|

市場調查報告書

商品編碼

1850401

GDPR 服務:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)GDPR Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

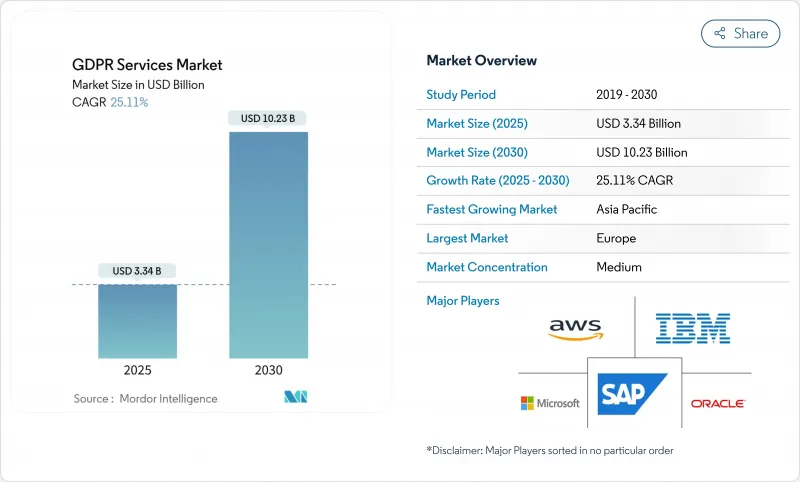

GDPR 服務市場預計到 2025 年將達到 33.4 億美元,到 2030 年將達到 102.3 億美元,年複合成長率為 25.1%。

這一成長軌跡反映出,在歐洲資料保護機構於2024年處以12億歐元罰款之後,企業正從規避處罰轉向積極主動實施隱私權保護計畫。英國脫歐後跨境資料傳輸激增,以及美國和歐盟資料隱私框架的實施,擴大了合規差距,供應商正透過自動化發現引擎和隱私設計藍圖來應對這些差距。雲端運算的活性化、人工智慧驅動的資料映射工具的廣泛應用,以及金融和能源產業監管力度的加強,將進一步推動對端到端管治平台的需求。目前市場競爭依然適中,主要軟體供應商正在整契約意管理、資料分類和持續監控等功能,而全球顧問公司也在擴展其託管服務組合,以應對認證隱私官持續短缺的問題。

全球 GDPR 服務市場趨勢與洞察

GDPR罰款不斷攀升,促使企業加大合規支出。

2024年,歐洲監管機構從廣泛的宣傳宣傳活動轉向策略性的高額罰款,儘管違規案件數量不多,但罰款總額仍高達12億歐元。一些引人注目的案例,例如LinkedIn被罰款3.1億歐元,顯示監管機構願意全面執行4%的收入上限,並促使企業建立全面的合規架構,而不是僅依賴最低限度的控制措施。金融服務、能源和通訊業者現在面臨著與社群媒體供應商長期以來所受到的同等審查,這擴大了專業供應商的潛在市場。董事會擴大將負責人薪酬與隱私指標掛鉤,資料保護工具和諮詢支援的預算也不斷增加。隨著企業逐漸摒棄形式主義的審計,轉向持續合規審核,能夠量化風險降低並整合持續監控的供應商將更受青睞。

英國脫歐後跨境資料流動激增以及歐盟-美國資料隱私框架

2024年充分性決定的實施將增加資料傳輸的數量和複雜性。英國公司目前正同時應對英國GDPR和歐盟法規。標準合約條款的應用仍然存在不一致之處,迫使企業尋求能夠自動進行資料傳輸影響評估並產生即時文件的平台。由於跨國公司需要統一的儀錶板來管理具有約束力的公司規則、認證機制和持續更新的風險登記冊,因此,兼具法律專業知識和技術整合能力的服務供應商正日益受到青睞。

認證資料保護官技能持續短缺

第37條規定的資料保護官(DPO)需求成長速度超過了可用資源,促使監管機構對未指定DPO的公共機構處以罰款。託管式DPO即服務(Managed DPO-as-a-Service)透過融合法律解釋和技術監督來彌補這一缺口。擁有跨多個司法管轄區資格的服務提供者需要能夠擴展到各個子公司的承包專業技術支持,因此收取更高的費用。

