|

市場調查報告書

商品編碼

1850130

化學注入橇:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)Chemical Injection Skids - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

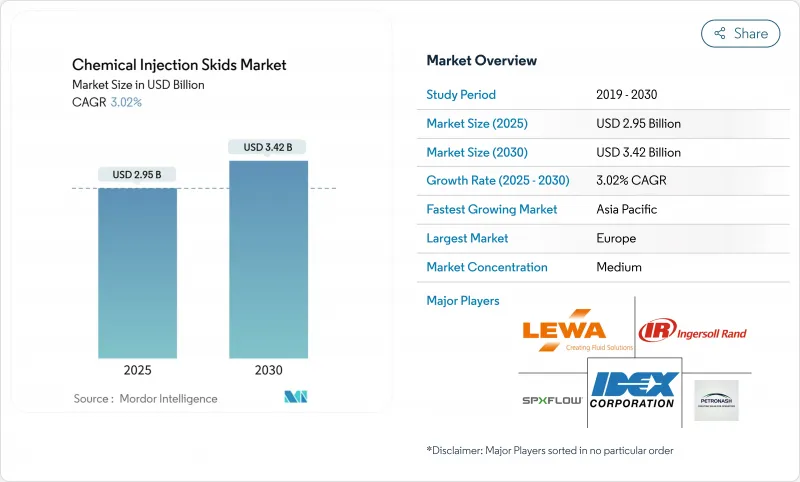

預計 2025 年化學注入橇市場價值將達到 29.5 億美元,到 2030 年預計將達到 34.2 億美元,複合年成長率為 3.02%。

下游石化聯合企業的擴張、排放法規的日益嚴格以及油氣作業對可靠流量保障的需求推動了行業的穩步成長。業者將精密注入撬塊視為防止因結垢、腐蝕和微生物污染而導致意外停機的保障。隨著水處理廠採用自動化技術以滿足營養物去除法規(不合規將面臨經濟處罰),投資需求也不斷增加。隨著乙烯、氨和PTA產能的擴張,亞太地區大型多進料機組的訂單正在加速成長。泵浦專家和系統整合商之間的適度整合標誌著一個成熟階段,在這個階段,服務可靠性、材料工程和數位監控將使供應商脫穎而出。

全球化學注入撬市場趨勢與洞察

下游石化產能快速成長

像中國耗資200億美元的山東綜合體這樣的大型企劃需要數百個專用注入點,用於腐蝕抑制、抗氧化劑注入和催化劑淬滅。系統供應商正在透過擴大生產線來應對這項挑戰:先進精密工業服務公司(Advanced Precision Industrial Services)將其沙烏地阿拉伯工廠的年撬裝產量提高了500%,以解決中東地區EPC訂單積壓問題。新建裂解裝置對流量控制公差的要求比鑽井和生產作業更嚴格,這使得化學品注入撬裝設備從選用配件轉變為關鍵路徑設備。聚合物島、芳烴島和公用工程島都需要單獨的計量迴路,每增加一個乙烯裝置就能產生乘數效應。下游擴建計畫創造了持久的、與計劃相關的需求,從而緩衝了化學品注入撬裝市場對油價波動的影響。

對水處理應用的需求不斷成長

市政當局現在在單一製程中部署多種聚合物、凝聚劑和氣味控制混合物。這種複雜性促使營運商轉向整合高黏度聚合物幫浦和重量式給料器的全自動多化學品撬裝系統。精確的劑量可減少化學品過度使用的損失並降低污泥處理成本,使北美工廠的平均投資回收期為兩年。工業用戶也支持這一趨勢,因為特種化學品製造商在排放到下水道之前必須遵守嚴格的氯化物、磷酸鹽和 COD 限制。設備供應商透過併購擴展其產品組合。英格索蘭 (Ingersoll Rand) 對 SSI 充氣的收購增強了曝氣專業知識並補充了其用於完整水包的計量泵產品線。即使在傳統石油和天然氣訂單疲軟的情況下,這種轉變也創造了一個充滿活力的化學注入撬裝市場。

初期投資成本高

在提高採收率測試中,整合化學注入站的資本支出可能超過1500萬美元,這為在價格低迷時期轉向手動鼓式供油技術的獨立營運商設置了進入門檻。配備防爆馬達、無密封計量幫浦、PLC和冗餘儀器的複雜撬裝系統也構成了較高的進入門檻。額外的試運行和培訓成本可能會使費用翻倍,並延遲中端營運商的投資回報。供應商正在透過租賃車隊和基於績效的租賃計劃來應對,但在融資緊張的領域,採用這些技術仍然謹慎。

