|

市場調查報告書

商品編碼

1850048

醫療資產管理:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)Healthcare Asset Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

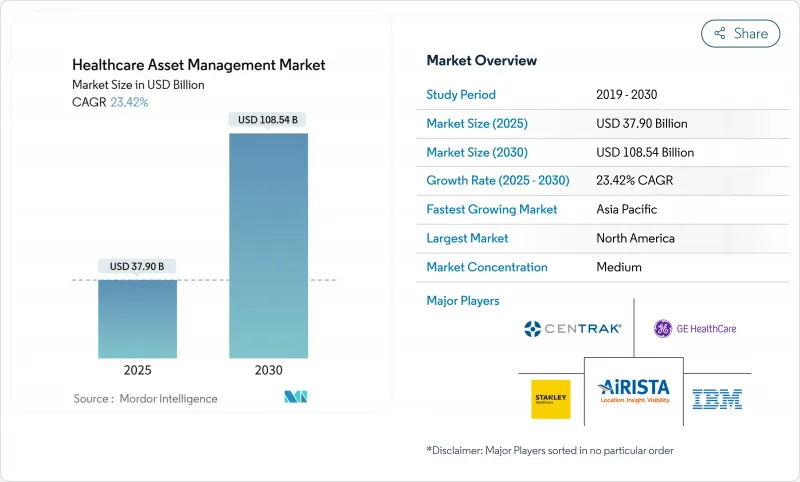

預計 2025 年醫療資產管理市場規模為 379 億美元,到 2030 年將達到 1,085.4 億美元,預測期內(2025-2030 年)的複合年成長率為 23.42%。

這一成長軌跡反映出監管要求、勞動力短缺和網路安全預期如何匯聚在一起,將資產追蹤從成本控制工具重新定位為數位醫療營運的策略支柱。醫院不僅轉向條碼庫存管理,還轉向互聯平台,以簡化對 FDA 2024 年設備安全指南的合規性。需求也與護理人員的限制直接相關。臨床容量的萎縮正在擴大系統的價值,這些系統使護理人員無需再尋找設備,而可以專注於患者的結果。同時,嵌入在標籤中的預測分析正在將維護從被動維護轉變為預測維護,從而減少停機時間並延長資產壽命。這些因素共同創造了一種醫療資產管理市場環境,在這種環境中,醫院、製藥廠和實驗室將綜合可視性、網路安全和分析視為必備功能,而不是可選的附加元件。

全球醫療資產管理市場趨勢與洞察

RFID 防偽需求不斷成長

據估計,假藥每年對全球經濟造成 2,000 億美元的損失,這促使監管機構實施序列化和譜係要求,使得端到端可視性至關重要。根據美國《藥品供應鏈安全法》,藥品製造商、批發商和配藥藥局必須在每個交貨點驗證產品來源。目前,大多數此類部署都採用經過加密認證的 RFID,將單品級識別與溫度敏感型生技藥品所需的即時環境監測相結合。雖然 2024 年起的半導體短缺導致標籤價格上漲高達 20%,但該公司仍在投資,因為違規罰款和召回成本遠遠超過硬體支出。 SATO 等供應商正在推出耐滅菌標籤,可在單一流程步驟中同時提供身分驗證和工作流程效率。這些因素支持製藥和生物技術製造客戶預計從 2025 年到 2030 年的複合年成長率達到 26.8%。

護理人員短缺導致效率提升壓力

由於大型都市區醫院的護理空缺率超過15%,護理團隊捉襟見肘,管理人員也面臨著盡可能從支援技術提高效率的壓力。研究表明,護士每班次有超過五分之一的時間用於尋找丟失的設備。實施即時定位系統 (RTLS) 可將搜尋時間縮短90%以上,無需增加人員即可提供直接勞動力,確保床位已配備到位。英國一家醫療機構已證明,每台設備的使用時間從60分鐘縮短至10分鐘,提高了病患安全評分和員工留任率。先進的部署結合了藍牙低功耗 (BLE) 徽章、緊急按鈕和預測分析,可在臨床醫生發出請求之前將設備放置在病房,從而減輕工作流程負擔並提高滿意度。

