|

市場調查報告書

商品編碼

1850368

資料管治:市場佔有率分析、產業趨勢、統計資料和成長預測(2025-2030 年)Data Governance - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

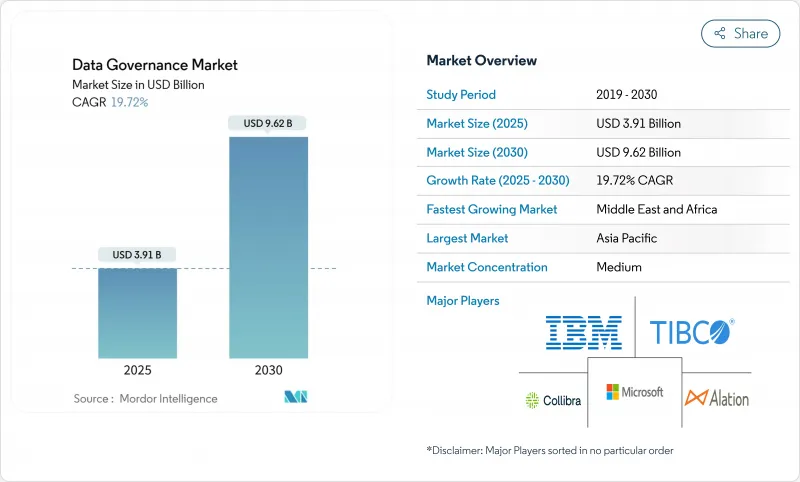

預計到 2025 年,資料管治市場規模將達到 39.1 億美元,到 2030 年將達到 96.2 億美元(複合年成長率 19.72%)。

推動這一成長的因素包括監管力度加大、雲端運算普及速度加快,以及人們日益認知到,良好的資料治理對於可信任人工智慧、即時支付和跨境商務至關重要。隨著資料外洩處罰加大以及經營模式向資料貨幣化轉型,金融機構、醫療服務提供者和製造商都在加大投資。供應商正在將人工智慧融入資料溯源和編目工具中,以實現分類任務的自動化,同時強調部署的靈活性,以支援主權雲端和混合架構。因此,資料管治市場正從以合規性為中心的單一解決方案演變為能夠編配分散式資料資產的品質、安全性和責任制的整合平台。

全球數據管治市場趨勢與洞察

歐盟人工智慧法和全球人工智慧監管呼籲建立可解釋的數據血緣關係

歐盟人工智慧法規將於2024年8月生效,該法規要求部署高風險人工智慧的公司記錄資料來源、轉換過程和品質指標。未能遵守該法規的公司可能面臨高達3,982萬美元(佔全球收入的7%)的罰款,這迫使公司實施複雜的血緣平台,以追蹤端到端的資料流。供應商正在將模型級元資料與傳統編目系統整合,使審核能夠追蹤訓練集並檢測偏差。跨國公司預計巴西和加拿大也將推出類似的法規,這將使合規成為全球性要求。這些壓力正在推動對能夠在單一管治工作空間中連接資料集、模型和業務成果的工具的需求。因此,資料管治市場正在轉向將人工智慧監管與傳統管理功能結合的解決方案。

FedNow 和即時支付軌道為北美銀行、金融服務和保險業 (BFSI) 提供亞毫秒級資料完整性保障

FedNow 服務於 2023 年 7 月運作,目前在參與銀行全天候運作。亞毫秒級的結算速度要求資料品質極高且血緣關係連續,以滿足洗錢防制檢查的要求,同時確保交易不會中斷。金融機構正在部署人工智慧驅動的篩檢和資料增強管道,以便即時發出異常警報。傳統的批次合規體系已無法滿足這些需求,因此銀行正在對元資料儲存庫進行現代化改造,並實現控制測試的自動化。這種趨勢推動了雲端原生管治供應商的訂閱收入成長,這些供應商可以將規則直接嵌入到結算工作流程中。同時,這也促進了旨在將血緣工具改造到大型主機核心系統的諮詢業務,從而在更廣泛的資料管治市場中創造了一個利潤豐厚的細分領域。

