|

市場調查報告書

商品編碼

1850325

新一代防火牆:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)Next Generation Firewall - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

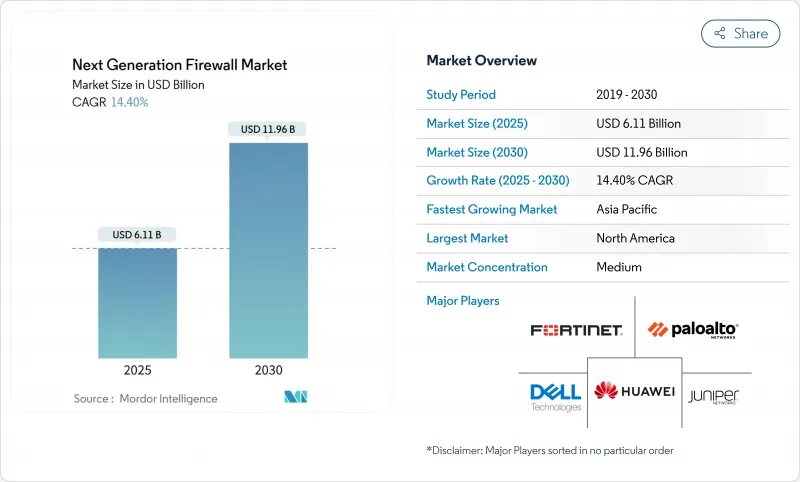

預計到 2025 年,新世代防火牆市場規模將達到 61.1 億美元,到 2030 年將達到 119.6 億美元,複合年成長率為 14.4%。

向零信任架構的轉變、更廣泛的雲端工作負載分佈以及內建的AI威脅分析(可將誤報率降低高達71%)正在推動下一代防火牆的普及。儘管硬體設備仍佔據主導地位,但隨著企業尋求在混合環境中實現軟體定義安全,虛擬和雲端原生部署正在迅速擴展。北美以36%的營收佔有率領先市場,而亞太地區則經歷了最快的成長,這得益於各國政府實施主權雲端指令和區域資料居住法。 IT電信(46%的佔有率)和銀行、金融服務和保險(BFSI)行業的需求最為集中,因為更嚴格的法令遵循和高價值的數位資產正促使金融機構更加關注即時威脅防禦。能夠將ASIC級性能、AI主導的檢測和整合策略管理相結合的供應商,最有可能在下一代防火牆市場中抓住新的機會。

全球新一代防火牆市場趨勢與洞察

加速雲端遷移需要內聯 L7 安全防護

如今,68% 的企業工作負載運行在公有雲、私有雲或混合雲端中,這導致東西向流量暴露在外,而傳統防火牆無法對其進行檢測。與僅依賴邊界防護的控制措施相比,具備應用感知偵測功能的雲端原生新世代防火牆 (NGFW) 可將平均威脅偵測時間縮短 63%,並將安全事件減少 47%。隨著 72% 的企業計劃在 2025 年增加雲端預算,並且 NGFW 已穩固確立為分散式架構的控制平面,對微服務的深度可見性將使安全團隊能夠維護統一的策略。

混合工作的普及擴大了攻擊面。

混合辦公模式的不斷普及導致遠端存取終端數量激增,目前已有 42% 的設備處於未管理狀態。採用零信任網路存取機制的新一代防火牆 (NGFW)檢驗每個連接,並推動 SonicWall Cloud Secure Edge 的預訂量年增 54%。身分感知策略可防止憑證欺詐,有效應對自 2023 年以來此類攻擊 37% 的成長,並使企業能夠在員工於公司網路和家庭網路之間切換時保護其安全。

資本密集型ASIC藍圖限制了中小企業級晶片價格的下降。

高性能 SSL/TLS 解密正促使供應商要求客製化晶片。 Fortinet 的 SP5 處理器在顯著降低功耗的同時,防火牆吞吐量提升了 7 倍,但高昂的研發成本導致入門級產品價格居高不下,43% 的中小企業表示成本是他們面臨的最大障礙。雖然 ASIC 晶片提高了能源效率(FortiGate 70G 每 Gbps 的功耗比競爭對手低 62 倍),但對於預算有限的買家來說,初始投資仍然是一筆不小的負擔。

