|

市場調查報告書

商品編碼

1850353

紫外線LED:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030年)UV LED - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

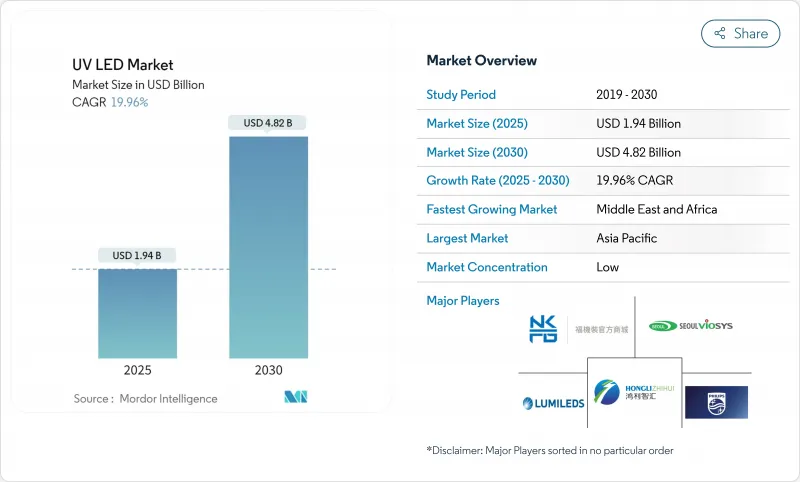

預計到 2025 年,UV LED 市場規模將達到 19.4 億美元,到 2030 年將達到 48.2 億美元,年複合成長率為 19.96%。

全球禁用汞燈、對節能固化解決方案的需求激增以及晶片量子效率的快速提升是推動成長的主要因素。水俁公約、歐盟RoHS指令和加拿大汞法規的生效時間在2025年至2027年間趨於一致,這將促使終端用戶採用紫外線LED。 AlGaN外延、覆晶結構和溫度控管的同步進步,使深紫外線元件的外部量子效率在250 mA電流下達到9.19%,縮小了與傳統汞燈的性能差距。印刷、包裝和水處理產業的強勁成長勢頭,也使供應商對2030年的收入前景充滿信心。

全球紫外LED市場趨勢與洞察

嚴格的汞燈淘汰政策加速了紫外線LED的普及。

全球法規正在逐步淘汰照明設備中的汞源。 《水俁公約》已促使147個締約國承諾在2027年前逐步淘汰螢光。歐盟RoHS指令已將每盞燈的汞含量限制在5毫克以內,預計2027年後將全面禁止使用。加拿大2025年的法規也反映了這個方向。隨著用戶不斷轉型,一些已用固態LED陣列取代汞燈的印刷生產線報告稱,能耗降低了85%。因此,那些預先認證UV LED設備的供應商正在獲得長期維修合約。

亞洲各地對水消毒的需求激增

快速的都市化給印度、印尼和中國沿海地區的中心供水網路帶來了壓力。挪威的現場試驗表明,使用LED反應器在545立方米/天的處理量下可去除3個對數單位的大腸桿菌群,證明該技術適用於市政供水。其緊湊的外形尺寸使得UV-C發送器可以整合到家用飲水機、小型工廠和鄉村診所。亞洲設備製造商正在擴大整合模組的規模,使其能夠在太陽能微電網上運行,從而加速離網供水安全。

量子效率上限限制了高功率應用

波長低於280奈米的深紫外線LED的電能轉換效率通常低於5%,遠低於低壓汞燈20-30%的效率。需要千瓦級輸出功率的水務公司必須部署大型LED陣列,這推高了資本成本。目前的研究重點是量子點、超晶格和透明基板,以提高電洞注入和光提取效率。 AlGaN超晶格設計已將外部量子效率提高到35毫瓦時的8.6%,但要實現這種性能水平的大規模生產仍需數年時間。

細分市場分析

到2024年,UV-A系統將佔據72%的收入佔有率,繼續在印刷品固化和仿冒品檢測領域保持領先地位;而隨著醫療保健和市政用戶採用無汞消毒解決方案,UV-C的複合年成長率將達到22.5%。歐司朗的OSLON™ UV 3535紫外線殺菌燈在265nm波長下可提供115mW的功率,使用壽命長達20,000小時,這標誌著可靠的水和空氣反應器發展的一個重要里程碑。 UV-B紫外線殺菌燈則專注於照光治療和農業光形態發生領域,形成了特定的市場需求。