企業級資料處理歷程工具整體擁有成本高昂

一級銀行在部署企業級血緣平台方面舉步維艱,每年在許可、整合和硬體更新方面花費數百萬美元。阿爾託大學的一項研究發現,與舊有系統的整合以及缺乏標準導致專案工期和預算大幅膨脹。一些機構為了降低成本而採用手動映射,這延緩了平台的全面普及。儘管供應商推出了模組化定價和按需付費的雲端版本,但高昂的價格仍然是資料管治市場擴張的一大阻礙。

細分市場分析

到2024年,軟體解決方案將佔總收入的57.1%,其自動化策略執行、元資料擷取和血緣視覺化等功能將為資料管治市場提供支援。人工智慧分類和異常檢測如今已成為基礎功能,幫助企業即時遵守歐盟人工智慧法規和FedNow指令。隨著供應商將模型管治模組整合到人工智慧管道審核系統中,軟體資料管治市場規模預計將會擴大。

包括實施、培訓和維運在內的各項服務預計將以23.4%的複合年成長率成長。人才短缺和日益複雜的監管環境正促使企業將框架設計和日常管理外包。為了在分散的服務市場中脫穎而出,託管服務提供者正在透過增加資料品質和服務許可合規方面的服務等級協定(SLA)來提升自身競爭力。

服務成長也得益於業界特定的諮詢服務:銀行客戶需要符合BCBS 239標準的血緣加速器,醫療保健客戶則需要符合HIPAA標準的模板。這種垂直領域的客製化服務為精品諮詢公司和全球系統整合商創造了發展空間。因此,資料管治市場正持續從純粹的授權模式轉變為多種經常性收益源的模式。

由於金融服務和醫療保健公司堅持對敏感記錄進行在地化管理,預計到2024年,本地部署仍將保持53.6%的市場佔有率。儘管企業擴大轉向SaaS,但大型主機共存和受監管的工作負載仍然更傾向於資料中心。隨著雲端安全認證的普及,本地部署解決方案的資料管治市場佔有率預計將逐漸下降。

受雲端主權指令和遠距辦公規範的推動,雲端管治工具正以 22.8% 的複合年成長率成長。諸如 EDM 理事會的 CDMC 等框架提供了最佳實踐,以增強審核的信心。混合模式已成為主流:敏感的黃金記錄保留在本地,而目錄搜尋、品質規則和彙報則在雲端執行。供應商正在跨平台策略編配方面展開競爭,以確保跨地域控制的一致性。

資料管治市場按元件(軟體、服務)、配置(雲端、本地部署)、組織規模(大型企業、中小企業)、業務職能(IT與營運、法律與合規、其他)、應用領域(合規管理、風險管理、其他)、最終用戶產業(銀行、金融服務和保險 (BFSI)、IT與電信、其他)以及地區進行細分。市場預測以美元計價。

區域分析

北美地區受益於成熟的數位轉型投資和框架(例如強調管治的、符合 FedRAMP 標準的聯邦企業架構),預計到 2024 年將佔全球收入的 35.6%。金融機構競相整合 FedNow 系統,充分體現了監理期限如何推動支出成長。美國) 關於人工智慧安全性的規則制定進一步促進了平台功能的改進。該地區的資料管治市場規模得益於密集的顧問公司和超大規模雲端服務供應商生態系統,這些公司和供應商原生整合了資料管理功能。

亞洲是成長最快的地區,複合年成長率高達26.3%。印度的《資料保護法》和《資料保護條例》重塑了資料流,而中國的資料出口負面清單草案則強化了本地託管要求。這些法規將推動對主權雲端目錄的投資,以便實施區域特定的資料保留策略。日本和韓國正在完善現有法規,使其與全球標準接軌,從而加強跨境合作。跨國公司正在為區域特定的管治叢集編制預算,擴大了潛在的資料管治市場。

在《一般資料保護規範》(GDPR) 和新頒布的歐盟人工智慧立法的推動下,歐洲的資料治理市場持續保持顯著成長。歐洲的資料管治立法正在刺激醫療、能源和交通等領域的資料空間發展,從而推動可互通元元資料標準的需求。中東和非洲的資料治理市場尚處於發展初期,但智慧城市計劃和海灣合作理事會的資料主權規則正在加速其發展。加拿大的國家藍圖指出了35項標準化方面的差距,並鼓勵聯邦政府資助試點計畫。這些動態共同作用,為資料管治市場打造了一條地域分佈廣泛但又受監管主導的擴張路徑。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 歐盟人工智慧法和全球人工智慧監管對可解釋資料血緣的要求