細分市場分析

到2024年,本地部署將佔總營收的68.7%,這顯示在GDPR服務市場規模下,企業對直接資料管理的需求依然強勁。然而,採用模式揭示了結構性遷移路徑:企業優先考慮將私有雲端節點用於受監管的工作負載,並將敏感度較低的分析外包給SaaS服務。這種轉變得益於加密等突破性技術的運用,包括用於保護處理中資料的機密運算。資料駐留規則正在指南架構選擇。泛歐企業正在將儲存叢集本地化,並透過安全的API網路關聯合查詢。供應商藍圖現在將經過驗證的硬體隔離區與策略主導的金鑰託管相結合,使合規團隊無需進行客製化的程式碼審查即可檢驗技術保障措施。

以雲端為中心的產品正以 27.0% 的複合年成長率成長。與基礎設施即代碼 (IaC) 管道的整合意味著隱私控制與網路和應用程式狀態一起被編碼,從而將審核週期從數週縮短至數小時。混合模式支援運行時策略決策。個人資料可以在國家/地區執行,但聚合的遙測資料會傳輸到全球儀表板。隨著客戶對保障的要求越來越高,服務提供者正在發布加密認證報告,並接受經認證機構的遠端檢測。這種透明度正在再形成採購清單,並增強更廣泛的 GDPR 服務市場中雲端採用的勢頭。

涵蓋發現、管治和授權模組的解決方案平台將在2024年佔支出的58.6%,隨著企業面臨實施複雜性的挑戰,服務收入將以26.3%的複合年成長率快速成長。自動化數據映射引擎可抓取Petabyte級混合環境,標準化元資料,並提供支援風險評分的集中式清單。許可編配節點取代了傳統的僅橫幅機制,可將細微的偏好傳達給網站、行動應用程式和連網裝置。多租戶API有助於與票務、SIEM和資料倉儲工具整合,從而在企業指揮中心提供隱私指標的可見性。

諮詢、合規管理以及資料保護官即服務 (DPOaaS) 合約正在創造越來越穩定的收入來源。對持續控制測試和符合監管機構要求的儀錶板的需求,正將一次性審核轉變為持續性項目。服務提供者正在為金融、醫療保健和零售等行業開發行業專屬模板,以加快客戶入駐流程,同時融入監管方面的細微差別。人工智慧主導的行動指南提案補救措施、自動產生資料保護影響評估 (DPIA),並監控因資料轉移影響而導致的偏差。這些功能使 GDPR 服務市場能夠很好地適應監管機構從一次性執法轉向持續監管的趨勢。 GDPR 服務業正處於成熟階段,這主要得益於本節中提到的三種服務的出現:

GDPR 服務市場報告按部署類型(本地部署、雲端部署)、交付模式(解決方案、服務)、組織規模(大型企業、中小企業)、最終用戶(銀行、金融服務、保險 (BFSI)、通訊、IT 等)和地區進行細分。

區域分析

歐洲是需求中心,佔2024年收入的38.5%,這得益於監管機構開展協調一致的調查、發布詳細指南並提高合規預期。各國主管機關正日益實施結構性補救措施,迫使資料控制者重組處理流程。總部位於歐盟的跨國公司正在採用廣泛地區的隱私營運模式,利用集中式資料保護官中心和統一的工具,以多種語言處理資料主體請求。歐洲資料保護委員會的年度行動計畫列出了人工智慧訓練資料、兒童隱私和跨境資料傳輸等主題優先事項,確保為服務供應商提供持續的改進計劃。

