|

市場調查報告書

商品編碼

1850354

電信電源系統:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)Telecom Power Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

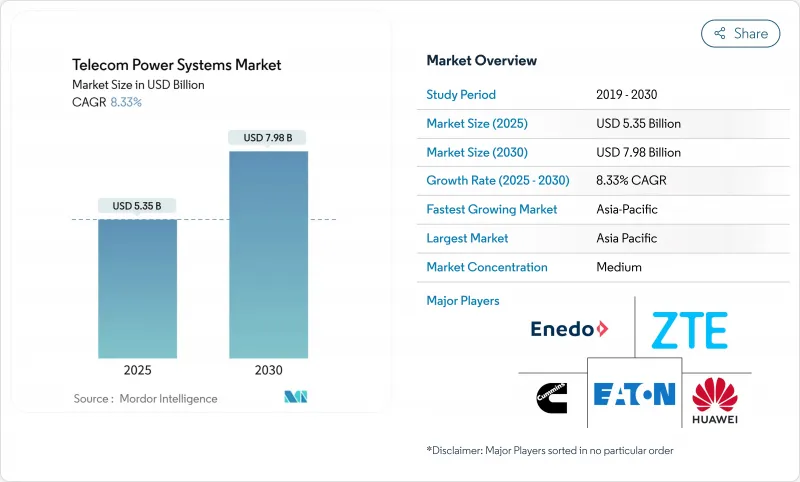

預計到 2025 年電信電源系統市場規模將達到 53.5 億美元,到 2030 年將達到 79.8 億美元,年複合成長率為 8.33%。

為了滿足5G宏無線電電力消耗,通訊業者正優先考慮更有效率的整流器、AC/DC混合架構和先進的電池化學技術。持續的網路密集化、邊緣站點的建設以及監管機構為控制能源消耗而施加的壓力,正在加速對專用電力基礎設施的投資。鋰離子電池的長壽命和低生命週期成本正推動電池採購從閥控式鉛酸蓄電池(VRLA)轉向其他類型的電池,而燃料電池在關鍵站點的零排放備用電源方面也越來越受歡迎。亞太地區仍然是最具影響力的需求中心,這主要得益於大規模的農村電氣化和積極的5G部署計劃,而北美和歐洲則在增強應對極端天氣事件的能力和碳排放合規性方面投入巨資。

全球電信電源系統市場趨勢與洞察

5G大型基地台部署快速成長

大規模5G宏基地台部署使每個站點的電力負載翻倍,單一基地台的功率需求現已超過20kW。為了抵消不斷上漲的電力成本並適應有限的基地台空間,營運商正在維修現有基地台,採用轉換效率高達96%的緊湊型高效整流器。功率密度壓力也加速了向高壓直流(DC)配電的過渡,從而減少了導體尺寸和熱損耗。在人口密集的城市地區,整合式直流電源架與鋰離子電池組結合,可在尖峰時段實現快速發行。提供模組化5G就緒電源架的供應商透過縮短安裝時間和最大限度地減少站點停機時間,正在搶佔市場佔有率。隨著5G無線網路擴展到大規模MIMO配置,主動冷卻和精確溫度控管的需求也成為重要的採購促進因素。

農村電氣化:混合動力創新的催化劑

未通電和部分通電地區正在投資太陽能-柴油和太陽能-電池混合動力系統,這些系統可在維持99.99%運轉率的同時,減少高達70%的柴油消耗。混合動力控制器現在編配多源輸入,最佳化不同化學成分的發電機運作和充電狀態。通訊業者將這些系統視為實現全球37億仍缺乏可靠寬頻的人口普遍連結的橋樑。像EdgePoint在馬來西亞的太陽能混合動力塔這樣的現場部署塔,在最佳照度下可提供高達100%的能量,使每個塔的年度二氧化碳排放減少78%。農村電力接入的改善進一步推動了低功耗小型基地台和固定無線接入模式的發展,擴大了電信電力系統市場的潛在覆蓋範圍。