- FedNow 和即時支付軌道為北美銀行、金融服務和保險業 (BFSI) 提供亞毫秒級資料完整性保障

- 亞太地區的主權雲端監管法規(例如印度的DPDP法案)正在加速對國內資料目錄的投資。

- 透過零售媒體貨幣化提升產品主資料質量

- 工業4.0中的邊緣分析需要近邊緣元資料聯合

- 市場限制

- 一級銀行企業級資料處理歷程工具整體擁有成本高昂

- 認證資料管理員和DCAM從業人員短缺

- 傳統大型主機互通性問題限制了國防機構的即時管治。

- 監理展望

- 波特五力分析

- 供應商的議價能力

- 買方/消費者的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 按組件

- 軟體

- 數據品質和分析工具

- 元資料管理與資料編目

- 主資料管理

- 數據沿襲和影響分析

- 資料安全與隱私管治

- 服務

- 專業服務

- 託管服務

- 軟體

- 透過部署

- 雲

- 本地部署

- 按組織規模

- 主要企業

- 小型企業

- 按業務職能

- IT和營運

- 法律與合規

- 金融與風險

- 行銷與銷售

- 人力資源

- 其他功能

- 透過使用

- 合規管理

- 風險管理

- 審核管理

- 事件管理

- 數據品管

- 其他用途

- 按最終用戶行業分類

- BFSI

- 資訊科技和通訊

- 醫療保健和生命科學

- 零售與電子商務

- 政府和國防部

- 製造業

- 能源與公共產業

- 媒體與娛樂

- 其他行業

- 按地區

- 北美洲

- 美國

- 加拿大

- 拉丁美洲

- 巴西

- 阿根廷

- 智利

- 墨西哥

- 其他南美洲

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 瑞典

- 挪威

- 芬蘭

- 丹麥

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞

- 澳洲

- 紐西蘭

- 亞太其他地區

- 中東

- 海灣合作理事會(沙烏地阿拉伯、阿拉伯聯合大公國、卡達)

- 土耳其

- 以色列

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 肯亞

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- Strategic Developments

- Vendor Positioning Analysis

- 公司簡介

- IBM Corporation

- Microsoft Corporation

- Oracle Corporation

- SAP SE

- Collibra NV

- Informatica Inc.

- Alation Inc.

- SAS Institute Inc.

- TIBCO Software Inc.

- Talend SA

- Varonis Systems Inc.

- Amazon Web Services

- Precisely LLC

- Ataccama Corp.

- Quest Software(erwin Data Intelligence)

- OneTrust LLC

- OpenText Corp.(incl. Micro Focus)

- ASG Technologies(Rocket Software)

- Snowflake Inc.

- Databricks Inc.

- Cloudera Inc.

- Alfresco Software Inc.

第7章 市場機會與未來展望

第8章:市場機會與未來展望

- 閒置頻段與未滿足需求評估

The data governance market sized is estimated at USD3.91 billion in 2025 and is forecast to reach USD 9.62 billion by 2030, reflecting a 19.72% CAGR.

The surge is underpinned by stricter regulatory mandates, accelerating cloud adoption, and the growing realization that well-governed data is crucial for trustworthy AI, real-time payments, and cross-border commerce. Financial institutions, healthcare providers, and manufacturers are broadening investments as penalties for breaches escalate and as business models shift toward data monetization. Vendors are embedding AI into lineage and catalog tools to automate classification tasks, while buyers emphasize deployment flexibility that supports sovereign-cloud and hybrid architectures. The data governance market is therefore evolving from compliance-focused point solutions to integrated platforms that orchestrate quality, security, and accountability across dispersed data estates.

