|

市場調查報告書

商品編碼

1850972

虛擬資料室:市場佔有率分析、產業趨勢、統計資料、成長預測(2025-2030 年)Virtual Data Room - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

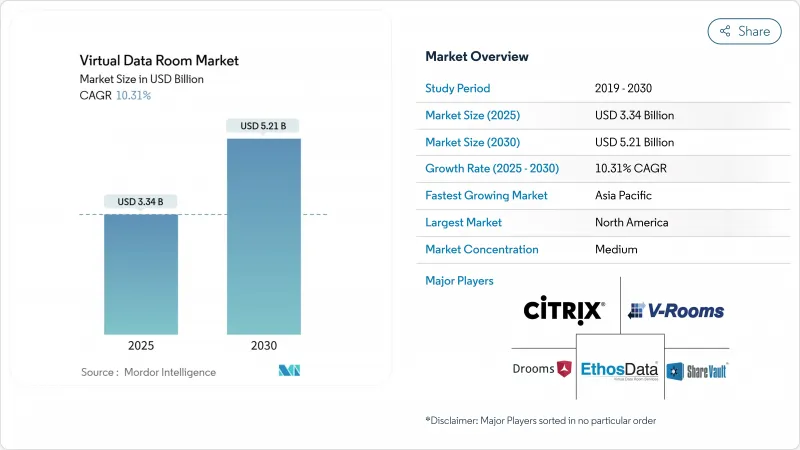

預計到 2025 年,虛擬資料室市場規模將達到 33.4 億美元,到 2030 年將達到 52.1 億美元,複合年成長率為 10.31%。

隨著企業加速推動敏感文件的數位化,以符合日益嚴格的監管要求並簡化跨境交易,市場需求不斷成長。交易規模日益擴大、複雜度不斷提升,促使企業採用安全可靠、支援人工智慧的平台進行實質審查調查和併購後整合。中國的《網路資料安全管理條例》和歐盟的《資料法》迫使服務提供者將儲存在地化並整合精細的審核追蹤,從而推動了歐洲、中東和非洲地區以及亞太地區的市場擴張。訂閱模式的價格已降至每月400至1000美元,消除了以往的成本障礙。產業特定功能,例如生命科學文件的eCTD檢視器,進一步推動了醫療保健和生物技術領域的發展,這兩個產業是成長最快的終端用戶垂直產業,複合年成長率高達15.2%。

全球虛擬資料室市場趨勢與洞察

加速跨境併購進程,需要遵守多個司法管轄區的法規

2024年跨國併購交易金額成長5%,但交易數量下降,凸顯出交易重心正向高價值交易轉移,而這類交易必須滿足相互交織的監管要求,包括反壟斷法、外國投資法和資料隱私法。阿拉伯聯合大公國新的併購控制基準值和德國日益嚴格的外國直接投資篩選機制,都反映了買方面臨的繁複核准流程。印度的《數位個人資料保護法》要求明確的同意和針對特定國家的處理條款,進一步加劇了資訊流的複雜性。供應商正在整合資料主權開關和即時監管清單,以幫助交易團隊根據司法管轄區分類文件位置、使用者存取權限和保留期限。

受監管行業對遠端審核和董事會協作的需求

亞太地區的金融機構正在加速雲端遷移,以降低成本並實現合規現代化,但93%的機構表示,它們在滿足審核要求方面面臨挑戰,這促使它們投資建設具有不可篡改日誌的安全董事會入口網站。中國的《資料安全管理辦法》要求銀行將資訊分類並記錄所有存取事件。納斯達克的子公司管治專利表明,多實體資料分層正在推動簡化監管審查。

資料主權規則限制跨境託管

歐盟《一般資料保護規範》(GDPR)與美國《雲端法案》(CLOUD Act)之間的衝突迫使跨國公司對資料儲存進行隔離,否則將面臨執法風險,迫使服務供應商在德國、日本和澳洲等地開設區域資料中心。中國的「可信數據空間」計畫也同樣限制了國際傳輸,並增加了基礎設施重複建設的資本支出。此外,德國的中小型企業還必須遵守NIS-2和DORA網路安全法規,這增加了合規成本,影響了他們對服務提供者的選擇。