不同地區的應用趨勢各異:歐洲已將255-275nm波長的紫外線發送器標準化應用於食品加工管道,而日本則正在探索將308nm波長的UV-B紫外線應用於皮膚病學領域。隨著量子效率的不斷提高,預計到2030年,用於醫療空氣消毒的UV-C模組的紫外線LED市場規模將以行業平均水平的兩倍速度成長。遠UVC 222nm準分子發送器的突破性進展可望實現對生活空間的持續安全消毒,進一步拓展其應用範圍。

由於易於整合,模組仍將佔據最大的收入佔有率,預計到 2024 年將達到 42%。然而,晶片的複合年成長率將達到 23.7%,這反映了消費性電子和實驗室設備對客製化光引擎的需求。 GaN-on-SiC基板降低了熱阻,使得 2025 年的原型晶片能夠實現 100mW 的輸出功率。燈具細分市場主要面向改裝插座,但隨著陣列的普及,其銷售量正在逐漸下降。

超小型晶片正為新型生物感測器和實驗室晶片設備提供動力。調查團隊已展示了尺寸為 90 奈米、外量子效率達 20% 的奈米級鈣鈦礦 LED。隨著封裝材料從陶瓷轉向模塑複合材料,每毫瓦的平均成本正在下降,推動了可攜式消毒設備的設計應用。因此,預計到 2030 年,紫外線 LED 在晶片級銷售額的市佔率將上升至 35%。

區域分析

到2024年,亞太地區將佔據紫外線LED市場55%的營收佔有率。中國為實現自主研發,催生了本土外延供應商和專屬式元件封裝生產線。日本和韓國則貢獻了其高精度製造技術,而台灣地區則專注於深紫外線晶片的氮化鎵基板。不斷成長的公共衛生預算推動了特大城市對紫外線水淨化和空氣淨化技術的需求,進一步鞏固了該地區的市場主導地位。

北美位居第二。加州加速淘汰汞燈,加上聯邦政府對國內晶片生產能力的資助,正在推動醫療保健和先進製造業採用LED燈。然而,專利積壓和人事費用上升限制了LED燈的普及速度。歐洲也緊跟其後,強制推行能源效率標準。生態設計規則預測,到2030年,96%的燈具將是LED燈,這將為紫外線解決方案的推廣鋪平道路。

中東和非洲是成長最快的地區,複合年成長率達20.4%,主要得益於海水淡化廠和新建醫院採用LED反應器。海灣國家正在資助智慧城市項目,這些項目明確規定使用無汞照明。在南美洲,飲料填充和水產養殖業發展勢頭強勁,而市政供水企業則因認證週期而進展緩慢。在所有地區,隨著監管和技術的同步成熟,紫外LED市場正以趨同的速度持續成長。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 歐盟和加州嚴格的汞燈淘汰政策加速了紫外線LED的普及

- 新冠疫情後,亞洲各地對即用型水消毒的需求激增。

- 為符合食品安全法規,軟包裝產業正迅速轉向低遷移油墨

- 歐洲能源價格上漲使低功率紫外線LED固化生產線更具優勢。

- 微型LED背光技術藍圖圖推動半導體工廠採用深紫外線偵測工具

- 遠紫外光(222奈米)在機場和醫院等人員密集場所的空氣淨化方面正廣泛應用。

- 市場限制

- 基於AlGaN的UVC晶片的量子效率上限(<5%)限制了其在高功率應用方面的潛力。

- 北美地區以版稅為主導的智慧財產權格局提高了新進入者的成本門檻。

- 工業固化生產線中高密度陣列的溫度控管挑戰

- 認證週期過長會延誤新興國家農村供水設施的發展(NSF/ANSI 55-2022)

- 產業生態系分析

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 按技術(波長)

- UV-A

- UV-B

- UV-C

- 按產品/外形規格

- 燈

- 模組

- 大批

- 尖端

- 透過輸出

- 低功耗(小於10毫瓦)

- 中功率(10-100毫瓦)

- 高功率(超過100毫瓦)

- 透過使用

- 固化(油墨、塗料、黏合劑)

- 消毒和滅菌

- 感測與測量

- 醫療和照光治療

- 仿冒品檢測與安全

- 園藝和室內農業

- 其他小眾應用(3D列印、光刻)

- 按最終用戶行業分類

- 醫療保健和生命科學

- 印刷和包裝

- 電子和半導體

- 水務及污水處理業務

- 食品/飲料加工

- 汽車和航太

- 住宅及商業建築

- 工業製造

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 東南亞

- 亞太其他地區

- 南美洲

- 巴西

- 其他南美洲

- 中東和非洲

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 其他中東地區

- 非洲

- 南非

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- ams OSRAM AG

- Signify NV

- Nichia Corporation

- Seoul Viosys Co., Ltd.