資料隱私和網路安全問題

到2024年,醫療資料外洩的平均成本將達到每次977萬美元,安全風險成為快速部署的關鍵阻礙力。 FDA 2024年的指南草案要求加強上市前安全測試,並強制要求採購方在產品上運作前承擔加密、網路分段和持續監控的費用。因此,許多醫院選擇本地部署或隔離網路,限制資料流向雲端,犧牲部分分析能力以降低風險。缺乏安全韌體的舊設備進一步增加了整合的複雜性,延長了計劃工期,並增加了預算。

細分分析

到2024年,RFID將佔總收入的56.2%,這證實了數十年來通訊協定的成熟度和強大的供應鏈使其成為追蹤藥品庫存和手術套件的預設技術。 RFID醫療資產管理市場規模預計到2024年將達到213億美元,顯示該技術已深入滲透到照護現場櫃和中央無菌處理領域。然而,軟體定義的工作流程除了識別之外,越來越需要位置資訊。因此,預計到2030年,利用低功耗藍牙、Wi-Fi和超寬頻的即時定位系統將以28.1%的複合年成長率成長,超過靜態RFID的成長。

隨著供應商將RFID和RTLS整合到多模標籤中,從而彌合被動ID和即時遙測之間的差距,第二階段的成長將會出現。被動RFID可以限制昂貴藥物的損耗,而RTLS則可以確保輸液幫浦在病人病情最嚴重的地方流通。雖然硬體仍然佔據支出的主導地位,標籤、閘道器和激勵器已覆蓋整個院區,但利潤來源正轉向將設備識別、定位和使用情況整合到單一儀表板的平台許可。隨著這種融合的持續,醫療資產管理市場可能會將單模產品視為利基市場。

受數百萬標籤、閱讀器和吸頂式信標持續購買的推動,硬體將在2024年佔據62.4%的收入。然而,隨著醫院從資本支出轉向成果管理,服務將以25.6%的複合年成長率領先。透過訂閱執行時間,供應商可以保證正常運行時間、韌體和監管審核日誌,使IT團隊能夠專注於服務患者。預計到2030年,醫療資產管理市場(即服務)的規模將達到326億美元,這標誌著一個成熟週期的到來:基礎設施將變得無所不在,差異化將轉向諮詢式最佳化。

專業託管服務還能解決一些最具挑戰性的難題,例如變更管理、系統整合和網路安全認證。服務合約通常包含遠端設備健康檢查、演算法更新和合規性文檔,費用在多年期內平均分攤,並與報銷週期保持一致。醫院擴大透過證明每月費用可以透過避免護理人員加班、提高床位周轉率和降低設備租金來抵消,以此來證明其合約的合理性。

醫療資產管理市場按技術(RFID、即時定位系統等)、組件(硬體、軟體、服務)、應用(設備/器械追蹤、庫存/供應鏈管理等)、最終用戶(醫院/診所、實驗室/診斷中心等)和地區細分。市場預測以美元(USD)計算。

區域分析

2024年,北美將佔全球收入的37.8%,這得益於美國全面的序列化法律、成熟的電子病歷(EHR)骨幹網路以及日益增多的醫療設備網路威脅事件,這些事件有利於整合式安全平台的發展。加拿大各省正在採取類似的政策,墨西哥的私立醫院正在投資資產追蹤,以確保醫療遊客的安全並滿足美國保險公司的審核。政府對不安全行為進行懲罰的報銷模式已將可追溯性列為董事會層面的指標,這將進一步推動該地區醫療資產管理市場的採用。

亞太地區是成長最快的地區,預計到2030年複合年成長率將達到22.5%。中國、印度和東南亞的公立醫院建設計畫正在推動待開發區部署,這些項目無需傳統的條碼步驟,從一開始就實現了RFID-RTLS整合。許多此類設施正在將資產管理與國家數位健康雲整合,從而實現整個地區供應鏈的即時藥品認證。隨著資本投資與全民健康覆蓋目標的契合,供應商報告已簽訂涵蓋數百家新醫院的多年期主合約。