資本密集型場地現代化

為5G網路改造電力基礎設施,每個宏基站的成本可能在2.5萬美元到4萬美元之間,而且在過渡期間通常需要對現有系統進行並行維護,這實際上會使近期資本支出翻倍。規模較小的業者面臨資產負債表的壓力,這導致升級計畫延期,並延長了低效率設備的使用壽命。諸如電力即服務(Power-as-a-Service)之類的資金籌措模式正在興起,但除一級營運商外,其應用仍然有限。漫長的現代化改造週期阻礙了高壓直流和鋰離子電池的及時普及,限制了電信電源系統市場的近期成長潛力。在新興經濟體,外匯波動和進口零件的高成本也進一步阻礙了快速升級改造。

細分市場分析

到2024年,功率在5至20千瓦之間的中階解決方案將佔據電信電源系統市場佔有率的46%。中端解決方案仍將是承載4G LTE層和不斷擴展的5G領域的宏基地台的骨幹。電信電源系統市場正策略性地向20千瓦以上的平台轉型,複合年成長率(CAGR)為11.32%。這些更大功率的系統能夠滿足高負載需求,例如大規模MIMO無線電、邊緣電腦架以及密閉機房內的主動冷卻。供應商正致力於熱插拔模組和智慧負載管理,使營運商能夠在不中斷站點服務的情況下分階段進行升級。

城市高密度化和頻率共享促使營運商在單一屋頂上部署多個頻寬,從而增加了每個站點的負載。高容量整流器和鋰離子電池組的組合既能限制佔地面積,又能滿足運行時間要求。散熱設計已成為一項重要的競爭優勢。戶外機櫃採用液冷技術來應對不斷增加的熱通量。另一方面,功率低於 5kW 的低功耗解決方案仍在為小型基地台供電,但隨著室內分散式部署向採用集中式電源的雲端無線存取網路 (Cloud RAN) 架構過渡,其市場佔有率正在萎縮。

到2024年,併網系統將佔總收入的55%,這主要得益於歐洲、北美和東亞地區強大的城市電網。然而,混合式太陽能-柴油架構是電信電源系統市場中成長最快的細分領域,年複合成長率高達14.01%。非洲、南亞和東南亞的營運商正在採用這些混合方案,以減少高達70%的柴油消耗,並確保長達15年的能源成本可預測性。控制器可以協調光伏陣列、電池組和發電機的運作時間,從而最佳化發電機調度並減少總總合。

除了成本之外,對永續性的承諾也使混合電網更具可行性。混合微電網透過減少範圍 1排放,支持了塔式電站公司的科學目標。 EdgePoint 公司在馬來西亞建造的 5.9 kWp 塔式電站表明,在太陽輻射高峰期,太陽能可以滿足 100% 的站點負荷,從而減少 78% 的年度碳排放。由於間歇性,風能和獨立式太陽能光電等純再生能源仍屬於小眾市場,但電池價格的下降和能源管理分析技術的應用正在逐步擴大其普及範圍。

預計到2024年,整流器將佔組件收入的28%,並將繼續透過碳化矽MOSFET拓撲結構的發展來降低損耗並縮小散熱器尺寸。燃料電池領域正以15.10%的複合年成長率成長,滿足那些需要長時間自主運作且避免柴油發電帶來的環境影響的場所的需求。固體電解質燃料電池系統的電效率約為60%,且僅排放水蒸氣,因此非常適合人口密集地區和環境監管嚴格的地區。早期應用案例包括資料中心附近的收發器站叢集,這些集群需要在電網中斷超過8小時的情況下保持不間斷運作。

電池子系統正從密閉式鉛酸電池過渡到鋰離子電池和固態電池。冷卻曾經是次要考慮因素,但現在至關重要,因為主動電子元件和電池必須共用一個緊湊的機殼。供應商正在將變速壓縮機組和冷板解決方案整合到產品中,以降低高達 40% 的冷卻功耗。控制器和遠端監控硬體正在整合人工智慧預測分析功能,以減少非計劃現場維護,並使維護週期與實際磨損情況相符。

