|

市場調查報告書

商品編碼

2035062

資料中心UPS:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)Data Center UPS - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

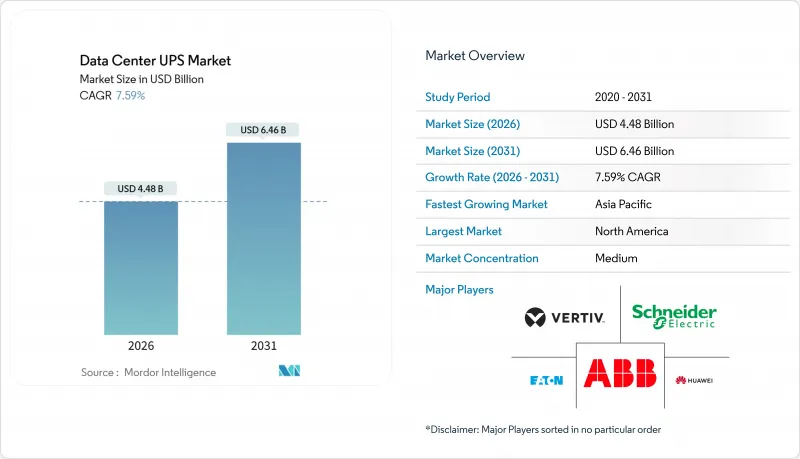

預計到 2026 年,資料中心 UPS 市場規模將達到 44.8 億美元,到 2031 年將達到 64.6 億美元,複合年成長率為 7.59%。

這份展望闡述了人工智慧 (AI) 工作負載、機架功率密度不斷提高以及資料主權政策如何推動營運商轉向雙轉換和模組化拓撲結構,以在維持持續高電流負載的同時降低熱風險。供應商正在重新設計採用碳化矽 (SiC) 半導體的逆變器級,以應對供應鏈中斷的影響。隨著鋰離子電池在超過 500 kVA 的系統中實現總擁有成本 (TCO) 持平,資料中心 UPS 市場正轉向化學電池,以實現併網儲能。零售和電信業的邊緣部署正在催生一個分散式、小型化的需求細分市場,擴大基本客群的同時,也對傳統銷售管道提出了挑戰。同時,歐洲主要城市資料中心建設的凍結正將資金轉移到區域性城市,並加速向液冷技術的轉型,從而縮小了上游 UPS 的規模。

全球資料中心UPS市場趨勢與洞察

超大規模資料中心正在加速擴張,越來越多的設施容量超過 10MW。

到2025年,超大規模業者將運作47個容量超過10兆瓦的園區,年增38%,從而形成一個持續多年的UPS採購計畫。典型的園區設計方案包括部署4-6組容量為2-3兆伏安的UPS,單筆合約金額超過1500萬美元,這使得供應商能夠根據需求定製冷卻介面和電池機殼類型。由於北維吉尼亞和新加坡的電力公司目前預計併網等待時間為36-48個月,開發商正在指定配備柴油旋轉備用電源的UPS設備,以應對持續數小時的停電。模組化機架可以以500千伏安為增量進行擴展,使建造者能夠隨著伺服器機架的部署分階段進行資本投資,從而減少因容量閒置造成的損失。歐盟和印度的自主人工智慧法規正在推動新一輪5-8兆瓦的部署,將超大規模資料中心的版圖擴展到傳統的北美地區之外。

AI 和 ML 工作負載的功率密度正在飆升:每個機架超過 20kW。

到2026年,訓練叢集的功率密度將超過每機架100kW,遠超過兩年前的15-20kW標準。這種巨大的轉變迫使UPS製造商重新設計配電單元,使其能夠提供400A的連續電流而不產生電壓降。在高密度環境下,由於長銅線造成的電阻損耗,集中式機房的管理難度加大,加速了安裝在負載10公尺範圍內的柱式模組的轉變。直接晶片冷卻(DTC)技術消除了風扇的額外功耗,使營運商能夠將UPS的額定容量降低高達20%。鋰離子電池的能量密度為250Wh/L,而VRLA(鉛酸電池)的能量密度僅80Wh/L,鋰離子面積更小,釋放了更多機架空間,降低了每機架UPS的成本。日益成長的複雜性加劇了技能差距,促使買家轉向包含安裝、試運行和遠端監控的承包工程合約。