細分市場分析

到2024年,軟體收入將佔總收入的68%,鞏固其作為虛擬資料室市場支柱的地位。然而,隨著越來越多的客戶尋求監管諮詢、人工智慧分析和整合支持,服務領域的成長速度更快,年複合成長率達13.9%。大型客戶擴大將平台授權與工作流程設計計劃捆綁銷售,反映出軟體、軟體與通訊(SS&C)業務的收入在2024年成長至48.4億美元。英國價值65億美元的G-Cloud 14等政府競標也明確指定了託管服務,檢驗了從純粹的軟體交付向基於結果的合約模式的轉變。

當交易涉及隱私保護機制時,對加值服務的需求將會增加,供應商會部署專門團隊來制定資料駐留規則、保留期限和人工智慧主導的補救模型。因此,預計到2030年,實施諮詢、工作流程自動化和隨叫隨到的合規顧問服務將佔市場支出成長的30%以上。這些服務流將有助於對沖核心授權的價格壓力,並增強現有企業的收入多元化。

到2024年,雲端交付將佔總營收的83%,年複合成長率高達14.6%,成為成長最快的領域。這顯示市場普遍認為,超大規模基礎設施如今已能滿足銀行層級的管控要求。雖然以GB計費(每月60-77美元)仍會影響數據量大的用戶,但每月400-1000美元的固定費率方案正促使中等規模的用戶進行轉型。主權條款正推動部分客戶採用混合部署模式,將敏感資料存檔保留在本地,而將分析運算遷移到雲端。

服務供應商正投資多租戶加密和客戶管理金鑰,以確保監管機構認可雲端環境與本地環境同等甚至更佳。公共雲端區域能夠滿足居住法規的接近性,同時降低延遲,加速地理位置分散的交易團隊採用雲端服務。隨著技術信心的增強,預計到 2030 年,傳統本地部署的虛擬資料室市佔率將萎縮至少於 10%。

區域分析

北美地區受益於強勁的資本市場、活躍的私募股權活動以及清晰的資訊揭露法律,在2024年佔據了41%的收入佔有率。該地區虛擬數據室市場的規模主要得益於能源、醫療保健和科技行業的眾多回頭客,他們每年都在執行多個交易項目。 SS&C公司2024年營收成長至48.4億美元,也印證了這項市場需求。

歐洲在疫情後併購市場加速復甦,預計2025年交易量將成長10%。歐盟資料法新增了互通性義務,有利於擁有豐富API介面的平台和在區域內設有儲存節點的供應商。德國加強對外國直接投資的審查,以及中端市場私募股權的復甦,為利用虛擬資料室(VDR)進行即時問答和重新編輯以縮短交易完成時間創造了新的應用場景。

亞太地區將達到最高的複合年成長率,達到14.4%。中國的金融科技發展規劃和資料安全法規正在推動國內託管,鼓勵全球服務供應商建立合資企業和自主雲端平台。日本面向電子供應鏈的法律主導服務強調針對特定產業的合規性在地化創新。印度的新資料隱私法將推動跨國科技和醫藥貿易的普及,鞏固亞太地區作為2030年前全球成長引擎的地位。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 跨境強制令加速實施,要求跨司法管轄區合規,推動市場發展。

- 受監管行業對遠端審核和董事會協作的需求

- 生命科學與科技媒體領域智慧財產權驅動型交易的興起

- 在虛擬資料室平台中採用整合式人工智慧/機器學習分析

- 從孤立的 FTP/電子郵件遷移到安全的基於 SaaS 的資料室

- 市場限制

- 資料主權規則限制跨境託管

- 使用者持續的錯誤配置會導致安全漏洞。

- 對於只有一次性計劃的中小型企業而言,訂閱費用過高

- 供應商轉換和商品化帶來的價格壓力

- 價值鏈分析

- 技術展望

- 對宏觀經濟趨勢的市場評估

- 波特五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭的激烈程度

第5章 市場規模與成長預測

- 按組件

- 軟體

- 服務

- 透過部署模式

- 雲端基礎的

- 本地部署

- 按組織規模

- 小型企業

- 主要企業

- 按業務職能

- 法律與合規

- 財務管理(管理與審計、資金籌措、重組)

- 智慧財產管理

- 銷售與行銷/通路夥伴關係

- 其他業務職能

- 按最終用戶行業分類

- BFSI

- 資訊科技和通訊

- 醫療保健和生命科學

- 政府、公共部門和法律服務

- 其他終端用戶產業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 德國

- 法國

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 亞太其他地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中東

- GCC

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Vault Rooms Inc.

