|

市場調查報告書

商品編碼

1850257

神經網路軟體:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)Neural Network Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

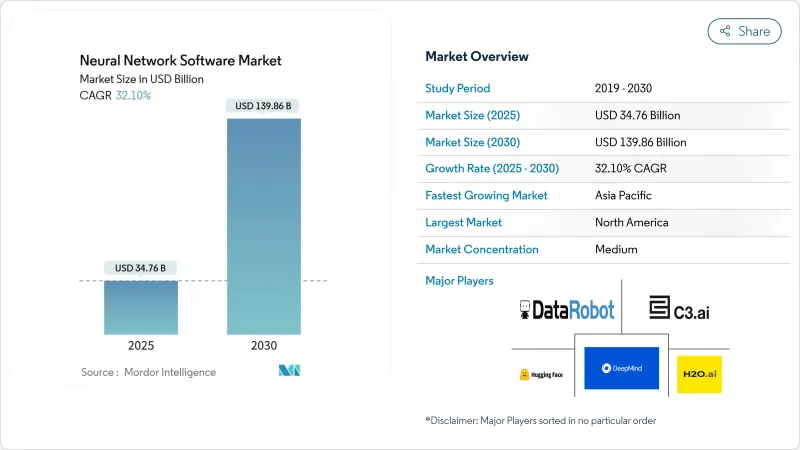

預計到 2025 年,神經網路軟體市場規模將達到 347.6 億美元,到 2030 年將達到 1,398.6 億美元,預測期(2025-2030 年)的複合年成長率為 32.10%。

在自主人工智慧專案、底層模型生態系統以及降低採用門檻的雲端平台的支援下,隨著企業從概念驗證轉向全面部署,人工智慧的擴張速度正在加快。 OpenAI 的收益預計將從 2024 年 12 月的 55 億美元飆升至 2025 年 6 月的 100 億美元,這表明市場對大規模神經網路部署的商業需求日益成長。亞太地區是成長最快的地區,中國、日本、印度和韓國正在將大規模語言模式在地化並建構人工智慧雲端。雖然軟體工具仍佔據大部分市場佔有率,但隨著企業尋求整合和最佳化方面的專業知識,服務也在加速擴張。雲端超大規模雲端超大規模資料中心業者、企業軟體供應商和人工智慧專家競相在模型效率、管治和垂直解決方案方面脫穎而出,競爭日益激烈。

全球神經網路軟體市場趨勢與洞察

雲端基礎的AI平台實現了存取的民主化。

到 2025 年,企業在生成式人工智慧方面的支出將增加 30%,因為中型企業正在採用能夠消除資本障礙的託管平台。紅帽公司收購 Neural Magic 後,在其混合雲產品中新增了一個最佳化的推理庫,從而能夠在私有叢集中高效部署。 Rackspace 的 AI Anywhere 服務以可預測的訂閱價格打包預先建立模型,使缺乏內部專業知識的公司也能實現複雜的神經網路架構。谷歌的 Gemini 系列透過將文字到圖像和視訊生成 API 整合到其標準雲端主機中,進一步擴大了人工智慧的普及範圍,使開發人員無需客製化基礎設施即可測試多模態推理。此類平台措施加快了價值實現速度,並擴大了神經網路軟體在新興企業用戶中的市場。

企業對預測分析的需求日益成長

神經網路在故障預測方面達到了94%的準確率,製造業正從被動維護轉向主動維護。寶馬雷根斯堡工廠透過分析現有零件數據,每年可減少組裝停機時間超過500分鐘,這在工業領域展現了極高的投資報酬率。通用汽車透過將物聯網感測器與人工智慧驅動的調度引擎結合,減少了15%的計畫外停機時間,每年節省2,000萬美元。金融機構也取得了類似的成果,混合深度學習模型能夠偵測出98.7%的詐欺性支付。這些顯著的經濟效益正在加速軟體採購週期,並提高了供應商對快速實施支援的期望。

深度學習 MLOps 人才短缺

僅28%採用人工智慧的公司聘用了專門從事機器學習運維(MLOps)的工程師,而75%的歐洲雇主將在2024年面臨人工智慧職位空缺,這凸顯了技能缺口的持續存在。儘管科技巨頭目前提供認證課程以加速技能提升,但這些課程無法跟上快速變化的框架。如果缺乏足夠的從業人員來實施這些模型,部署時間將會延長,業務收益將會上升,即使需求成長,短期內神經網路軟體市場的獲利能力也會受到限制。

