|

市場調查報告書

商品編碼

1850288

大規模MIMO-市場佔有率分析、產業趨勢、統計、成長預測(2025-2030)Massive MIMO - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

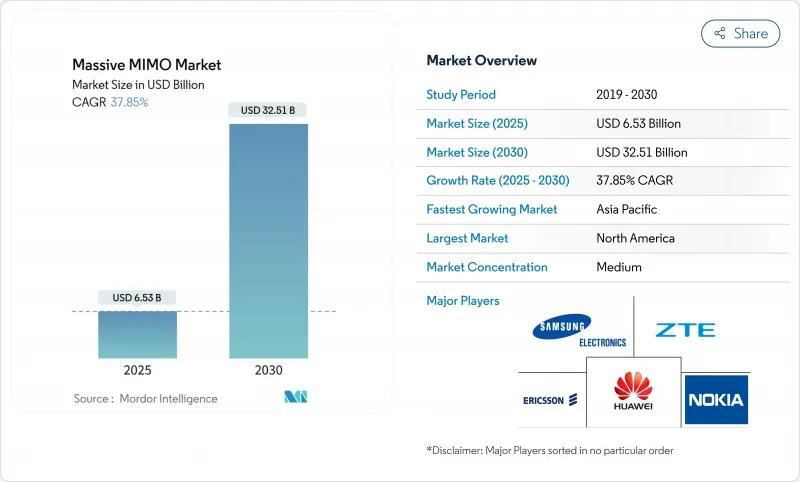

預計到 2025 年,大規模 MIMO 市場價值將達到 65.3 億美元,到 2030 年將成長至 325.1 億美元。

這反映了 37.85% 的複合年成長率,證實了該技術在 5G 部署中的戰略重要性。

大規模MIMO市場正受惠於全球整體5G裝置量的持續成長,預計到2029年,5G用戶數將達到83億人。此外,私有5G網路的日益普及以及對開放式RAN架構的政策支持,都促進了多廠商生態系統的發展。硬體廠商也積極研發更高階的陣列,例如128T128R和512T512R,以提高單站點吞吐量。營運商則部署了原生AI節能軟體,以實現淨零排放目標。工業IoT和固定無線存取等應用情境的不斷湧現將進一步提升對大規模MIMO的需求,確保該技術在預測期內繼續成為網路密集化策略的核心。

全球大規模MIMO—市場趨勢與洞察

行動數據流量和設備密度快速成長

預計到2030年,中國的行動數據流量將成長四倍,由此產生的網路密度將使傳統的小區分割策略難以有效應對。固定無線接入線路預計將從2024年的1.6億條成長到2030年的3.5億條,其中80%將由大規模MIMO無線陣列和中興通訊主導的5G-Advanced網路提供服務。工業IoT將進一步加劇網路壓力,中國計畫在2027年建成1萬家無線工廠,每家工廠都將對網路容量提出嚴峻的效能要求。隨著5G在主要市場的滲透率超過75.9%,小區邊緣的擁塞將加劇,波束成形對於維持一致的使用者體驗至關重要。因此,大規模MIMO市場與流量成長直接相關,使營運商能夠在不按比例擴展站點的情況下滿足吞吐量需求。

5G NR(6GHz 以下頻段和毫米波)在全球範圍內的快速部署

根據愛立信預測,到2024年底,全球獨立組網(SA)5G用戶數預計將達到12億,到2030年將達到36億。中國計劃到2025年新建450萬個5G基地台,並強制要求大規模MIMO作為新基地台的預設天線系統。愛立信表示,毫米波技術的經濟效益將在2025年得到提升,屆時愛立信、NBN公司和高通公司將展示一條基於先進波束成形技術的14公里Gigabit鏈路。私有5G將在2024年推動無線接取網路(RAN)營收成長超過40%,而干擾管理無線電技術對於保障服務等級協定(SLA)至關重要。