細分分析

到2024年,石化產業將佔據化學品注入撬塊市場佔有率的35.16%,這得益於遍布裂解、加氫和聚合裝置的分散式加藥點。由於大型聯合裝置很少容忍計劃外停機,因此營運商青睞配備熱備用泵的雙撬式機架,這些泵可以在不中斷流程的情況下進行更換。由於每個新的乙烯裝置都需要根據具體情況配備酸抑制劑、消泡劑、中和劑和除生物劑迴路,因此該細分市場支撐了化學品注入撬塊的市場規模。

到2030年,用水和污水處理設施的複合年成長率將達到3.78%,是最快的。隨著公共尋求營養物去除合規性,多進料系統正在將聚合物、明礬和聚合氯化鋁注入整合到單一框架中,節省占地面積。隨著市政當局從勞力密集罐式測試轉向自動回饋迴路,將聚合物過量減少15%,多進料系統的應用將會增加。水處理化學品注入撬裝設備的市場規模預計將會增加,這反映了三級處理和污泥脫水生產線的擴張。

區域分析

2024年,歐洲將佔銷售額的28.65%,這得益於德國1,600億歐元的化學品產量以及鼓勵高精度分配設備的合規文化。佔該行業96%的德國中小企業正在採購緊湊型撬裝設備,用於批量特種生產;而像BASF這樣規模的綜合體則正在採購帶有自動切換功能的全封閉ISO集裝箱解決方案。 2010年至2020年期間,能源價格較平均上漲了四倍,促使工廠升級為變速驅動裝置,從而將泵浦功率降低20%,這刺激了現有設施的改造活動。

到2030年,亞太地區將實現最快的複合年成長率,達到3.36%。中國的煉油化工一體化浪潮和印度製藥業的擴張需要同步的添加劑流程,以確保原料純度和反應器保護。 SCG Chemicals在越南投資7億美元的乙烷擴建計劃採用三泵撬裝系統和重量式混合系統,以適應乙烷成分的波動。區域EPC公司正在採用模組化成套設備,這些設備在運輸過程中已進行預接線和測試,以最大限度地減少現場勞動力,因為熟練焊工短缺。

北美市場在頁岩油石化投資和成熟的海上油田(滑橇每七年更換一次)的推動下,市佔率保持穩定。預測性維護的重點是添加數位雙胞胎和振動分析,使操作員能夠在發生故障之前安排軟管和隔膜的更換。墨西哥的保稅加工工廠正在擴建,透過為油漆、黏合劑和電子產品塗裝生產線提供小容量滑橇來擴大基本客群。在南美、中東和非洲,巴西的Comperj計劃和沙烏地阿拉伯的「願景2030」下游多元化計劃正在部署整合先進化學注入功能的連續製程裝置,雖然規模有所滯後,但發展勢頭正在增強。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場狀況

- 市場概況

- 市場促進因素

- 下游石化產能新增快速成長

- 水處理應用需求不斷成長

- 更嚴格的環境排放標準

- 在腐蝕和阻垢應用中的使用日益增多

- 擴大使用綠色化學品需要多進料滑軌設計

- 市場限制

- 初期投資成本高

- 滑軌製造和維修領域技術純熟勞工短缺

- 原物料價格波動

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章市場規模及成長預測

- 按最終用戶產業

- 石化產品

- 化學品

- 能源和電力

- 石油和天然氣

- 水處理

- 按泵類型

- 活塞/柱塞泵

- 隔膜泵

- 蠕動幫浦

- 其他計量泵

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭態勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- AES Arabia Ltd.

- Carotek, Inc

- Casainox FS Pty Ltd

- Euro Mechanical

- IDEX Corporation

- Ingersoll Rand

- INTECH

- Integrated Flow Solutions, Inc.

- ITC SL

- Lewa GmbH

- Petrak Industries, Inc.

- Petronash

- Proserv UK Ltd

- SEKO SpA

- SLB

- SPX FLOW, Inc.

- TechnipFMC plc

- Watson-Marlow Fluid Technology Solutions

第7章 市場機會與未來展望

The chemical injection skids market is valued at USD 2.95 billion in 2025 and is forecast to reach USD 3.42 billion by 2030, expanding at a 3.02% CAGR.

Steady growth is anchored in the expansion of downstream petrochemical complexes, tougher discharge regulations, and the need for reliable flow assurance across oil-and-gas operations. Operators view precision-dosing skids as insurance against unplanned shutdowns caused by scaling, corrosion, or microbial fouling. Investment momentum is reinforced as water-treatment plants adopt automation to meet nutrient-removal rules that carry financial penalties for non-compliance. Europe continues to purchase high-specification equipment to satisfy the EU's Fit-for-55 goals, while Asia-Pacific accelerates orders for large multi-feed packages alongside new ethylene, ammonia, and PTA capacity. Moderate consolidation among pump specialists and system integrators signals a maturity phase in which service reliability, materials engineering, and digital monitoring differentiate suppliers.

