|

市場調查報告書

商品編碼

1848306

塑膠添加劑:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)Plastic Additives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

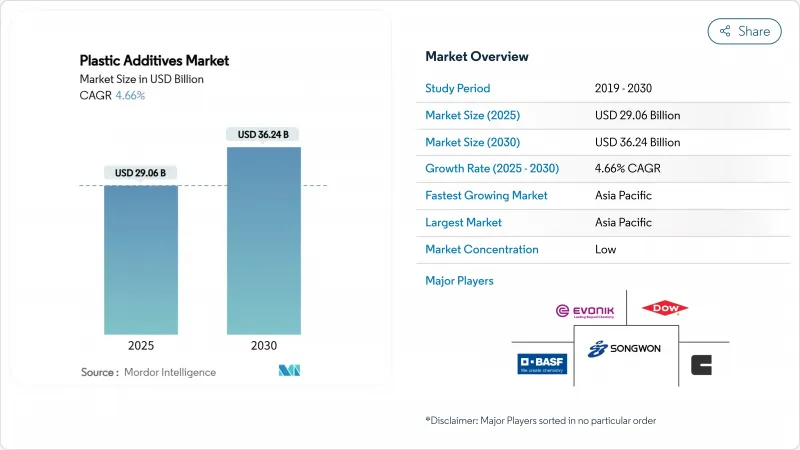

塑膠添加劑市場規模預計在 2025 年為 290.6 億美元,預計到 2030 年將達到 362.4 億美元,預測期內(2025-2030 年)的複合年成長率為 4.66%。

儘管原料價格波動和化學品監管趨嚴,但輕量化電動車 (EV) 零件的強勁需求、亞太地區快速的都市化以及嚴格的全球包裝法規仍在支撐成長。受中國和印度特種化學品生產擴張的推動,亞太地區佔全球銷售額的 54%。加工助劑是成長最快的添加劑類型,受益於向不含 PFAS 化學品的過渡。同時,隨著品牌優先考慮更安全的成分,消費品應用的成長速度超過了所有其他終端用途。BASF和科萊恩計劃在 2024 年前完成 PFAS 的淘汰工作,以領先歐盟和美國的新法規。

全球塑膠添加劑市場趨勢與洞察

轉向輕量化電動車零件

電動車的日益普及推動了對耐熱、耐壓和抗振添加劑的需求。BASF的無鹵化阻燃劑 Ultramid T6000 PPA 可實現更薄更輕的接線端子,進而降低潮濕環境下的腐蝕風險。目前,汽車製造商使用的塑膠約佔平均汽車重量的 15%,而下一代電動車的設計目標將使這一比例達到 25%,從而推動添加劑的使用。沙烏地基礎工業公司的 NORYL GTX LMX310 樹脂等類似創新可將充電埠的碳足跡減少 30%,Avient 的 Hydrocerol發泡可將車門面板的重量減輕 20%。隨著電池組重量的增加,結構部件節省的每一公斤都變得更有價值,這使得電動車成為塑膠添加劑市場的長期催化劑。

替代傳統材料

由於成本和使用壽命的考慮,塑膠正日益取代木材、鋼骨和混凝土在建築領域的應用。BASF穩定劑可延長PVC屋頂板和複合牆板的戶外使用壽命,減少重新塗漆週期和維護成本。電氣機殼領域也發生了類似的轉變,阻燃添加劑使符合IEC標準的聚合物機殼變得更薄。這種材料轉變正在推動塑膠添加劑市場的發展,因為每種新的聚合物應用都需要抗氧化劑、紫外線穩定劑、抗衝改質劑和其他添加劑來匹配先前聚合物的性能。

原物料價格波動

2024-2025年,由於亞洲和拉丁美洲的採礦中斷,有機錫穩定劑和亞磷酸酯抗氧化劑的供應趨緊,錫和磷的價格大幅波動。由於缺乏對沖工具,小型配方商被迫徵收臨時額外費用,這削弱了買家信心,並推遲了合約續約。一些生產商正在重新配製穩定劑,以取代鈣鋅或受阻胺,但直接替代很少能實現無縫銜接。

細分分析

加工助劑是成長最快的類別,預計到2030年複合年成長率將達到4.71%。日益嚴格的PFAS法規正推動加工商轉向新型無氟化學品,例如百爾羅赫的Baerolub AID。 「其他」類別,包括抗氧化劑、阻燃劑和抗衝改質劑,將在2024年佔據塑膠添加劑市場佔有率的70%,這反映了包裝、建築和移動等多樣化的終端用途需求。新型防滑和防霧添加劑正在滿足對再生材料薄膜的需求,進一步擴大其應用範圍。