射頻前端的高單位成本與高功耗

中國佔據全球98%的氮化鎵晶圓產量,引發了人們對射頻前端模組(高階陣列的關鍵組件)供應穩定性和價格的擔憂。受行動電話需求疲軟的影響,組件製造商Qorvo在2025年第三季的營收下降了12.4%。人工智慧驅動的節能演算法可以將無線電消費量降低高達80%,但所需的額外矽材料會增加組件成本,直到產量擴大。儘管美國國防部正在資助一項國內鎵加工試點項目,但商業化生產要到2027年或更晚才能實現,這將使營運商面臨外匯波動和出口限制的風險。這些因素將限制成本敏感地區的用戶立即採用該技術,並促使他們推遲升級計劃。

細分市場分析

5G NR 6GHz 以下頻段技術預計在 2024 年將佔總收入的 58%,其傳播特性支援廣域覆蓋和室內穿透,使其成為早期 5G推出的首選方案。此頻段受益於多個地區中頻段分配的協調統一,簡化了設備生態系統並降低了無線電成本。相較之下,目前僅應用於高階場景的 5G NR 毫米波技術正以 39.8% 的複合年成長率成長,顯示其在固定無線存取和體育場館熱點領域的應用正在加速。隨著營運商複製澳洲 14 公里農村鏈路的成功經驗,毫米波 MIMO 的龐大市場規模預計將顯著擴大,這證明了高頻段在非都市區寬頻領域的經濟效益。

儘管如此,6GHz以下頻段對於控制平面錨定仍然至關重要,它使通訊業者能夠實施兼顧覆蓋範圍和容量的均衡頻率策略。 Reliance Jio 的 AirFiber 測試表明,與光纖相比,毫米波固定無線接入 (FWA) 可縮短最後一公里部署時間。雖然日本的 5G 私有化牌照政策仍偏向 6GHz以下頻段,但倉庫中早期的毫米波計劃預示著未來將出現多元化發展。隨著設備成本的下降和 5G-Advanced 傳播增強技術的成熟,毫米波的市場佔有率預計將上升,到 2030 年,其在龐大的 MIMO 市場收入中所佔佔有率將不斷成長。

64T64R面板憑藉其在高小區邊緣吞吐量、可控重量和功耗方面的出色平衡,預計在2024年將佔據39%的市場佔有率。營運商在升級高密度城域宏基地台時更傾向於選擇這種規格,因為它安裝時所需的結構加固極少。隨著廠商不斷提升散熱器效率,以及人工智慧工具降低波束校準成本,128T128R及更高規格的面板將以41.2%的複合年成長率成長。喬治亞研究展示了一種支援27-41 GHz頻段大量單元的接收器架構,證明了超大型陣列的可行性。

隨著應用領域朝向延展實境(XR)和工業機器人發展,對穩定多Gigabit吞吐量的需求日益成長,通訊業者測試256單元原型。預計到2030年,128T128R系統的大規模MIMO市場規模將達到119億美元,佔總營收的36.6%。高通的4096單元千兆MIMO概念展示了實現容量階躍式提升的途徑。短期內,32T32R陣列將繼續維持分層市場結構,以滿足農村地區和成本敏感型部署的需求,在這些地區,由於塔架負載容量的限制,無法使用更重的面板。

大型 MINO 市場報告按技術(LTE (4G)、5G NR Sub-6 GHz、其他)、天線類型(16T16R、32T32R、其他)、部署類型(集中式 (C-RAN)、分散式 RAN、其他)、架構(時分雙工 (TDD)、頻分雙工 (FDD)、其他市場細分、其他行動)。