- ShareVault(Pandesa Corporation)

- Drooms GmbH

- Citrix Systems Inc.

- Ansarada Pty Ltd

- CapLinked Inc.

- Firmex Corporation

- SmartRoom(BMC Group)

- Intralinks Holdings Inc.

- Datasite(Merrill Corp.)

- iDeals Solutions Group

- Onehub

- SecureDoc Information Management Pty Ltd

- Brainloop AG

- HighQ Solutions Ltd

- Digify

- ForData

- EthosData

- Venue(Donnelley Financial)

- DealRoom

第7章 市場機會與未來展望

The virtual data room market size is valued at USD 3.34 billion in 2025 and is forecast to reach USD 5.21 billion by 2030, registering a 10.31% CAGR.

Demand is expanding as enterprises accelerate the digitization of sensitive documents to meet tightening regulatory mandates and to streamline cross-border transactions. Deals are becoming larger and more complex, pushing corporates to adopt secure, AI-enabled platforms for due diligence and post-merger integration. China's Network Data Security Management Regulations and the EU Data Act are compelling providers to localize storage and embed granular audit trails, reinforcing market expansion in both EMEA and Asia-Pacific. Large enterprises still generate most revenue, yet SMEs are the fastest-growing buyers because subscription-based models have fallen to USD 400-1,000 per month, removing historical cost barriers. Industry-specific functionality-such as eCTD viewers for life-sciences dossiers-adds further momentum in healthcare and biotech, the fastest-growing end-user vertical at 15.2% CAGR.

Global Virtual Data Room Market Trends and Insights

Accelerated Cross-border M&A Requiring Multi-jurisdiction Compliance

Cross-border deal values rose 5% in 2024 even as volumes slipped, highlighting the shift toward high-stakes transactions that must satisfy overlapping antitrust, foreign investment, and data-privacy laws. New merger-control thresholds in the UAE and stricter FDI filters in Germany illustrate the maze of approvals buyers confront. India's Digital Personal Data Protection Act requires explicit consent and country-specific processing clauses, further complicating information flows. Vendors are embedding data-sovereignty toggles and real-time regulatory checklists so deal teams can map document location, user access, and retention periods by jurisdiction.

Demand for Remote Audit & Board Collaboration in Regulated Industries

Financial institutions in Asia-Pacific are accelerating cloud migration to cut costs and modernize compliance, yet 93% cite difficulty meeting audit demands, fueling investment in secure board portals with immutable logs. China's Data Security Management Measures oblige banks to classify information and document every access event, a mandate now hard-wired into enterprise-grade VDRs. Nasdaq's patent for subsidiary governance showcases the push for multi-entity data hierarchies that streamline regulator reviews.

Data-Sovereignty Rules Limiting Cross-border Hosting

Conflicts between the EU's GDPR and the US CLOUD Act force multinationals to compartmentalize storage or risk enforcement action, driving providers to open regional data centers in Germany, Japan, and Australia. China's Trusted Data Space blueprint similarly restricts outbound transfers, raising capex for infrastructure duplication. German SMEs must also meet NIS-2 and DORA cybersecurity controls, adding compliance overhead that influences provider selection.

Other drivers and restraints analyzed in the detailed report include:

- Rise of IP-centric Transactions in Life Sciences & TMT

- Adoption of Integrated AI/ML Analytics within VDR Platforms

- Persistent User Mis-configuration Driving Security Breaches

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software anchored 68% of revenue in 2024, underscoring its status as the backbone of the virtual data room market. The services component, however, is scaling faster at 13.9% CAGR as clients seek regulatory consulting, AI analytics, and integration support. Large accounts increasingly bundle platform licenses with workflow-design projects, mirroring SS&C's revenue uplift to USD 4.84 billion in 2024. Government tenders such as the UK's USD 6.5 billion G-Cloud 14 are also specifying managed services, validating a shift from pure software delivery to outcome-based engagements.

