technologies Ltd

- Larsen and Toubro Infotech Ltd

- Accenture plc

- Infosys Ltd

- Capgemini SE

- Atos SE

- Keysight Technologies Inc.

- SmartBear Software

- Perfecto (Perforce Software)

- Applitools Ltd

- Parasoft Corporation

- Katalon Inc.

- mabl Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Adoption of Agile and DevOps methodologies

- 4.2.2 Need for accelerated digital transformation post-COVID

- 4.2.3 Rising adoption of AI-augmented testing platforms

- 4.2.4 Shift to cloud-native architectures and micro-services

- 4.2.5 Compliance pressure for faster yet secure releases

- 4.2.6 Sustainability-linked IT procurement favouring efficient testing

- 4.3 Market Restraints

- 4.3.1 Scarcity of end-to-end test-environment orchestration skills

- 4.3.2 Legacy monolithic architectures slowing test automation

- 4.3.3 Tool-chain fragmentation and vendor lock-in concerns

- 4.3.4 Test-data-privacy regulation limiting production-like data

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assessment of the Impact of Macroeconomic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Managed Services

- 5.1.2 Professional Services

- 5.2 By Interface

- 5.2.1 Web

- 5.2.2 Desktop

- 5.2.3 Mobile

- 5.3 By Deployment Mode

- 5.3.1 On-premise

- 5.3.2 Cloud

- 5.4 By Testing Type

- 5.4.1 Functional Testing

- 5.4.2 Performance and Load Testing

- 5.4.3 Security Testing

- 5.4.4 API Testing

- 5.4.5 UI/UX Testing

- 5.5 By Organization Size

- 5.5.1 Large Enterprises

- 5.5.2 Small and Medium Enterprises

- 5.6 By Industry Vertical

- 5.6.1 BFSI

- 5.6.2 IT and Telecom

- 5.6.3 Retail and eCommerce

- 5.6.4 Healthcare and Life Sciences

- 5.6.5 Manufacturing

- 5.6.6 Media and Entertainment

- 5.6.7 Others

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.2.3 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 Germany

- 5.7.3.2 United Kingdom

- 5.7.3.3 France

- 5.7.3.4 Italy

- 5.7.3.5 Spain

- 5.7.3.6 Russia

- 5.7.3.7 Rest of Europe

- 5.7.4 Asia-Pacific

- 5.7.4.1 China

- 5.7.4.2 India

- 5.7.4.3 Japan

- 5.7.4.4 South Korea

- 5.7.4.5 Australia

- 5.7.4.6 Rest of Asia-Pacific

- 5.7.5 Middle East and Africa

- 5.7.5.1 Middle East

- 5.7.5.1.1 Saudi Arabia

- 5.7.5.1.2 United Arab Emirates

- 5.7.5.1.3 Turkey

- 5.7.5.1.4 Rest of Middle East

- 5.7.5.2 Africa

- 5.7.5.2.1 South Africa

- 5.7.5.2.2 Nigeria

- 5.7.5.2.3 Rest of Africa

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves and Developments

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 IBM Corporation

- 6.4.2 Broadcom Inc. (CA Technologies)

- 6.4.3 Tricentis GmbH

- 6.4.4 Micro Focus International plc

- 6.4.5 Sauce Labs Inc.

- 6.4.6 Mindtree Ltd (LTIMindtree)

- 6.4.7 EPAM Systems Inc.

- 6.4.8 HCL Technologies Ltd

- 6.4.9 Cigniti Technologies Ltd

- 6.4.10 Cognizant Technology Solutions Corp.

- 6.4.11 Tech Mahindra Ltd

- 6.4.12 Hexaware Technologies Ltd

- 6.4.13 Larsen and Toubro Infotech Ltd

- 6.4.14 Accenture plc

- 6.4.15 Infosys Ltd

- 6.4.16 Capgemini SE

- 6.4.17 Atos SE

- 6.4.18 Keysight Technologies Inc.

- 6.4.19 SmartBear Software

- 6.4.20 Perfecto (Perforce Software)

- 6.4.21 Applitools Ltd

- 6.4.22 Parasoft Corporation

- 6.4.23 Katalon Inc.

- 6.4.24 mabl Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

持續測試市場:按測試類型、自動化等級、部署模型、組織規模、應用類型和產業分類 - 全球預測(2026-2032 年)

持續測試市場:按測試類型、自動化等級、部署模型、組織規模、應用類型和產業分類 - 全球預測(2026-2032 年) 2026年全球連續測試市場報告持續穿透測試市場按部署方式、類型、服務模式、訂閱模式、組織規模和產業分類,全球預測(2026-2032 年)

2026年全球連續測試市場報告持續穿透測試市場按部署方式、類型、服務模式、訂閱模式、組織規模和產業分類,全球預測(2026-2032 年) 持續測試市場規模、佔有率和成長分析(按組件、部署類型、組織規模、應用、最終用戶產業和地區分類)-2026-2033年產業預測

持續測試市場規模、佔有率和成長分析(按組件、部署類型、組織規模、應用、最終用戶產業和地區分類)-2026-2033年產業預測 全球持續測試市場規模研究與預測,按測試類型、部署、工具類型、垂直產業(銀行、金融服務和保險)和區域預測 2025-2035

全球持續測試市場規模研究與預測,按測試類型、部署、工具類型、垂直產業(銀行、金融服務和保險)和區域預測 2025-2035 2024 年至 2031 年按服務、部署類型、組織規模、介面、垂直和地區劃分的持續測試市場

2024 年至 2031 年按服務、部署類型、組織規模、介面、垂直和地區劃分的持續測試市場