區域分析

2024年,北美將貢獻全球40%的收入,這主要得益於C頻段的積極部署、企業級固定無線接入網(FWA)的普及以及有利於開放式無線接入網(Open RAN)的政策。 Verizon計劃在2025年投入175億至185億美元,其中相當一部分將用於升級64T64R扇區,以保持其每用戶吞吐量的競爭力。加拿大電信公司TELUS與三星合作,推出首個全國性虛擬化無線存取網路(VRAN)。美國聯邦通訊委員會(FCC)關於70/80/90GHz回程傳輸和37GHz頻譜共享的改革,進一步拓展了毫米波在農村寬頻領域的商業價值。

亞太地區預計將成為成長最快的地區,到2030年將以37.89%的複合年成長率成長。中國在2025年3月前已建成超過440萬個5G基地台,並承諾在年底前新增450萬基地台。印度預計將在2024年下半年實現全國5G覆蓋,其中Reliance Jio將佔據85%的活躍小區,從而為32T32R和64T64R無線電模組創造巨大的採購管道。政府的「Bharat 6G」等計畫將強調本土研發,並可能重塑區域廠商市場佔有率格局。中國聯通宣布,將在2025年底前覆蓋300個城市的5G-Advanced網路,將進一步增加天線訂單。

在歐洲,營運商在謹慎擴張的同時,也在努力平衡資本效率和監管機構對供應商多元化的審查。三星和O2 Telefónica將於2024年運作德國首個採用64T64R無線電技術的商用虛擬無線接取網路(vRAN)站點,顯示市場對測試解耦式協定堆疊的需求旺盛。愛立信和MasOrange在西班牙展示了開放式可編程網路,重點關注自動化和能源最佳化,而不是單純的容量。法國和義大利的頻譜競標傾向於3.4-3.8 GHz頻段的連續頻段,進一步鞏固了TDD的主導地位。因此,在對每瓦性能和供應鏈韌性的關注驅動下,歐洲大規模MIMO市場正保持著穩健而適度的成長。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 行動數據流量和設備密度快速成長

- 5G NR(6GHz 以下和毫米波)在全球快速部署

- 高效率的波束成形技術可降低營運商的資本支出。

- 支援多廠商mMIMO的Open-RAN催化劑

- AI輔助細胞邊緣光束最佳化

- 市場限制

- 射頻前端單位成本高、功耗大

- 複雜的站點級部署與維護

- 半導體級氮化鎵 (GaN) 供應風險

- 抵禦電磁輻射和城市足跡

- 價值鏈分析

- 監管環境

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 透過技術

- LTE(4G)

- 5G NR sub-6GHz

- 5G NR 毫米波

- 依天線類型

- 16T16R

- 32T32R

- 64T64R

- 128T128R 或更高版本

- 依部署類型

- 集中式(C-RAN)

- 分散式無線存取網

- 開放式無線接取網

- 建築設計

- 時分雙工(TDD)

- 頻分雙工(FDD)

- 混合雙股

- 透過最終用戶應用程式

- 行動網路營運商

- 企業及私人網路

- 公共與國防

- 固定無線接入(FWA)

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 其他南美洲

- 歐洲

- 德國

- 英國

- 法國

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- ASEAN

- 亞太其他地區

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Samsung Electronics

- Ericsson

- Huawei

- Nokia

- ZTE

- Qualcomm

- Intel

- Texas Instruments

- Qorvo

- NEC

- Fujitsu

- CommScope

- Airspan Networks

- Mavenir

- Parallel Wireless

- Keysight Technologies

- Rohde and Schwarz

- Viavi Solutions

- Analog Devices

- Renesas

第7章 市場機會與未來展望

The massive MIMO market stood at USD 6.53 billion in 2025 and is projected to expand to USD 32.51 billion by 2030, reflecting a vigorous 37.85% CAGR that confirms the technology's strategic importance for 5G roll-outs.Steady operator migration from broad-coverage roll-outs toward capacity-oriented urban deployments is amplifying demand, because beamforming increases spectral efficiency and lifts average revenue per user.

