|

市場調查報告書

商品編碼

1850068

汽車降雨感應器:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)Automotive Rain Sensor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

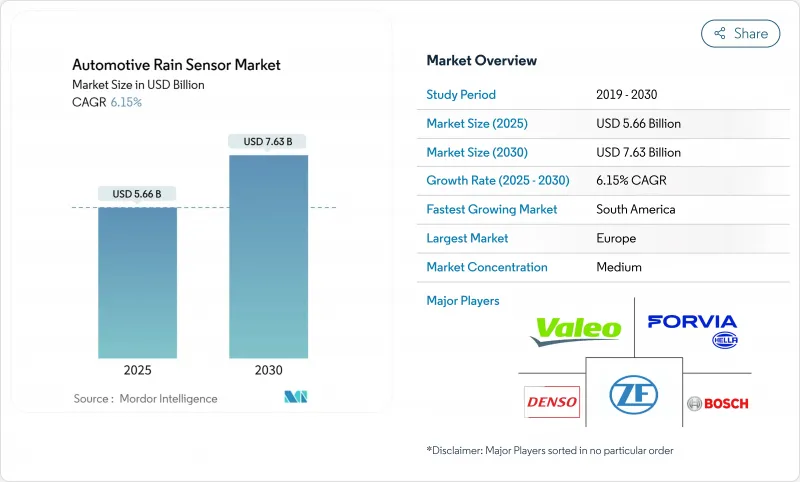

目前預計汽車降雨感應器市場規模將在 2025 年達到 56.6 億美元,預計到 2030 年將達到約 76.3 億美元,複合年成長率為 6.15%。

穩步推進的電氣化進程、L2+級駕駛援助系統的日益普及以及監管政策的不斷完善,正持續推動雨量感測器從舒適性添加物功能向安全關鍵型感測輸入設備轉變。 ADAS功能捆綁、半導體小型化以及支援訂閱的軟體堆疊正在擴大雨量感測器的潛在用戶群體,而降低成本的MEMS技術創新則正在擴大其在大眾市場的普及度。供應商與晶片製造商之間日益激烈的競爭也壓縮了硬體利潤空間,但同時也加速了整合光學、電容式和濕度模組的功能升級。綜上所述,隨著OEM廠商圍繞集中式、空中下載(OTA)和可更新的平台重建車輛電氣架構,這些因素共同作用,將使汽車降雨感應器市場在未來幾年持續處於轉型發展階段。

全球汽車降雨感應器市場趨勢及洞察

ADAS普及率的不斷提高使得多功能環境感知變得至關重要

L2+ 和 L3 級感知系統需要精確的雨滴、光照和霧氣數據,以確保相機鏡頭和雷射雷達視窗清晰,這使得感測器從可有可無的附加功能轉變為核心安全保障。歐洲的原始設備製造商 (OEM) 正在將光學降雨感應器與濕度和光照通道整合到單一 PCB 板上,從而減輕線束重量並實現整合診斷。北美卡車製造商也在將雨量偵測功能整合到前視叢集中,以延長自動緊急煞車的運作。高解析度 CCD 陣列能夠提高水滴分類的準確性,並將資料輸入到融合軟體中,該軟體可在單一控制迴路中協調雨刷速度、自我調整頭燈和除霧器邏輯。因此,採購團隊現在不僅關注雨刷延遲,還關注雷達和攝影機的協同性能指標,這使得多感測器解決方案的成功對於一級供應商的收入成長至關重要。

電氣化和高壓架構將推動其普及應用。

E平台可在400V和800V電壓下運行,為訊號處理ASIC和雷射微調VCSEL發射器提供穩定的功率餘量,在高濕度瞬變條件下性能優於12V同類產品。中央運算域透過安全的CAN-FD連結將原始水滴向量資料傳輸至區域控制器,機器學習模型在此最佳化擦拭巾時機,從而延長刮水片壽命並降低空調負荷。透過空中韌體更新,OEM廠商可以迭代地提高偵測閾值,從而開啟計量收費模式,並結合預測性維護警報功能。因此,電池供電品牌不再將降雨感應器作為被動式玻璃配件進行銷售,而是將其作為節能資產進行推廣,可減少高達6%的窗戶除霧次數。

