|

市場調查報告書

商品編碼

1850013

粉末塗料:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030)Powder Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

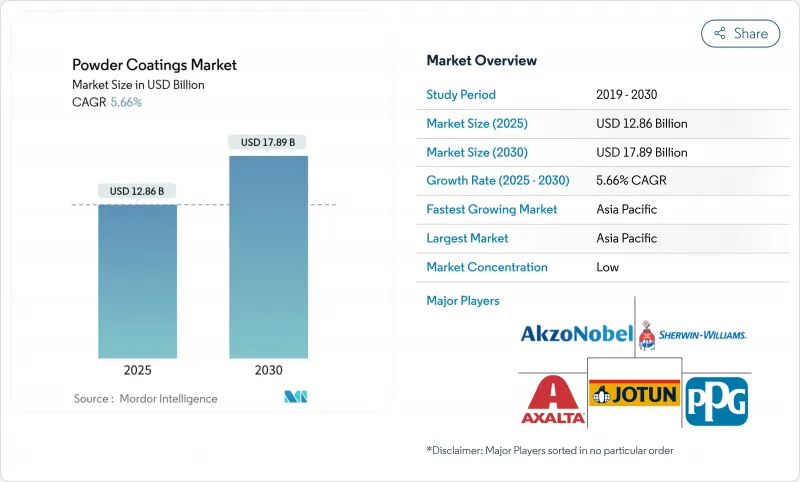

粉末塗料市場規模預計在 2025 年為 128.6 億美元,預計到 2030 年將達到 178.9 億美元,預測期內(2025-2030 年)的複合年成長率為 5.66%。

這項技術的需求正在成長,因為它能夠提供無溶劑、單塗層塗料,符合日益嚴格的揮發性有機化合物 (VOC) 法規,同時最大限度地減少生產廢棄物。亞太地區強勁的工業活動、熱敏基材加速採用低溫化學品以及原始設備製造商 (OEM) 努力實現供應鏈本地化,這些都是支撐粉末塗料市場的大趨勢。聚酯樹脂、低溫烘烤配方和薄膜系統正在設定新的性能標準,拓寬最終用途應用範圍,使其超越傳統的金屬零件。儘管原料波動和超薄薄膜應用限制抑制了市場發展勢頭,但在效率提升和碳減排指令的支撐下,整體上升趨勢仍然穩健。

全球粉末塗料市場趨勢與洞察

嚴格的VOC排放法規改變塗料技術

監管機構認為粉末塗料是污染最低的工業整理加工劑,因為它們幾乎不排放揮發性有機化合物 (VOC),並且省去了昂貴的溶劑回收過程。根據汽車生命週期研究,與液體塗料相比,粉末塗料每輛車可減少 23.40 公斤二氧化碳排放和 1.47 公斤揮發性有機化合物排放,產生可衡量的永續性紅利,與原始設備製造商的脫碳藍圖圖產生共鳴。歐洲綠色新政和更新的美國環保署國家排放標準正在鼓勵塗料製造商加快更換溶劑底漆底漆。領先的配方設計師正在搶在法規收緊之前推出不含 TGIC 和無鉻的產品,以應對未來的禁令。碳定價的上升進一步加強了商業案例,證明與多級液體噴房相比,粉末塗裝線的能耗強度更低。因此,全球粉末塗料塗裝線的裝置容量擴張速度比其他任何技術都快。

低溫化學擴大了應用可能性

最新突破使得在低於120°C的溫度下即可完全固化,從而能夠使用傳統工藝流程下容易翹曲的中密度纖維板、塑膠和複合材料。在248°F下運行的先進系統可為組裝家具、相框和裝飾面板提供低光澤、耐刮擦的飾面。亞太地區家具產業受益匪淺,無需使用多種無VOC塗層即可獲得鮮豔的色彩。由於靜電噴塗粉末可以回收和再利用過噴材料,並提高一次通過率,生產線操作員也實現了兩位數的材料節省。當爐溫設定值降低導致能源需求下降時,實際回報迅速。全球供應商不斷改進樹脂化學成分,以縮短固化時間,提高傳送帶速度並提升日產量。