The massive MIMO market receives additional momentum from an installed base headed toward 8.3 billion global 5G subscriptions by 2029, greater adoption of private 5G networks, and policy support for Open RAN architectures that encourage multi-vendor ecosystems. Hardware vendors are also moving to higher-order 128T128R and 512T512R arrays, which multiply throughput per site, while operators deploy AI-native energy-saving software to meet net-zero goals. Emerging industrial IoT and fixed-wireless-access use cases add incremental site demand, ensuring that the technology remains the backbone of network densification strategies over the forecast period.

Global Massive MIMO Market Trends and Insights

Surging Mobile-Data Traffic and Device Density

China expects mobile data traffic to quadruple by 2030, creating density levels that legacy cell-splitting strategies cannot manage cost-effectively. Fixed-wireless-access lines are forecast to climb from 160 million in 2024 to 350 million by 2030, with 80% serviced by 5 G-Advanced networks anchored by massive MIMO radio arrays, ZTE. Industrial IoT adds further load; China targets 10,000 wireless-enabled factories by 2027, each placing tight performance constraints on network capacity. As 5G penetration exceeds 75.9% in leading markets, congestion at the cell edge intensifies, making beamforming vital for sustaining a consistent user experience. The massive MIMO market, therefore, aligns directly with traffic growth, positioning operators to meet throughput needs without proportional site expansion.

Rapid Global Roll-out of 5G NR (Sub-6 GHz and mmWave)

Standalone 5G subscriptions reached 1.2 billion worldwide by end-2024 and are forecast to touch 3.6 billion by 2030, according to Ericsson. China plans to add 4.5 million new 5G base stations by 2025, mandating massive MIMO as the default antenna system for fresh sites. India achieved nationwide 5G coverage by October 2024, accelerating demand for high-order arrays during back-haul upgrades. mmWave economics improved in 2025 when Ericsson, NBN Co, and Qualcomm demonstrated 14 km gigabit links that rely on advanced beamforming, according to Ericsson. Private 5G saw over 40% RAN revenue growth in 2024, and interference-managed radios are indispensable for guaranteed service-level agreements.

High Unit Cost and Power-Consumption of RF Front-end

China controls 98% of gallium nitride wafer output, raising supply-security and pricing concerns for RF front-end modules essential in high-order arrays. Component maker Qorvo recorded a 12.4% sales decline in Q3 2025 as handset demand softened, hinting that vendor margins already feel pressure from cost-push inflation. AI-enabled power-saving algorithms can trim radio energy draw by up to 80%, but they require additional silicon, raising bill-of-materials until volume scales. The U.S. Defense Department has funded domestic gallium processing pilots, yet commercial volumes will lag beyond 2027, leaving operators exposed to currency swings and export controls. These factors restrain near-term adoption in cost-sensitive geographies and encourage deferred upgrades.

Other drivers and restraints analyzed in the detailed report include:

- Operator CAPEX Savings via Beamforming Efficiency

- Open RAN Catalysts Enabling Multi-vendor Massive MIMO

- Complex Site-level Deployment and Maintenance

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

5G NR Sub-6 GHz technology commanded 58% revenue in 2024 because its propagation traits support wide-area coverage and indoor penetration, making it the default option for early 5G launches. The segment benefited from harmonized mid-band allocations across several regions, which streamlined device ecosystems and reduced radio costs. In contrast, 5G NR mmWave occupies only premium use cases today, but its 39.8% CAGR indicates accelerating take-up in fixed wireless access and stadium hotspots. The massive MIMO market size for mmWave is projected to widen significantly as operators replicate the 14 km rural link success in Australia, proving high-frequency economics for non-urban broadband.

The Sub-6 layer nevertheless remains essential for control-plane anchoring, giving carriers a balanced spectrum strategy that marries coverage and capacity. Reliance Jio's AirFiber trials show mmWave FWA cutting last-mile rollout times compared with fiber. Japan's private 5G licensing landscape still favors Sub-6, but early mmWave projects in warehouses hint at forthcoming diversification. Once device costs fall and propagation enhancements mature under 5G-Advanced, the mmWave share should climb, contributing a rising portion of the massive MIMO market revenue through 2030.