Global Data Governance Market Trends and Insights

EU AI Act and Global AI-Regulation Requiring Explainable Data Lineage

The EU AI Act, effective August 2024, obliges companies deploying high-risk AI to document data origins, transformations, and quality metrics. Failure can trigger fines up to USD 39.82 million or 7% of global turnover, pushing enterprises to adopt advanced lineage platforms that illustrate end-to-end data flows. Vendors are integrating model-level metadata with traditional catalog systems so that auditors can trace training sets and detect bias. Multinationals anticipate similar provisions in Brazil and Canada, turning compliance into a global requirement. These pressures elevate demand for tools that link datasets, models, and business outcomes in a single governance workspace. As a result, the data governance market is pivoting toward solutions that fuse AI oversight with conventional stewardship capabilities.

FedNow and Real-Time Payment Rails Forcing Sub-Millisecond Data Integrity in North-American BFSI

The FedNow Service went live in July 2023 and now operates 24/7 across participating banks. Sub-millisecond settlement demands pristine data quality and continuous lineage to satisfy anti-money-laundering checks without slowing transactions. Institutions are deploying AI-enabled screening and enrichment pipelines to flag anomalies instantly. Legacy batch-oriented compliance stacks cannot keep pace, so banks are modernizing metadata repositories and automating control tests. This driver accelerates subscription revenue for cloud-native governance vendors that can embed rules directly into payment workflows. It also spurs consulting engagements aimed at retrofitting lineage tools to mainframe cores, a lucrative niche within the wider data governance market.

High Total Cost of Ownership for Enterprise-Scale Data Lineage Tooling

Tier-1 banks grapple with multi-million-dollar annual outlays for licenses, integration, and hardware refresh when rolling out enterprise lineage platforms. An Aalto University study confirms that integration with legacy systems and the absence of standards inflate timelines and budgets. Some institutions resort to manual mapping to lower expenses, slowing full-fledged deployments. Vendors respond with modular pricing and consumption-based cloud editions, yet sticker shock remains a prominent brake on expansion within the data governance market.

Other drivers and restraints analyzed in the detailed report include:

- APAC Sovereign-Cloud Mandates Accelerating In-Country Data Catalog Investments

- Retail-Media Monetization Elevating Product-Master Data Quality Spend

- Talent Shortage of Certified Data Stewards and DCAM Practitioners

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software solutions accounted for 57.1% of revenue in 2024, anchoring the data governance market with capabilities that automate policy enforcement, metadata harvesting, and lineage visualization. AI-driven classification and anomaly detection are now baseline features, helping organizations comply with the EU AI Act and FedNow directives in real time. The data governance market size for software is projected to deepen as vendors embed model-governance modules that audit AI pipelines.

Services, encompassing implementation, training, and managed operations, are forecast to expand at 23.4% CAGR. Talent shortages and rising regulatory complexity push organizations to outsource framework design and day-to-day stewardship. Managed services providers are layering SLAs for data quality and consent compliance, differentiating themselves in a fragmented services arena.

Growth in services is also propelled by industry-specific advisory packages. Banking clients demand lineage accelerators pre-mapped to BCBS 239, while healthcare buyers request HIPAA-ready templates. This vertical tailoring leaves room for boutique consultancies alongside global system integrators. Consequently, the data governance market continues shifting from purely licensing models toward mixed recurring revenue streams.

On-premise deployments retained a 53.6% share in 2024 as financial services and healthcare firms insist on local control over sensitive records. Mainframe coexistence and regulated workloads reinforce datacenter preferences despite broader enterprise migration to SaaS. The data governance market share for on-premise solutions is expected to erode gradually as cloud security certifications widen.

Cloud governance tools are advancing at 22.8% CAGR, driven by sovereign-cloud mandates and remote-work norms. Frameworks such as the EDM Council's CDMC provide best practices that reassure auditors. Hybrid patterns dominate: sensitive golden records sit on-premise, while catalog search, quality rules, and reporting run in the cloud. Vendors compete on cross-plane policy orchestration that keeps controls consistent across locations, a capability now essential to win enterprise contracts.

Data Governance Market is Segmented by Component (Software, Services), Deployment (Cloud, On-Premise), Organization Size (Large Enterprises, Small and Medium Enterprises), Business Function (IT and Operations, Legal and Compliance, and More) Application (Compliance Management, Risk Management, and More), End-User Industry (BFSI, IT and Telecom, and More), Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America commanded 35.6% revenue in 2024, supported by mature digital-transformation investments and frameworks such as the Federal Enterprise Architecture that emphasize FedRAMP-aligned governance. Financial institutions racing to integrate FedNow exemplify how regulatory deadlines catalyze spending. AI safety rule-making by the National Institute of Standards and Technology further spurs platform enhancements. The data governance market size in the region benefits from dense ecosystems of consultants and hyperscale cloud providers that embed stewardship capabilities natively.