初始資本支出(CAPEX)溢價:約為雙重轉換法的 35%。

採用雙級逆變器和大型散熱器的雙轉換系統比線上互動式UPS貴約35%,這給力求達到Tier III標準的企業帶來了沉重的資本預算壓力。目前,租賃方案將UPS容量打包成服務,透過將資本支出(CAPEX)轉化為營運支出(OPEX)來降低採用難度,但新興市場的利率仍超過10%,阻礙了其廣泛應用。模組化機架可以100-500 kVA為增量進行擴展,有助於買家融資,但由於韌體不一致和負載平衡邏輯等互通性問題,可能會帶來潛在的可靠性風險。低成本的中國進口產品提供了一種替代方案,但對智慧財產權和售後服務的擔憂限制了其在亞太地區以外地區的普及。因此,價格差異限制了資料中心UPS市場中預算敏感型用戶的潛在客戶群。

細分市場分析

模組化和平行冗餘機架預計將以 8.13% 的複合年成長率成長,超過整個資料中心 UPS 市場的成長速度。雙轉換在線式 UPS 仍將主導市場,到 2025 年將佔據 44.65% 的市場佔有率,以滿足 Tier III 和 Tier IV 機房對無縫容錯移轉的需求。線上互動式 UPS 產品在小規模企業環境中保持著一定的市場佔有率,其 40% 的成本優勢彌補了諧波失真和較短的運作。另一方面,備用 UPS 則廣泛部署在邊緣機櫃中,以滿足對超低資本支出 (CAPEX) 的需求。對於柴油發電機起火後需要 20 秒內恢復供電的設施,旋轉式和飛輪式 UPS 可供選擇,補償了機械結構的複雜性,以方便電池維護。

隨著機架密度的增加,採購決策正朝著模組化方向發展。這是因為資料中心的負載在一個租賃期內可能從 500 kVA 飆升至 2 MVA。能夠以 100-500 kVA 為增量進行擴展的機架可以避免在 30% 負載下運作帶來的效率下降,並提高年度電源使用效率 (PUE)。軟體定義控制層可以調節負載平衡,但這會帶來韌體管理方面的風險,營運商必須對其進行審核。因此,模組化方案與按需計費的託管租賃模式一起,正持續獲得廣泛應用。

2025年,容量超過200 kVA的系統將佔總銷售額的52.23%,預計2031年將達到8.56%的複合年成長率,高於整體市場成長率。大型機架系統的經濟優勢在每機架功率超過100 kW的人工智慧訓練叢集中得到了充分體現,這類集群通常需要並聯UPS電源組。

21–200 kVA 等級的設備適用於企業和區域託管設施,這些設施的機架功率密度通常低於 15 kW。 20 kVA 以下的設備安裝在零售和電信行業的邊緣節點,但由於伺服器機架整合式電源模組無需外部機櫃,因此面臨價格壓力。企業站點整合為兆瓦級園區進一步增加了對更大容量機架的需求。

儘管截至2025年,集中式機房仍佔據46.21%的市場佔有率,但隨著營運商追求能源效率和快速恢復,分散式架構正以8.72%的複合年成長率快速擴張。將UPS模組放置在距離負載10公尺以內,可減少高達5%的銅纜損耗。

然而,在四級設施中,集中式 2N+1 佈局仍然是首選,因為它簡化了認證審核。在分階段擴建中,分散式設計更具優勢,因為初始設備安裝可以從單排開始,從而可以將 40-60% 的 UPS 設備投資推遲到租戶需求出現時再進行。在現有設施的維修中,通常會保留集中式機房,並考慮先前在開關設備和母線槽方面的投資。

