|

市場調查報告書

商品編碼

1850286

農場管理軟體:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)Farm Management Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

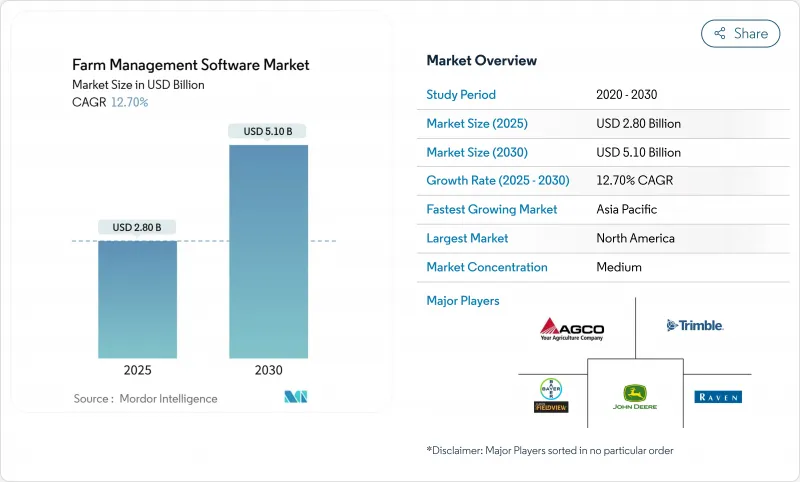

預計到 2025 年,農場管理軟體市場規模將達到 28 億美元,到 2030 年將達到 51 億美元,年複合成長率為 12.70%。

全球農業面臨多重壓力,推動了兩位數的強勁成長:結構性農業勞動力短缺、耕地面積減少、氣候相關的生產風險,以及下游買家對永續性指標的檢驗需求。雲端交付平台佔據了目前部署的大部分佔有率,因為它們可以降低前期投資成本、實現自動升級,並支援各種規模農場即時整合感測器、機械、衛星和氣象數據。雖然精密農業仍然是主要應用場景,但水產養殖軟體的成長速度最快,因為對永續蛋白質的需求促使生產者轉向數據主導的水質和飼料效率管理。亞太地區是成長最快的地區,這得益於大規模的公共數位農業項目,而北美地區憑藉早期採用的優勢和成熟的經銷商支持網路,仍然是收入領先者。設備製造商、投入品供應商和新興企業正在建立開放API生態系統,以產生持續的訂閱收入,並競相將農場管理軟體市場定位在更廣泛的農業技術體系的核心位置。

全球農場管理軟體市場趨勢與洞察

農業勞動力短缺和耕地減少正在推動農業機械化。

農場管理軟體作為數位骨幹,協調自動駕駛曳引機、機器人收割機和精準噴藥機,從而實現全天候運作,且人事費用低於傳統人工。 Bluewhite 的售後自動化套件透過雲端控制面板進行整合,可規劃設備路線並近乎即時地監控機器運行狀況,從而展現出整個作業季的投資回報。隨著土地資源日益稀缺,種植者利用基於精細地理空間分析的變數施肥方案,最大限度地提高單位面積產量。全球收割自動化舉措旨在十年內實現美國一半特種作物收割的機械化。這目標的前提是廣泛部署資料編配平台,以便在動態的田間條件下同步多個自主單元。勞動力短缺和土地稀缺的雙重困境,使得農場管理軟體市場成為關鍵基礎設施,而非可有可無的技術。

精密農業技術的快速整合創造了平台需求

農場感測器、無人機影像和機器遙測技術的爆炸性成長正在產生Petabyte的數據。早期採用變數播種結合感測器驅動的施肥調整技術的農戶報告稱,在保持產量的同時,農藥和養分用量最多可節省80%,軟體訂閱成本可在兩年內收回。農場管理平台正日益成為整合中心,將土壤濕度探頭、氣象站和引擎CAN總線資料整合到一個統一的控制面板中。約翰迪爾的「See and Spray」技術已在超過一百萬英畝的土地上部署,證明演算法定向噴灑可以減少除草劑的使用,同時降低碳排放。歐盟已累計「地平線歐洲」計畫的資金,用於在2024年至2027年間將類似的數位基礎設施擴展到27.4萬個農場。隨著硬體多樣性的增加,基於開放API的農場管理軟體自然成為控制中心。

