|

市場調查報告書

商品編碼

1850105

歐洲安全檢測:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)Europe Security Testing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

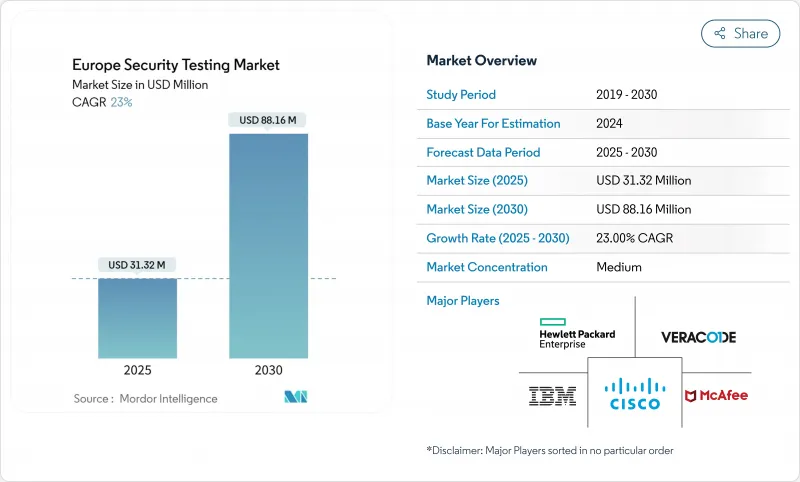

歐洲安全測試市場規模預計到 2025 年將達到 313.2 億美元,預計到 2030 年將達到 881.6 億美元,在預測期內將以 23% 的強勁複合年成長率成長。

這一近三倍的成長反映出歐洲日益嚴峻的數位威脅情勢,隨著數位轉型步伐的加快,各組織機構面臨日益複雜的網路威脅。該市場的成長軌跡遠超歷史水平,預示著歐洲安全重點的根本性轉變。

市場格局正受到嚴格監管的重塑,尤其是《網路與資訊安全指令2》(NIS2)和《數位營運彈性法案》(DORA)的實施,這兩項法規強制要求對關鍵產業進行全面的安全測試。 2024年,雲端部署將佔據主導地位,市佔率達61%,其次是應用程式安全測試,市佔率為39%。從地區來看,英國以23.11%的市佔率領先,而法國的成長速度最快,到2030年複合年成長率將達到26.4%。

隨著埃森哲和IBM等老牌企業面臨歐洲專業安全測試供應商的壓力,市場競爭日益激烈。這些供應商利用人工智慧主導的自動化技術提供更有效率的測試解決方案。為了減少誤報並在開發週期的早期階段整合安全措施,企業正尋求減少誤報,市場也因此顯著轉向互動式應用安全測試(IAST),其複合年成長率高達27.8%。這一趨勢在製造業尤為明顯,該行業在終端用戶中成長最快,複合年成長率達25.2%,這主要得益於工業IoT的日益普及以及IT和OT安全需求的融合。

歐盟成員國之間資料主權規則的碎片化給實施雲端基礎的安全測試解決方案帶來了挑戰,但也推動了混合部署模式的創新,這些模式能夠同時滿足營運和合規要求。特別是金融服務機構和政府機構,已經開始進行早期試點項目,為應對後量子時代的安全威脅做好準備。

歐洲安全測試市場趨勢與洞察

從2023年起,針對關鍵基礎設施的網路攻擊將急劇增加。

2024年針對歐洲電網和鐵路系統的一系列複雜攻擊迫使關鍵基礎設施營運商重新思考其測試方案。據歐盟網路安全局(ENISA)稱,安全事件數量增加了38%,其中OT入侵技術繞過了傳統的邊界控制。安全預算正轉向能夠繪製融合的IT和OT環境漏洞圖的服務,尤其是在處理監控和資料擷取流量的電網中。能夠結合紅藍測試的服務提供者如今正受益於跨多個國家的合約規模。強制性事件報告製度的擴展進一步推動了這一需求,因為即時測試的證據對於監管申報至關重要。