入門A/B級車的價格敏感度較高

在印度、部分東協國家和拉丁美洲,成本主導平台為整個儀錶面板電子組件預留的預算不足75美元,幾乎沒有空間容納價格在25-30美元之間的降雨感應器模組。印度的國內含量法規提高了非本地化PCBA的進口關稅,擠壓了一級供應商的盈利,並減緩了採購速度。在整合MEMS的價格降至15美元以下之前,車長小於4公尺的車輛仍將依賴手動可變間歇式雨刷。與本地玻璃貼合夥伴關係建立合作關係的供應商可以降低運費額外費用,但目前訂單量低,此類資本支出難以實現。

細分市場分析

預計到2024年,乘用車降雨感應器市場將佔據71.23%的市場佔有率,並在2030年之前維持6.55%的強勁複合年成長率。轎車車型在各配置等級中保持穩定的安裝率,而掀背車的價格則繼續向高階車型傾斜。輕型商用車車隊擴大指定使用自動雨刷功能,以最大限度地減少駕駛員分心和保險索賠,而中型卡車由於改裝的複雜性而進展緩慢。需求調整將使平均系統構成比。

與週轉率高的輕型商用車車隊相比,乘用車的更新換代週期雖然較慢,但銷售成長穩定。研究遠端資訊處理技術的車隊營運商報告稱,啟用預測性雨刷分析功能後,擋風玻璃維修索賠減少了7%,這進一步增強了該技術的商業價值。總體而言,SUV的普及推動了汽車降雨感應器市場向功能豐富的套裝方向發展,而大規模生產的掀背車利潤率較低,這在一定程度上平衡了這一趨勢。

2024年,具有高信噪比的光學CCD/CMOS元件將佔總收入的81.64%。前五的光學控制器ASIC晶片已達到B版或更高版本,降低了成本曲線,使MEMS參與企業能夠獲得性價比優勢。電容式/MEMS裝置的複合年成長率將達到8.83%,因為它們可以避免玻璃鍵合的公差限制。紅外線反射式混合元件雖然單價較高,但將滿足-25 度C以下防冰性能的特定應用需求。

根據戰略藍圖,MEMS供應商正將環境光感測器和紅外線接近感測器整合到共用晶粒空間內,從而將PCB尺寸縮小35%。同時,光學產業的現有企業正透過整合尖端的AI推理核心來確保產量,以實現液滴的自校準識別並保持技術領先地位。光學裝置將繼續保持其高階和嚴苛應用領域的市場地位,而MEMS將推動其普及化。

區域分析

歐洲37.84%的市佔率反映了聯合國歐洲經濟委員會(UNECE)嚴格的可見度標準以及2025年新車撞擊測試(NCAP)的評分系統。此系統對雨水、光線和濕度融合功能給予兩分安全分,因此B級以上掀背車必須安裝感應器。南美洲成熟的高階車型組合也確保了高利潤光學陣列的主導地位。在巴西聖保羅大眾市場OEM中心的引領下,南美洲是成長最快的地區,複合年成長率(CAGR)高達10.33%。消費者從入門級車型升級到緊湊型SUV,為自動雨刷的物料清單騰出了空間;此外,聯邦政府為促進電子元件本地化而提供的獎勵,也推動了馬瑙斯附近一家感測器外殼成型企業的成立。

亞太地區是一個複雜的區域。中國的新車評估計畫將從2027年起評估自動視覺性管理技術,將刺激其製造地(該基地年產能已達2,500萬輛)的出貨量。在印度和部分東協國家,進口電子產品的課稅推高了成本。儘管如此,隨著電動車的普及,降雨感應器再次變得重要起來:出口到泰國和印尼的售價低於1.5萬美元的中國製造微型電動汽車配備了基本的電容式感測器,以便於適應右舵駕駛。因此,亞太地區既是成長最快的地區,也是競爭最分散的地區。