小農戶的主導地位限制了軟體投資報酬率

小農戶耕種面積佔全球農業用地面積的80%,但耕地面積通常不到5公頃,收入不足以支付綜合軟體訂閱費用。撒哈拉以南非洲的縱向研究表明,信貸取得、數位素養和推廣支持是技術採納的關鍵促進因素,任何一個因素的缺失都會減緩採納速度。肯塔基州的一項研究證實了耕地面積與精準農業技術採納之間存在正相關關係,而老農戶即使被告知成本效益,仍然抵制數位化介面。拉丁美洲的評估報告指出,根深蒂固的文化習俗和不穩定的網路連結也是阻礙技術採納的因素。因此,農場管理軟體市場將呈現兩極化的成長模式:一方面,大型商業生產者的需求強勁;另一方面,以自給自足為導向的小農戶(他們在亞洲和非洲的糧食系統中佔據主導地位)的採納速度較慢。

細分市場分析

雲端部署將在2024年創造最大收益,佔據農場管理軟體市場52%的佔有率,當年達到14.6億美元,並預計到2030年將以17.40%的複合年成長率成長。在雲端環境中,軟體即服務(SaaS)訂閱模式佔據主導地位。自動更新消除了停機時間,而多租戶架構則將固定成本分攤到數千用戶身上。雖然本地和基於Web的系統仍然服務於那些對資料主權有嚴格要求的公司,但區域頻寬的升級正在縮小這個市場。約翰迪爾的營運中心展示了雲端聚合如何實現單一租戶本地部署無法實現的跨農場基準化分析。包括現場級加密和多因素身份驗證在內的日益成熟的安全通訊協定,也緩解了先前用戶對雲端技術的猶豫。

由於機器學習演算法會隨著資料量的增加而變得更加精準,網路效應放大了雲端運算的價值。一個基於500萬個匿名樣本訓練的土壤有機碳預測工具,可將實驗室檢測成本降低60%,使用戶無需離開原有生態系統即可受益。受平台即服務(PaaS)層驅動的農場管理軟體市場規模預計將在2030年前持續成長,因為獨立開發者會部署微服務(例如,在地化灌溉調度器),這些微服務無需大量編碼即可連接到綜合儀表板。現今,供應商之間的競爭主要圍繞著開放API庫和第三方應用收益分成框架展開,這使得雲端運算模式的戰略意義日益凸顯。

區域分析

北美仍是最大的收入貢獻者,佔市場佔有率的34%。這部分歸功於當地田間設備已具備遙測功能,且平台啟動簡便。美國農業部「氣候智慧型商品」配額政策推動了對合規模組的需求,經銷商網路也提供現場培訓以彌補技能缺口。玉米帶地區企業的雲端滲透率超過70%,農場將2-5%的收入用於數位化工具,鞏固了該地區的市場主導地位。隨著早期採用者逐漸飽和市場,成長將放緩至11.10%的複合年成長率,但特種作物和再生農業實踐檢驗領域仍有成長機會。

亞太地區以16.20%的複合年成長率引領全球成長,這得益於中國、印度和東南亞國家政策支持的數位化項目。印度耗資64億美元的「數位農業計畫」旨在整合覆蓋400個地區的感測器數據和衛星影像,從而有效地為數千萬小農戶承擔平台費用。中國各省的試點計畫正在將農業軟體融入金融服務流程,使投入貸款與檢驗的產量預測掛鉤。儘管整體農業食品科技領域的資金籌措有所萎縮,但創投仍保持韌性,預計2024年,區域農業軟體新興企業將籌集3億美元資金。然而,農場規模通常小於5公頃,限制了技術的規模化應用。每月30美元的套餐費用往往超過農場淨收入,減緩了自給自足型農民的接受度。

歐洲9.40%的複合年成長率反映了精準農業技術的持續成熟應用,這主要得益於通用農業政策中關於數位化記錄保存的規定。 「地平線歐洲」津貼撥款7億歐元(約8.03億美元)用於精密農業試點項目,這些項目需要一個整合的軟體平台。法國的「大規模田間舉措」等國家計畫將設備補貼與強制性數據共用框架結合,進一步鞏固了開放標準平台。小型家庭農場面臨傳承方面的挑戰,因此需要支持能夠簡化代際知識傳承的數位化工具。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 農業勞動力短缺和耕地減少

- 快速整合精密農業技術

- 政府數位農業獎勵和補貼

- 對即時農業決策支援的需求

- 透過FMS平台實現碳權貨幣化

- 一個開放的 API 生態系統,可建立超級應用農場平台

- 市場限制

- 小農場的優勢

- 軟體、硬體和培訓的前期成本很高

- 農民的資料隱私和網路安全問題

- 農村地區農業資料科學人才短缺

- 監管環境

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 按類型

- 本地/網路

- 雲端基礎的

- Software as a Service(SaaS)

- Platform as a Service(PaaS)

- 透過使用

- 精密農業

- 牲畜監測

- 智慧溫室

- 水產養殖

- 其他用途

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 北美其他地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 亞太其他地區

- 中東

- 沙烏地阿拉伯

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 肯亞

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Trimble Inc.