薄膜應用挑戰限制市場滲透

25µm 超光滑薄膜難以均勻塗覆,尤其是在尖角和凹槽周圍。隨著塗層品質的減少,抗刮性和不透明度也會下降,這使得薄膜粉末對需要完美表面的高階電子產品機殼的吸引力降低。雖然施用器正在適應更嚴格的製程視窗和線上塗層測厚儀,但在複雜幾何形狀下仍存在差異。對於智慧型手機和筆記型電腦,霧化塗層可以輕鬆達到 10µm 且不會出現橘皮現象,因此液體塗層替代品仍能保持市場佔有率。設備維修,例如先進的電暈槍和流化料斗,增加了資本支出,減緩了小型加工商的採用。儘管如此,供應商正在設計更細的粒徑分佈和專有的流動劑來縮小差距。

細分分析

到2024年,聚酯組合物將佔據粉末塗料市場佔有率的38%,主導建築、家電和汽車內裝線市場。預計複合年成長率為6.25%,這意味著聚酯在粉末塗料市場中的佔有率反映了該樹脂的耐候性和豐富的色彩選擇。不含TGIC和低溫固化交聯劑的改良符合《生態設計指令》,而顏料的進步即使在沿海氣候條件下也能保持光澤。隨著聚酯共混物中加入功能性奈米顆粒,在不影響固化速度的情況下改善去污性能,粉末塗料市場將繼續受益。

環氧粉末憑藉其優異的耐化學性,在開關設備和管道閥門等嚴苛的室內環境中佔據著重要的地位。然而,它們易受紫外線照射,限制了其在戶外的應用,與聚酯樹脂相比,銷售量有所下降。環氧-聚酯混合材料可有效緩解粉化現象,提升其在家用電器中的貨架吸引力,並推動亞洲新興生產中心的需求成長。聚氨酯粉末開闢了一個高階市場,其優異的耐化學性和耐磨性使其更高的成本物有所值。科思創的低溫固化技術為複合材料車輪和碳纖維部件開闢了應用前景。丙烯酸、聚氯乙烯和聚烯解決方案可滿足特殊需求,例如防塗鴉運輸面板和洗碗機架,展現了支持樹脂多樣化成長的廣泛選擇。

到2024年,熱固性粉末塗料將佔據90%的市場佔有率,這得益於其不可逆交聯網路結構,能夠抵抗紫外線、化學物質和磨損。熱塑性塑膠在汽車車輪、管道和建築建築幕牆佔有重要地位,憑藉高產量和規模優勢,確保了其成本領先地位。然而,熱塑性塑膠正處於上升期,複合年成長率高達6.01%,因為加工商重視其可重熔和可修復的表面特性,而這些特性在重型機械和購物車框架中尤為重要,因為在這些應用中,柔韌且抗衝擊的表面至關重要。

技術創新是這項轉變的核心。 IFS Puroplaz PE16 展示了改性聚烯如何在保持延展性的同時實現類似鋼材的黏合力,從而拓展了熱塑性塑膠在裝飾圍欄和遊樂場設備製造中的應用範圍。同樣,尼龍基粉末可用於支撐海上緊固件中厚實的抗碎裂薄膜。改良的阻燃配方使熱塑性塑膠與電氣機殼相容,從而減少了傳統熱固性材料的佔有率。雖然熱塑性塑膠需要高溫熔體流動,因此需要較高的固化能量,但對感應加熱和紅外線面板的深入研究旨在在 2025 年至 2030 年期間的部署中彌補這一差距。

區域分析

到2024年,亞太地區將佔全球粉末塗料需求的55%,到2030年,複合年成長率將達到5.89%,占同期粉末塗料市場規模成長的一半以上。中國建設業的復甦、印度資本財生產的加速以及東協白色家電組裝的激增都將推動該地區的粉末塗料消費。阿克蘇諾貝爾的瓜廖爾工廠計劃於2024年9月運作,年產量為5,166噸,顯示市場對國內需求的持續信心。

