|

市場調查報告書

商品編碼

1850247

分類系統:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)Sortation Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

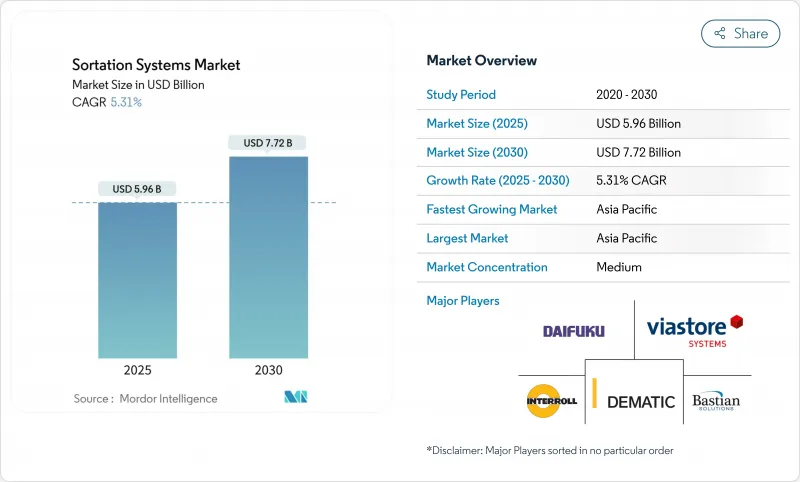

預計到 2025 年,分類系統市場規模將達到 59.6 億美元,到 2030 年將擴大到 77.2 億美元,複合年成長率為 5.31%。

緩慢但穩定的擴張標誌著該產業正從新型自動化轉型為核心基礎設施。交叉傳送帶設備也是成長最快的分揀平台,印證了其從高階利基產品轉向業界標準的轉變。市場主導地位的鞏固和擴張速度的加快,表明交叉傳送帶技術正從高階解決方案發展成為行業標準,這主要得益於其對各種形狀和重量包裹的卓越處理能力。電子商務和全通路營運商佔據了大部分需求,這表明小包裹自動化仍有很長的路要走。雖然硬體仍然佔據大部分收入,但向以軟體為中心的價值創造模式的轉變反映出,業界已認知到,競爭優勢越來越依賴演算法效率,而不僅僅是機械速度。按地區分類,亞太地區將在2024年佔據最大佔有率,這主要得益於中國跨境電商的發展以及印度的自動化投資,例如大DAIFUKU CO. LTD.計劃於2025年在印度推出的工廠。

全球分類系統市場趨勢與洞察

電子商務小包裹激增

小包裹成長重塑運力規劃:預計到 2028 年,美國年度小包裹量將達到 280 億件。中國跨境賣家加速數位化,並採用生成式人工智慧來改善需求預測。

人事費用上升和勞動短缺

倉庫工資上漲和技術人員短缺正給部署時間表帶來壓力。 63%的業者表示,技術純熟勞工短缺是他們面臨的最大障礙,預計到本世紀中期,供應鏈技術人員的空缺將達到77萬個。如今,採購標準不僅關注名義吞吐量,也同樣重視遠距離診斷和簡化維護。

高額資本投入與不確定性的投資報酬率

全尺寸分類機需要數百萬美元的投資和設施改造。營運商希望在18-24個月內收回成本,因此往往會放慢採用速度,更傾向於選擇模組化附加元件,雖然這樣可以延長投資回報期,但會損害長期效率。量化諸如降低解約率和提高客戶忠誠度等軟性收益仍然是一項挑戰。

細分市場分析

預計到2024年,交叉帶式分類機的銷售量將成長38%,年均成長7.8%,使其成為分類系統市場中規模最大、成長最快的細分市場。使用者青睞能夠處理不規則貨物而不降低運轉速度的設備。傾斜托盤式和滑靴式分類機非常適合易碎品或尺寸統一的紙箱占主導地位的應用場景。窄帶式分類機仍然在占地面積有限的老舊廠房中廣泛應用。隨著營運商尋求更高的靈活性和運轉率,彈出式輪和分流器系統的應用正在減少。

預計到 2030 年,交叉傳送帶平台分類系統的市場規模將超過 30 億美元,反映出其從利基市場向主流市場的轉變;而滑動鞋式分揀系統的市場佔有率將以中等個位數的速度成長,隨著其適用於需要溫和流量控制的服裝和宅配中心,其市場佔有率將以較低的個位數速度成長。