- Climate LLC.(Bayer AG)

- Farmers Edge Inc.

- Deere & Company

- AGCO Corporation

- Raven Industries(CNH Industrial)

- Topcon Corp.

- AGRIVI Ltd.

- CropX Technologies Ltd.

- Traction Ag Inc.

- SemiosBio Technologies

- CropZilla Software Inc.

- BASF Digital Farming GmbH(BASF SE)

- Ag Leader Technology(Ag Leader)

- Eagle IoT(Bentley Systems)

第7章 市場機會與未來展望

The farm management software market size is valued at USD 2.80 billion in 2025 and is forecast to reach USD 5.10 billion by 2030, expanding at a 12.70% CAGR.

Solid double-digit growth stems from converging pressures on global agriculture: structural farm-labor shortages, shrinking arable land, climate-induced production risk, and the need to verify sustainability metrics for downstream buyers. Cloud-delivered platforms dominate current deployments because they lower upfront capital outlays, automate upgrades, and allow farms of every size to integrate sensor, machine, satellite, and weather data in real time. Precision farming remains the primary use case, yet aquaculture software is registering the fastest growth as demand for sustainable protein pushes producers toward data-driven water-quality and feed-efficiency management. Asia-Pacific is the highest-growth region thanks to large-scale public digital-agriculture programs, while North America remains the revenue leader on the strength of early adoption and entrenched dealer support networks. Competitive intensity is rising as equipment manufacturers, input suppliers, and start-ups race to build open-API ecosystems that lock in recurring subscription revenue and position the farm management software market at the center of the broader ag-tech stack.

Global Farm Management Software Market Trends and Insights

Farm-Labor Shortage and Decreasing Arable Land Push Mechanization

Farm management software acts as the digital backbone that coordinates autonomous tractors, robotic harvesters, and precision sprayers, allowing 24-hour operation with lower labor costs than traditional crews. Bluewhite's aftermarket autonomy kits demonstrate a full season payback when integrated through cloud dashboards that schedule equipment routes and monitor near-real-time machine health. As land availability tightens, producers maximize yield per acre through variable rate prescriptions driven by detailed geospatial analytics. The Global Harvest Automation Initiative targets mechanizing half of the United States specialty-crop harvesting within a decade, a goal that presumes wide deployment of data-orchestrating platforms able to synchronize multiple autonomous units across dynamic field conditions. The intersection of labor shortages and land pressure cements the farm management software market as critical infrastructure rather than optional technology.

Rapid Integration of Precision-Agriculture Technologies Creates Platform Demand

The explosive growth of on-farm sensors, drone imagery, and machine telemetry generates petabytes of data that must be harmonized before it can guide timely field decisions. Early adopters who combined variable rate seeding with sensor-driven fertilizer adjustments reported pesticide and nutrient savings up to 80% while maintaining yield, enabling two-year payback periods on software subscriptions. Farm management platforms increasingly serve as integration hubs, merging soil-moisture probes, weather stations, and engine CAN bus feeds into cohesive dashboards. John Deere's See and Spray technology, deployed on more than 1 million acres, underscores how algorithm-controlled targeting slashes herbicide use while simultaneously reducing carbon footprint. The European Union earmarked Horizon Europe funds to extend similar digital infrastructure to 274,000 farms between 2024 and 2027, amplifying demand for software layers that maintain data interoperability across mixed fleets and vendor ecosystems. As hardware diversity expands, open-API-oriented farm management software becomes the natural control center.

Dominance of Smallholder Farms Limits Software Return on Investment

Smallholders account for 80% of global farm holdings, yet often cultivate plots under five hectares, generating revenue insufficient to offset comprehensive software subscriptions. Longitudinal studies in Sub-Saharan Africa show that credit access, digital literacy, and extension support are decisive factors in technology uptake, and deficits in any one dimension derail adoption. Surveys in Kentucky confirm positive correlations between acreage and precision-tech adoption, while older farmer demographics resist digital interfaces even after cost-benefit explanations. Latin American evaluations highlight entrenched cultural practices and unreliable connectivity as additional barriers. Consequently, the farm management software market sees bifurcated growth, with robust demand from large commercial growers and slower penetration among subsistence-oriented smallholders that dominate food systems in Asia and Africa.

