|

市場調查報告書

商品編碼

1850085

石油和天然氣安全:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)Oil And Gas Security - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

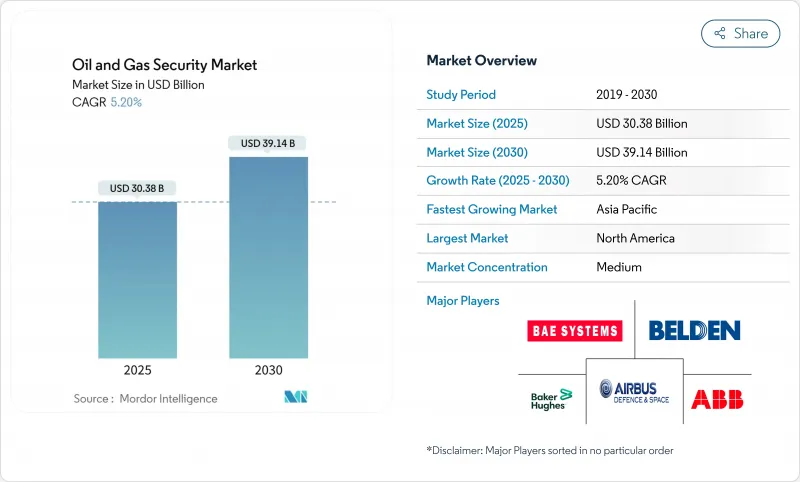

預計 2025 年石油和天然氣安全市場規模為 303.8 億美元,到 2030 年將達到 391.4 億美元,預測期內(2025-2030 年)的複合年成長率為 5.20%。

這一成長軌跡表明,即使在大宗商品價格波動的情況下,能源公司仍在持續加大安全項目的投入。隨著網路事件不僅影響資訊技術 (IT) 資產,也影響操作技術(OT) 資產,主導公司正在加速從預防性安全措施轉向主動安全措施的轉變。日益加劇的地緣政治緊張局勢、日益嚴格的管道監管以及日益成長的保險需求,使得公司在網路和實體控制方面都投入了巨額預算。能夠提供整合 OT-IT 堆疊(包括硬體、軟體和託管服務)的供應商很可能在未來五年內獲得巨大的價值。

全球石油和天然氣安全市場趨勢和洞察

OT-IT融合的擴大增加了網路風險

曾經與企業網路隔離的營運資產如今已連接到雲端和企業系統,擴大了其攻擊面。這種連結引發的事件使攻擊者能夠將重點從IT轉移到對安全至關重要的OT,從而增加了物理中斷的可能性。美國機構報告稱,即使是低技能的團體也能成功攻擊工業控制系統,暴露出其薄弱的隔離措施和最低限度的多因素身份驗證。因此,網路分區、零信任策略和即時異常檢測正在從最佳實踐轉變為基本期望。隨著企業在不中斷生產的情況下進行現代化改造,日益增加的複雜性迫使企業分階段推出平行架構。改善管治以連接IT安全、工程和製造團隊是未來支出的關鍵組成部分。

強制性的TSA和IEC管道網路法規

運輸安全管理局(TSA) 修訂後的指令要求管道營運商在規定的期限內檢驗控制措施、彌補差距並報告違規行為。 IEC 62443 也正在成為全球控制系統的基準,而日本的 CERT 等區域組織則提供實施指導。歐洲的 NIS2 指示進一步增加了義務,要求在 24 小時內揭露事件。不合規行為將面臨經濟處罰和潛在的停工令,這已將安全保障從一項可自由支配的開支提升為一項營運必需品。隨著營運商尋求承包違規方案,對同時具備管治和技術部署專業知識的供應商的需求也日益增加。