加速歐盟NIS2和DORA合規期限

隨著NIS2將於2024年10月生效,DORA將於2025年1月運作,合規期限日益縮短,迫使企業將定期安全評估制度化。 DORA針對銀行的三年週期性威脅主導滲透測試已促使企業與外部測試機構簽訂多年框架協議,而NIS2對供應鏈的關注也推動了對第三方程式碼庫的下游檢驗。跨國企業集團正在集中管理編配,以避免重複審核,這促使企業採用統一平台來安排、執行測試並記錄證據,以滿足多個監管機構的要求。

CREST認證安全測試人員短缺

歐洲人才短缺問題依然嚴峻,光是英國每年就需要新增7,000名專業人才。雲端運算和營運技術(OT)領域的人才缺口尤為突出,導致大型轉型計劃的啟動被延遲。雖然自動化可以減少日常工作,但它無法取代客戶期望高級測試人員提供的上下文分析,從而限制了歐洲安全測試市場的整體交付能力。

細分市場分析

預計到2024年,雲端基礎的模式將佔據歐洲安全測試市場61%的佔有率,並在2030年之前以26.01%的複合年成長率成長。到2030年,歐洲雲端部署安全測試市場規模預計將達到540億美元,反映出市場對能夠在幾分鐘內模擬攻擊者地理位置的彈性測試環境的需求日益成長。英國公司通常每週從雲端原生平台發動外部攻擊模擬,而德國公司則更傾向於採用混合配置,將加密金鑰保存在本地。為了滿足法國嚴格的資料在地化法規,服務提供者目前正在將主權雲端控制措施(例如區域內金鑰管理和專用安全營運人員編制配備)打包在一起。雖然本地部署仍然很重要,尤其是在處理敏感資訊的場所(例如國防部),但這些機構也在嘗試安全的「運算輸出,資料輸入」模式,既可以限制原始資料的暴露,又可以將測試日誌異地儲存。隨著歐洲超大規模雲端服務商承諾在區域市場投入數十億歐元,混合編配正成為兼顧營運敏捷性和國家安全需求的可行橋樑。因此,歐洲安全測試市場正持續向整合部署方案轉型,該方案能夠在私人機架和受監管雲端之間無縫遷移工作負載,同時保持審核追蹤的完整性。

到2024年,應用安全測試(AST)將佔據歐洲安全測試市場39%的收入佔有率,隨著Web、行動和無伺服器工作負載的成長,應用安全測試將引領市場普及。在AST領域,以雲端為中心的評估成長最快,複合年成長率(CAGR)高達31%,這主要得益於DORA條款要求金融機構審查傳統代碼和容器化代碼。將動態掃描整合到提交管道中的持續整合工具進一步鞏固了AST在歐洲安全測試市場的佔有率,從而能夠在運作前進行風險分級。網路安全測試是零信任部署的核心,尤其是在併購後建置的扁平化網路中進行隔離時。在遠端存取漏洞被公開披露後,VPN評估變得尤為重要,這些漏洞可以繞過多因素身份驗證。防火牆測試先前專注於規則集的維護,現在則加入了規避性流量模擬,以衡量針對使用網域偽裝的攻擊者的偵測深度。隨著雲端、行動和API介面的融合,企業越來越需要整合式測試方案,這些方案能夠交叉引用多種測試類型的洞察,並在不超出預算的情況下最大限度地提高覆蓋範圍。

歐洲安全測試市場按部署方式(本地部署、雲端、混合部署)、類型(網路安全測試、應用安全測試等)、測試工具(Web應用測試工具、程式碼審查工具等)、最終用戶產業(政府機構、銀行、金融服務和保險等)以及國家進行細分。市場預測以美元計價。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 從2023年起,針對關鍵基礎設施(電力和鐵路)的網路攻擊將會增加。

- 加速歐盟NIS2和DORA合規期限

- 軟體供應鏈中DevSecOps採用的左移

- 工業IoT在德國中型工廠的普及

- 歐洲公共部門競標中的強制性滲透測試條款

- 抗量子密碼過渡試點(低調)

- 市場限制

- CREST認證安全測試人員短缺

- 歐盟27國中小企業的預算將在2024年信貸緊縮後凍結。

- 資料主權規則的碎片化正在減緩雲端基礎的測試速度。

- 假陽性疲勞導致檢測頻率降低(不易察覺)