北美受益於回流政策。美國環保署(EPA)嚴格的揮發性有機化合物(VOC)限值正在推動工廠升級,墨西哥組裝現在也指定使用粉末來製造底盤支架和輪轂,以滿足《美墨加協定》(USMCA)的含量規定。區域負責人指出,由於粉末可以在當地進行大量生產,因此無需高溶劑實驗室的安全控制,配色週期更快。

歐洲成熟的設備基礎更注重技術創新而非產量。歐盟將於2025年對亞洲進口環氧樹脂徵收臨時反傾銷稅,這將保護歐盟生產商免受價格波動的影響,並穩定國內粉末製造商的原料利潤。永續性的挑戰正在推動生物基樹脂和可再生能源固化系統的研發,確保其繼續保持低碳領先地位。

受NEOM、杜哈地鐵延長線和阿拉伯聯合大公國物流區等價值10億美元的大型計劃的推動,中東和非洲粉末塗料市場正在顯著成長。 Al Taiseer Aluminum在沿岸地區擠壓精加工市場佔有21%的佔有率,這清楚地表明了該地區的龍頭企業正在如何塑造規範標準。拉丁美洲的絕對規模仍然較小,但巴西和阿根廷的汽車投資逐漸推動消費,尤其是聚酯面漆的消費。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場狀況

- 市場概況

- 市場促進因素

- 嚴格的VOC排放法規和脫碳法規加速無溶劑塗料

- 低溫燒成化學為中密度纖維板和熱敏基板開闢了商機,尤其是在亞洲

- 外商直接投資推動東協和印度家電產量激增

- 隨著汽車生產回歸墨西哥和歐洲,OEM 需求增加

- 海灣合作理事會大型基礎設施計劃推動建築鋁擠壓塗布的發展

- 市場限制

- 粉末塗料稀釋困難

- 紫外光固化粉末對複雜形狀的適應性有限

- 聚酯和環氧樹脂原料價格波動正在擠壓利潤空間

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章市場規模及成長預測(價值)

- 依樹脂類型

- 環氧樹脂

- 聚酯纖維

- 環氧聚酯

- 聚氨酯

- 丙烯酸纖維

- 其他樹脂種類(聚氯乙烯、聚烯)

- 按塗層類型

- 熱固性粉末塗料

- 熱塑性粉末塗料

- 按最終用途行業

- 建築和裝飾

- 車

- 產業

- 其他(家具、家電等)

- 按基材

- 金屬

- 中密度纖維板和木材

- 塑膠和複合材料

- 玻璃及其他非導電基板

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 法國

- 英國

- 義大利

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭態勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Advanced Powder Coatings

- Akzo Nobel NV

- Asian Paints PPG Pvt. Ltd.

- Axalta Coating Systems, LLC

- BASF

- Berger Paints India

- Cardinal

- Hempel A/S

- IFS Coatings

- IGP Pulvertechnik AG

- Jotun

- Kansai Paint Co.,Ltd.

- NATIONAL PAINTS FACTORIES CO. LTD.

- Nippon Paint Holdings Co., Ltd.

- PPG Industries, Inc.

- RPM International Inc.(TCI Powder Coatings)

- SAK Coat

- Teknos Group

- The Sherwin-Williams Company

- TIGER Coatings GmbH & Co. KG

第7章 市場機會與未來展望

The Powder Coatings Market size is estimated at USD 12.86 billion in 2025, and is expected to reach USD 17.89 billion by 2030, at a CAGR of 5.66% during the forecast period (2025-2030).

Demand is rising as the technology offers solvent-free, single-coat finishes that comply with tightening VOC rules while minimizing production waste. Strong industrial activity across Asia-Pacific, accelerating adoption of low-temperature chemistries for heat-sensitive substrates, and OEM efforts to localize supply chains are broad trends sustaining the powder coatings market. Polyester resins, low-bake formulations, and thin-film systems are setting new performance benchmarks that widen end-use scope beyond traditional metal parts. Although raw-material volatility and application limits on very thin films temper momentum, the overall trajectory remains firmly upward, supported by efficiency gains and carbon-reduction mandates.