北美地區的普及速度較為穩定,而非迅猛,但較高的平均交易價格促使主流皮卡和SUV安裝了複雜的感測器融合套件。空中升級的普及催生了預測性擋風玻璃維護的訂閱模式,這種模式產生的持續收入緩解了硬體的商品化趨勢。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 隨著ADAS(先進駕駛輔助系統)的普及,多功能環境感測器(雨量、光線、霧)變得至關重要。

- 電氣化和高壓車載架構將加速固態光學雨量感測器的普及應用。

- 推動自動雨刷系統相關法規的製定

- 消費者對中型車舒適性和便利性功能的需求日益成長

- 擋風玻璃抬頭顯示器(HUD)模組整合需要清潔度感測(未經充分通報)

- 透過汽車的空中升級,基於訂閱的雨刷自動化功能將創造新的收入(未充分報告)。

- 市場限制

- 入門級A/B級車對價格的高度敏感度將限制印度和東協地區的感測器安裝率。

- 汽車級光電二極體和垂直腔面發射雷射短缺

- 擋風玻璃設計上的不一致會使光學耦合變得複雜,並增加檢驗成本(未充分報告)。

- 軟體定義的雨量偵測可望與僅使用攝影機的ADAS系統競爭(儘管其覆蓋範圍較小)。

- 價值鏈/供應鏈分析

- 監管環境

- 技術展望

- 波特五力模型

- 新進入者的威脅

- 買方/消費者的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 按車輛類型

- 搭乘用車

- 掀背車

- 轎車

- SUV 與跨界車

- 商用車輛

- 輕型商用車(LCV)

- 中型和重型商用車輛

- 搭乘用車

- 透過技術

- 光學(CCD/CMOS)

- 紅外線反射

- 基於電容/MEMS的

- 按銷售管道

- OEM安裝

- 售後改裝

- 透過使用

- 自動雨刷控制

- 整合式雨量、光照和濕度感測器

- ADAS感測器融合模組

- 按地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 亞太其他地區

- 中東和非洲

- 土耳其

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 其他中東和非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- HELLA GmbH & Co. KGaA

- Valeo SA

- DENSO Corporation

- ZF Friedrichshafen AG

- Robert Bosch GmbH

- STMicroelectronics NV

- Analog Devices Inc.

- ams-OSRAM AG

- onsemi

- Hamamatsu Photonics KK

- Sensata Technologies Inc.

- Melexis NV

- Texas Instruments Inc.

- Panasonic Holdings Corp.

第7章 市場機會與未來展望

The automotive rain sensor market currently stands at USD 5.66 billion in 2025 and is predicted to reach roughly USD 7.63 billion by 2030, reflecting a 6.15% CAGR.

Steady electrification, rising Level 2+ driver-assistance adoption, and regulatory momentum continue to shift rain sensors from comfort add-ons to safety-critical perception inputs. ADAS feature bundling, semiconductor miniaturization, and subscription-ready software stacks are enlarging the addressable base, while cost-down MEMS innovation is broadening access for volume segments. Increased supplier competition from chip makers is also compressing hardware margins but accelerating functional upgrades through integrated optical, capacitive, and humidity modules. Collectively, these forces sustain a multi-year transformation trajectory for the automotive rain sensor market as OEMs reshape vehicle electrical architectures around centralized, over-the-air-update-capable domains.