在北美,諸如《加州消費者隱私法案》(CCPA)和《弗吉尼亞州消費者資料保護法案》 (維吉尼亞 CDPA)等州級法規,以及即將訂定的聯邦立法,都在不斷擴大其適用範圍並保持強勁成長。同時在歐盟和美國市場營運的美國公司正在推行單一框架策略,以減少重疊,並將互通平台作為一項關鍵的採購標準。加拿大的C-27法案和更新後的產業法規也強化了對統一隱私架構的必要性。雲端超大規模企業正在部署區域資料中心和自主雲端平台,以滿足在地化需求,而託管服務諮詢公司則致力於彌合不同司法管轄區之間的法規解釋差異。

亞太地區以25.7%的複合年成長率成為成長最快的地區,這主要得益於印度《數位個人資料保護法》、中國《個人資訊保護法》以及日本和新加坡的相關修正案與歐盟原則的一致性。當地監管機構正在發布產業通知,要求供應商進行類似GDPR第28條的審核和風險評估,尤其是在金融科技、數位醫療和智慧城市部署領域。各公司正在全部區域部署資料映射程序,以應對不同的違規通知時限和同意模式。熟悉當地語言和法律文化的供應商正在蓬勃發展,跨境資料導出評估正成為標準服務模組。南美和中東的發展軌跡與之類似,它們將歐盟的相關要素融入本國國情,從而將GDPR服務市場的地理範圍擴展到新的地區。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- GDPR罰款不斷上漲將推動企業加強合規支出。

- 英國脫歐後跨境資料流動激增以及歐盟-美國資料隱私框架

- 快速實現雲端優先遷移需要以隱私為核心設計架構。

- 資料外洩事件日益頻繁,推動了對專業合規服務的需求。

- 將隱私工程融入您的 DevSecOps 流程

- 引入人工智慧驅動的發現工具,自動繪製個人數據

- 市場限制

- 認證資料保護官的技能缺口非常大。

- 中小企業的合規成本很高。

- 分散且無法互通性的供應商解決方案增加了整合複雜性。

- 各國執法實務的差異造成了監管上的不確定性。

- 價值鏈分析

- 監管環境

- 技術展望

- 波特五力分析

- 買方的議價能力

- 供應商的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 評估宏觀經濟趨勢對市場的影響

第5章 市場規模與成長預測

- 依部署類型

- 本地部署

- 雲

- 公共雲端

- 私有雲端

- 混合雲端

- 報價

- 解決方案

- 數據發現與映射

- 資料管治

- 同意/設定管理

- API和整合管理

- 風險評估與資料保護影響評估工具

- 服務

- 諮詢顧問

- 整合與實施

- DPO-as-a-Service

- 託管合規服務

- 解決方案

- 按組織規模

- 主要企業

- 小型企業

- 最終用戶

- 銀行、金融服務和保險(BFSI)

- 通訊/IT

- 零售和消費品

- 醫療保健和生命科學

- 製造業

- 政府和公共部門

- 其他行業

- 地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲和紐西蘭

- 亞太其他地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- IBM Corporation

- Microsoft Corporation

- SAP SE

- Oracle Corporation

- Amazon Web Services Inc.

- Veritas Technologies LLC

- Micro Focus International plc

- Capgemini SE

- SecureWorks Inc.

- Wipro Limited

- DXC Technology Company

- Accenture plc

- Atos SE

- Tata Consultancy Services Ltd

- Larsen and Toubro Infotech Ltd

- Infosys Ltd

- OneTrust LLC

- TrustArc Inc.

- Deloitte Touche Tohmatsu Ltd

- PricewaterhouseCoopers International Ltd

- KPMG International Ltd

第7章 市場機會與未來展望

The GDPR services market size was valued at USD 3.34 billion in 2025 and is forecast to reach USD 10.23 billion by 2030, advancing at a 25.1% CAGR.

The growth trajectory reflects enterprises shifting from penalty-avoidance to proactive privacy programs as European data-protection authorities levied EUR 1.2 billion in fines during 2024. Heightened cross-border data transfers following Brexit, along with the EU-U.S. Data Privacy Framework, opened compliance gaps that vendors address with automated discovery engines and privacy-by-design blueprints. Rising cloud adoption, the surge of AI-powered data-mapping tools, and expanding sectoral oversight in finance and energy further accelerate demand for end-to-end governance platforms. Competitive intensity remains moderate; leading software providers integrate consent management, data classification, and continuous monitoring, while global consultancies expand managed-service portfolios to meet the persistent shortage of certified privacy officers.