64T64R panels held 39% volume share in 2024 by balancing high cell-edge throughput with manageable weight and power draw. Operators favor this format when upgrading macro sites in dense metros because installation requires minimal structural reinforcement. The 128T128R and larger class will register a 41.2% CAGR as vendors improve heat-sink efficiency and as AI tools mitigate beam calibration overhead. Research at Georgia Tech demonstrates receiver architectures that support substantial element counts across 27-41 GHz bands, signaling practical viability for extremely large-scale arrays.

As applications migrate toward XR and industrial robotics, demand for consistent multi-gigabit throughput climbs, prompting carriers to test 256-element prototypes. The massive MIMO market size for 128T128R systems is projected to reach USD 11.9 billion by 2030, equal to 36.6% of overall sales. Qualcomm's 4,096-element Giga-MIMO concept underlines the runway for step-function capacity gains, although commercial adoption is likely after 2028 when power-amplifier efficiency improves. Near-term, 32T32R arrays still serve rural and cost-sensitive deployments where tower loading limits preclude heavier panels, preserving a multi-tier market structure.

Massive MINO Market Report is Segmented by Technology (LTE (4G), 5G NR Sub-6 GHz, and More), Antenna Type (16T16R, 32T32R, and More), Deployment Type (Centralised (C-RAN), Distributed RAN, and More), Architecture (Time-Division Duplex (TDD), Frequency-Division Duplex (FDD), and More), End-User Application (Mobile Network Operators, Enterprises and Private Networks, and More), and Geography.

Geography Analysis

North America generated 40% of global revenue in 2024 on the back of aggressive C-band roll-outs, enterprise FWA adoption, and favorable policy toward Open RAN. Verizon plans USD 17.5-18.5 billion in 2025 capital outlays, a sizable share earmarked for 64T64R sector upgrades that keep per-subscriber throughput competitive. Canada's TELUS is partnering with Samsung to deploy the first nationwide virtualized RAN, underscoring regional appetite for software-defined radios. FCC reforms around 70/80/90 GHz backhaul and 37 GHz sharing further broaden mmWave business cases for rural broadband.

Asia Pacific is the fastest-growing territory, forecast at 37.89% CAGR to 2030 as China surpasses 4.4 million 5G sites by March 2025 and commits to 4.5 million additional base stations within the year. India reached nationwide 5G coverage in late 2024, with Reliance Jio responsible for 85% of active cells, creating a sizable procurement funnel for 32T32R and 64T64R radios. Government programs such as Bharat 6G emphasize indigenous R&D, potentially reshaping regional vendor shares. China Unicom's 5G-Advanced coverage across 300 cities by end-2025 further raises antenna order volumes, providing economies of scale that exert downward price pressure globally.

Europe shows measured expansion as operators juggle capital efficiency and regulatory scrutiny over vendor diversification. Samsung and O2 Telefonica activated Germany's first commercial vRAN site with 64T64R radios in 2024, signaling market willingness to test disaggregated stacks. Ericsson and MasOrange demonstrated an open programmable network in Spain, focusing on automation and energy optimization rather than raw capacity. Spectrum auctions in France and Italy favored contiguous 3.4-3.8 GHz blocks, reinforcing TDD dominance. The European massive MIMO market therefore emphasizes performance per watt and supply-chain resilience, supporting gradual but firm growth.

