|

市場調查報告書

商品編碼

1850008

智慧製造:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)Smart Manufacturing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

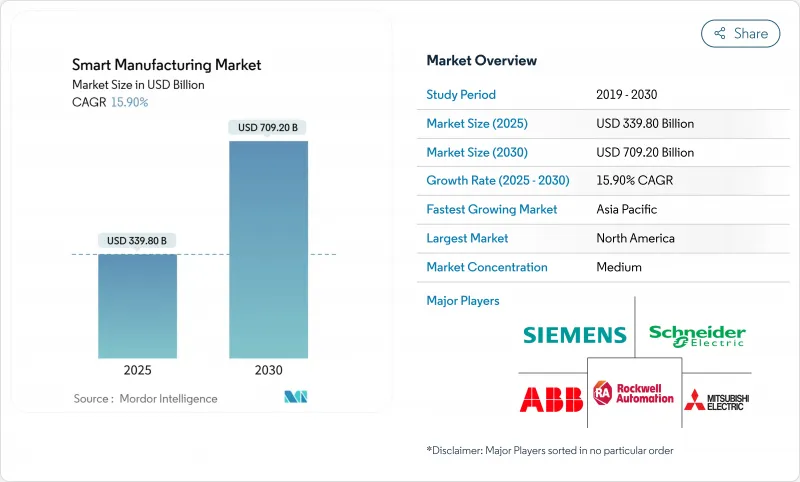

預計到 2025 年,智慧製造市場規模將達到 3,398 億美元,到 2030 年將成長至 7,092 億美元,年複合成長率為 15.90%。

即時分析、機器互聯和人工智慧驅動的製程控制正在融合,從而顯著提高效率;同時,各國政府也紛紛推出激勵措施,以增強國內製造業的韌性。能源成本上漲和碳定價推動了對工廠級透明化解決方案的需求,而勞動力短缺則刺激了對協作機器人和自主物料輸送系統的需求。供應商正在將私有5G和邊緣分析技術融入新產品中,以實現安全關鍵流程的微秒響應速度。競爭格局也從硬體更新周期轉向軟體訂閱模式,後者透過預測性洞察和能源最佳化來實現獲利。

全球智慧製造市場趨勢與洞察

工業4.0/工業物聯網的日益普及可提高效率

工業物聯網 (IIoT) 的應用目前可帶來 52% 的生產效率提升和 25% 的成本節約,這得益於工廠對感測器、分析和雲端儀錶板的整合。美國製造業拓展夥伴計畫(美國 Manufacturing Extension Partnership )透過其智慧製造項目,已幫助 36,000 家公司在 2024 年前實現 162 億美元的銷售額成長。互聯資產的數據匯入整合資料湖,使營運商能夠消除生產線停機並動態調整產能。航太等對精度要求極高的行業正在積極採用數位化可追溯性來減少廢品和保固索賠,從而推動其連接架構的持續升級。

政府對數位化工廠的獎勵和政策要求

聯邦和州政府層級的資助計畫正透過有針對性的財政支持和法律規範,加速智慧製造的普及應用。例如,州製造業領導計畫(Manufacturing Leadership Program)向中小型製造商提供5000萬美元,透過提供高效能運算資源和技術援助來提升其製造能力。同時,德國的工業4.0舉措(由為中小企業提供技術應用指導的「中小企業4.0卓越中心」支持)預計到2020年每年將投資400億歐元。

中小企業面臨高資本支出和不確定的投資報酬率

由於前期投資和投資回報期的不確定性,中小企業在採用智慧製造技術方面面臨著許多障礙。實施一套完整的智慧製造系統的成本可能從數十萬美元到數百萬美元不等,這給資源有限的企業帶來了沉重的財務負擔。互聯系統的投資報酬率計算複雜,使得中小企業決策者難以證明投資的合理性,尤其是在收益可能需要兩到三年才能顯現的情況下。

細分市場分析

2024年,製造執行系統(MES)將佔據智慧製造市場22.4%的佔有率,凸顯其作為工廠營運數位化支柱的重要地位。隨著製造商要求實現全球工廠的即時可視性,預計到2032年,MES智慧製造市場規模將達到417.8億美元。數位雙胞胎平台正以18.7%的複合年成長率快速成長,使工程師能夠模擬設備在各種負載下的運作情況,進而將試運行時間縮短30%。雖然PLC和SCADA仍然至關重要,但供應商正在整合人工智慧模組以實現參數的自主調整。邊緣分析軟體縮短了高速包裝線上的決策週期,標誌著資料中心正從集中式伺服器轉變為現場微型資料中心。