電信電源解決方案市場報告按功率範圍(低、中、高)、電源(併網、柴油發電機、其他)、組件(轉換器、整流器、其他)、系統結構(交流電源系統、直流電源系統、其他)、儲能技術(VRLA電池、其他)、網路生成(4G/LTE、其他)、輸出功率配置(小於2千瓦、2-1000、其他地區進行。

區域分析

亞太地區預計到2024年將佔總營收的41%,複合年成長率達10.42%。大規模待開發區鐵塔部署,以及農村地區高容量直流儲槽和太陽能混合供電系統的應用,正在推動電信電源系統市場的發展。日本和韓國透過邊緣運算節點推動了市場需求,這些節點需要高壓直流配電來滿足對延遲要求嚴格的應用。

北美則位居第二,這主要得益於C頻段5G的持續升級以及對氣候適應能力的重視。通訊業者正在透過增加耐高溫鋰離子電池組和設計能夠承受更長時間電網中斷的機殼,來加強發電廠,使其免受野火和颶風的侵襲。加拿大運輸公司正在部署低溫電池技術和遠端遙測技術,以最大限度地減少冬季卡車側翻事故;墨西哥的鐵塔公司則正在投資混合陣列,以穩定偏遠地區的電力供應。

歐洲市場正受到全球最嚴格的能源效率法規的影響。電訊必須揭露站點層級的能源指標,這加速了混合可再生電站和智慧整流器的應用。德國正將其工業4.0獎勵策略放在強大的5G網路覆蓋和先進的電源櫃上。英國則專注於服務連續性。新法規提高了營運商對服務中斷的責任,並鼓勵採用冗餘的UPS設計。東歐國家正利用歐盟凝聚基金,直接以鋰離子電池和混合AC/DC電源軌對傳統機房進行現代化改造。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 價值鏈分析

- 市場促進因素

- 5G大型基地台部署快速成長

- 新興市場農村電氣化進程加速

- 通訊業者的能源效率義務

- 鋰離子和磷酸鋰電池UPS系統正變得越來越受歡迎。

- 遠端基地台衛星回程傳輸擴展

- RAN資料中心與邊緣站點的整合

- 市場限制

- 資本密集型場地現代化

- 增加離網地區的維運支出

- 消防安全和環境合規成本

- 功率半導體供應鏈前置作業時間延長

- 監管格局

- 波特五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

- 投資分析

第5章 市場規模與成長預測

- 按功率範圍

- 低的

- 中等的

- 高的

- 透過電源

- 並聯型

- 柴油發電機

- 可再生能源(太陽能、風能)

- 混合動力(太陽能柴油、燃料電池混合動力)

- 按組件

- 電源單元

- 轉換器

- 整流器

- 逆變器

- 控制器和監視器

- 電池

- 發電機

- 太陽能發電模組

- 燃料電池

- 冷凍/空調系統

- 依系統結構

- 交流電源系統

- 直流電源系統

- 混合交流/直流系統

- 儲能技術

- VRLA 電池

- 鋰離子電池

- 鎳基電池

- 超級電容

- 氫燃料電池

- 網路生成

- 2G/3G 傳統

- 4G/LTE

- 5G NR

- 衛星/低地球回程傳輸

- 專用LTE/5G網路

- 按輸出功率配置

- 小於2千瓦

- 2~10kW

- 10~20kW

- 20度或以上

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 智利

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- ASEAN

- 其他亞太地區

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 非洲

- 南非

- 奈及利亞

- 肯亞

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Huawei Digital Power

- Delta Electronics(Inc. and Eltek)

- Vertiv Group

- Eaton Corporation

- Cummins Inc.