Demand for premium services rises when transactions span privacy regimes, prompting vendors to position specialized teams that configure data-residency rules, retention schedules, and AI-driven redaction models. As a result, implementation consulting, workflow automation, and on-call compliance advisory are expected to command over 30% of incremental market spend by 2030. The services stream therefore acts as a hedge against price pressure in core licensing, reinforcing revenue diversity for established players.

Cloud delivery captured 83% of 2024 revenue and exhibits the highest growth pace at 14.6% CAGR, signalling market consensus that hyperscale infrastructure can now satisfy bank-grade controls. Per-gigabyte fees-ranging from USD 60-77 per month-still influence heavy-data users, but flat-rate options at USD 400-1,000 monthly encourage midsize buyers to migrate. Sovereignty clauses are steering some clients to hybrid setups where sensitive archives stay on-premise while analytics compute bursts into the cloud.

Providers invest in multi-tenant encryption and customer-managed keys so that regulators accept cloud as an equivalent or superior control environment. The global build-out of public-cloud regions creates proximity that slices latency while satisfying residency statutes, accelerating adoption in geographically dispersed deal teams. As technological confidence mounts, legacy on-premise installations are expected to shrink below 10% of the virtual data room market by 2030.

The Virtual Data Room Market is Segmented by Component (Software, Services), Deployment Mode (Cloud-Based, On-Premise), Organization Size (SMEs, Large Enterprises), by Business Function (Legal and Compliance, Financial Management, Intellectual-Property Management, and More), End-User Industry (BFSI, IT and Telecom, Healthcare and Life Sciences, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 41% of 2024 revenue, supported by deep capital markets, robust private equity activity, and well-defined disclosure laws. The virtual data room market size for the region is buoyed by repeat buyers in energy, healthcare, and technology sectors that execute multi-deal pipelines annually. SS&C's rise to USD 4.84 billion revenue in 2024 underscores this demand.

Europe is gaining momentum as M&A recoveries accelerate post-pandemic, with expected 10% volume growth in 2025. The EU Data Act adds interoperability obligations that favor vendors with API-rich platforms and in-region storage nodes. Germany's heightened FDI scrutiny and mid-cap private equity rebound create use cases where VDR-enabled real-time Q&A and redaction speed closing timelines.

Asia-Pacific posts the highest CAGR at 14.4%. China's Financial Technology Development Plan and data-security regulations compel domestic hosting, prompting global providers to establish joint ventures and sovereign clouds. Japan's LegalTech-led services for electronics supply chains highlight localized innovation that addresses industry-specific compliance. India's new data-privacy law drives adoption in tech and pharma cross-border deals, cementing APAC's role as a growth engine through 2030.

- Vault Rooms Inc.

- ShareVault (Pandesa Corporation)

- Drooms GmbH

- Citrix Systems Inc.

- Ansarada Pty Ltd

- CapLinked Inc.

- Firmex Corporation

- SmartRoom (BMC Group)

- Intralinks Holdings Inc.

- Datasite (Merrill Corp.)

- iDeals Solutions Group

- Onehub

- SecureDoc Information Management Pty Ltd

- Brainloop AG

- HighQ Solutions Ltd

- Digify

- ForData

- EthosData

- Venue (Donnelley Financial)

- DealRoom

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated Cross-border MandA Requiring Multi-jurisdiction Compliance Drives the Market

- 4.2.2 Demand for Remote Audit and Board Collaboration in Regulated Industries

- 4.2.3 Rise of IP-centric Transactions in Life Sciences and TMT

- 4.2.4 Adoption of Integrated AI/ML Analytics within VDR Platforms

- 4.2.5 Migration from Siloed FTP/Email to Secure SaaS-based Data Rooms

- 4.3 Market Restraints

- 4.3.1 Data-Sovereignty Rules Limiting Cross-border Hosting

- 4.3.2 Persistent User Mis-configuration Driving Security Breaches

- 4.3.3 High Subscription Costs for SME One-off Projects

- 4.3.4 Vendor-switching and Commoditization Pressure on Pricing

- 4.4 Value Chain Analysis

- 4.5 Technological Outlook

- 4.6 Assessment of Macro Economic Trends on the Market

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud-based

- 5.2.2 On-premise

- 5.3 By Organization Size

- 5.3.1 Small and Medium Enterprises (SMEs)