舊式 SCADA 升級成本超支

許多平台依賴已有20年歷史的監控系統,而這些系統的設計初衷並非針對網路暴露。企業經常低估分段、多因素身份驗證和加密遙測所需的工程和停機成本。當相容性問題在部署中期浮現時,升級成本往往是原始預算的兩到三倍。更長的資產生命週期使得資本配置變得困難,迫使營運商在短期生產力損失和長期彈性之間做出權衡。學術研究表明,低效率的跨職能溝通會進一步拖延執行並推高成本。

細分分析

到2024年,監控平台將佔據30.4%的收入佔有率,證實了市場長期以來對周界監控和情境察覺的關注。與視訊分析、無人機和門禁控制相關的石油和天然氣安全市場規模仍然龐大,但隨著預算轉向數位防禦,其年成長率將有所放緩。網路和網路安全解決方案的複合年成長率為8.1%,這反映了強制性的管道法規和針對現場資產的勒索軟體的興起。像「殖民管道」攻擊這樣的事件凸顯出,營運中斷可能是由於筆記型電腦而非圍欄突破造成的,這促使資本流向入侵偵測和安全的遠端存取閘道器。

展望未來,融合攝影機訊號與網路遙測的整合指揮中心預計將超越單一用途的部署。這種整合可以透過將實體徽章與網路登入關聯來減少誤報。能夠將攝影機、防火牆和控制器的事件交叉標記到統一螢幕上的供應商可能會在石油和天然氣安全市場中佔據越來越大的佔有率。因此,雖然監控系統仍然很重要,但它們正擴大被嵌入到更廣泛的網實整合平台中,導致獨立設備銷售下降,而軟體分析收入增加。

2024年,硬體仍將佔據石油和天然氣安全市場的52.6%,涵蓋危險區域強化防火牆、本質安全型攝影機和抗震伺服器。然而,隨著營運商簽訂24/7全天候監控和事件回應合約以填補技能短缺,託管服務細分市場的複合年成長率將達到9.3%。隨著新站點對高級分析、威脅情報回饋和定期紅隊評估的需求不斷增加,與服務保留相關的石油和天然氣安全市場規模正在擴大。

服務的成長也與需要獨立檢驗和記錄的監管審核息息相關。由於缺乏內部能力,企業正在轉向專門從事 OT 資產管理的託管服務供應商 (MSSP)。這些供應商將資產發現、漏洞管理和合規性報告捆綁在多年期合約中。硬體供應商正透過基於結果的模式來應對這項挑戰,將設備和服務打包在一起,從而拉平收益並深化客戶保留率。

石油和天然氣安全市場按安全產品類型(網路和網路安全、監視、篩檢和檢測等)、組件(硬體、軟體平台、服務)、營運階段(上游、中游、下游)、部署類型(內部部署、雲端、混合/邊緣雲端)、應用程式(探勘和生產站點、海上平台和 FPSO 等)和地區進行細分。

區域分析

受美國運輸安全管理局(TSA)強制指令以及Colonial Pipeline勒索軟體事件後續影響的推動,北美將在2024年佔據全球油氣安全市場的36.22%。加拿大的威脅評估報告指出,國營企業正將生產基地和中游樞紐作為攻擊目標,這促使政府在培訓和津貼(OT)細分方面建立公私合作夥伴關係。在聯邦審核指出防火牆過時且人機介面(HMI)未修補後,墨西哥灣和北坡的海上資產正在尋求緊急網路升級。

隨著中國擴大邊境地區的主幹管道和儲存容量,將營運技術安全與北京的主權雲端運算授權相結合,亞太地區到2030年的複合年成長率將達到9.1%,成為全球最高。日本將頒布經濟安全規則,將石油和天然氣列為關鍵社會基礎設施,要求業者向監管機構提交安全計畫。印度將擴建煉油廠和LNG接收站,並從班加羅爾和海得拉巴的當地安全營運中心採購託管服務。為因應南海地區日益緊張的局勢,澳洲和韓國將在新的液化天然氣出口計劃中納入營運技術安全條款。