- Schneider Electric

- ABB Group

- ZTE Corporation

- Enedo(Efore Group)

- Alpha Technologies(EnerSys)

- GE Vernova

- Siemens AG

- Mitsubishi Electric

- Nokia Corporation(AirScale Power)

- Ericsson Power Systems

- Innova Power Solutions

- Huawei-Zhongshan TroPower JV

- Delta-Reliance Teleinfra JV

- GenCell Energy

- Ballard Power Systems

第7章 市場機會與未來展望

The telecom power systems market size stands at USD 5.35 billion in 2025 and is projected to reach USD 7.98 billion by 2030, advancing at an 8.33% CAGR.

Operators are prioritizing higher-efficiency rectifiers, hybrid AC/DC architectures, and advanced battery chemistries to accommodate the doubled power draw of 5G macro radios. Sustained network densification, edge-site build-outs, and regulatory pressure to curb energy use are accelerating investment in purpose-built power infrastructure. Lithium-ion's longer life and lower lifetime cost are tilting battery procurement away from VRLA, while fuel cells are gaining attention for zero-emission backup at critical sites. Asia Pacific remains the most influential demand center thanks to large-scale rural electrification and aggressive 5G timelines, whereas North America and Europe are investing heavily in resilience against severe weather events and carbon compliance.

Global Telecom Power Systems Market Trends and Insights

Surging 5G Macro-Cell Roll-outs

Massive 5G macro deployment is doubling the electrical load per site, with individual base stations now demanding more than 20 kW. Operators are retrofitting compact high-efficiency rectifiers that reach 96% conversion efficiency to offset rising utility costs and to fit within constrained tower footprints. Power density pressure is also accelerating the move to higher-voltage DC distribution that cuts conductor size and thermal losses. In dense urban clusters, integrated DC power shelves paired with lithium-ion strings enable quick energy dispatch during traffic peaks. Vendors offering modular 5G-ready power shelves have captured early share because they shorten installation windows and minimize site downtime. As 5G radios ramp to massive-MIMO configurations, demand for active cooling and precise thermal management is becoming a parallel purchase driver.

Rural Electrification: Catalyst for Hybrid Power Innovation

Off-grid and weak-grid communities are drawing investment into solar-diesel and solar-battery hybrids that cut diesel burn by up to 70% while preserving 99.99% uptime. Hybrid controllers now orchestrate multi-source inputs, optimizing generator run hours and state of charge across diverse chemistries. Telecom operators view these systems as a bridge to universal connectivity for an estimated 3.7 billion people still lacking reliable broadband. Field deployments, such as EdgePoint's solar hybrid towers in Malaysia, supply up to 100% of site energy under optimal irradiance and curb annual carbon emissions by 78% per tower. Improved rural power availability is further unlocking low-power small-cell and fixed-wireless access models, expanding the total addressable footprint for the telecom power systems market.

Capital-Intensive Site Modernization

Retro-fitting 5G-ready power infrastructure costs USD 25,000-40,000 per macro site and often requires parallel legacy support during migration, effectively doubling near-term capital outlay. Smaller operators face balance-sheet pressure that slows upgrade schedules and prolongs the operating life of less-efficient gear. Financing models such as power-as-a-service are emerging, yet uptake is modest outside tier-1 players. Prolonged modernization cycles hinder timely adoption of high-voltage DC and lithium-ion, limiting the short-term growth potential of the telecom power systems market. In developing economies, currency fluctuations and high cost of imported components add another barrier to rapid overhaul.

Other drivers and restraints analyzed in the detailed report include:

- Energy Efficiency Mandates Drive Innovation

- Lithium-ion Adoption Reshapes Backup Economics

- Off-Grid Operations: Maintenance Challenges Persist

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Medium-range solutions of 5-20 kW captured 46% of the telecom power systems market share in 2024. They remain the backbone for macro sites that host 4G LTE layers and incremental 5G sectors. The telecom power systems market is witnessing a strategic pivot toward >=20 kW platforms that are growing at an 11.32% CAGR. These larger systems satisfy the aggregated load of massive-MIMO radios, edge compute racks, and active cooling within confined shelters. Vendors focus on hot-swappable modules and intelligent load management so that operators can phase-upgrade without site outages.