細分市場分析

到2024年,大型企業將佔據70%的收入佔有率,因為它們雄厚的預算使它們能夠部署多Gigabit設備,從而實現對加密流量的零延遲檢測。大型企業仍青睞設備端ASIC加速與集中式策略編配的組合。同時,中小企業預計到2030年將以16.3%的複合年成長率成長,這主要得益於基於消費的訂閱模式和降低資本門檻的託管服務。靈活的授權和承包管理使資源有限的團隊能夠在外包複雜性的同時獲得企業級的控制權。因此,下一代防火牆市場正在形成兩種截然不同的價值提案:為全球跨國企業提供毫不妥協的吞吐量,以及為中小企業提供簡化的、服務主導的交付方式。

監管要求也將影響支出模式。大型企業面臨嚴格的審核追蹤,必須證明其在資料中心、分店和子公司擁有精細的控制能力。同時,中小企業將傾向於採用整合平台,將SD-WAN、IPS和零信任存取整合到單一堆堆疊中,從而避免「工具蔓延」。隨著計量型虛擬防火牆的廣泛普及,下一代防火牆市場預計將繼續對新用戶開放,尤其是在資本密集度較高的新興經濟體。

到2024年,硬體設備將維持55%的市場佔有率,這反映了它們在本地資料中心中可靠的效能特性。採用ASIC晶片的旗艦產品,例如FortiGate 700G,可提供164Gbps的防火牆吞吐量,其能效比行業平均水平高出七倍,這凸顯了高頻寬營運商為何仍然偏愛具有確定性延遲的物理設備。同時,在彈性工作負載和基礎設施即程式碼經濟模式的推動下,虛擬和雲端基礎產品的收益佔有率將以15.4%的複合年成長率成長。

雲端託管的新一代防火牆 (NGFW) 的優勢在於其集中式 AI 分析功能,該功能能夠關聯多個租戶的威脅。 Versa Networks 在獨立安全測試中取得了 99.90% 的得分,展現出與現有硬體產品相媲美的性能。隨著企業精簡其工具鏈,他們擴大將防火牆功能整合到整體 SASE 或 SSE 框架中,從而增強了虛擬產品的連接性。這種雙重重演進正使新一代防火牆市場能夠同時滿足效能受限的資料中心和敏捷 DevOps 管線的需求。

區域分析

北美將保持其領先地位,市場佔有率高達36%,並將持續到2024年。零信任框架的早期應用、NIST指南等合規性促進因素以及領先供應商的存在,將維持高水準的支出。美國金融服務和醫療機構優先考慮對加密流量進行深度檢查和微隔離,從而推動了對高階設備的需求。聯邦政府的關鍵基礎設施現代化項目也將進一步活性化採購。

預計到2030年,亞太地區的複合年成長率將達到16.2%。日本、印度和新加坡等國的自主雲政策以及數位服務經濟的快速發展,將加速雲端原生防禦的部署。 Palo Alto Networks近期將Prisma Access Browser擴展到區域資料中心,顯示該公司致力於在滿足居住法規的同時,實現安全的遠端存取。託管安全服務的興起也有助於緩解技能短缺問題,使企業無需組建龐大的內部團隊即可部署企業級下一代防火牆(NGFW)功能。

歐洲擁有龐大且極具潛力的市場基礎,因為GDPR和NIS2指令要求對流量偵測和資料處理進行嚴格監管。即將訂定的歐盟人工智慧法案將更加強調將人工智慧負責任地整合到安全產品中,並影響供應商如何定位其威脅偵測引擎。能源、交通和金融市場等關鍵基礎設施公共產業的需求尤其顯著。

中東和非洲地區正呈現強勁成長勢頭,這主要得益於5G、智慧城市計劃和電子政府平台等數位轉型措施的推動。沙烏地阿拉伯和阿拉伯聯合大公國在網路安全領域投入了大量GDP,促進了激烈的市場競標,買家也正在尋求後量子密碼學支援和靈活的消費模式。儘管新一代防火牆的市場規模較小,但這些地區為市場帶來了多樣性,並為系統整合商提供了通路機會。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 加速雲端遷移需要啟用內聯 L7 安全性

- 混合工作的普及擴大了攻擊面。

- 受監理產業強制採用零信任架構

- 新一代防火牆 (NGFW) 內建了人工智慧驅動的即時威脅情報來源。

- 主權雲端計畫促進區域下一代防火牆支出

- 市場限制

- 資本密集型ASIC藍圖限制了中小企業的價格下跌

- 深層封包檢測人員短缺導致服務成本上升。

- 資料儲存碎片化減緩了全球SaaS下一代防火牆的普及

- 開放原始碼eBPF防火牆正在蠶食入門級產品的收益。

- 供應鏈分析

- 監管格局

- 技術展望

- 波特五力模型

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 按公司規模

- 小型企業

- 主要企業

- 按解決方案類型

- 硬體設備

- 虛擬/雲端基礎

- 透過部署模式

- 本地部署

- 公共雲端

- 私有雲/混合雲端

- 按最終用戶產業

- 銀行、金融服務和保險(BFSI)

