|

市場調查報告書

商品編碼

1850958

雲端託管服務:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)Cloud Managed Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

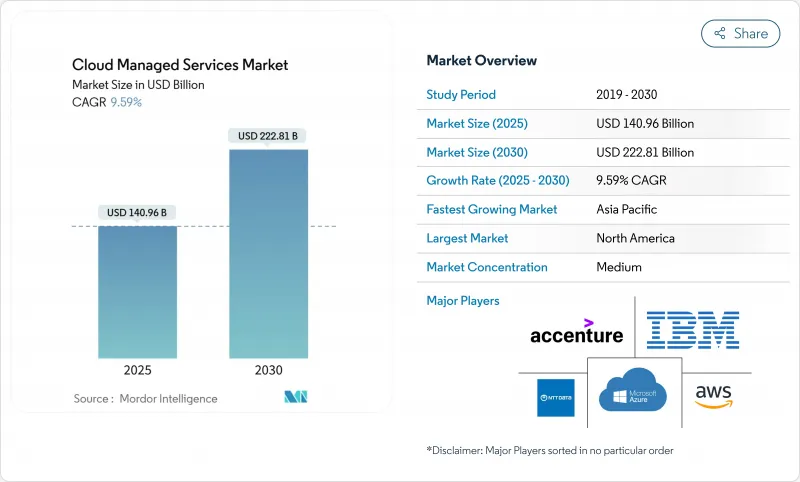

預計到 2025 年,雲端託管服務市場規模將達到 1,409.6 億美元,到 2030 年將成長至 2,228.1 億美元。

企業正持續從資產密集型基礎設施所有權模式轉型為按需付費的計量收費模式,以提高敏捷性、創造現金流並縮短創新週期。隨著多重雲端的蔓延和網路安全威脅給企業內部IT團隊帶來壓力,需求激增。金融服務業的數位轉型、人工智慧主導的工作負載以及永續性目標,都推動了對專業外部管理的需求。雖然北美佔據了大部分支出,但亞太地區憑藉其尚未開發的市場基礎和支持雲端運算的政策環境,成為成長最快的地區。競爭的焦點日益集中在自動化、合規深度和垂直行業專業知識上,而非簡單的成本套利。

全球雲端託管服務市場趨勢與洞察

金融服務業數位優先外包

銀行和保險公司如今正將託管雲端服務置於其現代化藍圖的核心位置。 2024年4月,塔塔諮詢服務公司(Tata Consultancy Services)擴大了與AWS的合作,承諾培訓25,000名工程師,使其掌握銀行級雲端現代化模式。金融機構認為,與外部合作夥伴攜手是實現生成式人工智慧、自動化合規檢查和縮短產品發布週期的唯一可行途徑。混合架構使下一代核心系統能夠與傳統平台共存,進而降低營運風險。改善客戶體驗是亞太地區銀行的首要任務,其雲端現代化預算撥款已超過成本節約目標。

企業中多重雲端和混合雲複雜性的快速成長

混合雲端和多重雲端部署已成為主流,但鮮有企業能夠真正掌握內部跨平台編配。 VMware 的一份報告顯示,93% 的客戶計劃長期維護混合架構。 Nutanix 的研究表明,到 2024 年,95% 的企業將在不同雲端平台之間遷移應用程式,以提高安全性並加速創新。因此,能夠提供跨雲端統一可視性、自動化工作負載部署和成本管治的合作夥伴需求激增。

對資料外洩和不斷演變的威脅的持續擔憂

英國一項調查發現,儘管許多中小企業承認雲端遷移具有靈活性和成本效益,但由於擔心安全漏洞,他們仍在推遲雲端遷移。合規性審核和客戶信任度令他們倍感壓力,導致他們與那些無法提供嚴格認證和事件回應指標的供應商簽訂了冗長的合約。

細分市場分析

託管基礎設施服務將繼續為資源配置奠定基礎,預計到 2024 年將佔總收入的 37.5%。然而,隨著企業優先考慮持續威脅調查、零信任實施和合規性報告,託管安全服務將以 10.7% 的複合年成長率加速成長。這將使託管安全市場的規模超過大多數其他細分市場。人工智慧驅動的安全營運中心(例如 Viking Cloud 的平台,該平台每天分析數十億個事件)透過縮短停留時間和自動化關聯分析,增強了服務提供者的優勢。網路、應用、備份和災難復原服務仍然強勁,推動著複雜的現代化計劃和傳統系統支援。