Global Automotive Rain Sensor Market Trends and Insights

Rising ADAS Penetration Mandates Multi-Function Environmental Sensing

Level 2+ and Level 3 perception stacks require precise raindrop, light, and fog data to keep camera lenses and LiDAR windows clear, recasting the sensor from a comfort extra into a core safety enabler. European OEM programs pair optical rain sensors with humidity and light channels on a single PCB for reduced harness weight and unified diagnostics. Chinese brands replicate the architecture to meet forthcoming NCAP visibility scoring, while North American truck makers embed rain detection in forward-vision clusters to extend automatic emergency braking uptime. High-resolution CCD arrays improve droplet classification, feeding fusion software that modulates wiper speed, adaptive headlights, and defogger logic in one control loop. Consequently, procurement teams now benchmark performance against radar-camera synergy metrics rather than wiper latency alone, making multi-sensor wins pivotal to Tier 1 revenue pipelines.

Electrification & Higher Onboard Voltage Architectures Accelerate Adoption

E-platforms working at 400 V and 800 V offer stable power headroom for signal-processing ASICs and laser-trimmed VCSEL emitters that outperform 12 V counterparts under high-humidity transients. Centralized compute domains pull raw droplet vectors over secure CAN-FD links into zone controllers where machine-learning models refine wipe timing, extending blade life, and trimming HVAC load. Over-the-air firmware releases let OEMs iteratively sharpen detection thresholds, opening pay-per-use revenue tiers tied to predictive maintenance alerts. Battery-electric brands, therefore, market rain sensors as energy-management assets, reducing window-defog cycles by up to 6%, rather than passive glass accessories.

High Price Sensitivity in Entry-Level A/B-Segment Cars

Cost-led platforms in India, parts of ASEAN, and Latin America allocate less than USD 75 for the entire instrument-panel electronics stack, leaving marginal headroom for a USD 25-30 rain-sensing module. Domestic content rules in India amplify import tariffs on unlocalized PCBAs, compressing Tier 1 profitability and slowing take rates. OEMs resort to manual-variable-intermittent wipers in sub-4-m vehicles until integrated MEMS pricing drops below USD 15. Suppliers that secure local glass-bonding partnerships can shave freight surcharges, but low-volume orders currently deter such CAPEX outlays.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Push for Automatic Wiper Systems

- Rising Consumer Demand for Comfort & Convenience Features

- Shortage of Automotive-Grade Photodiodes & VCSELs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The automotive rain sensor market size for passenger cars captured 71.23% share in 2024, and is expected to lead at a robust 6.55% CAGR through 2030. Sedan programs maintain consistent attach rates across trim lines, yet hatchbacks remain price-gated to upper variants. Fleets of light commercial vans now specify automatic wiping to minimize driver distraction and insurance claims, though medium trucks lag because of retrofit complexities. Demand alignment shows that every 10-point uptick in SUV mix raises system-average BOM ceiling by USD 4, supporting margin retention for Tier 1s. Over the forecast period, SUVs' larger windshield area drives higher droplet-noise in capacitive arrays, sustaining OEM preference for optical architectures that maintain +-2 ml sensitivity accuracy in heavy downpours.

Passenger-car refresh cycles grant slower but steadier volume accrual compared with high-churn small commercial fleets. Fleet operators investigating telematics report 7% lower windshield repair claims once predictive wipe analytics are activated, strengthening business cases. Overall, SUV proliferation ensures the automotive rain sensor market remains skewed toward feature-rich packages, balancing the lower margins of high-volume hatchbacks.

Optical CCD/CMOS devices controlled 81.64% of 2024 revenue owing to proven signal-to-noise fidelity. With the top five optical controller ASICs already at silicon-revision B or later, cost curves flatten, giving MEMS entrants a price-to-performance opening. Capacitive / MEMS-based devices will clock an 8.83% CAGR as they sidestep glass-coupling tolerances, ideal for vehicles using advanced UV-blocking laminated windshields. Infrared-reflective hybrids capture niche programs needing anti-icing credibility below -25 °C, albeit at higher per-unit cost.

Strategy roadmaps show MEMS suppliers bundling ambient-light sensors and IR proximity in shared die space, trimming PCB footprint by 35%. Conversely, optical incumbents shield volumes by embedding AI-edge inference cores, enabling self-calibrating droplet recognition that sustains specification leadership. Coexistence rather than displacement defines the horizon: optical retains premium and severe-duty niches; MEMS drives democratization.