- Crystal IS Inc.(Asahi Kasei)

- Lumileds Holding BV

- Nikkiso Co., Ltd.(UV Business)

- LG Innotek Co., Ltd.

- LITE-ON Technology Corp.

- Honlitronics(Hongli Zhihui Group)

- Stanley Electric Co., Ltd.

- SemiLEDs Corporation

- Violumas Inc.

- DOWA Electronics Materials Co., Ltd.

- Nordson Corporation

- Luminus Devices, Inc.

- Heraeus Holding GmbH(Noblelight)

- Phoseon Technology(Excelitas)

- Sensor Electronic Technology Inc.(SETi)

- Bolb Inc.

第7章 市場機會與未來展望

The UV LED market is valued at USD 1.94 billion in 2025 and is forecast to reach USD 4.82 billion by 2030, reflecting a 19.96% CAGR.

Growth is powered by global mercury-lamp bans, surging demand for energy-efficient curing solutions, and rapid gains in chip quantum efficiency. Regulatory timelines under the Minamata Convention, EU RoHS, and Canadian mercury rules converge in 2027-2025, pushing end users toward UV LED adoption, Parallel advances in AlGaN epitaxy, flip-chip structures, and thermal management have lifted external quantum efficiency for deep-UV devices to 9.19% at 250 mA, closing the performance gap with legacy mercury lamps. Strong replacement momentum in printing, packaging, and water treatment is reinforcing supplier revenue visibility through 2030.

Global UV LED Market Trends and Insights

Stringent Mercury-Lamp Phase-Out Policies Accelerating UV LED Adoption

Global regulation is eliminating mercury sources in lighting. The Minamata Convention aligned 147 signatories on a 2027 fluorescent exit. The EU RoHS Directive already caps mercury content at 5 mg per lamp, with full bans expected after 2027. Canada's 2025 rules mirror this direction. As users transition, printing lines report 85% lower energy use after swapping mercury lamps for solid-state arrays. Vendors that pre-qualified UV LED equipment are therefore securing long-term retrofit contracts.

Surge in Point-of-Use Water Disinfection Demand Across Asia

Rapid urbanisation stresses central water grids in India, Indonesia, and coastal China. Field trials in Norway demonstrated 3-log coliform removal at 545 m3/day using LED reactors, validating the technology's viability for municipal flows. Compact form factors allow embedding UV-C emitters in home dispensers, small factories, and rural clinics. Asian equipment makers are scaling integrated modules that operate on solar micro-grids, accelerating off-grid water-safety rollouts.

Quantum Efficiency Ceiling Limiting High-Power Applications

Deep-UV LEDs below 280 nm typically deliver <5% wall-plug efficiency, far below the 20-30% of low-pressure mercury lamps.Water utilities needing kilowatt-scale output must deploy large LED arrays, inflating capital costs. Research now focuses on quantum dots, super-lattices, and transparent substrates to improve hole injection and light extraction. AlGaN super-lattice designs boosted EQE to 8.6% at 35 mW, yet mass manufacturing at such performance remains years away.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Shift to Low-Migration UV LED Inks in Flexible Packaging

- Energy Price Inflation Favouring Low-Power UV LED Curing Lines

- Royalty-Heavy IP Landscape Raising Cost Barriers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

UV-A systems held 72% revenue share in 2024, retaining dominance in graphic-arts curing and counterfeit detection. UV-C, however, is set for a 22.5% CAGR as healthcare and municipal users deploy mercury-free germicidal solutions. ams OSRAM's OSLON(TM) UV 3535 delivers 115 mW at 265 nm with 20,000-hour life, a key milestone for reliable water and air reactors. The UV-B niche addresses phototherapy and agricultural photomorphogenesis, carving specialised demand pockets.

Adoption dynamics vary by region. Europe is standardising 255-275 nm emitters in food-processing pipelines, while Japan explores 308 nm UV-B for dermatology. As quantum-efficiency gains continue, the UV LED market size for UV-C modules targeting medical air sterilisation is projected to grow at double the sector average through 2030. Breakthroughs in far-UVC 222 nm excimer emitters promise human-safe continuous disinfection of occupied spaces, further widening the use-case frontier.