受歐盟醫療器材法規 (EU-MDR) 的強制要求、歐洲醫療器材資料管理系統 (EUDAMED)資料庫的推出以及支持生命週期最佳化的國家永續性目標的推動,歐洲的醫療器材採用率正在穩步提升。德國和英國在早期採用方面處於領先地位,但隨著結構性基金優先考慮數位轉型,東歐的資金籌措機制正在迎頭趕上。 GDPR 之後,人們對網路安全的預期推動了對本地部署和混合雲端的需求,而本地資料駐留為平台供應商提供了更豐富的配置選項。由於英國脫歐增加了跨境醫療貿易的海關複雜性,英國的供應商正在優先考慮可追溯性,以避免港口延誤和產品浪費。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概況

- 市場促進因素

- RFID 防偽需求不斷成長

- 護理人員短缺導致效率提升壓力

- 病人安全法規(例如 UDI、EU-MDR)

- 嵌入標籤的基於人工智慧的預測性維護

- 與資產可追溯性掛鉤的績效薪酬

- 市場限制

- 資料隱私和網路安全問題

- RTLS/RFID 基礎設施前期成本高

- 對關鍵無線醫療設備的無線電干擾

- 碎片化的舊式 CMMS 阻礙了整合

- 產業價值鏈分析

- 監管格局

- 技術展望

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 影響市場的宏觀經濟因素

第5章市場規模與成長預測(價值)

- 依技術

- RFID

- 即時定位系統(RTLS)

- 低功耗藍牙 (BLE) 和 Wi-Fi

- 紅外線和超音波

- 按組件

- 硬體(標籤、閱讀器、閘道器)

- 軟體(分析、中介軟體)

- 服務(實施、管理、訓練)

- 按用途

- 設備和裝置追蹤

- 庫存/供應鏈管理

- 患者和工作人員追蹤

- 床位和容量管理

- 環境和狀態監測

- 按最終用戶

- 醫院和診所

- 實驗室和診斷中心

- 製藥和生物技術製造

- 長期照護及療養院

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 智利

- 南美洲其他地區

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 馬來西亞

- 新加坡

- 其他亞太地區

- 中東和非洲

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 埃及

- 其他非洲國家

- 北美洲

第6章 競爭態勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Stanley Healthcare(Stanley Black & Decker)

- CenTrak Inc.

- AiRISTA Flow Inc.

- GE HealthCare Technologies Inc.

- IBM Corporation

- Infor Inc.

- Motorola Solutions Inc.

- Siemens Healthineers AG

- Accenture plc

- Sonitor Technologies AS

- Zebra Technologies Corporation

- Johnson Controls(Tyco International)

- Honeywell International Inc.

- Impinj Inc.

- Alien Technology LLC

- HID Global Corporation

- Ascom Holding AG

- Midmark Corporation(Versus RTLS)

- Trimble Inc.(Atrius)

- Cerner Corporation(Oracle Health)

- TagMaster AB

- Radianse LLC

- Kontakt.io Inc.

- Litum IoT Technologies

- Elpas Ltd.(Securitas)

第7章 市場機會與未來趨勢

- 閒置頻段和未滿足需求評估

The Healthcare Asset Management Market size is estimated at USD 37.90 billion in 2025, and is expected to reach USD 108.54 billion by 2030, at a CAGR of 23.42% during the forecast period (2025-2030).

The growth trajectory reflects how regulatory mandates, workforce shortages, and cybersecurity expectations converge to reposition asset tracking from a cost-containment tool to a strategic pillar of digital health operations. Hospitals are looking beyond bar-code inventory toward connected platforms that streamline compliance with the FDA's 2024 device-security guidance, an obligation that can consume 5% or more of a manufacturer's annual revenue. Demand also ties directly to nursing-staff constraints; shrinking clinical capacity magnifies the value of systems that free caregivers from locating equipment and instead let them focus on patient outcomes. In parallel, predictive analytics embedded in tags move maintenance from reactive to anticipatory, trimming downtime and extending asset life. Taken together, these forces enable a healthcare asset management market environment in which hospitals, pharma plants, and laboratories regard integrated visibility, cybersecurity, and analytics as non-negotiable features rather than optional add-ons.