Other drivers and restraints analyzed in the detailed report include:

- Government Digital-Agriculture Incentives Accelerate Platform Adoption

- Demand for Real-Time Agronomic Decision Support Drives Platform Sophistication

- High Upfront Software, Hardware, and Training Costs Create Adoption Barriers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud deployment registered the largest 2024 revenue and held 52% of the farm management software market share, translating to USD 1.46 billion that year, and is forecast to expand at a 17.40% CAGR through 2030. Within the cloud, Software-as-a-service subscriptions dominate because automatic updates eliminate downtime, and multi-tenant architecture spreads fixed costs over thousands of users. Local and web-based systems continue to serve enterprises with strict data sovereignty requirements, yet bandwidth upgrades across rural corridors shrink that niche. John Deere's Operations Center illustrates how cloud aggregation allows cross-farm benchmarking that single-tenant local deployments cannot match. Security protocols have matured to include field-level encryption and multi-factor authentication, easing earlier adoption hesitations.

Network effects amplify the value of the cloud because machine-learning algorithms grow more accurate as data volumes compound. A soil-organic-carbon predictor trained on 5 million anonymized samples cut lab-testing costs by 60%, an advantage that keeps users inside the originating ecosystem. The farm management software market size attributed to Platform as a Service layer is projected to climb through 2030 as independent developers roll out micro-services, for example, localized irrigation schedulers, that plug into overarching dashboards without heavy coding requirements. Vendor competition now centers on open-API libraries and revenue-sharing frameworks for third-party apps, reinforcing the cloud model's strategic importance.

The Farm Management Software Market is Segmented by Type (Local/Web-based and Cloud-Based), Application (Precision Farming, Livestock Monitoring, Smart Greenhouse, Aquaculture, and Other Applications), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America remains the largest revenue contributor, accounting for 34% in market revenue, in part because field equipment already arrives telemetry-ready, making platform activation straightforward. The USDA's Climate-Smart Commodities allocations drive demand for compliance modules, while dealer networks provide on-site training that bridges skill gaps. Cloud penetration exceeds 70% among corn belt enterprises, and farms devote 2-5% of revenue to digital tools, cementing the region's primacy. Growth moderates to 11.10% CAGR because early adopters saturate the market, yet opportunities persist in specialty crops and regenerative-practice verification.

Asia-Pacific propels global growth with a 16.20% CAGR and benefits from policy-backed digitalization programs in China, India, and Southeast Asian nations. India's USD 6.40 billion Digital Agriculture Mission aims to integrate sensor data and satellite imagery across 400 districts, effectively underwriting platform costs for tens of millions of smallholders. Chinese provincial pilots embed farm software into financial services workflows, enabling input loans contingent on verified yield forecasts. Venture investment remained resilient, with regional farm-software start-ups raising USD 300 million in 2024 despite broader agrifood-tech funding contraction. Nevertheless, sub-five-hectare farm structures constrain addressable penetration; packages priced at USD 30 per month often exceed net farm income, explaining slower uptake among subsistence operators.

Europe's 9.40% CAGR reflects consistent but mature adoption, bolstered by Common Agricultural Policy stipulations for digital record keeping. Horizon Europe grants channel EUR 700 million (USD 803 million) into precision-farming pilots that require integrated software backbones. National programs such as France's Large-Scale Field Demo initiative couple equipment subsidies with mandatory data-sharing frameworks, further entrenching open-standards platforms. Smaller family farms face succession challenges, and digital tools that simplify multi-generational knowledge transfer gain traction.

- Trimble Inc.

- Climate LLC. (Bayer AG)

- Farmers Edge Inc.

- Deere & Company

- AGCO Corporation

- Raven Industries (CNH Industrial)

- Topcon Corp.

- AGRIVI Ltd.

- CropX Technologies Ltd.

- Traction Ag Inc.

- SemiosBio Technologies

- CropZilla Software Inc.