區域分析

北美地區,尤其是北維吉尼亞、矽谷和達拉斯-沃斯堡地區,集中了大量超大規模資料中心,預計到2025年將佔全球營收的39.43%。然而,由於土地稀缺和長達48個月的公共產業等待期,投資人正將目光轉向鳳凰城、亞特蘭大和哥倫布等城市,北美地區的成長速度正在放緩。加拿大憑藉其豐富的水力資源和涼爽的氣候吸引超大規模資料中心超大規模資料中心業者,但跨境資料監管使得工作負載向美國部署變得更加複雜。墨西哥正致力於蒙特雷和克雷塔羅的電網升級,以滿足近岸外包的需求。預計到2025年,鋰離子電池的普及率將超過40%,而總擁有成本(TCO)將成為重點領域。該地區擁有超過120個認證機房,並且是全球採用Tier IV標準的領先地區。

亞太地區預計將以9.02%的複合年成長率成長。在中國,二線城市憑藉廉價可再生能源的吸引力吸引了大量建設項目,而一線城市則面臨電力供應上限。在印度,由於數位支付的成長和強制性數據本地化,託管需求激增,但每月4-6小時的停電迫使企業對UPS系統進行過度設計。新加坡在2024年部分取消了2019年的建設上限,但這僅限於電源使用效率(PUE)低於1.3的設施。日本和澳洲擁有成熟的三級基礎設施,但面臨土地短缺,並擴大採用模組化UPS機架。東南亞,特別是馬來西亞和印度尼西亞,行動商務相關的邊緣運算需求正在成長,部署主要集中在20-100 kVA頻寬內。

到2025年,歐洲將佔全球人工智慧支出的約25%,但在一些城市建設暫停令限制水和電力分配的地區,成長速度正在放緩。 2026年生效的碳邊境調節機制將對高碳排放零件的供應鏈進行處罰,引導採購流向斯堪的斯堪地那維亞和德國的可再生能源工廠。政府主導的人工智慧應用強制令正在加速四級城市(Tier IV)的建設,振興斯德哥爾摩和米蘭等二線都市區。英國正受惠於脫歐後的數據監管政策,而南歐則利用太陽能和廉價土地與傳統樞紐城市競爭。南美洲的小規模,但巴西的數據主權法和智利的綠色能源正在吸引早期參與企業。中東地區正加速發展,政府已撥款100億美元用於區域人工智慧中心建設;非洲的成長中心主導在南非和奈及利亞,通訊業者正在這些國家建立邊緣基礎設施。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 超大規模資料中心(10兆瓦或以上)的建置正在加速。

- 零售和電信產業邊緣微型資料中心的激增。

- 超大規模資料中心業者的碳中和採購義務

- 在 500 kVA 或以上的 UPS 系統中,鋰離子電池相對於 VRLA 電池具有 TCO 優勢。

- AI/ML 工作負載的功率密度激增(20 kW/機架或更高)。

- 新興市場強制要求滿足三級以上運轉率的供應要求

- 市場限制因素

- 雙轉換拓樸結構的初始資本投資溢價(約 35%)

- 有關併網儲能的法規仍處於起步階段。

- 電力電子元件供應鏈波動

- 暫時中止歐盟主要城市資料中心的水和能源使用限制。

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的競爭

- 宏觀經濟因素對市場的影響

第5章 市場規模與成長預測

- UPS 類型

- 支援

- Line Interactive

- 雙轉換在線

- 模組化/並行冗餘

- 旋轉和飛輪

- 按功率容量

- 20千伏安或以下

- 21~200 kVA

- 超過200千伏安

- 以建築學為例

- 集中管理

- 分佈式(行級別)

- 模組化和擴充性

- 依電池類型

- 鉛酸蓄電池(VRLA)

- 鋰離子

- 鎳、鎘及其他

- 層級類型

- 一級和二級

- 三級

- 第四級

- 按資料中心規模

- 小規模資料中心

- 中型資料中心

- 大型資料中心

- 超大規模資料中心

- 依資料中心類型

- 託管資料中心

- 超大規模資料中心業者資料中心/雲端服務供應商

- 企業和邊緣資料中心

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 智利

- 阿根廷

- 南美洲其他地區

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 新加坡

- 澳洲

- 馬來西亞

- 亞太其他地區

- 中東和非洲

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲地區

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- ABB Ltd

- Schneider Electric SE

- Eaton Corporation plc

- Vertiv Holdings Co.

- Huawei Technologies Co. Ltd.

- Power Innovations International LLC

- Mitsubishi Electric Corp.