Global Healthcare Asset Management Market Trends and Insights

Rising demand for RFID to curb drug counterfeiting

Pharmaceutical counterfeiting drains an estimated USD 200 billion from the global economy each year, prompting regulators to impose serialisation and pedigree requirements that make end-to-end visibility indispensable. Under the U.S. Drug Supply Chain Security Act, drug makers, wholesalers, and dispensers must prove product provenance at every hand-off. RFID with cryptographic authentication now underpins most of these deployments because it combines item-level identification with real-time environmental monitoring, a necessity for temperature-sensitive biologics. Semiconductor shortages since 2024 lifted tag prices by up to 20%, yet organisations still invest because non-compliance fines and recall costs far exceed hardware spending. Vendors such as SATO have introduced sterilisation-resistant tags that deliver both authentication and workflow efficiency in one process step. These factors underpin the 26.8% CAGR projected for pharmaceutical and biotech manufacturing customers between 2025 and 2030.

Efficiency pressures from nursing-staff shortages

Nursing vacancy rates above 15% in major urban hospitals leave care teams stretched and force administrators to squeeze every efficiency gain possible from support technology. Studies reveal that nurses spend over one-fifth of each shift searching for missing equipment; RTLS implementations that cut search time by more than 90% therefore provide a direct labour dividend that keeps beds staffed without adding headcount. British facilities have demonstrated time reductions from 60 minutes to 10 minutes per device, translating into heightened patient-safety scores and improved staff retention. Advanced deployments now combine BLE badges, panic buttons, and predictive analytics that stage equipment on units before clinicians request it, easing workflow strain and boosting satisfaction.

Data-privacy and cybersecurity concerns

Average breach costs in healthcare reached USD 9.77 million per incident in 2024, making security risk a material deterrent to rapid roll-outs. The FDA's 2024 draft guidance urges stronger pre-market security testing, compelling buyers to fund encryption, network segmentation, and continuous monitoring before go-live. Many hospitals, therefore, begin with on-premises deployments or air-gapped networks that limit data flow to the cloud, trading some analytics capability for risk reduction. Legacy devices without secure firmware further complicate integrations, extending project timelines and inflating budgets.

Other drivers and restraints analyzed in the detailed report include:

- Patient-safety regulations (UDI, EU-MDR)

- AI-based predictive maintenance embedded in tags

- High upfront RTLS/RFID infrastructure cost

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

RFID accounted for 56.2% of 2024 revenue, underlining decades of protocol maturity and robust supply chains that made the technology the default for drug inventory and surgical kit tracking. The healthcare asset management market size for RFID was USD 21.3 billion in 2024, showing how deeply the modality is entrenched at point-of-care cabinets and central sterile processing. Yet software-defined workflows increasingly require location, not just identity. Real-Time Location Systems leveraging BLE, Wi-Fi, and ultra-wideband are therefore forecast to compound at 28.1% CAGR to 2030, eating into static RFID growth.

A second growth phase emerges as vendors collapse RFID and RTLS into multi-mode tags that pivot between passive ID and real-time telemetry, a design that preserves prior capital investment while enabling richer analytics. Deployments at paediatric-care centres demonstrate this twin-mode value: passive RFID limits shrinkage of high-value drugs, while RTLS ensures infusion pumps circulate where patient acuity is highest. Hardware still dominates spending because tags, gateways, and exciters blanket entire campuses; however, the profit pool is shifting toward platform licences that unite device identity, location, and utilisation into one dashboard. As this convergence proceeds, the healthcare asset management market will likely regard single-mode offerings as a niche.

Hardware captured 62.4% of 2024 sales thanks to ongoing purchases of millions of tags, readers, and ceiling-mounted beacons. Even so, services are pacing ahead with a 25.6% CAGR as hospitals pivot from capital expense toward managed outcomes. Under subscription agreements, vendors guarantee uptime, firmware currency, and regulatory-ready audit logs, freeing IT teams to focus on patient-facing initiatives. The healthcare asset management market size tied to services is forecast to reach USD 32.6 billion by 2030, pointing to a maturation cycle where infrastructure becomes ubiquitous and differentiation shifts to consultative optimisation.