Asia is the fastest-growing region at 26.3% CAGR. India's DPDP Act reshapes data flows, while China's draft negative list for data exports tightens local hosting requirements. These statutes propel investments in sovereign-cloud catalogs capable of enforcing locale-specific retention policies. Japan and South Korea refine existing directives to match global benchmarks, amplifying cross-border alignment. Multinationals now budget region-specific governance clusters, enlarging the addressable data governance market.

Europe retains significant scale through the GDPR and newly enacted EU AI Act. The European Data Governance Act stimulates sectoral data spaces in health, energy, and mobility, fostering demand for interoperable metadata standards . The Middle East and Africa are earlier in their maturity curve but are accelerating, driven by smart-city projects and Gulf Cooperation Council data-sovereignty rules. Canada's national roadmap pinpoints 35 standardization gaps, prompting federally funded pilots . Together, these dynamics produce a geographically diverse but regulatory-driven expansion path for the data governance market.

- IBM Corporation

- Microsoft Corporation

- Oracle Corporation

- SAP SE

- Collibra NV

- Informatica Inc.

- Alation Inc.

- SAS Institute Inc.

- TIBCO Software Inc.

- Talend SA

- Varonis Systems Inc.

- Amazon Web Services

- Precisely LLC

- Ataccama Corp.

- Quest Software (erwin Data Intelligence)

- OneTrust LLC

- OpenText Corp. (incl. Micro Focus)

- ASG Technologies (Rocket Software)

- Snowflake Inc.

- Databricks Inc.

- Cloudera Inc.

- Alfresco Software Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 EU AI Act and Global AI-Regulation Requiring Explainable Data Lineage

- 4.2.2 FedNow and Real-Time Payment Rails Forcing Sub-Millisecond Data Integrity in North-American BFSI

- 4.2.3 APAC Sovereign-Cloud Mandates (e.g., India DPDP Act) Accelerating In-Country Data Catalog Investments

- 4.2.4 Retail-Media Monetisation Elevating Product-Master Data Quality Spend

- 4.2.5 Edge Analytics in Manufacturing 4.0 Demands Near-Edge Metadata Federation

- 4.3 Market Restraints

- 4.3.1 High Total Cost of Ownership for Enterprise-Scale Data Lineage Tooling in Tier-1 Banks

- 4.3.2 Talent Shortage of Certified Data Stewards and DCAM Practitioners

- 4.3.3 Legacy Mainframe Interoperability Issues Limiting Real-Time Governance in Defense Agencies

- 4.4 Regulatory Outlook

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers / Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.1.1 Data Quality and Profiling Tools

- 5.1.1.2 Metadata Management and Data Catalog

- 5.1.1.3 Master Data Management

- 5.1.1.4 Data Lineage and Impact Analysis

- 5.1.1.5 Data Security and Privacy Governance

- 5.1.2 Services

- 5.1.2.1 Professional Services

- 5.1.2.2 Managed Services

- 5.1.1 Software

- 5.2 By Deployment

- 5.2.1 Cloud

- 5.2.2 On-Premise

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises (SMEs)

- 5.4 By Business Function

- 5.4.1 IT and Operations

- 5.4.2 Legal and Compliance

- 5.4.3 Finance and Risk

- 5.4.4 Marketing and Sales

- 5.4.5 Human Resources

- 5.4.6 Other Functions

- 5.5 By Application

- 5.5.1 Compliance Management

- 5.5.2 Risk Management

- 5.5.3 Audit Management

- 5.5.4 Incident Management

- 5.5.5 Data Quality Management

- 5.5.6 Other Applications

- 5.6 By End-user Industry

- 5.6.1 BFSI

- 5.6.2 IT and Telecom

- 5.6.3 Healthcare and Life Sciences

- 5.6.4 Retail and E-Commerce

- 5.6.5 Government and Defense

- 5.6.6 Manufacturing

- 5.6.7 Energy and Utilities

- 5.6.8 Media and Entertainment

- 5.6.9 Other Industries

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.2 Latin America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.2.3 Chile