細分分析

至2024年,軟體框架、函式庫和AutoML套件將佔總收入的54.4%,凸顯其作為神經網路軟體市場結構性支柱的地位。雖然TensorFlow、PyTorch和JAX等核心開發套件仍然必不可少,但對縮短實驗週期的承包模組的需求日益成長。隨著企業將整合、調優和生命週期管理外包,包括專業諮詢和託管營運在內的服務正以35.4%的複合年成長率成長。

到2024年,託管服務將佔據神經網路軟體市場35.4%的佔有率,這主要得益於雲端服務供應商將人工智慧專家納入訂閱套餐,並加快產品上市速度。此外,專注於特定領域需求(例如醫療影像合規性)的專業服務團隊也進一步提升了其服務佔有率。在預測期內,供應商之間的差異化將取決於其在特定領域的深度、基於結果的定價以及授權模式。

至2024年,公共雲端將佔據神經網路軟體市場61.3%的佔有率。企業可以按需利用GPU叢集,避免前期投資。然而,主權、延遲和監管要求正在推動市場成長轉向混合部署,預計到2030年,混合部署的複合年成長率將達到34.8%。

在混合架構中,資料儲存在本地或私有雲端中,而模型則在可擴展的公共環境中進行訓練。金融服務和醫療保健提供者正在採用這種拓撲結構,以在利用雲端規模的同時保護敏感資料。機密運算和聯邦學習的日益普及將進一步推動對混合架構的需求,並重塑供應商的資源規劃。

神經網路軟體市場按組件(軟體工具、平台、服務)、部署模式(雲端、本地部署、混合部署)、類型(資料探勘和歸檔、分析軟體、其他)、應用(詐欺偵測、硬體診斷、財務預測、其他)、最終用戶產業(銀行、金融服務和保險、醫療保健、其他)以及地區進行細分。市場預測以美元計價。

區域分析

北美擁有成熟的創業投資生態系統、先進的雲端基礎設施和豐富的人才儲備,預計到2024年營收將成長38.06%。 OpenAI的年度經常性收益翻倍至100億美元,凸顯了其商業性成熟度,而超大規模資料中心營運商也持續拓展其託管人工智慧業務。加拿大正利用蒙特婁和多倫多的學術叢集,但其對亞洲晶片製造的依賴限制了其自主運算能力的提升。墨西哥則利用近岸外包將神經網路解決方案整合到物流和汽車生產中,加強了區域供應鏈。

亞太地區預計將以35.7%的複合年成長率成長,到2030年,隨著中國、日本、印度和韓國採用國家級人工智慧雲端平台,神經網路軟體市場規模預計將達到3,000億美元。中國在44個重點研發領域中領先37個,並投入國家資金用於產業人工智慧升級。日本在印太地區開設了OpenAI的首個辦事處,旨在滿足當地對尊重語言細微差別和資料居住法的企業級GPT解決方案的需求。印度正透過政府沙盒孵化Start-Ups,而澳洲和新加坡則在安全和管治研究方面進行投資,從而創造了多元化的區域機會。

歐洲正透過其「主權人工智慧計畫」(Sovereign AI 計劃)追求技術自主。英偉達(NVIDIA)正向歐洲資料中心合作夥伴提供其3000百億億次浮點運算能力的Blackwell叢集,為受監管的人工智慧工作負載建構覆蓋整個歐洲大陸的脊椎。德國的工業人工智慧雲端和法國通訊業者主導的模式託管中心正在蓬勃發展。然而,人才短缺問題依然存在,75%的就業人員無法勝任人工智慧相關職位,這導致薪資上漲和跨境移民。嚴格的GDPR以及即將推出的人工智慧法律法規對提供管治工具的供應商有利,並正在影響採購優先事項。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概況

- 市場促進因素

- 雲端基礎的AI平台使神經網路普及化

- 企業對預測分析的需求日益成長

- 巨量資料與GPU日益普及

- 基礎模型創造了對新型工具鏈的需求

- 開放原始碼模型市場加速採用

- 自主人工智慧舉措需要本地神經網路堆疊

- 市場限制

- 深度學習MLOps人才短缺

- 資料隱私和管治的負擔

- GPU供應鏈不穩定導致成本上升

- 訓練負荷的能源和ESG審查

- 產業價值鏈分析

- 監管格局

- 技術展望

- 產業吸引力-波特五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

- 影響市場的宏觀經濟因素

第5章 市場規模及成長預測(數值)