隨著供應商將安全性與基礎設施和網路監控捆綁在一起,他們創建了整合平台,從而推高了切換成本。企業買家更重視獨立解決方案中那些突出的功能,例如統一的儀錶板、一致的服務等級協定 (SLA) 以及跨多重雲端環境的單一管治平台。

公共雲端選項在超大規模可用區和豐富的原生工具的推動下,預計到 2024 年將保持 52% 的市場佔有率。然而,隨著客戶尋求延遲控制、資料駐留和成本最佳化等優勢,混合模式正以 11.5% 的複合年成長率加速成長。野村綜合研究所利用 AWS Outposts 使一家日本銀行能夠在當地運行 AWS 服務,從而滿足其主權監管要求。 Equinix 日本與Sakura Internet的夥伴關係展示如何將託管和支援 GPU 的 AI 工作負載服務與公共經濟效益和私人控制相結合。私有雲端的成長仍然較為溫和,主要局限於超低延遲和特定的監管用例。

託管服務供應商現在透過提供一致的策略引擎、成本儀表板以及跨公共、私有和邊緣環境的可觀測性來脫穎而出,而對執行時間和資料位置有嚴格要求的客戶也越來越將供應商對混合整合的熟悉程度作為購買的先決條件。

雲端託管服務市場按服務類型(託管基礎設施服務、託管網路服務等)、部署類型(公共雲端、私有雲端、混合雲端)、公司規模(大型企業、中小企業)、最終用戶行業(銀行、金融服務和保險 (BFSI)、IT 和電信、零售和電子商務等)以及地區進行細分。市場預測以美元計價。

區域分析

北美仍將是最大的消費地區,預計到2024年將佔據雲端託管服務市場37.3%的佔有率。早期採用、成熟的合作夥伴生態系統以及活躍的創業融資環境,都支撐著對最佳化、人工智慧營運和合規自動化的需求。美國企業傾向於基於結果的契約,而加拿大企業則利用跨境地理接近性來增強兩地之間的業務彈性。墨西哥製造商正在整合託管邊緣閘道器,以支援其工業4.0專案。

到2030年,亞太地區將以9.3%的複合年成長率實現最快增速,這主要得益於各國政府津貼數位化的補貼以及寬頻接入的普及。華為雲端的合作夥伴網路現已覆蓋超過45,000家企業,並提供12,000個市場平台。印度IT巨頭正在對其傳統系統進行現代化改造,以服務出口至全球。韓國的5G骨幹網路將加速邊緣密集的工作負載部署。澳洲的地理位置相對封閉,因此對能夠與全球資源無縫互聯的本地管理節點的需求日益成長,OpenText公司正大力投資該領域,直至2025年。

歐洲複雜的監管體系促使服務提供者在資料駐留和永續性認證方面進行差異化競爭。德國中型製造商利用託管服務推進工業4.0,而法國和義大利則在國家人工智慧戰略的推動下加大對公共雲端的投資。英國金融機構委託部署統一威脅管理套件以滿足審慎監理局(PRA)的要求。該地區的綠色交易和永續消費品監管指令(CSRD)的報告機制抑制了對缺乏透明排放指標的服務提供者的需求。微軟承諾使用100%可再生能源為其資料中心供電,這項承諾影響了採購決策。

南美洲和中東及非洲是新興但充滿希望的地區,託管服務可以繞過有限的本地基礎設施。 Expereo 指出,企業正在增加對 SD-WAN 和 SASE 的投入,以便在地理位置分散的營運中提供一致的應用程式效能。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 金融服務業的數位優先計畫加速了託管雲端外包

- 企業中多重雲端和混合雲複雜性的爆炸性成長

- 網路風險和合規性日益成長,需要全天候的安全管理。

- 資訊長預算面臨的成本最佳化壓力(營運支出與資本支出)

- FinOps 的採用對持續的雲端成本管治提出了新的要求。

- 永續性和綠色雲端指令改變了供應商的選擇

- 市場限制

- 資料外洩的擔憂依然存在,威脅情況也在不斷變化。

- 供應商鎖定風險會延緩大規模工作負載遷移。

- 全球認證雲端架構師短缺

- 資料主權法律的碎片化增加了合規成本。

- 價值/供應鏈分析

- 監管環境

- 技術展望(邊緣運算、5G、人工智慧運維)