在歐洲,現代化以NIS2框架為中心,該框架要求對重要能源營業單位進行全天候事件報告和年度審核。德國、法國和荷蘭的液化天然氣進口擴張規模不斷擴大,複雜性不斷增加,需要對海上到終端的連結進行加密。在中東和非洲,記錄在案的攻擊事件增加了206%,導致資金籌措投入增加,並在區域網路論壇上進行了展示。拉丁美洲仍處於起步階段,但隨著巴西、阿根廷和圭亞那加大產量並尋求與IEC 62443接軌,投資正在增加。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場狀況

- 市場概況

- 市場促進因素

- OT 和 IT 整合度的提高增加了網路風險

- 強制執行TSA和IEC管道網路規則

- 引入人工智慧預測安全分析

- 能源價格波動推動保險需求

- 需要從邊緣到核心的安全保障的海上自主資產

- 市場限制

- 傳統 SCADA 升級成本超支

- 偏遠盆地OT安全人才短缺

- 雲端基礎的資料主權糾紛

- ESG相關投資撤資抑制長期資本投資

- 產業價值鏈分析

- 監管格局

- 技術展望

- 產業吸引力-波特五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

- 影響市場的宏觀經濟因素

第5章市場規模與成長預測(價值)

- 按安全類型

- 網路和網路安全

- 監控

- 篩檢和檢測

- 指揮與控制

- 實體存取控制

- 其他類型

- 按組件

- 硬體

- 軟體平台

- 服務(託管和專業)

- 按營運階段

- 上游(探勘和生產)

- 中游(管道和儲存)

- 下游(煉油和分銷)

- 依部署方式

- 本地部署

- 雲

- 混合/邊緣雲端

- 按用途

- 探勘和生產基地

- 海上平台和FPSO

- 管道監控

- 煉油廠和石化廠

- 液化天然氣和天然氣處理

- 零售和配送終端

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 智利

- 南美洲其他地區

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 馬來西亞

- 新加坡

- 澳洲

- 其他亞太地區

- 中東和非洲

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 埃及

- 其他非洲國家

- 北美洲

第6章 競爭態勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- ABB Ltd.

- Airbus Defence and Space

- BAE Systems plc

- Baker Hughes Cyber-Security Services

- Belden Inc.

- Check Point Software Technologies Ltd.

- Cisco Systems Inc.

- Claroty Ltd.

- Dragos Inc.

- Fortinet Inc.

- Honeywell International Inc.

- Huawei Technologies Co. Ltd.

- Johnson Controls International plc

- Kaspersky Lab JSC

- Microsoft Corp.

- Nozomi Networks Inc.

- Palo Alto Networks Inc.

- Parsons Corp.

- Rockwell Automation Inc.

- Schneider Electric SE

- Siemens AG

- Tenable OT Security

- Thales Group

- Trend Micro Inc.

- Waterfall Security Solutions Ltd.

第7章 市場機會與未來趨勢

- 閒置頻段和未滿足需求評估

The Oil And Gas Security Market size is estimated at USD 30.38 billion in 2025, and is expected to reach USD 39.14 billion by 2030, at a CAGR of 5.20% during the forecast period (2025-2030).

This growth trajectory shows that energy companies are putting sustained capital into security programs even as commodity prices swing. The shift from reactive safeguards to proactive, intelligence-driven models is accelerating because cyber incidents now expose operational technology (OT) as well as information technology (IT) assets. Heightened geopolitical tension, stricter pipeline rules, and rising insurance prerequisites keep budgets anchored on both cyber and physical controls. Vendors that can blend hardware, software, and managed services into a unified OT-IT stack are positioned to capture disproportionate value in the next five years.