Urban densification and spectrum pooling push operators to terminate multiple frequency bands at a single rooftop, raising per-site load. High-capacity rectifiers coupled with lithium-ion strings limit footprint while maintaining runtime objectives. Thermal design has emerged as a competitive differentiator; outdoor cabinets integrate liquid cooling to handle the increased heat flux. Conversely, low-power solutions below 5 kW continue serving small cells but their share is tapering as indoor distributed deployments migrate to cloud-RAN architectures with centralized power.

Grid-connected systems accounted for 55% of revenue in 2024 owing to robust urban grids in Europe, North America, and East Asia. Hybrid solar-diesel architectures, however, are expanding at a 14.01% CAGR and represent the fastest-growing slice of the telecom power systems market. Operators in Africa, South Asia, and Southeast Asia adopt these hybrids to cut diesel usage by up to 70% and lock in predictable energy cost over a 15-year horizon. Controllers that coordinate PV arrays, battery banks, and generator runtime optimize generator scheduling and curtail trip totals.

Beyond cost, sustainability commitments elevate hybrid viability. Hybrid micro-grids support corporate science-based targets by lowering scope 1 emissions at tower companies. EdgePoint's 5.9 kWp Malaysian tower shows solar can meet 100% of site load during peak irradiance, eliminating 78% of yearly carbon output. Pure renewables such as wind or standalone PV remain niche due to intermittency, but battery price declines and energy-management analytics are gradually expanding their deployment envelope.

Rectifiers constituted 28% of component revenue in 2024 and continue to evolve through silicon-carbide MOSFET topologies that cut loss and shrink heat sinks. The fuel-cell segment is climbing at a 15.10% CAGR, addressing sites that require extended autonomy without the environmental penalties of diesel. Proton-exchange-membrane systems deliver about 60% electrical efficiency and water vapor emissions only, making them suitable for densely populated or environmentally regulated areas. Early adopters include base-transceiver-station clusters adjacent to data centers that seek uninterrupted runtime during grid disturbance windows exceeding eight hours.

Battery sub-systems are transitioning from sealed lead-acid toward lithium-ion and emerging solid-state formats. Cooling, once a secondary consideration, is now integral since active electronics and batteries must share tighter enclosures. Vendors package variable-speed compressor units and cold-plate solutions that slash cooling power by 40%. Controllers and remote monitoring hardware embed AI-enabled predictive analytics, trimming unplanned site visits and aligning maintenance intervals with actual wear.

Telecom Power Solutions Market Report is Segmented by Power Range (Low, Medium, High), Power Source (Grid-Connected, Diesel Generator, and More), Component (Converters, Rectifiers, and More), System Architecture (AC Power Systems, DC Power Systems, and More), Energy Storage Technology (VRLA Battery and More), Network Generation (4G / LTE and More), Output Power Configuration (less Than 2 KW, 2 - 10 KW, and More), and Geography.

Geography Analysis

Asia Pacific contributed 41% of 2024 revenue and is expanding at 10.42% CAGR, anchored by China's nationwide 5G blitz and India's accelerated Digital India mandate. Massive greenfield tower rollouts pair high-capacity DC shelves with solar hybrids in rural provinces, broadening the telecom power systems market. Japan and South Korea add incremental demand through edge-compute nodes that require high-voltage DC distribution for latency-critical applications.

North America ranks second, driven by continued C-band 5G upgrades and a sharp focus on climate resilience. Operators are hardening power plants against wildfires and hurricanes by adding lithium-ion packs with elevated temperature tolerance and designing enclosures that withstand longer grid-down intervals. Canadian carriers deploy cold-climate battery chemistries and remote telemetry to minimize winter truck rolls, while Mexican towercos invest in hybrid arrays to stabilize power in remote states.

Europe's market is shaped by some of the world's strictest energy-efficiency rules. Telecom firms are required to disclose site-level energy metrics, accelerating adoption of hybrid renewable plants and intelligent rectifiers. Germany channels Industry 4.0 stimulus toward robust 5G coverage and thus advanced power cabinets. The United Kingdom concentrates on service continuity; new regulations increase operator liability for interruptions, prompting redundant UPS design. Eastern European nations leverage EU cohesion funds to modernize legacy shelters directly with lithium-ion and hybrid AC/DC power rails.