The Automotive Rain Sensors Market Report is Segmented by Vehicle Type (Passenger Cars [Hatchback, Sedan, and More] and Commercial Vehicles (Light Commercial Vehicle (LCV) and More), Technology (Optical (CCD/CMOS) and More), Sales Channel (OEM-Installed and Aftermarket Retrofit), Application (ADAS Sensor Fusion Modules, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Geography Analysis

Europe's 37.84% share reflects strict UNECE visibility norms and 2025 NCAP scoring that awards two safety points for rain-light-humidity fusion, cementing sensor fitment as an entitlement across B-segment hatchbacks upward. The continent's established premium mix also ensures high-margin optical arrays dominate. South America, led by Brazil's volume OEM hubs in Sao Paulo, is the fastest climber with a 10.33% CAGR. Consumer upgrades from entry to compact SUVs introduce room in the BOM for automated wiping, while federal incentives to localize electronic content spur sensor-housing molding ventures near Manaus.

Asia-Pacific delivers nuanced dynamics. China's New Car Evaluation Program will credit automated visibility management starting in 2027, anchoring stable shipments within a manufacturing base already scaling 25 million vehicles yearly. Hindrances lie in India and parts of ASEAN, where taxation on imported electronics inflates cost. Nonetheless, EV push grants rain sensors renewed relevance: Chinese-built sub-USD 15,000 micro-EVs that export to Thailand and Indonesia include basic capacitive sensors to ease right-hand-drive adaptation. Hence, Asia-Pacific remains both the largest growth reservoir and the most fragmented battlefield.

North America's uptake is steady rather than spectacular, yet high average transaction prices allow complex sensor-fusion packages on mainstream pickups and SUVs. Over-the-air update culture seeds subscription models for predictive windshield maintenance, producing recurring revenues that temper hardware commoditization.

- HELLA GmbH & Co. KGaA

- Valeo SA

- DENSO Corporation

- ZF Friedrichshafen AG

- Robert Bosch GmbH

- STMicroelectronics N.V.

- Analog Devices Inc.

- ams-OSRAM AG

- onsemi

- Hamamatsu Photonics K.K.

- Sensata Technologies Inc.

- Melexis NV

- Texas Instruments Inc.

- Panasonic Holdings Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising ADAS penetration mandates multi-function environmental sensing (rain, light, fog)

- 4.2.2 Electrification & higher onboard voltage architectures accelerate adoption of solid-state optical rain sensors

- 4.2.3 Regulatory push for automatic wiper systems

- 4.2.4 Rising consumer demand for comfort & convenience features across mid-segment vehicles

- 4.2.5 Integration of windshield head-up-display (HUD) modules requires cleanliness sensing (under-reported)

- 4.2.6 Automotive over-the-air updates unlock new revenue via subscription-based wiper automation (under-reported)

- 4.3 Market Restraints

- 4.3.1 High price sensitivity in entry-level A/B-segment cars limits sensor attach-rates in India & ASEAN

- 4.3.2 Shortage of automotive-grade photodiodes & VCSELs

- 4.3.3 Windshield design heterogeneity complicates optical coupling & raises validation cost (under-reported)

- 4.3.4 Competition from camera-only ADAS stacks promising software-defined rain detection (under-reported)

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Vehicle Type

- 5.1.1 Passenger Cars

- 5.1.1.1 Hatchback

- 5.1.1.2 Sedan

- 5.1.1.3 SUVs and crossovers

- 5.1.2 Commercial Vehicles

- 5.1.2.1 Light Commercial Vehicle (LCV)

- 5.1.2.2 Medium and Heavy Commercial Vehicle

- 5.1.1 Passenger Cars

- 5.2 By Technology

- 5.2.1 Optical (CCD/CMOS)