Global Oil And Gas Security Market Trends and Insights

Growing OT-IT Convergence Elevating Cyber-Risk

Operational assets, once isolated from corporate networks, now connect to cloud and enterprise systems, broadening attack surfaces. Incidents prompted by this linkage allow adversaries to pivot from IT into safety-critical OT, increasing the likelihood of physical disruption. United States agencies report that even low-skill groups successfully target industrial control systems, exposing weak segmentation and minimal multifactor authentication. Network zoning, zero-trust policies, and real-time anomaly detection are therefore moving from best practice to baseline expectation. Complexity grows as firms modernize without halting production, forcing staged rollouts and parallel architectures. Improved governance that aligns IT security, engineering, and production teams forms a critical piece of spend over the forecast horizon.

Mandatory TSA and IEC Cyber Rules for Pipelines

Revised Transportation Security Administration directives compel pipeline operators to verify controls, close gaps, and report breaches in set time windows. IEC 62443 is simultaneously emerging as the global control-system benchmark, with regional groups such as Japan's CERT delivering implementation guidance. Europe's NIS2 directive layers additional duties by mandating incident disclosure within 24 hours. Monetary penalties and potential shutdown orders for non-compliance raise security from discretionary spending to operational necessity. Vendors versed in both governance and technical deployment are in demand as operators seek turnkey compliance programs.

Legacy SCADA Upgrades Cost Overruns

Many platforms still rely on 20-year-old supervisory control systems never architected for network exposure. Firms routinely underestimate the engineering and downtime expense needed for segmentation, multifactor authentication, and encrypted telemetry. Upgrades often cost two to three times the original budget when compatibility hurdles surface mid-deployment. Extended asset lifecycles make capital allocation difficult, forcing operators to weigh short-term productivity loss against long-term resilience. Academic studies find that ineffective cross-department communication further delays execution and inflates cost.

Other drivers and restraints analyzed in the detailed report include:

- AI-Driven Predictive Security Analytics Adoption

- Energy-Price Volatility Boosting Insurance Requirements

- Shortage of OT-Security Talent in Remote Basins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Surveillance platforms commanded 30.4% revenue share in 2024, confirming the market's long-standing focus on perimeter and situational awareness. The oil and gas security market size tied to video analytics, drones, and access control remains significant, but annual growth moderates as budgets reallocate toward digital defenses. Network and cybersecurity solutions, advancing at an 8.1% CAGR, reflect mandatory pipeline rules and the rise in ransomware aimed at field assets. Incidents such as the Colonial Pipeline attack emphasized that an operational halt can stem from a laptop rather than a fence breach, nudging capital toward intrusion detection and secure remote-access gateways.

In the forecast window, integrated command centers that fuse camera feeds with cyber telemetry are expected to outpace single-purpose deployments. This convergence reduces false positives by correlating physical badges with network logins. Vendors able to cross-tag events from cameras, firewalls, and controllers into a unified screen are likely to capture an expanding slice of the oil and gas security market. Consequently, surveillance remains vital but increasingly embedded within broader cyber-physical platforms, moderating standalone unit sales while lifting software analytics revenue.

Hardware still comprised 52.6% of the oil and gas security market share in 2024, spanning firewalls ruggedized for hazardous zones, intrinsically safe cameras, and vibration-resistant servers. However, the managed-services segment posts a 9.3% CAGR as operators contract 24 X 7 monitoring and incident response to offset skill gaps. The oil and gas security market size attached to service retainers is increasing because each new site demands advanced analytics, threat intelligence feeds, and periodic red-team assessments.

Service growth is also tied to regulatory audits, which require independent validation and documentation. Firms lacking internal capacity rely on MSSPs that specialise in OT assets; these providers bundle asset discovery, vulnerability management, and compliance reporting into multi-year agreements. Hardware vendors are reacting through outcome-based models that package equipment and services, thereby smoothing revenue and deepening customer lock-in.

Oil and Gas Security Market is Segmented by Security Type (Network and Cyber Security, Surveillance, Screening and Detection, and More), Component (Hardware, Software Platforms, and Services), Operation Stage (Upstream, Midstream, and Downstream), Deployment Mode (On-Premise, Cloud, and Hybrid/Edge-Cloud), Application (Exploration and Production Sites, Offshore Platforms and FPSOs, and More), and Geography.