Global GDPR Services Market Trends and Insights

Escalating GDPR Fine Values Spur Proactive Compliance Spending

European regulators moved from broad awareness campaigns to strategic high-value penalties in 2024, imposing EUR 1.2 billion in total fines despite a lower case count. High-profile actions-such as LinkedIn's EUR 310 million penalty-demonstrated a willingness to apply the full 4% revenue ceiling, motivating enterprises to build holistic compliance architectures rather than rely on minimal controls. Financial services, energy, and telecom operators now face the same scrutiny long applied to social-media providers, expanding the addressable market for specialist vendors. Boards increasingly tie executive compensation to privacy metrics, driving larger budgets for data-protection tooling and advisory support. Vendors that can quantify risk reduction and integrate continuous monitoring win favor as organizations abandon checkbox audits for living compliance programs.

Surge in Cross-Border Data Flows Post-Brexit and EU-U.S. Data Privacy Framework

Operationalization of the adequacy decision in 2024 increased data-transfer volumes and complexity; UK firms now juggle UK-GDPR and EU rules concurrently. Standard Contractual Clauses remain inconsistently applied, compelling businesses to seek platforms that automate transfer-impact assessments and produce real-time documentation. Service providers that blend legal expertise with technical integration capabilities gain traction as multinationals require unified dashboards for Binding Corporate Rules, certification mechanisms, and continuously updated risk registers.

Persistent Skills Gap in Certified Data Protection Officers

Article 37's DPO mandate outstrips available talent, prompting regulators to fine even public bodies for non-designation. Managed DPO-as-a-Service offerings fill the void, blending legal interpretation with technical oversight. Providers holding multi-jurisdictional credentials command premium fees as firms seek turnkey expertise that scales across subsidiaries.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Cloud-First Migrations Requiring Privacy-by-Design Architectures

- Heightened Frequency of Data Breaches Drives Demand for Specialized Compliance Services

- High Compliance Cost Burden on SMEs and Micro-Firms

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

On-premises implementations retained 68.7% revenue in 2024, illustrating continuing appetite for direct data control within the GDPR services market size. Adoption patterns, however, reveal a structural migration path: organizations prioritize private-cloud nodes for regulated workloads while outsourcing less-sensitive analytics to SaaS. The shift is powered by encryption-in-use breakthroughs such as confidential computing, which keep data protected during processing. Data residency rules guide architecture choices; pan-European firms localize storage clusters, then federate queries through secure API gateways. Vendor roadmaps now bundle attested hardware enclaves with policy-driven key escrow, enabling compliance teams to validate technical safeguards without bespoke code reviews.

Cloud-centric offerings record a 27.0% CAGR as boards equate elasticity with resilience. Integration with infrastructure-as-code pipelines means privacy controls are codified alongside network and application states, reducing audit cycles from weeks to hours. Hybrid models allow runtime policy decisions: personal data may execute in a national zone, while aggregated telemetry feeds global dashboards. As customers demand assurances, providers publish cryptographic attestation reports and undergo independent GDPR readiness audits performed by accredited bodies. This transparency is reshaping procurement checklists and reinforcing cloud adoption momentum within the broader GDPR services market.

Solutions platforms-spanning discovery, governance, and consent modules-accounted for 58.6% of spending in 2024, yet services revenue is growing faster at 26.3% CAGR as enterprises confront implementation intricacies. Automated data-mapping engines crawl petabyte-scale hybrid estates, normalize metadata, and feed centralized inventories that underpin risk scoring. Consent orchestration nodes propagate granular preferences across websites, mobile apps, and connected devices, replacing legacy banner-only mechanics. Multi-tenant APIs facilitate integration with ticketing, SIEM, and data warehouse tools, making privacy metrics visible in enterprise command centers.