Professional and managed services also address the hardest obstacles-change management, systems integration, and cybersecurity accreditation-that no amount of shelf hardware alone can solve. Service contracts typically bundle remote device health checks, algorithm updates, and compliance documentation generation, costs that spread evenly across multi-year terms and match reimbursement cycles. Hospitals increasingly justify deals by showing that avoided nursing overtime, faster bed turnover, and reduced device rentals offset monthly subscription fees.

Healthcare Asset Management Market is Segmented by Technology (RFID, Real-Time Location Systems, and More), Component (Hardware, Software, and Services), Application (Equipment and Device Tracking, Inventory/Supply-Chain Management, and More), End-User (Hospitals and Clinics, Laboratories and Diagnostic Centers, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America held 37.8% of 2024 revenue, sustained by the United States' comprehensive serialisation law, a mature EHR backbone, and rising incidents of medical device cyber threats that favour integrated, secure platforms. Canadian provinces are adopting similar policies, while Mexican private-sector hospitals invest in asset tracking to retain medical tourists and satisfy U.S. insurer audits. Government reimbursement models that penalise safety lapses make traceability a board-level metric, further supporting healthcare asset management market adoption across the region.

Asia-Pacific is the fastest-growing area with a 22.5% CAGR expected through 2030. Public-hospital construction programmes in China, India, and Southeast Asia enable greenfield deployments that skip legacy bar-code steps and implement RFID-RTLS convergence from day one. Many of these facilities integrate asset management with national digital-health clouds, allowing real-time drug authentication across regional supply chains. As capital investment aligns with universal health-coverage goals, vendors report multi-year master contracts covering hundreds of new hospitals.

Europe shows steady uptake led by the EU-MDR mandate, EUDAMED database roll-outs, and national sustainability targets that favour lifecycle optimisation. Germany and the United Kingdom drive early deployments, but funding mechanisms in Eastern Europe are catching up as structural funds emphasise digital transformation. Cybersecurity expectations anchored in GDPR elevate demand for on-premises or hybrid clouds with local data residency, nudging platform suppliers to broaden configuration options. With Brexit adding customs complexity for cross-channel medical trade, British providers rely on traceability to avoid port delays and product waste.

- Stanley Healthcare (Stanley Black & Decker)

- CenTrak Inc.

- AiRISTA Flow Inc.

- GE HealthCare Technologies Inc.

- IBM Corporation

- Infor Inc.

- Motorola Solutions Inc.

- Siemens Healthineers AG

- Accenture plc

- Sonitor Technologies AS

- Zebra Technologies Corporation

- Johnson Controls (Tyco International)

- Honeywell International Inc.

- Impinj Inc.

- Alien Technology LLC

- HID Global Corporation

- Ascom Holding AG

- Midmark Corporation (Versus RTLS)

- Trimble Inc. (Atrius)

- Cerner Corporation (Oracle Health)

- TagMaster AB

- Radianse LLC

- Kontakt.io Inc.

- Litum IoT Technologies

- Elpas Ltd. (Securitas)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for RFID to curb drug counterfeiting

- 4.2.2 Efficiency pressures from nursing?staff shortages

- 4.2.3 Patient-safety regulations (e.g., UDI, EU-MDR)

- 4.2.4 AI-based predictive maintenance embedded in tags

- 4.2.5 Pay-for-performance reimbursement tied to asset traceability

- 4.3 Market Restraints

- 4.3.1 Data-privacy and cybersecurity concerns

- 4.3.2 High upfront RTLS/RFID infrastructure cost

- 4.3.3 Radio-interference with critical wireless medical devices

- 4.3.4 Fragmented legacy CMMS slowing integration

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Technology

- 5.1.1 RFID

- 5.1.2 Real-Time Location Systems (RTLS)

- 5.1.3 Bluetooth Low Energy (BLE) and Wi-Fi

- 5.1.4 Infrared and Ultrasound

- 5.2 By Component

- 5.2.1 Hardware (Tags, Readers, Gateways)

- 5.2.2 Software (Analytics, Middleware)