2024年,電子商務和全通路零售商將佔41.2%的交易量,年均成長率達7.4%。郵政和小包裹業者仍是第二大市場,但利潤率壓力使得自動化更成為一種成本控制手段,而非成長催化劑。隨著樞紐機場對行李傳送系統進行現代化改造,機場持續提供企劃為基礎的合作機會。食品飲料和製藥生產線正在採用高精度分類技術以確保合規性,從而推動了配備感測器的交叉傳送帶和高速托盤單元的普及。

預計到 2030 年,電子商務產業將佔市場佔有率的 30 億美元以上。機場專案預計在客運和貨運投資的共同推動下,實現暫時的個位數中期複合年成長率。

全球分類系統市場按分類機類型(例如,交叉帶分揀機、傾斜托盤分類機、滑靴分類機)、終端用戶行業(例如,郵政小包裹、電子商務及全通路零售、機場)、提供的服務(例如,硬體、軟體)、吞吐量(例如,低速、中速)和地區進行細分。市場預測以美元計價。

區域分析

亞太地區佔據分類系統市場36.5%的佔有率,年複合成長率達8.6%。中國物流業正利用人工智慧技術將取貨效率提升30%,配送效率提升35%,進而推動智慧分類機的進一步普及。印度大力推動自動化,DAIFUKU CO. LTD.的2025製造中心便是例證,該中心旨在實現生產在地化並縮短前置作業時間。東南亞電子商務的蓬勃發展也帶動了都市區微型履約中心靈活分類技術的投資。

北美地區仍然是收入成長的主要驅動力,這主要得益於機場行李處理設施的持續改造和小包裹中心的升級。由於許多首批設施已經自動化,投資正轉向維修、軟體和永續性升級,實現了4%左右的溫和成長。歐洲則在綠色環保要求和營運績效之間尋求平衡,營運商傾向於使用節能馬達和可回收的傳送帶材料,以符合歐盟的循環經濟目標。

在中東和非洲,隨著海灣地區機場加大對樞紐設施的投資,以及非洲電子商務取代傳統零售,需求雖處於起步階段但正在成長。南美洲則在主要城市走廊進行選擇性部署,這些地區的小包裹量和勞動成本上漲使得資本支出物有所值。巴西和智利的政策制定者已表示有意簡化海關程序,這間接支援了在出口導向物流園區部署分類機。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 電子商務小包裹激增

- 勞動成本上升和人手不足

- 更多SKU需要更精確的管理

- 機場行李處理升級

- 配備人工智慧視覺的動態分類機

- 以永續性為重點的節能措施

- 市場限制

- 高額資本投入與不確定性的投資報酬率

- 熟練工程師短缺

- 軟體層互通性差距

- 城市噪音管制值

- 價值/供應鏈分析

- 監管環境

- 技術展望

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 依分類機類型

- 交叉帶分類機

- 趨勢特徵分類器

- 滑動鞋分類機

- 窄頻分類機

- 推式托盤/分類托盤分類機

- 彈出式輪式分類機

- 按最終用戶行業分類

- 郵政和小包裹遞送公司

- 電子商務與全通路零售

- 機場(行李處理)

- 食品/飲料

- 製藥和醫療保健

- 第三方物流和合約物流

- 汽車和工業製造

- 報價

- 硬體

- 軟體

- 服務(安裝、MRO)

- 按吞吐量

- 慢速(低於3k)

- 中速(3k-10k)

- 高速(10k-25k)

- 速度超快(超過 25k)

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲和紐西蘭

- 東南亞

- 亞太其他地區

- 中東和非洲

- 海灣合作理事會(原沙烏地阿拉伯)

- 沙烏地阿拉伯

- 土耳其

- 南非

- 以色列

- 其他中東和非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Daifuku Co., Ltd.

- Vanderlande Industries

- Honeywell Intelligrated

- Siemens Logistics

- Beumer Group GmbH

- Interroll Holding AG

- Dematic Corporation(KION Group)

- Murata Machinery Ltd.

- KNAPP AG

- Bastian Solutions

- Viastore Systems Gmbh

- SSI Schaefer

- TGW Logistics

- Fives Intralogistics

- BOWE SYSTEC

- Pitney Bowes

- Equinox MHE

- Falcon Autotech

- GBI Intralogistics

- OPEX Corporation

- Okura Yusoki

- Zebra Technologies(Fetch Robotics)

第7章 市場機會與未來展望

The sortation systems market reached USD 5.96 billion in 2025 and is projected to advance to USD 7.72 billion by 2030 at a 5.31% CAGR.