Global Powder Coatings Market Trends and Insights

Stringent VOC-Emission Regulations Transforming Coating Technologies

Regulatory agencies now view powder coatings as the lowest-polluting industrial finish because the process emits negligible VOCs and eliminates costly solvent recovery steps. Automotive life-cycle studies show powder conversion cuts 23.40 kg CO2 and 1.47 kg VOCs per vehicle versus liquid paint, creating a measurable sustainability dividend that resonates with OEM decarbonization roadmaps. Europe's Green Deal and the United States EPA's updated National Emission Standards are pushing coaters to accelerate replacement of solventborne primers. Leading formulators have pre-empted tighter limits by launching TGIC-free and chrome-free chemistries that anticipate future bans. Rising carbon-pricing schemes further strengthen the business case, as powder lines demonstrate lower energy intensity than multi-stage liquid booths. As a result, global installed capacity for powder coatings market finishing lines is expanding faster than for any other technology.

Low-Bake Chemistries Expanding Application Possibilities

Recent breakthroughs allow full cure below 120°C, unlocking MDF, plastics, and composites that once warped under conventional schedules. Pioneering systems processed at 248°F enable low-gloss, scratch-resistant finishes on assembled furniture, picture frames, and decorative panels. The Asia-Pacific furniture cluster is the immediate beneficiary, as producers gain a VOC-free route to vibrant colors without multiple topcoats. Line operators also record double-digit material savings because an electrostatically applied powder recovers overspray for reuse, improving first-pass transfer. Practical payback occurs quickly when energy demand falls, given the lower oven set-points. Global suppliers continue to refine resin chemistry to shorten curing time, letting conveyor speeds rise and daily throughput climb.

Thin Film Application Challenges Limiting Market Penetration

Ultra-smooth, 25 µm films remain difficult to deposit uniformly, especially on sharp edges and recessed cavities. Reduced coating mass can lower scratch resistance and opacity, making thin-film powders less attractive for premium electronics housings that demand flawless surfaces. Applicators compensate with tighter process windows and in-line thickness gauges, yet variability persists on intricate geometries. Liquid alternatives keep share in smartphones and laptops because atomized paints easily hit 10 µm without orange peel. Equipment retrofits-such as advanced corona guns and fluidized hoppers-raise capital outlays, slowing adoption among small job shops. Nonetheless, suppliers are engineering finer grind distributions and proprietary flow agents to close the gap.

Other drivers and restraints analyzed in the detailed report include:

- Domestic Appliance Manufacturing Surge in Asia

- Automotive Production Reshoring Driving Regional Demand

- UV-Curable Powder Limitations Constraining Growth

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polyester compositions account for 38% of the powder coatings market share in 2024, giving the group an unrivaled footprint across architectural, appliance, and automotive trim lines. Their 6.25% CAGR forecast means the polyester portion of the powder coatings market reflects the resin's weather fastness and wide color palette. Reformulation to TGIC-free and low-bake cross-linkers aligns with eco-design directives, while pigmentation advances retain gloss even in coastal climates. The powder coatings market continues to benefit as polyester blends incorporate functional nanoparticles that improve stain release without compromising cure speed.

Epoxy powder retains a strategic position in heavy-duty indoor settings such as switchgear and pipe valves because of superior chemical resistance. Yet UV fragility limits outdoor exposure, capping volume growth versus polyester. Epoxy-polyester hybrids mitigate chalking and expand shelf appeal for home appliances, driving incremental demand in emerging Asian production hubs. Polyurethane powders carve out premium niches where chemical and abrasion resistance justify added cost; Covestro's low-temperature cures open composite wheels and carbon fiber parts to this chemistry. Acrylic, PVC, and polyolefin solutions address specialized requirements such as anti-graffiti transit panels or dishwasher racks, illustrating the breadth of options sustaining resin-diversified growth.

Thermoset grades dominated 90% of the powder coatings market in 2024, thanks to irreversible cross-linked networks that withstand UV, chemicals, and abrasion. Their entrenched position in automotive wheels, pipelines, and building facades keeps volume high, and production scale ensures cost leadership. However, thermoplastics are trending upward at 6.01% CAGR as processors value the ability to remelt or repair surfaces, a feature prized in heavy machinery and shopping-cart frames. Over the forecast horizon, the thermoplastic slice of the powder coatings market size may double, particularly where flexible, impact-resistant skins are essential.