軟體定義升級能夠帶來穩定的年度經常性收入,促使現有企業將分析功能捆綁到授權續約中。人機介面工具正朝著擴增實境發展,為第一線技術人員提供引導式工作流程。產品生命週期管理解決方案與供應鏈入口網站整合,使設計人員能夠儘早檢驗產品的可製造性。這些技術創新鞏固了智慧製造市場作為持續改善投資關鍵管道的地位。

到2024年,軟體收入將佔總收入的49.6%,反映出工作流程正向數據主導型轉變。工業機器人預計將以17.5%的複合年成長率成長,有助於解決長期存在的勞動力短缺問題以及靈活批量生產的需求。控制設備現在整合了設備端推理引擎,無需雲端延遲即可實現自主調整。隨著工廠將整合、培訓和網路安全管理等業務外包,服務收入也將成長。

私有5G網路將再形成通訊領域,在單層樓內支援數萬個終端,並實現確定性延遲。供應商將與通訊業者共同製定頻譜策略,將連接性轉化為戰略護城河。因此,智慧製造市場將繼續模糊OT硬體和IT軟體之間的界限,從而創建一個用於創造數位價值的整合平台。

區域分析

2024年,北美將佔全球銷售額的42.3%,這得益於美國能源局提供的3300萬美元津貼計劃以及製造拓展夥伴計劃(Manufacturing Extension Partnership)在全國範圍內的推廣。創業投資正在加速技術應用,私募股權基金則致力於推出整合製造執行系統(MES)、機器人整合和保全服務的平台。區域供應商正在採用私有的5G測試平台來檢驗對延遲敏感的應用場景,例如遠端焊接。

亞太地區是成長最快的地區,複合年成長率達15.9%。其中,中國在「中國製造2025」的旗幟下設立了33個研發中心,韓國則以每萬名員工1,012台機器人的全球領先機器人密度位居世界前列。在三方合作夥伴的支持下,印度的「數位基礎設施成長計畫」正在降低新興企業的進入門檻,並將印度定位為製造執行系統(MES)發展領域的新興力量。

在歐洲,智慧製造正穩步普及,這主要得益於德國的工業4.0戰略,該戰略預計每年投資400億歐元(約合440億美元),並由德國的「中小企業4.0能力中心」推動。碳邊境調節機制進一步提升了對能源強度儀錶板的需求,並使歐洲供應商在碳計量模組方面擁有先發優勢。總而言之,這些動態共同增強了智慧製造市場的區域專業實力,並影響供應商的市場進入策略。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 工業4.0/工業物聯網的日益普及提高了效率

- 政府對數位化工廠的獎勵和政策要求

- 技術純熟勞工短缺將加速自動化技術的普及應用。

- 碳邊境調節機制(CBAM)促進工廠層級的能源透明度

- 基於數位雙胞胎的預測性維護服務收入

- 部署可實現超低延遲控制的專用 5G 網路

- 市場限制

- 中小企業資本投入高,投資報酬率不確定性

- 網路安全/資料主權問題

- 傳統類比設備限制了互通性

- 半導體供應鏈的不穩定性導致控制硬體交付延遲。

- 價值/供應鏈分析

- 監管環境

- 五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 投資分析

第5章 市場規模與成長預測

- 透過技術

- 可程式邏輯控制器(PLC)

- 監控與數據採集(SCADA)

- 企業資源規劃(ERP)

- 分散式控制系統(DCS)

- 人機介面(HMI)

- 產品生命週期管理(PLM)

- 製造執行系統(MES)

- 數位雙胞胎平台

- 邊緣分析軟體

- 其他技術

- 按組件

- 硬體

- 機器人技術

- 感應器

- 機器視覺系統

- 控制裝置

- 軟體

- MES

- PLM

- SCADA/ERP套件

- 數位雙胞胎/人工智慧和分析

- 服務

- 整合與實施

- 諮詢和培訓

- 託管服務

- 通訊部門

- 硬體

- 透過部署模式

- 本地部署

- 雲

- 混合

- 按最終用戶行業分類

- 車

- 半導體和電子學

- 石油和天然氣

- 化工和石油化工

- 製藥和生命科學

- 航太與國防

- 食品/飲料

- 金屬和採礦

- 能源與公共產業

- 物流和倉儲

- 其他行業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 智利

- 其他南美洲

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲和紐西蘭

- ASEAN-5

- 亞太其他地區

- 中東和非洲

- 中東

- 非洲

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- ABB Ltd.