- 按組件

- 軟體工具

- 框架和函式庫

- 自動機器學習平台

- 平台(PaaS)

- 服務

- 託管服務

- 專業服務

- 軟體工具

- 透過部署模式

- 雲

- 本地部署

- 混合

- 按類型

- 資料探勘與歸檔

- 分析軟體

- 最佳化軟體

- 視覺化軟體

- 按用途

- 詐欺偵測

- 硬體診斷

- 財務預測

- 影像最佳化

- 預測性維護

- 自然語言處理

- 語音辨識

- 其他

- 按最終用戶

- BFSI

- 衛生保健

- 零售與電子商務

- 國防和政府

- 媒體與娛樂

- 物流與運輸

- 能源和公共產業

- 製造業

- 其他終端使用者區域

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 智利

- 其他南美

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 馬來西亞

- 新加坡

- 澳洲

- 其他亞太地區

- 中東和非洲

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- DataRobot Inc.

- H2O.ai Inc.

- C3.ai Inc.

- Hugging Face Inc.

- DeepMind Technologies Ltd.

- OpenAI Inc.

- Clarifai Inc.

- GMDH LLC

- Neural Designer(Artelnics SL)

- Alyuda Research LLC

- Neural Technologies Ltd.

- Neuralware LLC

- AND Corporation

- Abacus.ai

- OctoML Inc.

- Databricks Inc.

- Seldon Technologies Ltd.

- Weights and Biases Inc.

- Comet ML Inc.

- Run:AI Labs Ltd.

- Lightning AI Inc.

- KNIME AG

- RapidMiner Inc.

- LatticeFlow AG

- Pachyderm Inc.

第7章 市場機會與未來趨勢

- 閒置頻段與未滿足需求評估

The Neural Network Software Market size is estimated at USD 34.76 billion in 2025, and is expected to reach USD 139.86 billion by 2030, at a CAGR of 32.10% during the forecast period (2025-2030).

Expansion is accelerating as enterprises move from proofs of concept to full-scale rollouts, supported by sovereign-AI programs, foundation-model ecosystems, and cloud platforms that lower adoption barriers. OpenAI's revenue jump from USD 5.5 billion in December 2024 to USD 10 billion in June 2025, illustrating rising commercial demand for large-scale neural network deployments. Asia-Pacific is the fastest-growing geography because China, Japan, India, and South Korea are localizing large language models and building national AI clouds. Component trends show software tools retaining the majority share, yet services are expanding faster as enterprises seek integration and optimization expertise. Competition continues to intensify, with cloud hyperscalers, enterprise software vendors, and specialist AI firms racing to differentiate on model efficiency, governance, and vertical solutions.

Global Neural Network Software Market Trends and Insights

Cloud-based AI Platforms Democratize Access

Enterprise generative-AI spending is rising 30% in 2025 as mid-market firms adopt managed platforms that remove capital barriers. Red Hat's purchase of Neural Magic adds optimized inference libraries to its hybrid cloud suite, enabling efficient deployments within private clusters. Rackspace's AI Anywhere service packages pre-built models with predictable subscription pricing, making complex neural network architectures attainable for firms lacking in-house expertise. Google's Gemini family extends democratization by embedding text-to-image and video generation APIs inside standard cloud consoles, letting developers test multimodal inference without bespoke infrastructure. These platform moves reduce time-to-value and expand the neural network software market across new corporate adopters.

Rising Enterprise Demand for Predictive Analytics

Manufacturers are shifting from reactive to proactive maintenance as neural networks reach 94% accuracy in fault prediction. BMW's Regensburg plant prevents over 500 minutes of annual assembly disruption by analyzing existing component data, confirming strong ROI in industrial contexts. General Motors cut unexpected downtime by 15% and saved USD 20 million yearly after linking IoT sensors with AI-driven scheduling engines. Financial institutions see parallel benefits, with hybrid deep-learning models catching 98.7% of fraudulent payments. Such clear economic gains accelerate software procurement cycles and raise expectations for rapid deployment support from vendors.