- 資訊科技(IT)和通訊

- 政府和國防部

- 衛生保健

- 製造業

- 零售與電子商務

- 能源和公共產業

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美

- 歐洲

- 英國

- 德國

- 法國

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲和紐西蘭

- 其他亞太地區

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Palo Alto Networks Inc.

- Fortinet Inc.

- Cisco Systems Inc.

- Check Point Software Technologies Ltd.

- Juniper Networks Inc.

- Huawei Technologies Co. Ltd.

- Dell Technologies(SonicWall)

- SonicWall Inc.

- Barracuda Networks Inc.

- Forcepoint LLC

- WatchGuard Technologies Inc.

- Sophos Ltd.

- Hillstone Networks

- Zscaler Inc.

- Untangle Inc.

- Trend Micro Inc.

- Alibaba Cloud

- F5 Inc.

- VMware Inc.

- Meraki(Cisco)

- GajShield Infotech

- A10 Networks Inc.

第7章 市場機會與未來展望

The next generation firewall market is valued at USD 6.11 billion in 2025 and is forecast to climb to USD 11.96 billion by 2030, reflecting a 14.4% CAGR.

Heightened adoption stems from the move to zero-trust architectures, wider cloud workload distribution, and embedded AI-threat analytics that cut false positives by up to 71%. Hardware appliances still dominate, yet virtual and cloud-native deployments are scaling quickly as enterprises pursue software-defined security for hybrid environments. North America leads with a 36% revenue share, while Asia-Pacific is expanding the fastest as governments roll out sovereign-cloud mandates and regional data-residency laws. Demand is concentrated in IT-Telecom (46% share) and BFSI, where stricter compliance regimes and high-value digital assets push institutions toward real-time threat prevention. Vendors able to combine ASIC-level performance, AI-driven detection, and unified policy management are best placed to capture emerging opportunities in the next generation firewall market.

Global Next Generation Firewall Market Trends and Insights

Accelerated cloud migration demands inline L7-aware security

Sixty-eight percent of enterprise workloads now run in public, private, or hybrid clouds, exposing east-west traffic that legacy firewalls cannot inspect. Cloud-native NGFWs equipped with application-aware inspection shorten average threat detection time by 63% and cut security incidents by 47% compared with perimeter-only controls. Deep visibility across microservices lets security teams retain uniform policies as 72% of enterprises boost cloud budgets in 2025, firmly positioning NGFWs as the control plane for distributed architectures.

Hybrid-work proliferation expanding attack surface

Remote access endpoints grew sharply when hybrid work became permanent, with 42% of devices now unmanaged. NGFWs that embed zero-trust network access validate every connection and have driven a 54% year-on-year booking increase for SonicWall's Cloud Secure Edge. Identity-aware policies prevent credential abuse, addressing the 37% rise in such attacks since 2023, and equip firms to secure staff who move between corporate and home networks.

Capital-intensive ASIC road-map limits SMB-grade price declines

High-performance SSL/TLS decryption drives vendors toward custom silicon. Fortinet's SP5 processor gives 7X higher firewall throughput while consuming far less power, yet the research and development outlay keeps entry-level pricing elevated, with 43% of small businesses citing cost as the chief barrier. Although ASICs improve energy efficiency-FortiGate 70G needs 62X fewer watts per Gbps than rivals-the upfront spend remains daunting for budget-constrained buyers.

Other drivers and restraints analyzed in the detailed report include:

- Mandatory zero-trust architecture roll-outs in regulated sectors

- AI-driven threat intelligence transforms detection capabilities

- Shortage of deep-packet-inspection talent raises service costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Large enterprises contributed 70% of 2024 revenue as their sizable budgets allowed deployment of multi-gigabit appliances inspecting encrypted traffic without latency. They continue to favor on-appliance ASIC acceleration paired with centralized policy orchestration. In contrast, SMEs are forecast to post a 16.3% CAGR to 2030, propelled by consumption-based subscriptions and managed services that lower capital hurdles. Flexible licensing and turnkey management let resource-limited teams gain enterprise-grade controls while outsourcing complexity. As a result, the next generation firewall market captures two distinct value propositions: uncompromising throughput for global multinationals and simplified, service-led offerings for smaller firms.