- 價值/供應鏈分析

- 監管環境

- 技術展望

- 波特五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 透過部署

- 本地部署

- 雲

- 混合

- 按類型

- 網路安全測試

- VPN測試

- 防火牆測試

- 其他服務類型

- 應用程式安全測試

- 按應用程式類型

- 行動應用安全測試

- Web應用程式安全性測試

- 雲端應用安全測試

- 企業應用安全測試

- 網路安全測試

- 按測試類型

- SAST

- DAST

- IAST

- RASP

- 按最終用戶行業分類

- 政府

- BFSI

- 衛生保健

- 製造業

- 資訊科技和通訊

- 零售

- 其他終端用戶產業

- 透過測試工具

- Web應用程式測試工具

- 程式碼審查工具

- 滲透測試工具

- 軟體測試工具

- 其他測試工具

- 按國家/地區

- 英國

- 德國

- 法國

- 其他歐洲地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Accenture

- Atos

- Cisco Systems

- Core Security Technologies

- CrowdStrike

- Fortinet

- Hewlett Packard Enterprise

- IBM

- Kaspersky

- Micro Focus(CyberRes)

- McAfee

- Netcraft

- Offensive Security

- Orange Cyberdefense

- Paladion(Tech Mahindra)

- PwC

- Qualys

- Securonix

- Synopsys

- Veracode

第7章 市場機會與未來展望

The Europe Security Testing Market size is estimated at USD 31.32 billion in 2025 and is projected to reach USD 88.16 billion by 2030, growing at a robust CAGR of 23% during the forecast period.

This nearly threefold expansion reflects the intensifying digital threat landscape across Europe, where organizations face increasingly sophisticated cyber threats amid accelerated digital transformation initiatives. The market's growth trajectory is significantly steeper than historical patterns, indicating a fundamental shift in security priorities across the continent.

The market is being reshaped by stringent regulatory forces, particularly the implementation of the Network and Information Security Directive 2 (NIS2) and Digital Operational Resilience Act (DORA), which mandate comprehensive security testing for critical sectors. Cloud deployment dominates with 61% market share in 2024, while application security testing represents the largest type of segment at 39%. The United Kingdom leads geographically with 23.11% market share, though France exhibits the fastest growth at 26.4% CAGR through 2030, driven by substantial government investments in cybersecurity infrastructure.

Competitive intensity in the market is escalating as established players like Accenture and IBM face pressure from specialized European security testing providers leveraging AI-driven automation to deliver more efficient testing solutions. The market is witnessing a notable shift toward Interactive Application Security Testing (IAST), growing at 27.8% CAGR, as organizations seek to reduce false positives and integrate security earlier in development cycles. This trend is particularly pronounced in the manufacturing sector, which is experiencing the fastest growth among end-users at 25.2% CAGR due to increasing industrial IoT adoption and the convergence of IT and OT security requirements.

The fragmented data sovereignty rules across EU member states are creating implementation challenges for cloud-based security testing solutions, though this is simultaneously driving innovation in hybrid deployment models that can satisfy both operational and compliance requirements. The market's evolution is further characterized by the emergence of specialized testing methodologies for quantum-resistant cryptography, particularly in financial services and government sectors, where early pilots are already underway to prepare for post-quantum security threats.

Europe Security Testing Market Trends and Insights

Heightened Post-2023 Critical-Infrastructure Cyber-Attacks

A succession of sophisticated attacks on European power grids and rail systems in 2024 pushed critical-infrastructure operators to overhaul testing blueprints. ENISA logged a 38% rise in incidents, with OT infiltration techniques bypassing legacy perimeter controls. Security budgets have been redirected toward services capable of mapping vulnerabilities across converged IT-OT environments, especially in distribution networks handling supervisory control and data acquisition traffic. Providers responding with combined red- and blue-team engagements are benefiting from contract sizes that now extend across multi-country footprints. Expansion of mandatory incident reporting regimes further cements demand, as real-time testing evidence becomes essential for regulatory filings.

Accelerated EU NIS2 & DORA Compliance Deadlines

NIS2 enforcement in October 2024 and DORA's go-live in January 2025 compressed compliance windows and forced organizations to institutionalize recurring security assessments. DORA's three-year threat-led penetration-testing cycle for banks has already triggered multiyear framework agreements with external testers, while NIS2's supply-chain focus is driving downstream validation of third-party code repositories. Cross-border conglomerates are centralizing test orchestration to avoid audit duplication, spurring uptake of unified platforms that schedule, execute, and document evidence for multiple regulators.