Global Chemical Injection Skids Market Trends and Insights

Rapid Growth in Downstream Petrochemical Capacity Additions

Mega-projects such as China's USD 20 billion Shandong complex require hundreds of dedicated dosing points for corrosion inhibition, antioxidant injection, and catalyst quenching. System suppliers respond by scaling fabrication lines: Advanced Precision Industrial Services lifted annual skid output 500% at its Saudi plant to meet Middle-East EPC backlogs. New crackers demand tighter flow-control tolerances than drilling or production operations, turning chemical injection skids from optional accessories into critical path equipment. Each additional ethylene train creates a multiplier effect because polymer, aromatics, and utilities islands all mandate separate dosing loops. The downstream build-out produces durable, project-linked demand that buffers the chemical injection skids market from oil price volatility.

Accelerating Demand from Water Treatment Applications

Municipalities now deploy multiple polymers, coagulants, and odor-control blends in a single process train; this complexity pushes operators toward fully automated, multi-chemical skids that integrate high-viscosity polymer pumps with gravimetric feeders. Accurate dosing trims chemical overuse penalties and reduces sludge-handling costs, bringing a two-year average payback in North American plants. Industrial users echo the trend as specialty-chemical producers face strict chloride, phosphate, and COD limits before discharging to sewers. Equipment vendors expand portfolios through M&A: Ingersoll Rand's purchase of SSI Aeration adds diffused-air expertise that complements its metering-pump line for complete water packages. Such shifts keep the chemical injection skids market vibrant even when traditional oil-and-gas orders soften.

High Initial Cost of Investment

Capital outlays for integrated chemical injection stations on an enhanced-oil-recovery test can top USD 15 million, a barrier that pushes independents toward manual drum-feed techniques during price downturns. The entry hurdle persists because sophisticated skids bundle explosion-proof motors, seal-less metering pumps, PLCs, and redundant instrumentation. Added spend on commissioning and training can double the invoice value, delaying payback for mid-tier operators. Vendors respond with rental fleets and performance-based leasing plans, yet adoption remains cautious in cash-constrained segments.

Other drivers and restraints analyzed in the detailed report include:

- Stricter Environmental Discharge Norms

- Increasing Usage for Corrosion and Scale Inhibition Application

- Skilled-Labor Shortage for Skid Fabrication & Maintenance

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The petrochemical sector held 35.16% of the chemical injection skids market share in 2024, underpinned by distributed dosing points across cracking, hydrogenation, and polymerization trains. Large complexes seldom tolerate unscheduled downtime, so operators favor duplex skid racks with hot-standby pumps that swap without disrupting flow. The segment anchors the chemical injection skids market size because each new ethylene unit demands conditions-specific acid inhibitors, antifoam, neutralizers, and biocide loops.

Water and wastewater facilities register the fastest 3.78% CAGR through 2030. Utilities seek nutrient-removal compliance, so multi-feed systems integrate polymer, alum, and PAC dosing on a single frame to conserve floor space. Adoption rises as municipalities shift from labor-intensive jar testing toward automated feedback loops that cut polymer overshoot by 15%. The chemical injection skids market size for water treatment is projected to rise, mirroring the build-out of tertiary treatment and sludge-dewatering lines.

The Chemical Injection Skids Market Report Segments the Industry by End-User Industry (Petrochemicals, Chemicals, Energy and Power, and More), Pump Type (Piston/Plunger Pumps, Diaphragm Pumps, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Europe accounted for 28.65% revenue in 2024, supported by Germany's EUR 160 billion chemical output and a compliance climate that rewards high-accuracy dosing equipment. German SMEs representing 96% of sector companies purchase compact skids for batch specialty production, whereas BASF-scale complexes procure fully enclosed ISO-container solutions with automated switchover. Energy prices have quadrupled versus 2010-2020 averages, so plants upgrade to variable-speed drives that cut pump power by 20%, stimulating retrofit activity across existing installations.

Asia-Pacific posts the fastest 3.36% CAGR through 2030. China's refinery-to-chemicals integration wave and India's pharmaceuticals build-out require synchronized additive streams that ensure feedstock purity and reactor protection. The USD 700 million SCG Chemicals ethane-enhancement project in Vietnam specifies triple-pump skids with gravimetric blending to accommodate variable ethane composition. Regional EPCs embrace modular packages shipped fully wired and tested, minimizing site labor where skilled welders remain scarce.