Innovation is central to this shift. IFS Puroplaz PE16 demonstrates how modified polyolefins achieve steel-like adhesion while preserving ductility, broadening thermoplastic reach into decorative fencing and playground structures. Similarly, nylon-based powders support thick, chip-resistant films on offshore fasteners. Improved flame-retardant formulations make thermoplastics compatible with electrical enclosures, eroding legacy thermoset share. While curing energy remains higher because thermoplastics require melt flow at elevated temperatures, intensified research on inductive heating and infrared panels aims to narrow that gap during 2025-2030 deployments.

The Powder Coatings Market Report Segments the Industry by Resin Type (Epoxy, Polyester, and More), Coating Type (Thermoset Powder Coatings and Thermoplastic Powder Coatings), End-Use Industry (Architecture and Decorative, Automotive, and More), Substrate (Metal, Plastics and Composites, and More), and Geography (Asia Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific retained 55% of global demand in 2024 and is on track for a 5.89% CAGR to 2030, translating into more than one-half of incremental powder coatings market size growth over the period. China's construction rebound, India's accelerating capital goods output, and ASEAN's surge in white-goods assembly all feed regional consumption. Multinationals continue to add local capacity; AkzoNobel's Gwalior plant brought 5,166 t/y online in September 2024, signaling sustained confidence in domestic appetite.

North America benefits from reshoring policies. The United States Environmental Protection Agency's strict VOC cap catalyzes plant upgrades, and Mexico's assembly corridor now specifies powder on chassis brackets and wheel rims to meet USMCA content rules. Regional formulators highlight faster color-match turnaround because powders can be batched locally without high-solvent lab safety controls.

Europe's mature installation base focuses on innovation rather than volume. The provisional anti-dumping duty on Asian epoxy resin imports adopted in 2025 shields EU producers from price swings, stabilizing raw-material margins for domestic powder makers. Sustainability agendas spur R&D into bio-based resins and renewable-energy-powered cure systems, ensuring continued low-carbon leadership.

The Middle East and Africa powder coatings market sees pronounced upside from billion-dollar megaprojects such as NEOM, Doha Metro extensions, and UAE logistics zones. Al Taiseer Aluminium commands 21% of the Gulf extrusion finishing segment, underscoring how regional champions shape specification norms. Latin America remains smaller in absolute terms, yet automotive investments in Brazil and Argentina gradually lift consumption, particularly of polyester topcoats.

- Advanced Powder Coatings

- Akzo Nobel N.V.

- Asian Paints PPG Pvt. Ltd.

- Axalta Coating Systems, LLC

- BASF

- Berger Paints India

- Cardinal

- Hempel A/S

- IFS Coatings

- IGP Pulvertechnik AG

- Jotun

- Kansai Paint Co.,Ltd.

- NATIONAL PAINTS FACTORIES CO. LTD.

- Nippon Paint Holdings Co., Ltd.

- PPG Industries, Inc.

- RPM International Inc. (TCI Powder Coatings)

- SAK Coat

- Teknos Group

- The Sherwin-Williams Company

- TIGER Coatings GmbH & Co. KG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stringent VOC-emission and decarbonization regulations accelerating solvent-free coatings

- 4.2.2 Low-bake chemistries opening MDF and heat-sensitive substrate opportunities, especially in Asia

- 4.2.3 Surging domestic appliance output in ASEAN and India backed by FDI inflows

- 4.2.4 Re-shoring of automotive production in Mexico and Europe boosting OEM demand

- 4.2.5 GCC infrastructure megaprojects driving architectural aluminium extrusion coatings

- 4.3 Market Restraints

- 4.3.1 Difficulty in Obtaining Thin Film of Powder Coating

- 4.3.2 Limited UV-curable powder compatibility with complex geometries

- 4.3.3 Volatile polyester and epoxy feedstock pricing eroding margins

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value )