Shortage of CREST-Certified Security Testers

Europe's talent deficit remains acute, with the United Kingdom alone needing 7,000 additional professionals every year. The gap is especially sharp in cloud and OT disciplines, delaying project kick-offs for large transformation programs. Automation mitigates routine tasks yet cannot replace the contextual analysis clients expect from senior testers, thereby constraining the absolute delivery capacity of the Europe security testing market.

Other drivers and restraints analyzed in the detailed report include:

- Shift-Left DevSecOps Adoption in the Software Supply Chain

- Industrial IoT Penetration in German Mittelst and Factories

- Budget Freeze Across EU-27 SMEs Amid 2024 Credit-Tightening

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud-based models delivered 61% of the Europe security testing market in 2024 and are on track for a 26.01% CAGR through 2030. The Europe security testing market size for cloud deployment is projected to reach USD 54 billion by 2030, reflecting mounting demand for elastic test environments that replicate attacker geographies within minutes. United Kingdom enterprises typically launch weekly external attack simulations from cloud-native platforms, while German firms favour hybrid configurations that retain encryption keys on-premises. Providers now bundle sovereign-cloud controls such as in-region key management and dedicated SOC staffing to satisfy France's strict data-locality statutes. On-premises installations remain relevant where classified information is processed, notably in defense ministries, yet even these agencies pilot secure "compute-out, data-in" patterns that keep test logs offsite while restricting raw data exfiltration. As European hyperscalers pledge multibillion-euro investments in regional zones, hybrid orchestration has emerged as a pragmatic bridge for organizations balancing operational agility with national-security mandates. The Europe security testing market therefore continues to pivot toward integrated deployment portfolios that shift workloads seamlessly between private racks and regulated clouds without disrupting audit trails.

Application security testing (AST) generated 39% of the Europe security testing market revenue in 2024 and leads adoption curves as web, mobile, and serverless workloads multiply. Within AST, cloud-specific assessments post the steepest climb at 31% CAGR, propelled by DORA clauses obliging financial entities to review both legacy and containerized code. The Europe security testing market share for AST is bolstered by continuous integration tools that embed dynamic scans into commit pipelines, enabling risk triaging before production. Network security testing still anchors zero-trust rollouts, particularly for segmenting flat networks amassed through M&A activity. VPN assessments gained urgency following publicized remote-access exploits that bypassed multi-factor authentication. Firewall testing, formerly a ruleset hygiene exercise, now incorporates evasive-traffic emulation to gauge inspection depth against adversaries using domain fronting. As cloud, mobile, and API surfaces converge, enterprises increasingly commission unified engagements that cross-reference findings from multiple test types, maximizing coverage without inflating budgets.

Europe Security Testing Market Segmented by Deployment (On-Premises, Cloud and Hybrid), Type (Network Security Testing, Application Security Testing and More), Testing Tool (Web Application Testing Tool, Code Review Tool and More), End-User Industry (Government, BFSI and More) and Country. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Accenture

- Atos

- Cisco Systems

- Core Security Technologies

- CrowdStrike

- Fortinet

- Hewlett Packard Enterprise

- IBM

- Kaspersky

- Micro Focus (CyberRes)

- McAfee

- Netcraft

- Offensive Security

- Orange Cyberdefense

- Paladion (Tech Mahindra)

- PwC

- Qualys

- Securonix

- Synopsys

- Veracode

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Heightened post-2023 critical-infrastructure cyber-attacks (Power and Rail)

- 4.2.2 Accelerated EU NIS2 and DORA compliance deadlines

- 4.2.3 Shift-left DevSecOps adoption in software supply-chain

- 4.2.4 Industrial IoT penetration in German Mittelstand factories

- 4.2.5 Mandatory penetration-testing clauses in European public-sector tenders

- 4.2.6 Quantum-resistant crypto migration pilots (under-the-radar)

- 4.3 Market Restraints

- 4.3.1 Shortage of CREST-certified security testers

- 4.3.2 Budget freeze across EU-27 SMEs amid 2024 credit-tightening

- 4.3.3 Fragmented data-sovereignty rules slowing cloud-based testing

- 4.3.4 False-positive fatigue reducing test frequency (under-the-radar)