Consulting, managed compliance, and DPO-as-a-Service engagements increasingly generate sticky annuities. Demand for continuous controls testing and regulator-ready dashboards turns point-in-time audits into rolling programs. Providers cultivate sector templates-finance, healthcare, retail-to expedite onboarding while embedding regulatory nuance. AI-driven playbooks propose remediation tasks, auto-generate DPIAs, and monitor for transfer-impact deviations. These capabilities ensure the GDPR services market stays aligned with regulators' shift from episodic enforcement to ongoing oversight. Three appearances of the GDPR services industry across this subsection underline the segment's maturation trajectory.

The GDPR Services Market Report is Segmented by Type of Deployment (On-Premises and Cloud), Offering (solutions and Services), Organization Size (Large Enterprises and Small and Medium Enterprises (SMEs)), End User (Banking, Financial Services and Insurance (BFSI), Telecom and IT, and More), and Geography.

Geography Analysis

Europe anchors demand, holding 38.5% revenue in 2024 as regulators pursue coordinated investigations and publish granular guidance that elevates compliance expectations. National authorities increasingly impose structural remedies, compelling controllers to re-engineer processing flows, a factor that sustains platform investments across the GDPR services market. Multinationals with EU headquarters adopt pan-regional privacy operating models, leveraging centralized DPO hubs and harmonized tooling that handles multi-lingual data-subject requests. The European Data Protection Board's annual action plans set thematic enforcement priorities-AI training data, children's privacy, and cross-border transfers-ensuring a steady pipeline of remediation projects for service providers.

North America maintains robust growth as state-level regulations such as the California Consumer Privacy Act, Virginia CDPA, and forthcoming federal proposals broaden coverage. U.S. firms operating in both the EU and domestic markets pursue single-framework strategies to reduce duplication, making interoperable platforms critical procurement criteria. Canadian Bill C-27 and updated sectoral codes reinforce the need for unified privacy architecture. Cloud hyperscalers position regional data centers and sovereign cloud variants to satisfy localization demands, while managed-service consultancies bridge statutory interpretation across jurisdictions.

Asia-Pacific records the fastest CAGR at 25.7% as India's Digital Personal Data Protection Act, China's Personal Information Protection Law, and amendments in Japan and Singapore mirror EU principles. Local regulators issue sector notices-particularly in fintech, digital health, and smart-city deployments-requiring vendor audits and risk assessments reminiscent of GDPR Article 28. Enterprises deploy region-wide data-mapping programs to cope with divergent breach-notification clocks and consent models. Providers fluent in regional languages and legal cultures grow rapidly, and cross-border data-export assessments become standard service modules. South America and the Middle East follow a similar trajectory, adapting EU elements to domestic contexts, which extends the geographic footprint of the GDPR services market size into new territories.

- IBM Corporation

- Microsoft Corporation

- SAP SE

- Oracle Corporation

- Amazon Web Services Inc.

- Veritas Technologies LLC

- Micro Focus International plc

- Capgemini SE

- SecureWorks Inc.

- Wipro Limited

- DXC Technology Company

- Accenture plc

- Atos SE

- Tata Consultancy Services Ltd

- Larsen and Toubro Infotech Ltd

- Infosys Ltd

- OneTrust LLC

- TrustArc Inc.

- Deloitte Touche Tohmatsu Ltd

- PricewaterhouseCoopers International Ltd

- KPMG International Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Escalating GDPR fine values spur proactive compliance spending

- 4.2.2 Surge in cross-border data flows post-Brexit and EU-U.S. Data Privacy Framework

- 4.2.3 Rapid cloud-first migrations requiring privacy-by-design architectures

- 4.2.4 Heightened frequency of data breaches drives demand for specialized compliance services

- 4.2.5 Embedding privacy engineering inside DevSecOps pipelines

- 4.2.6 Adoption of AI-powered discovery tools that auto-map personal data

- 4.3 Market Restraints

- 4.3.1 Persistent skills gap in certified Data Protection Officers

- 4.3.2 High compliance cost burden on SMEs and micro-firms

- 4.3.3 Fragmented, non-interoperable vendor solutions inflate integration complexity