- Samsung Electronics

- Ericsson

- Huawei

- Nokia

- ZTE

- Qualcomm

- Intel

- Texas Instruments

- Qorvo

- NEC

- Fujitsu

- CommScope

- Airspan Networks

- Mavenir

- Parallel Wireless

- Keysight Technologies

- Rohde and Schwarz

- Viavi Solutions

- Analog Devices

- Renesas

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging mobile-data traffic and device density

- 4.2.2 Rapid global roll-out of 5G NR (Sub-6 GHz and mmWave)

- 4.2.3 Operator CAPEX savings via beam-forming efficiency

- 4.2.4 Open-RAN catalysts enabling multi-vendor mMIMO

- 4.2.5 AI-assisted cell-edge beam-optimization

- 4.3 Market Restraints

- 4.3.1 High unit cost and power-consumption of RF front-end

- 4.3.2 Complex site-level deployment and maintenance

- 4.3.3 Semiconductor-grade gallium nitride (GaN) supply risk

- 4.3.4 EMF-exposure and urban footprint opposition

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Technology

- 5.1.1 LTE (4G)

- 5.1.2 5G NR Sub-6 GHz

- 5.1.3 5G NR mmWave

- 5.2 By Antenna Type

- 5.2.1 16T16R

- 5.2.2 32T32R

- 5.2.3 64T64R

- 5.2.4 128T128R and Above

- 5.3 By Deployment Type

- 5.3.1 Centralised (C-RAN)

- 5.3.2 Distributed RAN

- 5.3.3 Open RAN

- 5.4 By Architecture

- 5.4.1 Time-Division Duplex (TDD)

- 5.4.2 Frequency-Division Duplex (FDD)

- 5.4.3 Hybrid Duplex

- 5.5 By End-user Application

- 5.5.1 Mobile Network Operators

- 5.5.2 Enterprises and Private Networks

- 5.5.3 Public Safety and Defence

- 5.5.4 Fixed Wireless Access (FWA)

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Russia

- 5.6.3.5 Rest of Europe

- 5.6.4 Asia Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 ASEAN

- 5.6.4.6 Rest of Asia Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 UAE

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Samsung Electronics

- 6.4.2 Ericsson

- 6.4.3 Huawei

- 6.4.4 Nokia

- 6.4.5 ZTE

- 6.4.6 Qualcomm

- 6.4.7 Intel

- 6.4.8 Texas Instruments

- 6.4.9 Qorvo

- 6.4.10 NEC

- 6.4.11 Fujitsu

- 6.4.12 CommScope

- 6.4.13 Airspan Networks

- 6.4.14 Mavenir

- 6.4.15 Parallel Wireless

- 6.4.16 Keysight Technologies

- 6.4.17 Rohde and Schwarz

- 6.4.18 Viavi Solutions

- 6.4.19 Analog Devices

- 6.4.20 Renesas

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

大規模MIMO市場機會、成長要素、產業趨勢分析及2026-2035年預測

大規模MIMO市場機會、成長要素、產業趨勢分析及2026-2035年預測 大規模MIMO市場:依組件、頻段、天線數量、應用、部署模式及最終用戶產業分類-2026-2032年全球市場預測

大規模MIMO市場:依組件、頻段、天線數量、應用、部署模式及最終用戶產業分類-2026-2032年全球市場預測 大規模MIMO全球市場規模、佔有率、趨勢和成長分析報告,2026-2034年

大規模MIMO全球市場規模、佔有率、趨勢和成長分析報告,2026-2034年 2026年全球大規模MIMO市場報告

2026年全球大規模MIMO市場報告 5G 大規模 MIMO

5G 大規模 MIMO 大規模MIMO市場規模、佔有率和成長分析(按頻段、天線頻段、技術和地區分類)-2026-2033年產業預測大規模 MIMO 的全球市場:到 2033 年的機會與策略

大規模MIMO市場規模、佔有率和成長分析(按頻段、天線頻段、技術和地區分類)-2026-2033年產業預測大規模 MIMO 的全球市場:到 2033 年的機會與策略 Massive MIMO市場:全球產業分析,規模,佔有率,成長,趨勢,預測,2024年~2032年

Massive MIMO市場:全球產業分析,規模,佔有率,成長,趨勢,預測,2024年~2032年