- Emerson Electric Co.

- FANUC Corporation

- General Electric Co.

- Honeywell International Inc.

- Mitsubishi Electric Corp.

- Robert Bosch GmbH

- Rockwell Automation Inc.

- Schneider Electric SE

- Siemens AG

- Texas Instruments Inc.

- Yokogawa Electric Corp.

- Cisco Systems Inc.

- IBM Corp.

- Oracle Corp.

- SAP SE

- Johnson Controls Intl. plc

- PTC Inc.

- Dassault Systems SE

- 3D Systems Corp.

- Stratasys Ltd.

- Delta Electronics Inc.

- Capgemini SE

第7章 市場機會與未來展望

The smart manufacturing market size is valued at USD 339.80 billion in 2025 and is projected to climb to USD 709.20 billion by 2030, registering a 15.90% CAGR.

Real-time analytics, machine connectivity, and AI-powered process control are converging to unlock large efficiency gains, while governments channel incentives toward resilient domestic production capacity. Rising energy costs and carbon-pricing schemes heighten interest in factory-level transparency solutions, and labor shortages intensify demand for collaborative robots and autonomous material-handling systems. Vendors are embedding private 5G and edge analytics in new offerings, enabling micro-second response times for safety-critical processes. Competitive focus is shifting from hardware refresh cycles to software subscription models that monetize predictive insights and energy optimization.

Global Smart Manufacturing Market Trends and Insights

Rising adoption of Industry 4.0 / IIoT for efficiency

IIoT deployments now deliver 52% productivity gains and 25% cost reductions as factories integrate sensors, analytics, and cloud dashboards. The U.S. Manufacturing Extension Partnership supported 36,000 firms in 2024, adding USD 16.2 billion in sales through smart manufacturing programs.As connected assets feed unified data lakes, operators can eliminate line stoppages and dynamically rebalance capacity. Precision-critical sectors such as aerospace embrace digital traceability to reduce scrap and warranty claims, fueling sustained upgrades in connectivity architectures.

Government incentives & policy mandates for digital factories

Federal and state-level funding initiatives are accelerating smart manufacturing adoption through targeted financial support and regulatory frameworks. The State Manufacturing Leadership Program offers USD 50 million to enhance manufacturing capacity through high-performance computing resources and technical assistance for small and medium manufacturers.Germany's Industrie 4.0 initiative projects EUR 40 billion annual investment by 2020, supported by Mittelstand 4.0 centers of excellence that provide SMEs with technology adoption guidance.

High CAPEX & uncertain SME ROI

Small and medium enterprises face significant barriers to smart manufacturing adoption due to substantial upfront capital requirements and unclear return on investment timelines. Implementation costs for comprehensive smart manufacturing systems can range from hundreds of thousands to millions of dollars, creating financial strain for companies with limited resources. The complexity of calculating ROI for interconnected systems makes it difficult for SME decision-makers to justify investments, particularly when benefits may not materialize for 2-3 years.

Other drivers and restraints analyzed in the detailed report include:

- Skilled-labour shortages accelerating automation uptake

- Carbon-Border Adjustment Mechanism spurring factory-level energy transparency

- Cyber-security / data-sovereignty concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Manufacturing Execution Systems held 22.4% of the smart manufacturing market in 2024, underscoring their role as the digital backbone of plant operations. The smart manufacturing market size for MES is projected to reach USD 41.78 billion by 2032 as manufacturers mandate real-time visibility across global plants. Digital-twin platforms, expanding at an 18.7% CAGR, let engineers simulate equipment behavior under varying loads, trimming commissioning times by 30% . PLCs and SCADA remain foundational, yet vendors embed AI modules that autonomously tune parameters. Edge-analytics software shortens decision loops for high-speed packaging lines, illustrating the shift from centralized servers to shop-floor micro-data centers.