- 5.1 By Resin Type

- 5.1.1 Epoxy

- 5.1.2 Polyester

- 5.1.3 Epoxy-Polyester

- 5.1.4 Polyurethane

- 5.1.5 Acrylic

- 5.1.6 Other Resin Types (Polyvinyl Chloride, Polyolefins)

- 5.2 By Coating Type

- 5.2.1 Thermoset Powder Coatings

- 5.2.2 Thermoplastic Powder Coatings

- 5.3 By End-use Industry

- 5.3.1 Architecture and Decorative

- 5.3.2 Automotive

- 5.3.3 Industrial

- 5.3.4 Others (Furniture, Appliances, etc.)

- 5.4 By Substrate

- 5.4.1 Metal

- 5.4.2 MDF and Wood

- 5.4.3 Plastics and Composites

- 5.4.4 Glass and Other Non-conductive Substrates

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 France

- 5.5.3.3 United Kingdom

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Advanced Powder Coatings

- 6.4.2 Akzo Nobel N.V.

- 6.4.3 Asian Paints PPG Pvt. Ltd.

- 6.4.4 Axalta Coating Systems, LLC

- 6.4.5 BASF

- 6.4.6 Berger Paints India

- 6.4.7 Cardinal

- 6.4.8 Hempel A/S

- 6.4.9 IFS Coatings

- 6.4.10 IGP Pulvertechnik AG

- 6.4.11 Jotun

- 6.4.12 Kansai Paint Co.,Ltd.

- 6.4.13 NATIONAL PAINTS FACTORIES CO. LTD.

- 6.4.14 Nippon Paint Holdings Co., Ltd.

- 6.4.15 PPG Industries, Inc.

- 6.4.16 RPM International Inc. (TCI Powder Coatings)

- 6.4.17 SAK Coat

- 6.4.18 Teknos Group

- 6.4.19 The Sherwin-Williams Company

- 6.4.20 TIGER Coatings GmbH & Co. KG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

粉末塗料市場:樹脂類型、技術、固化溫度、基材類型、塗層類型、應用、最終用途-2026-2032年全球市場預測低溫粉末塗料市場:依樹脂類型、化合物類型、設備類型、表面處理類型、應用和最終用戶產業分類-2026-2032年全球市場預測抗菌粉末塗料市場:2026-2032年全球市場預測(按技術、抗菌劑類型、固化方法、配方類型、最終用途行業、應用和分銷管道分類)

粉末塗料市場:樹脂類型、技術、固化溫度、基材類型、塗層類型、應用、最終用途-2026-2032年全球市場預測低溫粉末塗料市場:依樹脂類型、化合物類型、設備類型、表面處理類型、應用和最終用戶產業分類-2026-2032年全球市場預測抗菌粉末塗料市場:2026-2032年全球市場預測(按技術、抗菌劑類型、固化方法、配方類型、最終用途行業、應用和分銷管道分類) 粉末塗料市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並提供2026-2034年的洞察和預測糖果塗層系統市場:按塗層材料、設備類型、應用和最終用途產業分類-全球預測,2026-2032年全球低溫粉末塗料市場規模、佔有率、趨勢及成長分析報告(2026-2034)

粉末塗料市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並提供2026-2034年的洞察和預測糖果塗層系統市場:按塗層材料、設備類型、應用和最終用途產業分類-全球預測,2026-2032年全球低溫粉末塗料市場規模、佔有率、趨勢及成長分析報告(2026-2034) 浸塗系統市場規模、佔有率和成長分析:按浸塗類型、塗料、終端用戶產業和地區分類-2026-2033年產業預測全球抗菌粉末塗料市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球粉末塗料市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

浸塗系統市場規模、佔有率和成長分析:按浸塗類型、塗料、終端用戶產業和地區分類-2026-2033年產業預測全球抗菌粉末塗料市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球粉末塗料市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 日本粉末塗料市場:規模、佔有率、趨勢和預測:按樹脂類型、塗裝方法、應用和地區分類,2026-2034年

日本粉末塗料市場:規模、佔有率、趨勢和預測:按樹脂類型、塗裝方法、應用和地區分類,2026-2034年