- Riello Elettronica SpA

- SOCOMEC Group SA

- Piller Power Systems GmbH

- Toshiba Corp.

- Gamatronic(SolarEdge Technologies Inc.)

- Delta Electronics Inc.

- Kohler Co.

- Legrand SA

- Socomec UPS India Pvt Ltd.

- Caterpillar Inc.

- AEG Power Solutions BV

- Tripp Lite(Eaton)

- Kehua Tech Co. Ltd.

第7章 市場機會與未來展望

The data center UPS market size stood at USD 4.48 billion in 2026 and is projected to reach USD 6.46 billion by 2031, reflecting a 7.59% CAGR.

This outlook captures how artificial intelligence workloads, rising rack power density, and sovereign data-sovereignty policies are steering operators toward double-conversion and modular topologies that sustain continuous high-current loads while keeping thermal risk in check. Vendors are redesigning inverter stages around silicon-carbide semiconductors to offset supply-chain shocks, and lithium-ion battery economics have hit total-cost-of-ownership parity in systems above 500 kVA, nudging the data center UPS market toward chemistries that enable grid-interactive storage. Edge deployments in retail and telecom add a distributed, small-form-factor layer of demand that challenges legacy sales channels yet broadens the customer base. At the same time, data-center moratoriums in leading European metros divert capital toward secondary cities and accelerate the shift to liquid cooling, which reduces upstream UPS sizing.

Global Data Center UPS Market Trends and Insights

Hyperscale Data-Center Build-Outs Accelerating >=10 MW Facilities

Hyperscale operators commissioned 47 campuses above 10 MW in 2025, a 38% annual jump that locks in multi-year UPS procurement pipelines. Typical site designs deploy four to six 2-3 MVA strings, creating single-contract values of USD 15 million or more and spurring vendor customization of cooling interfaces and battery enclosure formats. Utilities in Northern Virginia and Singapore now quote interconnection queues of 36-48 months, so developers specify UPS units with diesel rotary backup to bridge multi-hour grid outages. Modular frames that scale in 500 kVA steps let builders phase capital alongside server rack deployments, trimming idle capacity losses. Sovereign-AI rules in the European Union and India add another wave of 5-8 MW installations, broadening the hyperscale footprint beyond legacy North American hubs.

AI and ML Workload Power-Density Surge >=20 kW per Rack

Training clusters exceeded 100 kW per rack in 2026, eclipsing the 15-20 kW norm seen just two years earlier. This step-change forces UPS makers to redesign power distribution units capable of carrying 400 A continuous currents without voltage sag. Centralized rooms struggle at these densities because long copper runs incur resistive losses, catalyzing a shift to row-level modules situated within 10 m of the load. Direct-to-chip liquid cooling eliminates parasitic fan power, enabling operators to downsize rated UPS capacity by up to 20%. Floor-space savings from lithium-ion batteries, which pack 250 Wh/l compared with 80 Wh/l for VRLA, free up extra rack positions and reduce per-rack UPS cost. The complexity uptick widens a skills gap, steering buyers toward turnkey contracts that bundle installation, commissioning, and remote monitoring.

Upfront CAPEX Premium ~35% of Double-Conversion Topology

Double-conversion systems cost roughly 35% more than line-interactive models because they employ dual inverter stages and larger heat sinks, stretching capital budgets for enterprises targeting Tier III compliance. Leasing programs now package UPS capacity as a service, converting capex into opex and easing adoption, but finance rates in emerging markets still exceed 10%, dampening uptake. Modular frames that scale in 100-500 kVA blocks let buyers defer cash, yet interoperability issues such as mismatched firmware or load-sharing logic can expose hidden reliability risks. Lower-priced Chinese imports offer an alternative, but concerns around intellectual property and after-sales support curb penetration outside Asia-Pacific. The price gap therefore limits the addressable segment of the data center UPS market among budget-sensitive owners.