Geography Analysis

North America maintained a 36.22% stake in the oil and gas security market in 2024, supported by mandatory TSA directives and the lingering lessons of the Colonial Pipeline ransomware event. Canada's threat assessments cite state-sponsored actors targeting production and midstream hubs, prompting coordinated public-private drills and grants for OT segmentation. Offshore assets in the Gulf of Mexico and the North Slope face calls for urgent cyber upgrades following federal audits that flagged outdated firewalls and unpatched HMIs.

Asia-Pacific records the fastest CAGR at 9.1% through 2030 as China extends trunk pipelines and storage capacity into border regions, blending OT security with sovereign cloud mandates from Beijing. Japan legislated economic-security rules that classify oil and gas as critical social infrastructure, compelling operators to file security plans with regulators. India expands refinery capacity and LNG terminals, sourcing managed services from local security operations centers in Bengaluru and Hyderabad. Australia and South Korea embed OT security clauses into new LNG export projects after noting rising regional tension in the South China Sea.

Europe's modernization drive centers on the NIS2 framework that mandates 24-hour incident reporting and annual audits for essential energy entities. LNG import build-outs across Germany, France, and the Netherlands add scale and complexity, necessitating encrypted maritime-to-terminal links. The Middle East and Africa experience stepped-up funding after a 206% rise in documented attacks, showcased at regional cyber forums. Latin America remains nascent but sees incremental investment as Brazil, Argentina, and Guyana grow production and seek alignment with IEC 62443.

- ABB Ltd.

- Airbus Defence and Space

- BAE Systems plc

- Baker Hughes Cyber-Security Services

- Belden Inc.

- Check Point Software Technologies Ltd.

- Cisco Systems Inc.

- Claroty Ltd.

- Dragos Inc.

- Fortinet Inc.

- Honeywell International Inc.

- Huawei Technologies Co. Ltd.

- Johnson Controls International plc

- Kaspersky Lab JSC

- Microsoft Corp.

- Nozomi Networks Inc.

- Palo Alto Networks Inc.

- Parsons Corp.

- Rockwell Automation Inc.

- Schneider Electric SE

- Siemens AG

- Tenable OT Security

- Thales Group

- Trend Micro Inc.

- Waterfall Security Solutions Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing OT and IT convergence elevating cyber-risk

- 4.2.2 Mandatory TSA and IEC cyber rules for pipelines

- 4.2.3 AI-driven predictive security analytics adoption

- 4.2.4 Energy-price volatility boosting insurance requirements

- 4.2.5 Autonomous offshore assets needing edge-to-core security

- 4.3 Market Restraints

- 4.3.1 Legacy SCADA upgrades cost overruns

- 4.3.2 Shortage of OT-security talent in remote basins

- 4.3.3 Cloud-based data-sovereignty conflicts

- 4.3.4 ESG divestments curbing long-term capex

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Security Type

- 5.1.1 Network and Cyber Security

- 5.1.2 Surveillance

- 5.1.3 Screening and Detection

- 5.1.4 Command and Control

- 5.1.5 Physical Access Control

- 5.1.6 Other Types

- 5.2 By Component

- 5.2.1 Hardware

- 5.2.2 Software Platforms

- 5.2.3 Services (Managed and Professional)

- 5.3 By Operation Stage

- 5.3.1 Upstream (Exploration and Production)

- 5.3.2 Midstream (Pipelines and Storage)

- 5.3.3 Downstream (Refining and Distribution)

- 5.4 By Deployment Mode

- 5.4.1 On-premise

- 5.4.2 Cloud

- 5.4.3 Hybrid/Edge-Cloud

- 5.5 By Application

- 5.5.1 Exploration and Production Sites

- 5.5.2 Offshore Platforms and FPSOs

- 5.5.3 Pipeline Monitoring

- 5.5.4 Refineries and Petrochem Plants

- 5.5.5 LNG and Gas Processing

- 5.5.6 Retail and Distribution Terminals

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Chile

- 5.6.2.4 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 Malaysia

- 5.6.4.6 Singapore

- 5.6.4.7 Australia

- 5.6.4.8 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 United Arab Emirates

- 5.6.5.1.2 Saudi Arabia

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Egypt

- 5.6.5.2.4 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 ABB Ltd.