- Huawei Digital Power

- Delta Electronics (Inc. and Eltek)

- Vertiv Group

- Eaton Corporation

- Cummins Inc.

- Schneider Electric

- ABB Group

- ZTE Corporation

- Enedo (Efore Group)

- Alpha Technologies (EnerSys)

- GE Vernova

- Siemens AG

- Mitsubishi Electric

- Nokia Corporation (AirScale Power)

- Ericsson Power Systems

- Innova Power Solutions

- Huawei-Zhongshan TroPower JV

- Delta-Reliance Teleinfra JV

- GenCell Energy

- Ballard Power Systems

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Value Chain Analysis

- 4.3 Market Drivers

- 4.3.1 Surging 5G Macro-Cell Roll-outs

- 4.3.2 Rapid Rural Electrification in Emerging Markets

- 4.3.3 Energy-Efficiency Mandates for Telcos

- 4.3.4 Growing Preference for Lithium-ion and LFP UPS Systems

- 4.3.5 Satellite-Back-haul Expansion for Remote Towers

- 4.3.6 Data-center and Edge-site Convergence with RAN

- 4.4 Market Restraints

- 4.4.1 Capital-intensive Site Modernization

- 4.4.2 High OandM Spend in Off-grid Terrains

- 4.4.3 Fire-safety and Environmental Compliance Costs

- 4.4.4 Prolonged Supply-chain Lead-times for Power Semis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Power Range

- 5.1.1 Low

- 5.1.2 Medium

- 5.1.3 High

- 5.2 By Power Source

- 5.2.1 Grid-connected

- 5.2.2 Diesel Generator

- 5.2.3 Renewable (Solar, Wind)

- 5.2.4 Hybrid (Solar-Diesel, Fuel-cell Hybrid)