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 按服務類型

- 託管基礎設施服務

- 主機服務

- 資安管理服務

- 託管應用程式服務

- 其他服務類型

- 按部署模式

- 公共雲端

- 私有雲端

- 混合雲端

- 按公司規模

- 主要企業

- 小型企業

- 按最終用戶行業分類

- BFSI

- 資訊科技和通訊

- 零售與電子商務

- 醫療保健和生命科學

- 製造業

- 政府和公共部門

- 其他最終用戶

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 亞太其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 南非

- 其他中東和非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Amazon Web Services(AWS)

- Microsoft Corp.(Azure Managed Services)

- International Business Machines Corp.(IBM)

- Accenture plc

- Cisco Systems, Inc.

- Huawei Technologies Co., Ltd.

- Ericsson

- Fujitsu Ltd.

- NEC Corp.

- NTT DATA Corp.

- DXC Technology Co.

- Lumen Technologies, Inc.

- Rackspace Technology, Inc.

- Tata Consultancy Services Ltd.

- Wipro Ltd.

- HCLTech

- Capgemini SE

- Cognizant Technology Solutions

- Infosys Ltd.

- Atos SE

第7章 市場機會與未來展望

The cloud managed services market size reaches USD 140.96 billion in 2025 and is set to grow to USD 222.81 billion by 2030, reflecting a 9.59% CAGR.

Enterprises continue moving from asset-heavy infrastructure ownership to pay-as-you-go operating models that improve agility, free cash and shorten innovation cycles. Demand rises sharply as multi-cloud sprawl and cybersecurity threats strain in-house IT teams. Financial-services digital mandates, AI-driven workloads and sustainability targets intensify the need for expert external management. North America holds the lion's share of spending, yet Asia Pacific's large untapped base and pro-cloud policy environment make it the fastest-expanding region. Competition increasingly revolves around automation, compliance depth and vertical expertise rather than simple cost arbitrage.

Global Cloud Managed Services Market Trends and Insights

BFSI Digital-First Mandates Intensify Outsourcing

Banks and insurers now place managed cloud services at the core of their modernization roadmaps. In April 2024 Tata Consultancy Services expanded its AWS alliance, pledging to train 25,000 engineers on bank-grade cloud modernization patterns. Institutions view external partners as the only realistic route to embed generative-AI, automate compliance checks and shorten product release cycles. Hybrid set-ups allow next-generation core systems to coexist with legacy platforms, lowering operational risk. Asia-Pacific banks stand out: budget allocations for cloud modernization now outweigh cost-cutting targets as customer-experience gains become paramount.

Surge in Multi-Cloud and Hybrid Complexity Among Enterprises

Hybrid and multi-cloud adoption has become mainstream, yet few firms can master cross-platform orchestration internally. VMware reports that 93% of its customers intend to keep hybrid architectures long term.Nutanix finds that 95% of enterprises shifted applications between clouds in 2024 to improve security or speed innovation. The result is a booming need for partners who deliver unified visibility, automated workload placement, and cost governance across cloud estates.

Persistent Data-Breach Anxiety and Evolving Threat Landscape

UK research shows many SMEs still delay cloud migration because of perceived security gaps, even though they acknowledge benefits in flexibility and cost. Compliance audits and customer trust weigh heavily, lengthening deal cycles for providers that cannot produce rigorous certifications and incident-response metrics.

Other drivers and restraints analyzed in the detailed report include:

- Heightened Cyber-Risk and Compliance Push 24/7 Managed Security

- Cost-Optimization Pressure on CIO Budgets (Op-Ex vs Cap-Ex)

- Vendor Lock-In Risks Slow Large-Scale Workload Migration

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Managed infrastructure services continue to deliver foundational provisioning, capturing 37.5% of 2024 revenue. Yet managed security services grow faster at 10.7% CAGR as firms prioritize continuous threat hunting, zero-trust enforcement and compliance reporting. The cloud managed services market size for managed security will therefore outpace most other segments. AI-driven security operations centers, such as VikingCloud's platform that analyzes billions of events daily, strengthen provider advantage by shortening dwell time and automating correlation. Network, application, backup and disaster-recovery services remain steady, channeling complex modernization projects and legacy support.