- 6.4.2 Airbus Defence and Space

- 6.4.3 BAE Systems plc

- 6.4.4 Baker Hughes Cyber-Security Services

- 6.4.5 Belden Inc.

- 6.4.6 Check Point Software Technologies Ltd.

- 6.4.7 Cisco Systems Inc.

- 6.4.8 Claroty Ltd.

- 6.4.9 Dragos Inc.

- 6.4.10 Fortinet Inc.

- 6.4.11 Honeywell International Inc.

- 6.4.12 Huawei Technologies Co. Ltd.

- 6.4.13 Johnson Controls International plc

- 6.4.14 Kaspersky Lab JSC

- 6.4.15 Microsoft Corp.

- 6.4.16 Nozomi Networks Inc.

- 6.4.17 Palo Alto Networks Inc.

- 6.4.18 Parsons Corp.

- 6.4.19 Rockwell Automation Inc.

- 6.4.20 Schneider Electric SE

- 6.4.21 Siemens AG

- 6.4.22 Tenable OT Security

- 6.4.23 Thales Group

- 6.4.24 Trend Micro Inc.

- 6.4.25 Waterfall Security Solutions Ltd.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 White-Space and Unmet-Need Assessment

石油與天然氣安全市場:2026-2032年全球市場預測(依安全類型、組件、價值鏈階段、營運環境和部署模式分類)

石油與天然氣安全市場:2026-2032年全球市場預測(依安全類型、組件、價值鏈階段、營運環境和部署模式分類) 石油和天然氣安全市場規模、佔有率、趨勢和預測:按組件、安全類型、應用和地區分類,2026-2034 年

石油和天然氣安全市場規模、佔有率、趨勢和預測:按組件、安全類型、應用和地區分類,2026-2034 年 石油和天然氣安全市場規模、佔有率和成長分析:按組件、營運階段、安全類型、威脅類型、技術、應用、最終用戶、地區和產業預測,2026-2033年

石油和天然氣安全市場規模、佔有率和成長分析:按組件、營運階段、安全類型、威脅類型、技術、應用、最終用戶、地區和產業預測,2026-2033年 石油和天然氣網路安全市場規模、佔有率和成長分析(按安全類型、組件、部署方法、應用和地區分類)- 產業預測(2026-2033 年)可再生能源 SCADA 市場(按組件、部署、通訊技術、應用和最終用戶分類)—2025-2030 年全球預測

石油和天然氣網路安全市場規模、佔有率和成長分析(按安全類型、組件、部署方法、應用和地區分類)- 產業預測(2026-2033 年)可再生能源 SCADA 市場(按組件、部署、通訊技術、應用和最終用戶分類)—2025-2030 年全球預測 全球石油與天然氣網路安全市場

全球石油與天然氣網路安全市場 全球可再生能源 SCADA 市場(按組件、行業類型、活動類型和地區分類)- 2030 年預測

全球可再生能源 SCADA 市場(按組件、行業類型、活動類型和地區分類)- 2030 年預測 石油和天然氣安全市場報告:2030 年趨勢、預測和競爭分析

石油和天然氣安全市場報告:2030 年趨勢、預測和競爭分析 石油和天然氣安全市場規模、佔有率和趨勢分析報告:2024-2030 年按組成部分、最終用途、地區和細分市場預測

石油和天然氣安全市場規模、佔有率和趨勢分析報告:2024-2030 年按組成部分、最終用途、地區和細分市場預測