- 5.3.2 Large Enterprises

- 5.4 By Business Function

- 5.4.1 Legal and Compliance

- 5.4.2 Financial Management (MandA, Fund-raising, Restructuring)

- 5.4.3 Intellectual-Property Management

- 5.4.4 Sales and Marketing/ Channel Partnerships

- 5.4.5 Other Business Function

- 5.5 By End-user Industry

- 5.5.1 BFSI

- 5.5.2 IT and Telecom

- 5.5.3 Healthcare and Life Sciences

- 5.5.4 Government, Public Sector and Legal Services

- 5.5.5 Other End-user Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 United Kingdom

- 5.6.2.2 Germany

- 5.6.2.3 France

- 5.6.2.4 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Rest of South America

- 5.6.5 Middle East

- 5.6.5.1 GCC

- 5.6.5.2 Turkey

- 5.6.5.3 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Vault Rooms Inc.

- 6.4.2 ShareVault (Pandesa Corporation)

- 6.4.3 Drooms GmbH

- 6.4.4 Citrix Systems Inc.

- 6.4.5 Ansarada Pty Ltd

- 6.4.6 CapLinked Inc.

- 6.4.7 Firmex Corporation

- 6.4.8 SmartRoom (BMC Group)

- 6.4.9 Intralinks Holdings Inc.

- 6.4.10 Datasite (Merrill Corp.)

- 6.4.11 iDeals Solutions Group

- 6.4.12 Onehub

- 6.4.13 SecureDoc Information Management Pty Ltd

- 6.4.14 Brainloop AG

- 6.4.15 HighQ Solutions Ltd

- 6.4.16 Digify

- 6.4.17 ForData

- 6.4.18 EthosData

- 6.4.19 Venue (Donnelley Financial)

- 6.4.20 DealRoom

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

虛擬資料室市場-2026-2032年全球市場預測

虛擬資料室市場-2026-2032年全球市場預測 2026年全球虛擬資料室市場報告

2026年全球虛擬資料室市場報告 虛擬資料室市場規模、佔有率、趨勢和預測:按組件、部署類型、企業規模、業務功能、行業和地區分類,2026-2034 年

虛擬資料室市場規模、佔有率、趨勢和預測:按組件、部署類型、企業規模、業務功能、行業和地區分類,2026-2034 年 虛擬資料室市場分析及預測(至2035年):按類型、產品、服務、技術、組件、應用、部署、最終用戶、解決方案和模式分類

虛擬資料室市場分析及預測(至2035年):按類型、產品、服務、技術、組件、應用、部署、最終用戶、解決方案和模式分類 全球虛擬資料室市場規模、佔有率、趨勢和成長分析報告(2026-2034年)日本虛擬資料室市場報告:按組件、部署類型、公司規模、業務功能、產業和地區分類(2026-2034 年)全球虛擬資料室市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的分析以及未來預測(2026-2034 年)

全球虛擬資料室市場規模、佔有率、趨勢和成長分析報告(2026-2034年)日本虛擬資料室市場報告:按組件、部署類型、公司規模、業務功能、產業和地區分類(2026-2034 年)全球虛擬資料室市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的分析以及未來預測(2026-2034 年) 虛擬資料室市場規模、佔有率和成長分析(按組件、組織規模、部署類型和地區分類)-2026-2033年產業預測

虛擬資料室市場規模、佔有率和成長分析(按組件、組織規模、部署類型和地區分類)-2026-2033年產業預測 2032 年安全協作資料無塵室市場預測:按類型、組件、部署模式、企業規模、應用、最終用戶和地區進行的全球分析

2032 年安全協作資料無塵室市場預測:按類型、組件、部署模式、企業規模、應用、最終用戶和地區進行的全球分析 虛擬資料室市場-全球產業規模、佔有率、趨勢、機會和預測,按應用程式、按部署類型、按最終用戶、按地區和競爭細分,2020-2030 年預測

虛擬資料室市場-全球產業規模、佔有率、趨勢、機會和預測,按應用程式、按部署類型、按最終用戶、按地區和競爭細分,2020-2030 年預測