Second-order effects ripple across the cloud managed services industry as providers bundle security with infrastructure and network oversight, creating integrated platforms that raise switching costs. Enterprise buyers value unified dashboards, consistent SLAs and single-pane governance across multi-cloud estates features that independent point solutions struggle to match.

The public-cloud option retains 52% cloud managed services market share in 2024, anchored by hyperscale availability zones and rich native tooling. The hybrid model, however, accelerates at 11.5% CAGR as clients seek latency control, data residency and cost optimization advantages. Use of AWS Outposts by Nomura Research Institute lets Japanese banks run AWS services on-premises to satisfy sovereignty rules. Equinix Japan's partnership with Sakura Internet illustrates how co-location and GPU-ready services blend public economics with private control for AI workloads. Private-cloud growth remains modest, reserved for ultra-low-latency or niche regulatory cases.

Managed-service vendors now differentiate by offering consistent policy engines, cost dashboards and observability across public, private and edge footprints. Clients with strict uptime or data-location mandates increasingly treat provider proficiency in hybrid integration as a purchase prerequisite.

Cloud Managed Services Market is Segmented by Service Type (Managed Infrastructure Services, Managed Network Services, and More), Deployment Type (Public Cloud, Private Cloud, Hybrid Cloud), Enterprise Size (Large Enterprise and SMEs), End User Industry (BFSI, IT and Telecom, Retail and E-Commerce, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America remains the largest spender, retaining 37.3% share of the cloud managed services market in 2024. Early adoption, mature partner ecosystems and a robust venture funding scene sustain demand for optimization, AI operations and compliance automation. US enterprises favor outcome-based contracts, while Canadian firms leverage cross-border proximity for dual-region resilience. Mexican manufacturers integrate managed edge gateways to underpin Industry 4.0 programs.

Asia Pacific records the fastest 9.3% CAGR through 2030 as governments subsidize digitization and broadband access widens. Huawei Cloud's partner network now counts more than 45,000 firms and 12,000 marketplace offers, linking finance, telecom and AI start-ups across the region. India's IT majors revamp legacy estates for global service exports. Japan's high trust threshold spurs demand for hybrid setups backed by local data centers, while South Korea's 5G backbone accelerates edge-heavy workloads. Australia's isolation intensifies calls for local managed nodes that interconnect seamlessly with global resources, an area where OpenText is investing heavily in 2025.

Europe's regulatory mosaic drives provider differentiation on data-residency and sustainability credentials. Germany's Mittelstand manufacturers tap managed services for Industrie 4.0, while French and Italian public-cloud spend rises under national AI strategies. UK financial institutions commission integrated threat-management suites to align with PRA expectations. The region's Green Deal and CSRD reporting dampen demand for providers without transparent emissions metrics; Microsoft's pledge to power data centers with 100% renewable energy influences sourcing decisions.

South America and the Middle East and Africa represent nascent yet high-potential territories where managed services circumvent limited local infrastructure. Expereo notes businesses boosting spending on SD-WAN and SASE to deliver consistent application performance across geographically dispersed operations.

- Amazon Web Services (AWS)

- Microsoft Corp. (Azure Managed Services)

- International Business Machines Corp. (IBM)

- Accenture plc

- Cisco Systems, Inc.

- Huawei Technologies Co., Ltd.

- Ericsson

- Fujitsu Ltd.

- NEC Corp.

- NTT DATA Corp.

- DXC Technology Co.

- Lumen Technologies, Inc.

- Rackspace Technology, Inc.

- Tata Consultancy Services Ltd.

- Wipro Ltd.

- HCLTech

- Capgemini SE

- Cognizant Technology Solutions

- Infosys Ltd.