Moderate but steady expansion shows the field is transitioning from novel automation toward core infrastructure. Cross-belt equipment is also the fastest-expanding sorter platform, confirming a shift from premium niche toward de-facto standard. The convergence of dominant position and accelerated expansion signals cross-belt technology's evolution from premium solution to industry standard, driven by its superior handling of diverse package geometries and weights. E-commerce and omnichannel operators dominate demand, illustrating that parcel automation remains in a long runway. Hardware continues to account for majority of sales, yet the shift toward software-centric value creation reflects industry recognition that competitive differentiation increasingly depends on algorithmic efficiency rather than mechanical speed alone. Geographically, APAC leads highest share in 2024, fuelled by Chinese cross-border e-commerce and Indian automation investments exemplified by Daifuku's 2025 plant launch

Global Sortation Systems Market Trends and Insights

E-commerce parcel surge

Parcel growth reshapes capacity planning. United States annual parcel flow is forecast to hit 28 billion by 2028, a 5% yearly increase. Chinese cross-border sellers accelerate digitalisation and employ generative AI to improve demand forecasting, allowing facilities to move from reactive peaks to predictive load balancing.Sorters that self-adjust to volume spikes and shift routing rules on the fly now underpin peak-season resilience.

Labor-cost escalation & scarcity

Warehouse payroll inflation and technician shortages compress deployment timelines. A 63% majority of operators cite skilled labour gaps as the top obstacle, while 770,000 supply-chain technician vacancies are expected by mid-decade. Procurement criteria now weigh remote diagnostics and simplified maintenance as heavily as nominal throughput.

High capex & ROI uncertainty

Full-scale sorters require multimillion-dollar outlays plus facility remodelling. Operators demanding 18-24-month payback often delay adoption, favouring modular add-ons that can stretch ROI but impair long-term efficiency. Quantifying soft returns such as reduced churn and customer loyalty remains challenging.

Other drivers and restraints analyzed in the detailed report include:

- SKU proliferation demands accuracy

- Airport baggage-handling upgrades

- AI-vision powered dynamic sorters

- Sustainability-driven energy savings

- Skilled-technician shortage

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cross-belt units generated 38% revenue in 2024 and are set to rise 7.8% annually, giving the sorter class the largest and fastest path within the sortation systems market. Facilities prefer its capability to handle irregular packages without speed loss. Tilt-tray and sliding-shoe equipment stay relevant where either fragile goods or uniform cartons dominate. Narrow-belt installations persist in legacy buildings with limited floor plates. Pop-up wheel and diverter systems continue to fade as operators pursue higher flexibility and uptime.

The sortation systems market size for cross-belt platforms is projected to exceed USD 3 billion by 2030, reflecting entrenched migration from niche to mainstream. Meanwhile, sliding-shoe products hold a mid-single-digit sortation systems market share and show low-single-digit expansion as they retain fit in apparel and parcel hubs demanding gentle flow control.

E-commerce and omnichannel retailers captured 41.2% of 2024 turnover and are increasing 7.4% annually. Post-and-parcel operators remain the second-largest cohort, yet margin pressure converts automation into a cost-containment lever rather than growth catalyst. Airports contribute stable, project-based opportunities as hubs modernise baggage loops. Food, beverage and pharma lines embrace high-accuracy sorting to honour compliance, fuelling adoption of sensor-laden cross-belt and high-speed tray units.

By 2030, the e-commerce segment is expected to command more than USD 3 billion of the sortation systems market size. Airport programmes, though lumpy, could achieve mid-single-digit CAGR on the back of combined passenger and cargo investments.

Global Sortation System Market is Segmented by Sorter Type (Cross-Belt Sorters, Tilt-Tray Sorters, Sliding-Shoe Sorters, and More), by End-User Industry (Post and Parcel, E-Commerce and Omnichannel Retail, Airport, and More), by Offering (Hardware, and Software), by Throughput Rate (Low-Speed, Medium-Speed, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

APAC dominated the sortation systems market with 36.5% 2024 share and is expanding at 8.6% CAGR. China's logistics sector uses AI to lift collection efficiency 30% and delivery 35%, spurring further adoption of intelligent sorters. India's automation drive is illustrated by Daifuku's 2025 manufacturing complex designed to localise production and lower lead times. Southeast Asian e-commerce growth also channels investment into flexible sorting in urban micro-fulfilment nodes.