Regulatory obligations also shape spending patterns. Larger organizations confront stringent audit trails and must demonstrate granular control across data centers, branches, and subsidiaries. Smaller companies, meanwhile, gravitate toward consolidated platforms that integrate SD-WAN, IPS, and zero-trust access in a single stack, avoiding "tool sprawl." The widening availability of pay-as-you-go virtual firewalls is expected to keep the next generation firewall market accessible to new adopters, especially across developing economies where capital intensity is a concern.

Hardware appliances retained 55% share in 2024, reflecting trusted performance characteristics within on-premises data centers. ASIC-laden flagships such as the FortiGate 700G deliver 164 Gbps firewall throughput at 7X better power efficiency than the industry mean, underscoring why high-bandwidth operators continue to prefer physical devices for deterministic latency. Meanwhile, the portion of revenue from virtual and cloud-based offerings is rising at a 15.4% CAGR, accelerated by elastic workloads and the economics of infrastructure-as-code.

Cloud-hosted NGFWs draw strength from centralized AI analytics that correlate threats across multiple tenants. Versa Networks scored 99.90% in independent security tests, signaling parity with hardware incumbents. As enterprises rationalize toolchains, they increasingly embed firewall functions within holistic SASE or SSE frameworks, boosting attach rates for virtual products. This dual-track evolution ensures the next generation firewall market addresses both performance-bound data-center needs and agile DevOps pipelines.

Next Generation Firewall Market Report is Segmented by Enterprise Size (SMEs and Large Enterprises), Solution Type (Hardware Appliance and Virtual / Cloud-Based), Deployment Mode (On-Premises, Public Cloud, and More), End-User Industry (Banking, Financial Services and Insurance (BFSI), Information Technology (IT) and Telecom, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America maintained first place with a 36% share in 2024. Early adoption of zero-trust frameworks, compliance drivers such as the NIST guidelines, and the presence of leading vendors sustain high spending depths. Financial services and healthcare institutions in the United States prioritize deep inspection of encrypted traffic and micro-segmentation, reinforcing demand for high-end appliances. Federal programs that modernize critical infrastructure further amplify procurement.

Asia-Pacific is projected to grow at 16.2% CAGR through 2030. Sovereign-cloud policies in Japan, India, and Singapore, together with a surging digital-services economy, accelerate rollouts of cloud-native defenses. Palo Alto Networks' recent expansion of Prisma Access Browser to regional data centers underlines vendor efforts to meet residency rules while enabling secure remote access. The climb in managed security services also addresses skills shortages, allowing enterprises to deploy enterprise-grade NGFW capabilities without large in-house teams.

Europe forms a sizable addressable base as GDPR and the NIS2 Directive require robust traffic inspection and data-handling safeguards. The forthcoming EU AI Act places new emphasis on responsible AI integration within security products, influencing how vendors position threat-detection engines. Demand is notable among critical infrastructure operators in energy, transport, and financial market utilities.

The Middle East and Africa are registering solid growth as national digital-transformation agendas roll out 5G, smart-city projects, and e-government platforms. Robust GDP allocation to cybersecurity in Saudi Arabia and the United Arab Emirates stimulates competitive tenders, with buyers looking for post-quantum cryptography readiness and flexible consumption models. Although starting from a smaller base, these regions add diversity to the next generation firewall market and open channel opportunities for system integrators.

- Palo Alto Networks Inc.

- Fortinet Inc.

- Cisco Systems Inc.

- Check Point Software Technologies Ltd.

- Juniper Networks Inc.

- Huawei Technologies Co. Ltd.

- Dell Technologies (SonicWall)

- SonicWall Inc.

- Barracuda Networks Inc.

- Forcepoint LLC

- WatchGuard Technologies Inc.

- Sophos Ltd.

- Hillstone Networks

- Zscaler Inc.

- Untangle Inc.

- Trend Micro Inc.

- Alibaba Cloud

- F5 Inc.

- VMware Inc.