- 5.3 By Component

- 5.3.1 Power Supply Units

- 5.3.2 Converters

- 5.3.3 Rectifiers

- 5.3.4 Inverters

- 5.3.5 Controllers and Monitoring

- 5.3.6 Batteries

- 5.3.7 Generators

- 5.3.8 Solar PV Modules

- 5.3.9 Fuel Cells

- 5.3.10 Cooling/Climate Systems

- 5.4 By System Architecture

- 5.4.1 AC Power Systems

- 5.4.2 DC Power Systems

- 5.4.3 Hybrid AC/DC Systems

- 5.5 By Energy Storage Technology

- 5.5.1 VRLA Battery

- 5.5.2 Lithium-ion Battery

- 5.5.3 Nickel-based Battery

- 5.5.4 Super-capacitors

- 5.5.5 Hydrogen Fuel Cell

- 5.6 By Network Generation

- 5.6.1 2G/3G Legacy

- 5.6.2 4G / LTE

- 5.6.3 5G NR

- 5.6.4 Satellite / LEO Back-haul

- 5.6.5 Private LTE / 5G Networks

- 5.7 By Output Power Configuration

- 5.7.1 less than 2 kW

- 5.7.2 2 - 10 kW

- 5.7.3 10 - 20 kW

- 5.7.4 above 20 kW

- 5.8 By Geography

- 5.8.1 North America

- 5.8.1.1 United States

- 5.8.1.2 Canada

- 5.8.1.3 Mexico

- 5.8.2 South America

- 5.8.2.1 Brazil

- 5.8.2.2 Argentina

- 5.8.2.3 Chile

- 5.8.3 Europe

- 5.8.3.1 Germany

- 5.8.3.2 United Kingdom

- 5.8.3.3 France

- 5.8.3.4 Italy

- 5.8.3.5 Spain

- 5.8.3.6 Russia

- 5.8.4 Asia Pacific

- 5.8.4.1 China

- 5.8.4.2 India

- 5.8.4.3 Japan

- 5.8.4.4 South Korea

- 5.8.4.5 ASEAN

- 5.8.4.6 Rest of Asia Pacific

- 5.8.5 Middle East and Africa

- 5.8.5.1 Middle East

- 5.8.5.1.1 Saudi Arabia

- 5.8.5.1.2 UAE

- 5.8.5.1.3 Turkey

- 5.8.5.2 Africa

- 5.8.5.2.1 South Africa

- 5.8.5.2.2 Nigeria

- 5.8.5.2.3 Kenya

- 5.8.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Huawei Digital Power

- 6.4.2 Delta Electronics (Inc. and Eltek)

- 6.4.3 Vertiv Group

- 6.4.4 Eaton Corporation

- 6.4.5 Cummins Inc.

- 6.4.6 Schneider Electric

- 6.4.7 ABB Group

- 6.4.8 ZTE Corporation

- 6.4.9 Enedo (Efore Group)

- 6.4.10 Alpha Technologies (EnerSys)

- 6.4.11 GE Vernova

- 6.4.12 Siemens AG

- 6.4.13 Mitsubishi Electric

- 6.4.14 Nokia Corporation (AirScale Power)

- 6.4.15 Ericsson Power Systems

- 6.4.16 Innova Power Solutions

- 6.4.17 Huawei-Zhongshan TroPower JV

- 6.4.18 Delta-Reliance Teleinfra JV

- 6.4.19 GenCell Energy

- 6.4.20 Ballard Power Systems

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

2025年電信電源系統全球市場報告

2025年電信電源系統全球市場報告 電信電源系統市場(按組件、電源、額定功率、電網類型、應用和最終用戶分類)—2025-2030 年全球預測

電信電源系統市場(按組件、電源、額定功率、電網類型、應用和最終用戶分類)—2025-2030 年全球預測 電信電源系統市場規模、佔有率、趨勢和預測產品類型、組件、電源、電網類型和地區,2025 年至 2033 年

電信電源系統市場規模、佔有率、趨勢和預測產品類型、組件、電源、電網類型和地區,2025 年至 2033 年 通訊電源系統市場 - 成長、未來展望、競爭分析,2025 年至 2033 年

通訊電源系統市場 - 成長、未來展望、競爭分析,2025 年至 2033 年 電信電源系統市場規模、佔有率、成長分析,按組件、按電網類型、按額定功率、按動力來源、按技術、按地區 - 行業預測,2024-2031 年

電信電源系統市場規模、佔有率、成長分析,按組件、按電網類型、按額定功率、按動力來源、按技術、按地區 - 行業預測,2024-2031 年 電信電源系統市場(組件:整流器、逆變器、轉換器、控制器、發電機等;電網類型:併網和離網)- 全球行業分析、規模、佔有率、成長、趨勢和預測,2024 年- 2034

電信電源系統市場(組件:整流器、逆變器、轉換器、控制器、發電機等;電網類型:併網和離網)- 全球行業分析、規模、佔有率、成長、趨勢和預測,2024 年- 2034 全球電信電源系統市場:趨勢、預測、競爭分析

全球電信電源系統市場:趨勢、預測、競爭分析 2023-2030 年全球電信電源系統市場規模研究與預測(依產品類型、電網類型、電源與區域分析)電信電源系統市場-2018-2028年全球產業規模、佔有率、趨勢、機會與預測,依電網類型、組件、電源、地區、競爭細分

2023-2030 年全球電信電源系統市場規模研究與預測(依產品類型、電網類型、電源與區域分析)電信電源系統市場-2018-2028年全球產業規模、佔有率、趨勢、機會與預測,依電網類型、組件、電源、地區、競爭細分 通訊電源系統市場規模、佔有率和趨勢分析報告:2023-2030 年按產品類型、電網類型、電力源、地區和細分市場進行的預測

通訊電源系統市場規模、佔有率和趨勢分析報告:2023-2030 年按產品類型、電網類型、電力源、地區和細分市場進行的預測