North America remains a core revenue pillar through airport baggage rebuilds and ongoing parcel-centre upgrades. Growth moderates to a mid-4% rate as many first-wave facilities are already automated, causing spend to pivot towards retrofits, software, and sustainability upgrades. Europe balances green mandates with performance. Operators favour energy-efficient motors and recyclable belt materials to align with EU circularity targets.

Middle East and Africa present nascent but rising demand as Gulf airports invest in hub capability and African e-commerce leapfrogs conventional retail. South America exhibits selective uptake in metropolitan corridors where parcel volumes and labour inflation justify capital outlays. Policymakers in Brazil and Chile have signalled intent to streamline customs processes, indirectly supporting sorter adoption in export-oriented logistics parks.

- Daifuku Co., Ltd.

- Vanderlande Industries

- Honeywell Intelligrated

- Siemens Logistics

- Beumer Group GmbH

- Interroll Holding AG

- Dematic Corporation (KION Group)

- Murata Machinery Ltd.

- KNAPP AG

- Bastian Solutions

- Viastore Systems Gmbh

- SSI Schaefer

- TGW Logistics

- Fives Intralogistics

- BOWE SYSTEC

- Pitney Bowes

- Equinox MHE

- Falcon Autotech

- GBI Intralogistics

- OPEX Corporation

- Okura Yusoki

- Zebra Technologies (Fetch Robotics)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 E-commerce parcel surge

- 4.2.2 Labor-cost escalation & scarcity

- 4.2.3 SKU proliferation demands accuracy

- 4.2.4 Airport baggage-handling upgrades

- 4.2.5 AI-vision powered dynamic sorters

- 4.2.6 Sustainability-driven energy savings

- 4.3 Market Restraints

- 4.3.1 High capex & ROI uncertainty

- 4.3.2 Skilled-technician shortage

- 4.3.3 Software-layer interoperability gaps

- 4.3.4 Urban-noise compliance limits

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Sorter Type

- 5.1.1 Cross-belt Sorters

- 5.1.2 Tilt-tray Sorters

- 5.1.3 Sliding-shoe Sorters

- 5.1.4 Narrow-belt Sorters

- 5.1.5 Push-tray / Split-tray Sorters

- 5.1.6 Pop-up Wheel & Diverter Sorters

- 5.2 By End-user Industry

- 5.2.1 Post & Parcel Operators

- 5.2.2 E-commerce & Omnichannel Retail

- 5.2.3 Airports (Baggage Handling)

- 5.2.4 Food & Beverages

- 5.2.5 Pharmaceuticals & Healthcare

- 5.2.6 3PL & Contract Logistics

- 5.2.7 Automotive & Industrial Manufacturing

- 5.3 By Offering

- 5.3.1 Hardware

- 5.3.2 Software

- 5.3.3 Services (Installation, MRO)

- 5.4 By Throughput Rate

- 5.4.1 Low-speed (<3k)

- 5.4.2 Medium-speed (3k-10k)

- 5.4.3 High-speed (10k-25k)

- 5.4.4 Ultra High-speed (>25k)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Netherlands

- 5.5.3.7 Rest of Europe

- 5.5.4 APAC

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia & New Zealand

- 5.5.4.6 Southeast Asia

- 5.5.4.7 Rest of APAC

- 5.5.5 Middle East & Africa

- 5.5.5.1 GCC (ex-Saudi)

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Turkey

- 5.5.5.4 South Africa

- 5.5.5.5 Israel

- 5.5.5.6 Rest of Middle East & Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 Daifuku Co., Ltd.

- 6.4.2 Vanderlande Industries

- 6.4.3 Honeywell Intelligrated

- 6.4.4 Siemens Logistics

- 6.4.5 Beumer Group GmbH

- 6.4.6 Interroll Holding AG

- 6.4.7 Dematic Corporation (KION Group)

- 6.4.8 Murata Machinery Ltd.

- 6.4.9 KNAPP AG

- 6.4.10 Bastian Solutions

- 6.4.11 Viastore Systems Gmbh

- 6.4.12 SSI Schaefer

- 6.4.13 TGW Logistics

- 6.4.14 Fives Intralogistics

- 6.4.15 BOWE SYSTEC

- 6.4.16 Pitney Bowes

- 6.4.17 Equinox MHE

- 6.4.18 Falcon Autotech

- 6.4.19 GBI Intralogistics

- 6.4.20 OPEX Corporation

- 6.4.21 Okura Yusoki

- 6.4.22 Zebra Technologies (Fetch Robotics)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space & Unmet-need Assessment