- Meraki (Cisco)

- GajShield Infotech

- A10 Networks Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated cloud migration demands inline L7-aware security

- 4.2.2 Hybrid-work proliferation expanding attack surface

- 4.2.3 Mandatory zero-trust architecture roll-outs in regulated sectors

- 4.2.4 AI-driven, real-time threat-intel feeds embedded in NGFWs

- 4.2.5 Sovereign-cloud initiatives boosting regional NGFW spend

- 4.3 Market Restraints

- 4.3.1 Capital-intensive ASIC road-map limits SMB-grade price declines

- 4.3.2 Shortage of deep-packet-inspection talent raises service costs

- 4.3.3 Fragmented data-residency laws slowing global SaaS NGFW uptake

- 4.3.4 Open-source eBPF firewalls eroding entry-level revenues

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Enterprise Size

- 5.1.1 Small and Medium Enterprises (SMEs)

- 5.1.2 Large Enterprises

- 5.2 By Solution Type

- 5.2.1 Hardware Appliance

- 5.2.2 Virtual / Cloud-based

- 5.3 By Deployment Mode

- 5.3.1 On-premises

- 5.3.2 Public Cloud

- 5.3.3 Private / Hybrid Cloud

- 5.4 By End-User Industry

- 5.4.1 Banking, Financial Services and Insurance (BFSI)

- 5.4.2 Information Technology (IT) and Telecom

- 5.4.3 Government and Defense

- 5.4.4 Healthcare

- 5.4.5 Manufacturing

- 5.4.6 Retail and E-commerce

- 5.4.7 Energy and Utilities

- 5.4.8 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Russia

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Palo Alto Networks Inc.

- 6.4.2 Fortinet Inc.

- 6.4.3 Cisco Systems Inc.

- 6.4.4 Check Point Software Technologies Ltd.

- 6.4.5 Juniper Networks Inc.

- 6.4.6 Huawei Technologies Co. Ltd.

- 6.4.7 Dell Technologies (SonicWall)

- 6.4.8 SonicWall Inc.

- 6.4.9 Barracuda Networks Inc.

- 6.4.10 Forcepoint LLC

- 6.4.11 WatchGuard Technologies Inc.

- 6.4.12 Sophos Ltd.

- 6.4.13 Hillstone Networks

- 6.4.14 Zscaler Inc.

- 6.4.15 Untangle Inc.

- 6.4.16 Trend Micro Inc.

- 6.4.17 Alibaba Cloud

- 6.4.18 F5 Inc.

- 6.4.19 VMware Inc.

- 6.4.20 Meraki (Cisco)

- 6.4.21 GajShield Infotech

- 6.4.22 A10 Networks Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet Need Analysis

企業網路防火牆市場:依組件、部署類型、企業規模及產業分類-2026年至2032年全球市場預測

企業網路防火牆市場:依組件、部署類型、企業規模及產業分類-2026年至2032年全球市場預測 2026年全球網站開發市場報告新一代防火牆市場:按組件、部署模式、功能、組織規模、產業和銷售管道分類-2026-2032年全球市場預測2026年全球新一代防火牆市場報告

2026年全球網站開發市場報告新一代防火牆市場:按組件、部署模式、功能、組織規模、產業和銷售管道分類-2026-2032年全球市場預測2026年全球新一代防火牆市場報告 新一代防火牆 (NGFW) 市場分析及至 2035 年預測:按類型、產品類型、服務、技術、組件、應用、部署模式、最終用戶和功能分類網路應用程式防火牆(WAF)市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、部署模式、最終用戶、功能和解決方案分類下一代防火牆市場分析及至2035年預測:按類型、產品類型、服務、技術、組件、應用、部署類型和最終用戶分類

新一代防火牆 (NGFW) 市場分析及至 2035 年預測:按類型、產品類型、服務、技術、組件、應用、部署模式、最終用戶和功能分類網路應用程式防火牆(WAF)市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、部署模式、最終用戶、功能和解決方案分類下一代防火牆市場分析及至2035年預測:按類型、產品類型、服務、技術、組件、應用、部署類型和最終用戶分類 全球DNS防火牆市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球DNS防火牆市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 新一代防火牆市場-全球產業規模、佔有率、趨勢、機會及預測(按組件、公司規模、最終用途產業、地區及競爭格局分類,2021-2031年)新一代工業防火牆市場:按組件、組織規模、安全類型、部署模式和最終用戶產業分類-2026-2032年全球預測

新一代防火牆市場-全球產業規模、佔有率、趨勢、機會及預測(按組件、公司規模、最終用途產業、地區及競爭格局分類,2021-2031年)新一代工業防火牆市場:按組件、組織規模、安全類型、部署模式和最終用戶產業分類-2026-2032年全球預測