- 4.3.4 Divergent national enforcement practices causing regulatory uncertainty

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assessment of the Impact of Macroeconomic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type of Deployment

- 5.1.1 On-Premises

- 5.1.2 Cloud

- 5.1.2.1 Public Cloud

- 5.1.2.2 Private Cloud

- 5.1.2.3 Hybrid Cloud

- 5.2 By Offering

- 5.2.1 Solutions

- 5.2.1.1 Data Discovery and Mapping

- 5.2.1.2 Data Governance

- 5.2.1.3 Consent / Preference Management

- 5.2.1.4 API and Integration Management

- 5.2.1.5 Risk-Assessment and DPIA Tools

- 5.2.2 Services

- 5.2.2.1 Consulting and Advisory

- 5.2.2.2 Integration and Implementation

- 5.2.2.3 DPO-as-a-Service

- 5.2.2.4 Managed Compliance Services

- 5.2.1 Solutions

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises (SMEs)

- 5.4 By End User

- 5.4.1 Banking, Financial Services and Insurance (BFSI)

- 5.4.2 Telecom and IT

- 5.4.3 Retail and Consumer Goods

- 5.4.4 Healthcare and Life Sciences

- 5.4.5 Manufacturing

- 5.4.6 Government and Public Sector

- 5.4.7 Other Industries

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia and New Zealand

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 IBM Corporation

- 6.4.2 Microsoft Corporation

- 6.4.3 SAP SE

- 6.4.4 Oracle Corporation

- 6.4.5 Amazon Web Services Inc.

- 6.4.6 Veritas Technologies LLC

- 6.4.7 Micro Focus International plc

- 6.4.8 Capgemini SE

- 6.4.9 SecureWorks Inc.

- 6.4.10 Wipro Limited

- 6.4.11 DXC Technology Company

- 6.4.12 Accenture plc

- 6.4.13 Atos SE

- 6.4.14 Tata Consultancy Services Ltd

- 6.4.15 Larsen and Toubro Infotech Ltd

- 6.4.16 Infosys Ltd

- 6.4.17 OneTrust LLC

- 6.4.18 TrustArc Inc.

- 6.4.19 Deloitte Touche Tohmatsu Ltd

- 6.4.20 PricewaterhouseCoopers International Ltd

- 6.4.21 KPMG International Ltd

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

2025年全球GDPR服務市場報告

2025年全球GDPR服務市場報告 全球 GDPR 身分層市場:預測至 2032 年 - 按組件、部署類型、組織規模、最終用戶和地區進行分析

全球 GDPR 身分層市場:預測至 2032 年 - 按組件、部署類型、組織規模、最終用戶和地區進行分析 全球 GDPR 服務市場研究報告 - 產業分析、規模、佔有率、成長、趨勢及 2025 年至 2033 年預測

全球 GDPR 服務市場研究報告 - 產業分析、規模、佔有率、成長、趨勢及 2025 年至 2033 年預測 GDPR 服務市場報告(按產品、部署類型、組織規模、最終用戶和地區)2025 年至 2033 年

GDPR 服務市場報告(按產品、部署類型、組織規模、最終用戶和地區)2025 年至 2033 年 GDPR 服務市場 - 全球產業規模、佔有率、趨勢、機會和預測,細分,按部署模式、按產品、按組織規模、按最終用戶行業、按地區、按競爭,2019-2029F

GDPR 服務市場 - 全球產業規模、佔有率、趨勢、機會和預測,細分,按部署模式、按產品、按組織規模、按最終用戶行業、按地區、按競爭,2019-2029F GDPR 服務市場:按服務、組織規模和最終用戶分類 - 2025-2030 年全球預測GDPR合規服務的市場規模 - 按部署類型、提供的服務、組織規模和最終用戶 - 區域前景、競爭策略和細分市場預測(~2033年)

GDPR 服務市場:按服務、組織規模和最終用戶分類 - 2025-2030 年全球預測GDPR合規服務的市場規模 - 按部署類型、提供的服務、組織規模和最終用戶 - 區域前景、競爭策略和細分市場預測(~2033年)