Other drivers and restraints analyzed in the detailed report include:

- Edge Micro-Data-Center Proliferation in Retail and Telecom

- Lithium-Ion TCO Advantage Over VRLA in >=500 kVA UPS

- Supply-Chain Volatility for Power Electronic Components

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Modular and parallel-redundant frames are set to expand at an 8.13% CAGR, outrunning the broader data center UPS market. Double-conversion online units still dominate with a 44.65% share in 2025, anchored in Tier III and Tier IV halls that need seamless failover. Line-interactive products retain a niche in small-enterprise rooms because their 40% cost advantage compensates for harmonic distortion and shorter runtime, while standby units populate edge cabinets, chasing ultra-low capex. Rotary and flywheel designs serve facilities that demand sub-20s ride-through for diesel generator fire, trading battery maintenance for mechanical complexity.

Rising rack densities tilt the procurement calculus toward modularity because data hall load can jump from 500 kVA to 2 MVA inside a single lease cycle. Frames that click in 100-500 kVA increments avoid the efficiency penalty of operating at 30% load, lifting annualized power-usage effectiveness. Software-defined control layers orchestrate load-sharing, but they introduce firmware-management risk that operators must audit. As a result, modular penetration continues to climb in tandem with colocation leasing models that meter power on demand.

Systems above 200 kVA represented 52.23% of 2025 revenue and are forecast to post an 8.56% CAGR to 2031, ahead of overall market velocity. AI training clusters exceeding 100 kW per rack routinely require parallel UPS strings, validating the economics of large-frame systems.

The 21-200 kVA tier underpins enterprise and regional colocation halls, where power density remains below 15 kW per rack. Sub-20 kVA units inhabit edge nodes in retail and telecom and face price compression from server-rack-integrated cartridges that eliminate the need for external cabinets. Consolidation of enterprise sites into megawatt campuses further swells demand for large frames.

Centralized halls still held a 46.21% share in 2025, but distributed architectures are advancing at an 8.72% CAGR as operators hunt for energy savings and faster repairs. Positioning UPS modules within 10 m of the load cuts copper losses by up to 5%.

Tier IV facilities, however, continue to prefer 2N+1 centralized layouts that simplify certification audits. Phased buildouts reward distributed designs because initial fit-out can start with a single row, deferring 40-60% of UPS capital until tenant demand materializes. Retrofit sites often stick with centralized rooms, given sunk costs in switchgear and busway.

The Data Center UPS Market Report is Segmented by UPS Type (Standby, Line-Interactive, and More), Power Capacity (<=20 KVA, and More), Architecture (Centralized, and More), Battery Type (Lead-Acid VRLA, Lithium-Ion, and More), Tier Type (Tier 1 and 2, Tier 3, and Tier 4), Data Center Size (Small, Medium, and More), Data Center Type (Colocation, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America controlled 39.43% of 2025 revenue thanks to hyperscale density in Northern Virginia, Silicon Valley, and Dallas-Fort Worth. Growth moderates as land scarcity and 48-month utility queues push investors toward Phoenix, Atlanta, and Columbus. Canada uses hydroelectric surplus and cool weather to attract hyperscalers, yet cross-border data rules complicate U.S. workload placement. Mexico eyes grid upgrades in Monterrey and Queretaro to capture nearshoring demand. Lithium-ion penetration exceeded 40% of 2025 installs, underscoring TCO priorities. The region leads Tier IV adoption with more than 120 certified halls.

Asia-Pacific is set for a 9.02% CAGR as China's tier-2 cities entice builds with cheap renewable power while tier-1 metros face energy caps. India's colocation surge rides on digital payment growth and data-localization mandates, though 4-6-hour monthly grid outages force oversizing of UPS strings. Singapore partially lifted its 2019 build cap in 2024, but only for facilities that achieve power-usage effectiveness below 1.3. Japan and Australia maintain mature Tier III footprints but wrestle with land scarcity that favors modular UPS frames. Southeast Asia, particularly Malaysia and Indonesia, sees edge demand tied to mobile commerce, with deployments clustering in the 20-100 kVA band.

Europe accounted for roughly 25% of global spend in 2025, yet growth slows where city moratoriums cap water or power allocations. The Carbon Border Adjustment Mechanism effective 2026 penalizes carbon-heavy component supply chains, nudging procurement toward renewable-powered fabs in Scandinavia and Germany. Sovereign-AI mandates accelerate Tier IV builds, boosting secondary metros like Stockholm and Milan. The United Kingdom benefits from post-Brexit data rules, while Southern Europe leverages solar power and cheaper land to rival historic hubs. South America stays sub-scale, though Brazil's data-sovereignty law and Chile's green energy draw early movers. The Middle East accelerates with USD 10 billion earmarked for regional AI hubs, and Africa's pockets of growth center on South Africa and Nigeria where telecom-led edge builds take root.