- 5.2.3 Services (Deployment, Managed, Training)

- 5.3 By Application

- 5.3.1 Equipment and Device Tracking

- 5.3.2 Inventory/Supply-Chain Management

- 5.3.3 Patient and Staff Tracking

- 5.3.4 Bed and Capacity Management

- 5.3.5 Environmental and Condition Monitoring

- 5.4 By End-user

- 5.4.1 Hospitals and Clinics

- 5.4.2 Laboratories and Diagnostic Centers

- 5.4.3 Pharmaceutical and Biotech Manufacturing

- 5.4.4 Long-Term Care and Assisted-Living Facilities

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Malaysia

- 5.5.4.7 Singapore

- 5.5.4.8 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Egypt

- 5.5.5.2.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Stanley Healthcare (Stanley Black & Decker)

- 6.4.2 CenTrak Inc.

- 6.4.3 AiRISTA Flow Inc.

- 6.4.4 GE HealthCare Technologies Inc.

- 6.4.5 IBM Corporation

- 6.4.6 Infor Inc.

- 6.4.7 Motorola Solutions Inc.

- 6.4.8 Siemens Healthineers AG

- 6.4.9 Accenture plc

- 6.4.10 Sonitor Technologies AS

- 6.4.11 Zebra Technologies Corporation

- 6.4.12 Johnson Controls (Tyco International)

- 6.4.13 Honeywell International Inc.

- 6.4.14 Impinj Inc.

- 6.4.15 Alien Technology LLC

- 6.4.16 HID Global Corporation

- 6.4.17 Ascom Holding AG

- 6.4.18 Midmark Corporation (Versus RTLS)

- 6.4.19 Trimble Inc. (Atrius)

- 6.4.20 Cerner Corporation (Oracle Health)

- 6.4.21 TagMaster AB

- 6.4.22 Radianse LLC

- 6.4.23 Kontakt.io Inc.

- 6.4.24 Litum IoT Technologies

- 6.4.25 Elpas Ltd. (Securitas)

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 White-Space and Unmet-Need Assessment

醫療保健領域即時位置資訊系統市場:按技術類型、部署模式、最終用戶和應用分類-2026-2032年全球市場預測醫療資產管理市場:依醫療設備、資訊科技基礎設施、設施管理、藥品和實驗室設備分類-2026-2032年全球預測

醫療保健領域即時位置資訊系統市場:按技術類型、部署模式、最終用戶和應用分類-2026-2032年全球市場預測醫療資產管理市場:依醫療設備、資訊科技基礎設施、設施管理、藥品和實驗室設備分類-2026-2032年全球預測 即時野生動物追蹤市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、設備、部署類型、最終用戶及解決方案分類

即時野生動物追蹤市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、設備、部署類型、最終用戶及解決方案分類 全球醫療保健資產管理市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球醫療保健資產管理市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 醫療保健資產管理市場報告:按產品、應用、最終用戶和地區分類(2026-2034 年)日本醫療資產管理市場:按產品、應用、最終用戶和地區分類,2026-2034年

醫療保健資產管理市場報告:按產品、應用、最終用戶和地區分類(2026-2034 年)日本醫療資產管理市場:按產品、應用、最終用戶和地區分類,2026-2034年 醫療保健資產管理市場規模、佔有率和成長分析(按產品、應用、最終用戶和地區分類)—產業預測(2026-2033 年)即時分析市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察與預測(2024-2032 年)

醫療保健資產管理市場規模、佔有率和成長分析(按產品、應用、最終用戶和地區分類)—產業預測(2026-2033 年)即時分析市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察與預測(2024-2032 年) 醫療保健即時定位系統 (RTLS) 市場規模、佔有率和趨勢分析報告:按組件、技術、應用、最終用途、地區和細分市場預測 (2025-2033)

醫療保健即時定位系統 (RTLS) 市場規模、佔有率和趨勢分析報告:按組件、技術、應用、最終用途、地區和細分市場預測 (2025-2033) 全球醫療保健領域即時定位系統 (RTLS) 市場

全球醫療保健領域即時定位系統 (RTLS) 市場