Shortage of Deep-Learning MLOps Talent

Only 28% of AI adopters employ dedicated MLOps engineers, and 75% of European employers struggled to fill AI roles in 2024, spotlighting a persistent skills gap. Tech giants now deliver certification curricula to accelerate reskilling, yet curricula cannot match rapid framework changes. Without sufficient practitioners to operationalize models, deployment timelines lengthen and service revenues climb, capping short-term neural network software market gains even as demand grows.

Other drivers and restraints analyzed in the detailed report include:

- Growing Availability of Big Data and GPUs

- Foundation Models Create New Toolchain Demand

- Data-Privacy and Governance Burdens

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software frameworks, libraries, and AutoML suites delivered 54.4% of 2024 revenue, underscoring their role as the structural backbone of the neural network software market. Core development kits such as TensorFlow, PyTorch, and JAX remain essential, yet buyers increasingly demand turnkey modules that shorten experimentation cycles. Services, including professional consulting and managed operations, are rising at 35.4% CAGR as firms outsource integration, tuning, and lifecycle management.

Managed services captured incremental gains equal to 35.4% of the neural network software market size in 2024 as cloud providers embedded AI specialists within subscription packages to accelerate time-to-production. Professional service teams respond to sector-specific needs-e.g., healthcare imaging compliance-further boosting service share. Over the forecast window, vendor differentiation will hinge on domain depth and outcome-based pricing rather than licensing alone.

Public cloud retained 61.3% of the neural network software market share in 2024 because hyperscalers offer elastic compute for training and inference. Enterprises leverage GPU clusters on demand, avoiding up-front capital outlays. Yet sovereignty, latency, and regulatory requirements are shifting growth toward hybrid deployments, forecast at 34.8% CAGR to 2030.

Hybrid architectures let data reside on-premise or in private clouds while model training happens in scalable public environments. Financial services and healthcare operators adopt this topology to protect sensitive data while exploiting cloud scale. The growing use of confidential computing and federated learning will amplify hybrid demand, reshaping resource planning for vendors.

Neural Network Software Market is Segmented by Component (Software Tools, Platform, and Services), Deployment Mode (Cloud, On-Premise, and Hybrid), Type (Data Mining and Archiving, Analytical Software, and More), Application (Fraud Detection, Hardware Diagnostics, Financial Forecasting, and More), End-User Vertical (BFSI, Healthcare, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America held 38.06% revenue in 2024 due to an established venture-capital ecosystem, advanced cloud infrastructure, and dense talent pools. OpenAI doubling annual recurring revenue to USD 10 billion highlights commercial maturity, while hyperscalers continually widen managed-AI portfolios. Canada leverages academic clusters in Montreal and Toronto, yet chip fabrication dependence on Asia limits sovereign compute ambitions. Mexico leverages nearshoring to integrate neural network solutions in logistics and automotive production, strengthening regional supply chains.

Asia-Pacific is forecast to grow at 35.7% CAGR, with the neural network software market size jumping to USD 300 billion by 2030 as China, Japan, India, and South Korea implement national AI clouds. China leads 37 of 44 critical R&D disciplines, channelling state financing toward industrial AI upgrades. Japan hosts OpenAI's first Indo-Pacific office, confirming local demand for enterprise GPT solutions that respect linguistic nuance and data-residency laws. India nurtures start-ups through government sandboxes, while Australia and Singapore invest in safety and governance research, creating diversified regional opportunities.

Europe pursues technological autonomy through sovereign-AI projects. NVIDIA is supplying over 3,000 exaflops of Blackwell clusters to European data-center partners, forming a continental spine for regulated AI workloads. Germany's industrial AI cloud and France's telco-led model-hosting hubs add depth. However, talent shortages persist, with 75% of employers unable to staff AI roles, driving wage inflation and cross-border migration. Strict GDPR and forthcoming AI-Act requirements favor vendors offering governance tooling, shaping procurement priorities.

- DataRobot Inc.

- H2O.ai Inc.

- C3.ai Inc.

- Hugging Face Inc.

- DeepMind Technologies Ltd.

- OpenAI Inc.

- Clarifai Inc.

- GMDH LLC

- Neural Designer (Artelnics S.L.)

- Alyuda Research LLC

- Neural Technologies Ltd.