Modules retained the largest 42% slice of 2024 revenue due to integration ease. Chips, though, will post a 23.7% CAGR, reflecting demand for custom optical engines in consumer devices and lab instruments. GaN-on-SiC substrates cut thermal resistance, enabling chip-level powers of 100 mW in 2025 prototypes. The lamps sub-segment serves retrofit sockets but faces gradual volume decline as arrays gain traction.

Ultra-miniaturised chips underpin emerging biosensors and lab-on-a-chip devices. Researchers have demonstrated nano-scale perovskite LEDs with 20% EQE at 90 nm dimensions. As packaging shifts from ceramic to moulded composites, median cost per milliwatt is falling, stimulating design-in across portable sterilisation gadgets. Consequently, the UV LED market share of chip-level sales is forecast to rise to 35% by 2030.

The UV LED Market Report is Segmented by Technology (Wavelength) (UV-A, UV-B, and UV-C), Product/Form Factor (Lamps, Modules, and More), Power Output (Low Power, Medium Power, and More), Application (Curing, Disinfection and Sterilization, and More), End-User Industry (Healthcare and Life Sciences, Printing and Packaging, Automotive and Aerospace, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific held a commanding 55% share of UV LED market revenue in 2024. China's self-reliance push is spawning local epitaxy suppliers and captive device packaging lines. Japan and South Korea add high-precision fabrication know-how, while Taiwan specialises in gallium-nitride substrates for deep-UV chips. Rising public-health budgets channel demand for UV-based water and air purification across megacities, cementing regional dominance.

North America ranks second. California's accelerated mercury-lamp phase-out, coupled with federal funding for domestic chip capacity, drives adoption in healthcare and advanced manufacturing. However, a dense patent thicket and higher labour costs temper the expansion pace. Europe follows closely, powered by energy-efficiency mandates. Ecodesign rules forecast that 96% of installed lamps will be LEDs by 2030, creating a receptive environment for UV solutions.

The Middle East & Africa is the fastest-growing area, showing a 20.4% CAGR as desalination plants and new hospitals incorporate LED reactors. Gulf states fund smart-city programmes that specify mercury-free lighting. South America sees momentum in beverage bottling and aquaculture, though municipal water projects move slowly due to certification cycles. Across all geographies, simultaneous regulation and technology maturation keep the UV LED market on a convergent uplift path.

- ams OSRAM AG

- Signify N.V.

- Nichia Corporation

- Seoul Viosys Co., Ltd.

- Crystal IS Inc. (Asahi Kasei)

- Lumileds Holding B.V.

- Nikkiso Co., Ltd. (UV Business)

- LG Innotek Co., Ltd.

- LITE-ON Technology Corp.

- Honlitronics (Hongli Zhihui Group)

- Stanley Electric Co., Ltd.

- SemiLEDs Corporation

- Violumas Inc.

- DOWA Electronics Materials Co., Ltd.

- Nordson Corporation

- Luminus Devices, Inc.

- Heraeus Holding GmbH (Noblelight)

- Phoseon Technology (Excelitas)

- Sensor Electronic Technology Inc. (SETi)

- Bolb Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stringent Mercury Lamp Phase-Out Policies in EU and California Accelerating UV-LED Adoption

- 4.2.2 Surge in Point-of-Use Water Disinfection Demand Post-COVID-19 Across Asia

- 4.2.3 Rapid Shift to Low-Migration UV LED Inks in Flexible Packaging for Food Safety Compliance

- 4.2.4 Energy Price Inflation in Europe Favouring Low-Power UV-LED Curing Lines

- 4.2.5 Mini-LED Backlighting Roadmaps Driving Deep-UV Inspection Tools Adoption in Semiconductor Fabs

- 4.2.6 Growing Acceptance of Far-UVC (222 nm) for Occupied-Space Air Sanitisation in Airports and Hospitals

- 4.3 Market Restraints

- 4.3.1 Quantum Efficiency Ceiling (<5 %) of AlGaN-Based UVC Chips Limits High-Power Applications

- 4.3.2 Royalty-Heavy IP Landscape Raising Cost Barriers for New Entrants in North America

- 4.3.3 Thermal Management Challenges in High-Density UV LED Arrays for Industrial Curing Lines

- 4.3.4 Slow Certification Cycles (NSF/ANSI 55-2022) Delaying Municipal Water Projects in Emerging Economies

- 4.4 Industry Ecosystem Analysis

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Technology (Wavelength)