Software-defined upgrades create sticky annual recurring revenue, prompting incumbents to bundle analytics with license renewals. Human-machine interface tools migrate toward augmented reality, giving line technicians guided workflows. Product lifecycle management solutions integrate with supply-chain portals so designers validate manufacturability early. Collectively, these innovations reinforce the smart manufacturing market as the primary conduit for continuous improvement investments.

Software commanded 49.6% of 2024 revenue, reflecting the pivot toward data-driven workflows. Industrial robotics, projected to post a 17.5% CAGR, responds to chronic labor gaps and the need for flexible batch sizes.Smart sensors and machine-vision units feed high-resolution imagery to AI models that flag defects within milliseconds. Control devices now incorporate on-device inference engines, enabling autonomous adjustments without cloud latency. Service revenues expand as factories outsource integration, training, and managed cybersecurity.

Private 5G networks reshape the communication segment by supporting tens of thousands of end-points on a single floor with deterministic latency. Vendors co-develop spectrum strategies with telecom operators, turning connectivity into a strategic moat. As a result, the smart manufacturing market continues to blur lines between OT hardware and IT software, creating a unified platform for digital value creation.

The Smart Manufacturing Market is Segmented by Technology (Programmable Logic Controller (PLC), Supervisory Controller and Data Acquisition (SCADA), and More), Component (Hardware and More), Deployment Mode (On-Premise, Cloud and More), End-User Industry (Automotive, Semiconductors, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America accounted for 42.3% of 2024 revenue, underpinned by the U.S. Department of Energy's USD 33 million grant program and the Manufacturing Extension Partnership's nationwide outreach . Venture capital flows accelerate technology diffusion, and private equity funds pursue platform roll-ups that bundle MES, robotics integration, and cybersecurity services. Regional suppliers adopt private 5G testbeds to validate latency-sensitive use cases such as remote welding.

Asia Pacific is the fastest-growing region with a 15.9% CAGR, propelled by China's 33 Innovation Centers under the "Made in China 2025" banner and South Korea's world-leading robot density of 1,012 units per 10,000 employees. India's Digital Infrastructure Growth Initiative, backed by trilateral partners, lowers entry barriers for smart manufacturing startups, positioning the country as a rising hub for localized MES development.

Europe delivers steady adoption rooted in Germany's Industrie 4.0, backed by EUR 40 billion (USD 44 billion) annual investment projections and Mittelstand 4.0 competence centers. The Carbon Border Adjustment Mechanism amplifies demand for energy-intensity dashboards, giving European vendors first-mover advantage in carbon accounting modules. Collectively, these dynamics reinforce regional specialization within the smart manufacturing market, shaping vendor go-to-market playbooks.

- ABB Ltd.

- Emerson Electric Co.

- FANUC Corporation

- General Electric Co.

- Honeywell International Inc.

- Mitsubishi Electric Corp.

- Robert Bosch GmbH

- Rockwell Automation Inc.

- Schneider Electric SE

- Siemens AG

- Texas Instruments Inc.

- Yokogawa Electric Corp.

- Cisco Systems Inc.

- IBM Corp.

- Oracle Corp.

- SAP SE

- Johnson Controls Intl. plc

- PTC Inc.

- Dassault Systems SE

- 3D Systems Corp.

- Stratasys Ltd.

- Delta Electronics Inc.

- Capgemini SE

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising adoption of Industry 4.0 / IIoT for efficiency

- 4.2.2 Government incentives and policy mandates for digital factories

- 4.2.3 Skilled-labour shortages accelerating automation uptake

- 4.2.4 Carbon-Border Adjustment Mechanism (CBAM) spurring factory-level energy transparency

- 4.2.5 Digital-twin-based predictive-maintenance service revenues

- 4.2.6 Roll-out of private 5G networks enabling ultra-low-latency control

- 4.3 Market Restraints

- 4.3.1 High CAPEX and uncertain SME ROI

- 4.3.2 Cyber-security / data-sovereignty concerns

- 4.3.3 Legacy analogue equipment limiting interoperability

- 4.3.4 Semiconductor supply-chain volatility delaying control hardware

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porters Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

- 4.7 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Technology

- 5.1.1 Programmable Logic Controller (PLC)

- 5.1.2 Supervisory Control and Data Acquisition (SCADA)