- Neuralware LLC

- AND Corporation

- Abacus.ai

- OctoML Inc.

- Databricks Inc.

- Seldon Technologies Ltd.

- Weights and Biases Inc.

- Comet ML Inc.

- Run:AI Labs Ltd.

- Lightning AI Inc.

- KNIME AG

- RapidMiner Inc.

- LatticeFlow AG

- Pachyderm Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cloud-based AI platforms democratize neural networks

- 4.2.2 Rising enterprise demand for predictive analytics

- 4.2.3 Growing availability of big-data and GPUs

- 4.2.4 Foundation models create new toolchain demand

- 4.2.5 Open-source model marketplaces accelerate adoption

- 4.2.6 Sovereign-AI initiatives need local NN stacks

- 4.3 Market Restraints

- 4.3.1 Shortage of deep-learning MLOps talent

- 4.3.2 Data-privacy and governance burdens

- 4.3.3 GPU supply-chain volatility inflates costs

- 4.3.4 Energy and ESG scrutiny of training workloads

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Component

- 5.1.1 Software Tools

- 5.1.1.1 Frameworks and Libraries

- 5.1.1.2 AutoML Platforms

- 5.1.2 Platform (PaaS)

- 5.1.3 Services

- 5.1.3.1 Managed Services

- 5.1.3.2 Professional Services

- 5.1.1 Software Tools

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.2 On-premise

- 5.2.3 Hybrid

- 5.3 By Type

- 5.3.1 Data Mining and Archiving

- 5.3.2 Analytical Software

- 5.3.3 Optimization Software

- 5.3.4 Visualization Software

- 5.4 By Application

- 5.4.1 Fraud Detection

- 5.4.2 Hardware Diagnostics

- 5.4.3 Financial Forecasting

- 5.4.4 Image Optimization

- 5.4.5 Predictive Maintenance

- 5.4.6 Natural Language Processing

- 5.4.7 Speech Recognition

- 5.4.8 Others

- 5.5 By End-user Vertical

- 5.5.1 BFSI

- 5.5.2 Healthcare

- 5.5.3 Retail and E-Commerce

- 5.5.4 Defense and Government

- 5.5.5 Media and Entertainment

- 5.5.6 Logistics and Transportation

- 5.5.7 Energy and Utilities

- 5.5.8 Manufacturing

- 5.5.9 Other End-user Verticals

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Chile

- 5.6.2.4 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 Malaysia

- 5.6.4.6 Singapore

- 5.6.4.7 Australia

- 5.6.4.8 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 United Arab Emirates

- 5.6.5.1.2 Saudi Arabia

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 DataRobot Inc.

- 6.4.2 H2O.ai Inc.

- 6.4.3 C3.ai Inc.

- 6.4.4 Hugging Face Inc.

- 6.4.5 DeepMind Technologies Ltd.

- 6.4.6 OpenAI Inc.

- 6.4.7 Clarifai Inc.

- 6.4.8 GMDH LLC

- 6.4.9 Neural Designer (Artelnics S.L.)

- 6.4.10 Alyuda Research LLC

- 6.4.11 Neural Technologies Ltd.

- 6.4.12 Neuralware LLC

- 6.4.13 AND Corporation

- 6.4.14 Abacus.ai

- 6.4.15 OctoML Inc.

- 6.4.16 Databricks Inc.

- 6.4.17 Seldon Technologies Ltd.

- 6.4.18 Weights and Biases Inc.

- 6.4.19 Comet ML Inc.

- 6.4.20 Run:AI Labs Ltd.

- 6.4.21 Lightning AI Inc.

- 6.4.22 KNIME AG

- 6.4.23 RapidMiner Inc.

- 6.4.24 LatticeFlow AG

- 6.4.25 Pachyderm Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 White-Space and Unmet-Need Assessment

神經網路軟體市場:按交付類型、組織規模、組件、部署類型、培訓類型、行業和應用 - 全球預測 2025-2032

神經網路軟體市場:按交付類型、組織規模、組件、部署類型、培訓類型、行業和應用 - 全球預測 2025-2032 2025年神經網路軟體全球市場報告

2025年神經網路軟體全球市場報告 神經網路軟體市場、機會、成長動力、產業趨勢分析與預測,2024-2032

神經網路軟體市場、機會、成長動力、產業趨勢分析與預測,2024-2032