- ABB Ltd

- Schneider Electric SE

- Eaton Corporation plc

- Vertiv Holdings Co.

- Huawei Technologies Co. Ltd.

- Power Innovations International LLC

- Mitsubishi Electric Corp.

- Riello Elettronica S.p.A

- SOCOMEC Group S.A.

- Piller Power Systems GmbH

- Toshiba Corp.

- Gamatronic (SolarEdge Technologies Inc.)

- Delta Electronics Inc.

- Kohler Co.

- Legrand SA

- Socomec UPS India Pvt Ltd.

- Caterpillar Inc.

- AEG Power Solutions BV

- Tripp Lite (Eaton)

- Kehua Tech Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Hyperscale Data-Center Build-Outs Accelerating >=10 MW Facilities

- 4.2.2 Edge Micro-Data-Center Proliferation in Retail and Telecom

- 4.2.3 Carbon-Neutral Procurement Mandates by Hyperscalers

- 4.2.4 Lithium-Ion TCO Advantage Over VRLA in >=500 kVA UPS

- 4.2.5 AI / ML Workload Power-Density (>=20 kW / Rack) Surge

- 4.2.6 Mandatory Tier III+ Uptime Compliance in Emerging Markets

- 4.3 Market Restraints

- 4.3.1 Upfront CAPEX Premium (≈35 %) of Double-Conversion Topology

- 4.3.2 Grid-Interactive Energy-Storage Regulations Still Nascent

- 4.3.3 Supply-Chain Volatility for Power Electronic Components

- 4.3.4 Data-Center Moratoriums on Water / Energy Use in EU Metros

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By UPS Type

- 5.1.1 Standby

- 5.1.2 Line-Interactive

- 5.1.3 Double-Conversion On-Line

- 5.1.4 Modular / Parallel-Redundant

- 5.1.5 Rotary and Flywheel

- 5.2 By Power Capacity

- 5.2.1 <=20 kVA

- 5.2.2 21-200 kVA

- 5.2.3 >200 kVA

- 5.3 By Architecture

- 5.3.1 Centralized

- 5.3.2 Distributed (Row-Level)

- 5.3.3 Modular Scalable

- 5.4 By Battery Type

- 5.4.1 Lead-Acid (VRLA)