- 5.2.2 Infra-red Reflective

- 5.2.3 Capacitive / MEMS-based

- 5.3 By Sales Channel

- 5.3.1 OEM-Installed

- 5.3.2 Aftermarket Retrofit

- 5.4 By Application

- 5.4.1 Automatic Wiper Control

- 5.4.2 Integrated Rain-Light-Humidity Sensing

- 5.4.3 ADAS Sensor Fusion Modules

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Italy

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Turkey

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 United Arab Emirates

- 5.5.5.4 South Africa

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 HELLA GmbH & Co. KGaA

- 6.4.2 Valeo SA

- 6.4.3 DENSO Corporation

- 6.4.4 ZF Friedrichshafen AG

- 6.4.5 Robert Bosch GmbH

- 6.4.6 STMicroelectronics N.V.

- 6.4.7 Analog Devices Inc.

- 6.4.8 ams-OSRAM AG

- 6.4.9 onsemi

- 6.4.10 Hamamatsu Photonics K.K.

- 6.4.11 Sensata Technologies Inc.

- 6.4.12 Melexis NV

- 6.4.13 Texas Instruments Inc.

- 6.4.14 Panasonic Holdings Corp.

7 Market Opportunities & Future Outlook

- 7.1 Demand surge for combined rain-fog-light sensor modules to support L3 autonomy

- 7.2 Growth of subscription-based "feature-on-demand" wiper services post-2026

- 7.3 Localisation of sensor assembly in India, Brazil & Indonesia to bypass import duties

- 7.4 Development of hydrophobic nano-coated windshields reducing sensor calibration cycles

汽車降雨感應器市場:2026-2032年全球市場預測(按感測器類型、車輛類型、材料、技術、應用和銷售管道)

汽車降雨感應器市場:2026-2032年全球市場預測(按感測器類型、車輛類型、材料、技術、應用和銷售管道) 汽車雨量感測器市場分析及預測(至2035年):類型、產品、技術、組件、應用、功能、安裝方式、設備、解決方案

汽車雨量感測器市場分析及預測(至2035年):類型、產品、技術、組件、應用、功能、安裝方式、設備、解決方案 汽車降雨感應器全球市場規模、佔有率、趨勢和成長分析報告(2026-2034)

汽車降雨感應器全球市場規模、佔有率、趨勢和成長分析報告(2026-2034) 汽車降雨感應器市場-全球產業規模、佔有率、趨勢、機會和預測:按車輛類型、銷售管道、地區和競爭格局分類,2021-2031年

汽車降雨感應器市場-全球產業規模、佔有率、趨勢、機會和預測:按車輛類型、銷售管道、地區和競爭格局分類,2021-2031年 汽車降雨感應器市場規模、佔有率和成長分析(按靈敏度、工作模式、銷售管道、車輛類型和地區分類)-2026-2033年產業預測

汽車降雨感應器市場規模、佔有率和成長分析(按靈敏度、工作模式、銷售管道、車輛類型和地區分類)-2026-2033年產業預測 2032年汽車降雨感應器市場預測:按車型、銷售管道、技術、應用和地區分類的全球分析汽車降雨感應器市場 - 預測至 2025-2030 年

2032年汽車降雨感應器市場預測:按車型、銷售管道、技術、應用和地區分類的全球分析汽車降雨感應器市場 - 預測至 2025-2030 年 汽車雨量感知器市場,按車型、銷售管道和地區分類 - 2024-2032年行業分析、市場規模、市場佔有率和預測

汽車雨量感知器市場,按車型、銷售管道和地區分類 - 2024-2032年行業分析、市場規模、市場佔有率和預測 全球汽車降雨感應器市場(2024-2028)

全球汽車降雨感應器市場(2024-2028) 汽車雨滴感知器市場:2024-2031年全球產業分析、規模、佔有率、成長、趨勢、預測

汽車雨滴感知器市場:2024-2031年全球產業分析、規模、佔有率、成長、趨勢、預測