- Atos SE

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 BFSI digital-first initiatives accelerate managed-cloud outsourcing

- 4.2.2 Surge in multi-cloud and hybrid complexity among enterprises

- 4.2.3 Heightened cyber-risk and compliance push 24/7 managed security

- 4.2.4 Cost-optimization pressure on CIO budgets (Op-Ex vs Cap-Ex)

- 4.2.5 FinOps adoption creates new demand for continuous cloud cost governance

- 4.2.6 Sustainability and green-cloud mandates reshape provider selection

- 4.3 Market Restraints

- 4.3.1 Persistent data-breach anxiety and evolving threat landscape

- 4.3.2 Vendor lock-in risks slow large-scale workload migration

- 4.3.3 Global shortage of certified cloud-architect talent

- 4.3.4 Fragmented data-sovereignty laws inflate compliance cost

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook (Edge, 5G, Gen-AI Ops)

- 4.7 Porters Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Managed Infrastructure Services

- 5.1.2 Managed Network Services

- 5.1.3 Managed Security Services

- 5.1.4 Managed Application Services

- 5.1.5 Other Service Type

- 5.2 By Deployment Model

- 5.2.1 Public Cloud

- 5.2.2 Private Cloud

- 5.2.3 Hybrid Cloud

- 5.3 By Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises (SMEs)

- 5.4 By End-User Industry

- 5.4.1 BFSI

- 5.4.2 IT and Telecom

- 5.4.3 Retail and E-Commerce

- 5.4.4 Healthcare and Life Sciences

- 5.4.5 Manufacturing

- 5.4.6 Government and Public Sector

- 5.4.7 Other End-Users

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 South Africa

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Amazon Web Services (AWS)

- 6.4.2 Microsoft Corp. (Azure Managed Services)

- 6.4.3 International Business Machines Corp. (IBM)

- 6.4.4 Accenture plc

- 6.4.5 Cisco Systems, Inc.

- 6.4.6 Huawei Technologies Co., Ltd.

- 6.4.7 Ericsson

- 6.4.8 Fujitsu Ltd.

- 6.4.9 NEC Corp.

- 6.4.10 NTT DATA Corp.

- 6.4.11 DXC Technology Co.

- 6.4.12 Lumen Technologies, Inc.

- 6.4.13 Rackspace Technology, Inc.

- 6.4.14 Tata Consultancy Services Ltd.

- 6.4.15 Wipro Ltd.

- 6.4.16 HCLTech

- 6.4.17 Capgemini SE

- 6.4.18 Cognizant Technology Solutions

- 6.4.19 Infosys Ltd.

- 6.4.20 Atos SE

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

雲端管理服務市場:依服務類型、平台、組織規模和最終用戶分類-2026-2032年全球市場預測雲端管理網路市場:依部署類型、元件、解決方案類型、組織規模和產業分類-2026-2032年全球市場預測

雲端管理服務市場:依服務類型、平台、組織規模和最終用戶分類-2026-2032年全球市場預測雲端管理網路市場:依部署類型、元件、解決方案類型、組織規模和產業分類-2026-2032年全球市場預測 AWS託管服務全球市場報告(2026年)2026年全球雲端託管服務市場報告

AWS託管服務全球市場報告(2026年)2026年全球雲端託管服務市場報告 雲端託管服務市場分析及預測(至 2035 年):按類型、產品、服務、技術、組件、應用、部署、最終用戶和解決方案分類

雲端託管服務市場分析及預測(至 2035 年):按類型、產品、服務、技術、組件、應用、部署、最終用戶和解決方案分類 全球雲端管理網路市場規模、佔有率、趨勢和成長分析報告(2026-2034)全球雲端託管服務市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球雲端管理網路市場規模、佔有率、趨勢和成長分析報告(2026-2034)全球雲端託管服務市場規模、佔有率、趨勢和成長分析報告(2026-2034) 雲端管理服務市場規模、佔有率、趨勢和預測(按服務類型、部署模式、組織規模、行業垂直領域和地區分類),2026-2034 年

雲端管理服務市場規模、佔有率、趨勢和預測(按服務類型、部署模式、組織規模、行業垂直領域和地區分類),2026-2034 年 雲端管理局域網路市場 - 全球產業規模、佔有率、趨勢、機會及預測(按解決方案、服務、公司規模、產業、地區和競爭格局分類),2021-2031年日本雲端管理服務市場報告:依服務類型、部署模式、組織規模、產業及地區分類,2026-2034年

雲端管理局域網路市場 - 全球產業規模、佔有率、趨勢、機會及預測(按解決方案、服務、公司規模、產業、地區和競爭格局分類),2021-2031年日本雲端管理服務市場報告:依服務類型、部署模式、組織規模、產業及地區分類,2026-2034年