- 5.4.2 Lithium-Ion

- 5.4.3 Nickel-Cadmium and Others

- 5.5 By Tier Type

- 5.5.1 Tier 1 and 2

- 5.5.2 Tier 3

- 5.5.3 Tier 4

- 5.6 By Data Center Size

- 5.6.1 Small Data Center

- 5.6.2 Medium Data Center

- 5.6.3 Large Data Center

- 5.6.4 Hyperscale Data Center

- 5.7 By Data Center Type

- 5.7.1 Colocation Data Center

- 5.7.2 Hyperscalers Data Center/CSPs

- 5.7.3 Enterprise and Edge Data Center

- 5.8 By Geography

- 5.8.1 North America

- 5.8.1.1 United States

- 5.8.1.2 Canada

- 5.8.1.3 Mexico

- 5.8.2 South America

- 5.8.2.1 Brazil

- 5.8.2.2 Chile

- 5.8.2.3 Argentina

- 5.8.2.4 Rest of South America

- 5.8.3 Europe

- 5.8.3.1 United Kingdom

- 5.8.3.2 Germany

- 5.8.3.3 France

- 5.8.3.4 Italy

- 5.8.3.5 Spain

- 5.8.3.6 Rest of Europe

- 5.8.4 Asia-Pacific

- 5.8.4.1 China

- 5.8.4.2 Japan

- 5.8.4.3 India

- 5.8.4.4 Singapore

- 5.8.4.5 Australia

- 5.8.4.6 Malaysia

- 5.8.4.7 Rest of Asia-Pacific

- 5.8.5 Middle East and Africa

- 5.8.5.1 Middle East

- 5.8.5.1.1 United Arab Emirates

- 5.8.5.1.2 Saudi Arabia

- 5.8.5.1.3 Turkey

- 5.8.5.1.4 Rest of Middle East

- 5.8.5.2 Africa

- 5.8.5.2.1 South Africa

- 5.8.5.2.2 Nigeria

- 5.8.5.2.3 Rest of Africa

- 5.8.5.1 Middle East

- 5.8.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 ABB Ltd

- 6.4.2 Schneider Electric SE

- 6.4.3 Eaton Corporation plc

- 6.4.4 Vertiv Holdings Co.

- 6.4.5 Huawei Technologies Co. Ltd.

- 6.4.6 Power Innovations International LLC

- 6.4.7 Mitsubishi Electric Corp.

- 6.4.8 Riello Elettronica S.p.A

- 6.4.9 SOCOMEC Group S.A.

- 6.4.10 Piller Power Systems GmbH

- 6.4.11 Toshiba Corp.

- 6.4.12 Gamatronic (SolarEdge Technologies Inc.)

- 6.4.13 Delta Electronics Inc.

- 6.4.14 Kohler Co.

- 6.4.15 Legrand SA

- 6.4.16 Socomec UPS India Pvt Ltd.

- 6.4.17 Caterpillar Inc.

- 6.4.18 AEG Power Solutions BV

- 6.4.19 Tripp Lite (Eaton)

- 6.4.20 Kehua Tech Co. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

全球資料中心UPS市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球資料中心UPS市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026年全球資料中心不斷電系統(UPS)市場報告

2026年全球資料中心不斷電系統(UPS)市場報告 資料中心不斷電系統(UPS)市場:按類型、設計類型、容量、組件、部署模式、最終用戶和分銷管道分類-2026年至2032年全球預測

資料中心不斷電系統(UPS)市場:按類型、設計類型、容量、組件、部署模式、最終用戶和分銷管道分類-2026年至2032年全球預測 資料中心UPS市場分析及預測(至2035年):依類型、產品、服務、技術、組件、應用、部署、最終使用者、功能及安裝類型分類

資料中心UPS市場分析及預測(至2035年):依類型、產品、服務、技術、組件、應用、部署、最終使用者、功能及安裝類型分類 資料中心UPS市場:依拓撲結構(線上雙轉換、線上互動、備用)、模組化(模組化、一體式)、電池類型(VRLA、鋰離子)和應用(超大規模、託管、企業級、邊緣運算)劃分-全球預測至2036年2026年全球資料中心不斷電系統(UPS)市場報告

資料中心UPS市場:依拓撲結構(線上雙轉換、線上互動、備用)、模組化(模組化、一體式)、電池類型(VRLA、鋰離子)和應用(超大規模、託管、企業級、邊緣運算)劃分-全球預測至2036年2026年全球資料中心不斷電系統(UPS)市場報告 備用式UPS系統市場-全球產業規模、佔有率、趨勢、機會及預測(依容量、應用、地區及競爭格局分類,2021-2031年)資料中心UPS市場 - 全球產業規模、佔有率、趨勢、機會、預測:按產量、拓樸結構、應用、地區和競爭格局分類,2021-2031年資料中心UPS市場規模、佔有率、成長、全球產業分析:依類型、應用、區域洞察與預測(2026-2034)

備用式UPS系統市場-全球產業規模、佔有率、趨勢、機會及預測(依容量、應用、地區及競爭格局分類,2021-2031年)資料中心UPS市場 - 全球產業規模、佔有率、趨勢、機會、預測:按產量、拓樸結構、應用、地區和競爭格局分類,2021-2031年資料中心UPS市場規模、佔有率、成長、全球產業分析:依類型、應用、區域洞察與預測(2026-2034) 資料中心UPS市場規模、佔有率和成長分析(按類型、產品、容量、電池類型、資料中心類型、資料中心規模、應用和地區分類)—產業預測(2026-2033年)

資料中心UPS市場規模、佔有率和成長分析(按類型、產品、容量、電池類型、資料中心類型、資料中心規模、應用和地區分類)—產業預測(2026-2033年)