- 5.7.2.4 Mexico

- 5.7.2.5 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 Germany

- 5.7.3.2 United Kingdom

- 5.7.3.3 France

- 5.7.3.4 Italy

- 5.7.3.5 Spain

- 5.7.3.6 Sweden

- 5.7.3.7 Norway

- 5.7.3.8 Finland

- 5.7.3.9 Denmark

- 5.7.3.10 Rest of Europe

- 5.7.4 Asia-Pacific

- 5.7.4.1 China

- 5.7.4.2 India

- 5.7.4.3 Japan

- 5.7.4.4 South Korea

- 5.7.4.5 Southeast Asia

- 5.7.4.6 Australia

- 5.7.4.7 New Zealand

- 5.7.4.8 Rest of Asia-Pacific

- 5.7.5 Middle East

- 5.7.5.1 GCC (Saudi Arabia, UAE, Qatar)

- 5.7.5.2 Turkey

- 5.7.5.3 Israel

- 5.7.5.4 Rest of Middle East

- 5.7.6 Africa

- 5.7.6.1 South Africa

- 5.7.6.2 Nigeria

- 5.7.6.3 Kenya

- 5.7.6.4 Rest of Africa

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Strategic Developments

- 6.2 Vendor Positioning Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)}

- 6.3.1 IBM Corporation

- 6.3.2 Microsoft Corporation

- 6.3.3 Oracle Corporation

- 6.3.4 SAP SE

- 6.3.5 Collibra NV

- 6.3.6 Informatica Inc.

- 6.3.7 Alation Inc.

- 6.3.8 SAS Institute Inc.

- 6.3.9 TIBCO Software Inc.

- 6.3.10 Talend SA

- 6.3.11 Varonis Systems Inc.

- 6.3.12 Amazon Web Services

- 6.3.13 Precisely LLC

- 6.3.14 Ataccama Corp.

- 6.3.15 Quest Software (erwin Data Intelligence)

- 6.3.16 OneTrust LLC

- 6.3.17 OpenText Corp. (incl. Micro Focus)

- 6.3.18 ASG Technologies (Rocket Software)

- 6.3.19 Snowflake Inc.

- 6.3.20 Databricks Inc.

- 6.3.21 Cloudera Inc.

- 6.3.22 Alfresco Software Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

- 7.1.1 Databricks Inc.

- 7.1.2 Cloudera Inc.

- 7.1.3 Alfresco Software Inc.

8 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 8.1 White-Space and Unmet-Need Assessment

資料管治市場規模、佔有率和趨勢:按組件、部署類型、組織規模、業務功能、應用、最終用戶行業和地區分類(2026-2034 年)

資料管治市場規模、佔有率和趨勢:按組件、部署類型、組織規模、業務功能、應用、最終用戶行業和地區分類(2026-2034 年) 資料管治市場:2026-2032年全球市場預測(依解決方案、部署模式、組織規模、產業和應用分類)

資料管治市場:2026-2032年全球市場預測(依解決方案、部署模式、組織規模、產業和應用分類) 2026年全球非結構化資料管治市場報告2026年全球培訓資料管治市場報告2026年全球數據合約管治市場報告2026年全球資料來源市場報告2026年全球資料管治實務平台市場報告2026年全球資料管治市場報告

2026年全球非結構化資料管治市場報告2026年全球培訓資料管治市場報告2026年全球數據合約管治市場報告2026年全球資料來源市場報告2026年全球資料管治實務平台市場報告2026年全球資料管治市場報告 全球資料管治平台市場:預測(至 2034 年)-按產品、組件、應用、最終用戶和地區分類的分析

全球資料管治平台市場:預測(至 2034 年)-按產品、組件、應用、最終用戶和地區分類的分析 資料管治市場 - 全球產業規模、佔有率、趨勢、機會及預測(按組件、組織規模、部署模式、最終用戶、地區和競爭格局分類,2021-2031 年)

資料管治市場 - 全球產業規模、佔有率、趨勢、機會及預測(按組件、組織規模、部署模式、最終用戶、地區和競爭格局分類,2021-2031 年)