- 5.1.3 Enterprise Resource Planning (ERP)

- 5.1.4 Distributed Control System (DCS)

- 5.1.5 HumanMachine Interface (HMI)

- 5.1.6 Product Lifecycle Management (PLM)

- 5.1.7 Manufacturing Execution System (MES)

- 5.1.8 Digital-Twin Platforms

- 5.1.9 Edge-Analytics Software

- 5.1.10 Other Technologies

- 5.2 By Component

- 5.2.1 Hardware

- 5.2.1.1 Robotics

- 5.2.1.2 Sensors

- 5.2.1.3 Machine-Vision Systems

- 5.2.1.4 Control Devices

- 5.2.2 Software

- 5.2.2.1 MES

- 5.2.2.2 PLM

- 5.2.2.3 SCADA / ERP Suites

- 5.2.2.4 Digital-Twin / AI and Analytics

- 5.2.3 Services

- 5.2.3.1 Integration and Implementation

- 5.2.3.2 Consulting and Training

- 5.2.3.3 Managed Services

- 5.2.4 Communication Segment

- 5.2.1 Hardware

- 5.3 By Deployment Mode

- 5.3.1 On-Premise

- 5.3.2 Cloud

- 5.3.3 Hybrid

- 5.4 By End-user Industry

- 5.4.1 Automotive

- 5.4.2 Semiconductors and Electronics

- 5.4.3 Oil and Gas

- 5.4.4 Chemical and Petrochemical

- 5.4.5 Pharmaceuticals and Life Sciences

- 5.4.6 Aerospace and Defense

- 5.4.7 Food and Beverage

- 5.4.8 Metals and Mining

- 5.4.9 Energy and Utilities

- 5.4.10 Logistics and Warehousing

- 5.4.11 Other Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Netherlands

- 5.5.3.7 Russia

- 5.5.3.8 Rest of Europe

- 5.5.4 APAC

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 ASEAN-5

- 5.5.4.7 Rest of APAC

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.2 Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 ABB Ltd.

- 6.4.2 Emerson Electric Co.

- 6.4.3 FANUC Corporation

- 6.4.4 General Electric Co.

- 6.4.5 Honeywell International Inc.

- 6.4.6 Mitsubishi Electric Corp.

- 6.4.7 Robert Bosch GmbH

- 6.4.8 Rockwell Automation Inc.

- 6.4.9 Schneider Electric SE

- 6.4.10 Siemens AG

- 6.4.11 Texas Instruments Inc.

- 6.4.12 Yokogawa Electric Corp.

- 6.4.13 Cisco Systems Inc.

- 6.4.14 IBM Corp.

- 6.4.15 Oracle Corp.

- 6.4.16 SAP SE

- 6.4.17 Johnson Controls Intl. plc

- 6.4.18 PTC Inc.

- 6.4.19 Dassault Systems SE

- 6.4.20 3D Systems Corp.

- 6.4.21 Stratasys Ltd.

- 6.4.22 Delta Electronics Inc.

- 6.4.23 Capgemini SE

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

智慧製造市場規模、佔有率、趨勢和預測:按組件、技術、最終用途和地區分類,2026-2034 年

智慧製造市場規模、佔有率、趨勢和預測:按組件、技術、最終用途和地區分類,2026-2034 年 智慧製造市場規模、佔有率和趨勢分析報告:按組件、技術、最終用途、地區和細分市場預測(2026-2033 年)

智慧製造市場規模、佔有率和趨勢分析報告:按組件、技術、最終用途、地區和細分市場預測(2026-2033 年) 2026年全球智慧製造市場報告2026年全球雲端製造市場報告

2026年全球智慧製造市場報告2026年全球雲端製造市場報告 智慧製造市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、設備、流程及最終用戶分類智慧製造平台市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶、功能和解決方案分類Dark Factory全球市場報告2026

智慧製造市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、設備、流程及最終用戶分類智慧製造平台市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶、功能和解決方案分類Dark Factory全球市場報告2026 智慧製造市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察與未來預測(2026-2034)

智慧製造市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察與未來預測(2026-2034) 北美智慧製造市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本智慧製造市場報告(按組件、技術、最終用途和地區分類,2026-2034 年)

北美智慧製造市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本智慧製造市場報告(按組件、技術、最終用途和地區分類,2026-2034 年)