- 5.1.1 UV-A

- 5.1.2 UV-B

- 5.1.3 UV-C

- 5.2 By Product/Form Factor

- 5.2.1 Lamps

- 5.2.2 Modules

- 5.2.3 Arrays

- 5.2.4 Chips

- 5.3 By Power Output

- 5.3.1 Low Power (<10 mW)

- 5.3.2 Medium Power (10-100 mW)

- 5.3.3 High Power (>100 mW)

- 5.4 By Application

- 5.4.1 Curing (Inks, Coatings and Adhesives)

- 5.4.2 Disinfection and Sterilization

- 5.4.3 Sensing and Instrumentation

- 5.4.4 Medical and Phototherapy

- 5.4.5 Counterfeit Detection and Security

- 5.4.6 Horticulture and Indoor Farming

- 5.4.7 Other Niche Applications (3-D Printing, Lithography)

- 5.5 By End-user Industry

- 5.5.1 Healthcare and Life Sciences

- 5.5.2 Printing and Packaging

- 5.5.3 Electronics and Semiconductors

- 5.5.4 Water and Wastewater Utilities

- 5.5.5 Food and Beverage Processing

- 5.5.6 Automotive and Aerospace

- 5.5.7 Residential and Commercial Buildings

- 5.5.8 Industrial Manufacturing

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 South Korea

- 5.6.3.4 India

- 5.6.3.5 South East Asia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 United Arab Emirates

- 5.6.5.1.2 Saudi Arabia

- 5.6.5.1.3 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 ams OSRAM AG

- 6.4.2 Signify N.V.

- 6.4.3 Nichia Corporation

- 6.4.4 Seoul Viosys Co., Ltd.

- 6.4.5 Crystal IS Inc. (Asahi Kasei)

- 6.4.6 Lumileds Holding B.V.

- 6.4.7 Nikkiso Co., Ltd. (UV Business)

- 6.4.8 LG Innotek Co., Ltd.

- 6.4.9 LITE-ON Technology Corp.

- 6.4.10 Honlitronics (Hongli Zhihui Group)

- 6.4.11 Stanley Electric Co., Ltd.

- 6.4.12 SemiLEDs Corporation

- 6.4.13 Violumas Inc.

- 6.4.14 DOWA Electronics Materials Co., Ltd.

- 6.4.15 Nordson Corporation

- 6.4.16 Luminus Devices, Inc.

- 6.4.17 Heraeus Holding GmbH (Noblelight)

- 6.4.18 Phoseon Technology (Excelitas)

- 6.4.19 Sensor Electronic Technology Inc. (SETi)

- 6.4.20 Bolb Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

紫外線LED市場規模、佔有率、趨勢和預測:按類型、材料、應用、產業和地區分類,2026-2034年

紫外線LED市場規模、佔有率、趨勢和預測:按類型、材料、應用、產業和地區分類,2026-2034年 深紫外線(DUV)LED市場趨勢及產品分析(2026年)

深紫外線(DUV)LED市場趨勢及產品分析(2026年) 紫外線LED市場:2026-2032年全球市場預測(依產品類型、波長、輸出功率、封裝方式、應用領域、銷售管道及最終用戶分類)

紫外線LED市場:2026-2032年全球市場預測(依產品類型、波長、輸出功率、封裝方式、應用領域、銷售管道及最終用戶分類) 紫外線LED市場分析及預測(至2035年):依類型、產品、服務、技術、組件、應用、材料類型、裝置、最終使用者及解決方案分類

紫外線LED市場分析及預測(至2035年):依類型、產品、服務、技術、組件、應用、材料類型、裝置、最終使用者及解決方案分類 紫外線LED市場機會、成長促進因素、產業趨勢分析及預測(2026-2035年)

紫外線LED市場機會、成長促進因素、產業趨勢分析及預測(2026-2035年) 2026年全球UV-C LED市場報告2026年全球深層紫外線LED市場報告

2026年全球UV-C LED市場報告2026年全球深層紫外線LED市場報告 紫外線LED市場-全球產業規模、佔有率、趨勢、機會及預測(依技術、應用、區域及競爭格局分類,2021-2031年)

紫外線LED市場-全球產業規模、佔有率、趨勢、機會及預測(依技術、應用、區域及競爭格局分類,2021-2031年) UV LED固化市場:預測(2025-2030年)

UV LED固化市場:預測(2025-2030年) 紫外線LED-全球市佔率及排名、總收入及需求預測(2025-2031年)

紫外線LED-全球市佔率及排名、總收入及需求預測(2025-2031年)