- BASF Digital Farming GmbH (BASF SE)

- Ag Leader Technology (Ag Leader)

- Eagle IoT (Bentley Systems)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Farm-labor shortage and decreasing arable land

- 4.2.2 Rapid integration of precision-agriculture technologies

- 4.2.3 Government digital-agriculture incentives and subsidies

- 4.2.4 Demand for real-time agronomic decision support

- 4.2.5 Monetization of carbon credits through FMS platforms

- 4.2.6 Open-API ecosystems enabling super-app farm platforms

- 4.3 Market Restraints

- 4.3.1 Dominance of smallholder farms

- 4.3.2 High upfront software, hardware and training costs

- 4.3.3 Farmer data-privacy and cyber-security concerns

- 4.3.4 Shortage of ag-data science talent in rural areas

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 By Type

- 5.1.1 Local/Web-based

- 5.1.2 Cloud-based

- 5.1.2.1 Software as a Service (SaaS)

- 5.1.2.2 Platform as a Service (PaaS)

- 5.2 By Application

- 5.2.1 Precision Farming

- 5.2.2 Livestock Monitoring

- 5.2.3 Smart Greenhouse

- 5.2.4 Aquaculture

- 5.2.5 Other Applications

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 South America

- 5.3.2.1 Brazil

- 5.3.2.2 Argentina

- 5.3.2.3 Rest of South America

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Spain

- 5.3.3.5 Russia

- 5.3.3.6 Rest of Europe

- 5.3.4 Asia-Pacific

- 5.3.4.1 China

- 5.3.4.2 India

- 5.3.4.3 Japan

- 5.3.4.4 Australia

- 5.3.4.5 Rest of Asia-Pacific

- 5.3.5 Middle East

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 Turkey

- 5.3.5.3 Rest of Middle East

- 5.3.6 Africa

- 5.3.6.1 South Africa

- 5.3.6.2 Kenya

- 5.3.6.3 Rest of Africa

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes global overview, market-level overview, core segments, financials as available, strategic information, market rank/share, products and services, and recent developments)

- 6.4.1 Trimble Inc.

- 6.4.2 Climate LLC. (Bayer AG)

- 6.4.3 Farmers Edge Inc.

- 6.4.4 Deere & Company

- 6.4.5 AGCO Corporation

- 6.4.6 Raven Industries (CNH Industrial)

- 6.4.7 Topcon Corp.

- 6.4.8 AGRIVI Ltd.

- 6.4.9 CropX Technologies Ltd.

- 6.4.10 Traction Ag Inc.

- 6.4.11 SemiosBio Technologies

- 6.4.12 CropZilla Software Inc.

- 6.4.13 BASF Digital Farming GmbH (BASF SE)

- 6.4.14 Ag Leader Technology (Ag Leader)

- 6.4.15 Eagle IoT (Bentley Systems)

7 Market Opportunities and Future Outlook

農業管理軟體市場:依農業類型、功能、部署方式、農場規模及最終用戶分類-2026-2032年全球市場預測

農業管理軟體市場:依農業類型、功能、部署方式、農場規模及最終用戶分類-2026-2032年全球市場預測 2026年全球農場管理軟體市場報告

2026年全球農場管理軟體市場報告 農業企業管理軟體市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶及模組分類

農業企業管理軟體市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶及模組分類 全球農場管理軟體市場規模、佔有率、趨勢和成長分析報告(2026-2034年)農場管理軟體市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察與未來預測(2026-2034)

全球農場管理軟體市場規模、佔有率、趨勢和成長分析報告(2026-2034年)農場管理軟體市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察與未來預測(2026-2034) 農場管理軟體市場-全球產業規模、佔有率、趨勢、機會與預測:按農場類型、農場生產計畫、類型、應用、地區和競爭格局分類,2021-2031年

農場管理軟體市場-全球產業規模、佔有率、趨勢、機會與預測:按農場類型、農場生產計畫、類型、應用、地區和競爭格局分類,2021-2031年 日本農業管理軟體市場報告:依農業部門、實施類型、服務及地區分類,2026-2034年

日本農業管理軟體市場報告:依農業部門、實施類型、服務及地區分類,2026-2034年 農場管理軟體市場預測至2032年:按解決方案、功能、應用、最終用戶和地區分類的全球分析農場管理解決方案市場預測至 2032 年:按組件、部署類型、農場規模、農業類型、最終用戶和地區進行的全球分析

農場管理軟體市場預測至2032年:按解決方案、功能、應用、最終用戶和地區分類的全球分析農場管理解決方案市場預測至 2032 年:按組件、部署類型、農場規模、農業類型、最終用戶和地區進行的全球分析 農場管理軟體市場按應用和地區分類

農場管理軟體市場按應用和地區分類