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment

- 5.1.1 On-Premise

- 5.1.2 Cloud

- 5.1.3 Hybrid

- 5.2 By Type

- 5.2.1 Network Security Testing

- 5.2.1.1 VPN Testing

- 5.2.1.2 Firewall Testing

- 5.2.1.3 Other Service Types

- 5.2.2 Application Security Testing

- 5.2.2.1 By Application Type

- 5.2.2.1.1 Mobile Application Security Testing

- 5.2.2.1.2 Web Application Security Testing

- 5.2.2.1.3 Cloud Application Security Testing

- 5.2.2.1.4 Enterprise Application Security Testing

- 5.2.2.2 By Testing Type

- 5.2.2.2.1 SAST

- 5.2.2.2.2 DAST

- 5.2.2.2.3 IAST

- 5.2.2.2.4 RASP

- 5.2.1 Network Security Testing

- 5.3 By End-User Industry

- 5.3.1 Government

- 5.3.2 BFSI

- 5.3.3 Healthcare

- 5.3.4 Manufacturing

- 5.3.5 IT and Telecom

- 5.3.6 Retail

- 5.3.7 Other End-User Industries

- 5.4 By Testing Tool

- 5.4.1 Web Application Testing Tool

- 5.4.2 Code Review Tool

- 5.4.3 Penetration Testing Tool

- 5.4.4 Software Testing Tool

- 5.4.5 Other Testing Tools

- 5.5 By Country

- 5.5.1 United Kingdom

- 5.5.2 Germany

- 5.5.3 France

- 5.5.4 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Accenture

- 6.4.2 Atos

- 6.4.3 Cisco Systems

- 6.4.4 Core Security Technologies

- 6.4.5 CrowdStrike

- 6.4.6 Fortinet

- 6.4.7 Hewlett Packard Enterprise

- 6.4.8 IBM

- 6.4.9 Kaspersky

- 6.4.10 Micro Focus (CyberRes)

- 6.4.11 McAfee

- 6.4.12 Netcraft

- 6.4.13 Offensive Security

- 6.4.14 Orange Cyberdefense

- 6.4.15 Paladion (Tech Mahindra)

- 6.4.16 PwC

- 6.4.17 Qualys

- 6.4.18 Securonix

- 6.4.19 Synopsys

- 6.4.20 Veracode

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet Need Analysis

安全測試市場報告:按類型、測試工具、部署模式、最終用戶和地區分類,2026-2034 年

安全測試市場報告:按類型、測試工具、部署模式、最終用戶和地區分類,2026-2034 年 安全測試市場:按類型、組件、調查方法、產業、部署模型和組織規模分類-2026-2032年全球市場預測

安全測試市場:按類型、組件、調查方法、產業、部署模型和組織規模分類-2026-2032年全球市場預測 2026年全球安全測試市場報告

2026年全球安全測試市場報告 全球安全測試市場:按類型、網路安全測試、應用測試工具分類-預測(至 2031 年)

全球安全測試市場:按類型、網路安全測試、應用測試工具分類-預測(至 2031 年) 安全測試市場分析及預測(至 2035 年):按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶和解決方案分類日本安全測試市場報告(按類型、測試工具、部署模式、最終用戶和地區分類,2026-2034 年)

安全測試市場分析及預測(至 2035 年):按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶和解決方案分類日本安全測試市場報告(按類型、測試工具、部署模式、最終用戶和地區分類,2026-2034 年) 全球安全測試市場:市場規模、佔有率和趨勢分析(按類型、技術、部署方法、組織規模、最終用途和地區)、按細分市場預測(2025-2033)

全球安全測試市場:市場規模、佔有率和趨勢分析(按類型、技術、部署方法、組織規模、最終用途和地區)、按細分市場預測(2025-2033) 安全測試市場:按測試類型、按部署模式、按組織規模、垂直行業和按地區

安全測試市場:按測試類型、按部署模式、按組織規模、垂直行業和按地區 安全測試市場規模、佔有率和成長分析(按測試類型、部署模式、網路安全測試類型、組織規模、垂直和地區)- 2025-2032 年產業預測

安全測試市場規模、佔有率和成長分析(按測試類型、部署模式、網路安全測試類型、組織規模、垂直和地區)- 2025-2032 年產業預測 亞太安全測試 -市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

亞太安全測試 -市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)