North America secures a stable share via shale-driven petrochemical investments and mature offshore fields that rotate skids on 7-year renewal cycles. Emphasis on predictive maintenance adds digital twins and vibration analytics, allowing operators to schedule hose or diaphragm replacement before failure. Mexico's maquiladora expansion adopts smaller capacity skids feeding paint, adhesive, and electronics finishing lines, broadening the customer base. South America, and Middle East and Africa trail in volume but gain traction as Brazil's Comperj project and Saudi Arabia's Vision 2030 downstream diversification roll out continuous-process units that integrate advanced chemical injection functionality.

- AES Arabia Ltd.

- Carotek, Inc

- Casainox FS Pty Ltd

- Euro Mechanical

- IDEX Corporation

- Ingersoll Rand

- INTECH

- Integrated Flow Solutions, Inc.

- ITC SL

- Lewa GmbH

- Petrak Industries, Inc.

- Petronash

- Proserv UK Ltd

- SEKO S.p.A.

- SLB

- SPX FLOW, Inc.

- TechnipFMC plc

- Watson-Marlow Fluid Technology Solutions

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid growth in downstream petrochemical capacity additions

- 4.2.2 Accelerating demand from water treatment applications

- 4.2.3 Stricter environmental discharge norms

- 4.2.4 Increasing usage for corrosion and scale inhibition application

- 4.2.5 Rising use of green chemicals requiring multi-feed skid designs

- 4.3 Market Restraints

- 4.3.1 High initial cost of investment

- 4.3.2 Skilled-labor shortage for skid fabrication & maintenance

- 4.3.3 Volatility in raw material prices

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By End-User Industry

- 5.1.1 Petrochemicals

- 5.1.2 Chemicals

- 5.1.3 Energy and Power

- 5.1.4 Oil and Gas

- 5.1.5 Water Treatment

- 5.2 By Pump Type

- 5.2.1 Piston/Plunger Pumps

- 5.2.2 Diaphragm Pumps

- 5.2.3 Peristaltic Pumps

- 5.2.4 Other Metering Pumps

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 United Kingdom

- 5.3.3.2 Germany

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%) / Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 AES Arabia Ltd.

- 6.4.2 Carotek, Inc

- 6.4.3 Casainox FS Pty Ltd

- 6.4.4 Euro Mechanical

- 6.4.5 IDEX Corporation

- 6.4.6 Ingersoll Rand

- 6.4.7 INTECH

- 6.4.8 Integrated Flow Solutions, Inc.

- 6.4.9 ITC SL

- 6.4.10 Lewa GmbH

- 6.4.11 Petrak Industries, Inc.

- 6.4.12 Petronash

- 6.4.13 Proserv UK Ltd

- 6.4.14 SEKO S.p.A.

- 6.4.15 SLB

- 6.4.16 SPX FLOW, Inc.

- 6.4.17 TechnipFMC plc

- 6.4.18 Watson-Marlow Fluid Technology Solutions

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

- 7.2 Development of Technologically Advanced Chemical Injection System

化學注入撬裝設備市場:2026-2032年全球市場預測(依泵浦設計、材質、壓力等級、系統配置與應用分類)

化學注入撬裝設備市場:2026-2032年全球市場預測(依泵浦設計、材質、壓力等級、系統配置與應用分類) 2026年全球化學注入撬裝設備市場報告

2026年全球化學注入撬裝設備市場報告 化學注入撬裝設備市場-全球產業規模、佔有率、趨勢、機會和預測:按功能、應用、地區和競爭格局分類,2021-2031年

化學注入撬裝設備市場-全球產業規模、佔有率、趨勢、機會和預測:按功能、應用、地區和競爭格局分類,2021-2031年 化學注入撬裝設備:全球市場佔有率和排名、總收入和需求預測(2025-2031 年)液態氮分配系統市場(按系統類型、控制類型、系統元件、應用和分銷管道)—2025-2030 年全球預測

化學注入撬裝設備:全球市場佔有率和排名、總收入和需求預測(2025-2031 年)液態氮分配系統市場(按系統類型、控制類型、系統元件、應用和分銷管道)—2025-2030 年全球預測 化學品注入撬市場規模、佔有率、趨勢分析報告:按功能、最終用途、地區、細分市場預測,2025-2030 年

化學品注入撬市場規模、佔有率、趨勢分析報告:按功能、最終用途、地區、細分市場預測,2025-2030 年 化學注入撬市場(功能:消泡、腐蝕抑制、破乳等)- 2024-2034 年全球產業分析、規模、佔有率、成長、趨勢和預測

化學注入撬市場(功能:消泡、腐蝕抑制、破乳等)- 2024-2034 年全球產業分析、規模、佔有率、成長、趨勢和預測