受大規模包裝和管道需求的推動,聚乙烯將在2024年保持17%的收入佔有率,支撐大宗樹脂塑膠添加劑的市場規模。回收內容要求推動了對相容劑和擴鏈劑的需求,以恢復再生聚乙烯(rPE)流的熔體強度。相較之下,長期以來受回收障礙困擾的聚苯乙烯,由於化學回收技術的突破,將廢聚苯乙烯轉化為乙苯,用於永續航空燃料添加劑,正在復甦。

聚氯乙烯在窗框和電線塗層中應用廣泛,但因其殘留鄰苯二甲酸酯而受到嚴格審查。生物來源聚氯乙烯(PVC) 穩定劑的創新,使生產商能夠擺脫對化石基原料的依賴,並符合綠色建築標籤的要求。

區域分析

預計到2024年,亞太地區將佔全球塑膠添加劑總收入的54%,該地區塑膠添加劑市場規模將以5.23%的複合年成長率持續擴張。中國的石化自力更生獎勵策略和印度放鬆外商投資管制將吸引性能穩定劑和色母粒的新產能,從而確保國內供應鏈的穩定。

北美市場依然成熟且富有創新精神。美國汽車製造商優先發展電動車平台,推動了溫度控管零件對阻燃劑和高流動性添加劑的需求;而加拿大對一次性塑膠的禁令則推動了符合 ASTM D6400 標準的可堆肥母粒的需求。墨西哥受益於近岸外包,吸引了許多擠出機製造商在地採購採購母粒以縮短前置作業時間。這兩個地區都經歷了溫和的成長,但利潤率較高。

歐洲的政策是世界上最嚴格的政策之一。 《包裝和包裝廢棄物法規》規定,塑膠必須在2030年之前實現可回收,並鼓勵加工商透過經認可的實驗室證明添加劑的兼容性。南美洲和中東/非洲的市場規模較小,但具有良好的上升潛力。巴西對生物聚合物的推動與支持澱粉和聚乳酸(PLA)混合物的添加劑一致。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場狀況

- 市場概況

- 市場促進因素

- 電動車輕量化零件的轉變推動了對高性能添加劑的需求

- 塑膠在某些應用中取代了傳統材料

- 快速的都市化和不斷成長的消費者購買力推動了塑膠的需求

- 可堆肥包裝要求推動生物基添加劑母粒的採用

- 醫療保健和食品接觸塑膠中抗菌表面的快速成長

- 市場限制

- 錫、磷等原物料價格波動對利潤率造成壓力

- 歐洲和北美逐步淘汰鄰苯二甲酸酯類塑化劑並縮小其範圍

- 對基於 PFAS 的加工助劑的監管審查限制了其採用

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章市場規模及成長預測

- 按類型

- 潤滑劑

- 加工助劑(含氟氟聚合物基)

- 流動改進劑

- 滑爽添加劑

- 抗靜電添加劑

- 顏料潤濕劑

- 填料分散劑

- 防霧添加劑

- 塑化劑

- 其他類型(發泡、防黏劑、偶聯劑等)

- 按塑膠類型

- 聚乙烯(PE)

- 聚丙烯(PP)

- 聚氯乙烯(PVC)

- 聚苯乙烯(PS)

- 聚對苯二甲酸乙二醇酯(PET)

- 聚碳酸酯(PC)

- 聚醯胺(PA)

- 其他類型的塑膠

- 按形式

- 母粒

- 粉末

- 液體濃縮物

- 按用途

- 包裹

- 消費品

- 建造

- 車

- 其他(醫療、3D列印)

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 北歐國家

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭態勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介{包括全球概況、市場層級、核心細分市場、財務狀況、策略資訊、市場排名/佔有率、產品和服務、最新發展}

- BASF

- ADEKA CORPORATION

- Albemarle Corporation

- Arkema

- Avient Corporation

- Baerlocher GmbH

- Clariant

- Croda International Plc

- Dow

- Emery Oleochemicals

- Evonik Industries AG

- Exxon Mobil Corporation

- KANEKA CORPORATION

- LANXESS

- Mitsui & Co.Plastics Ltd.

- Nouryon

- Peter Greven GmbH & Co. KG

- SABO SpA

- Songwon Industrial Co. Ltd.

- Struktol Company of America, LLC

第7章 市場機會與未來展望

The Plastic Additives Market size is estimated at USD 29.06 billion in 2025, and is expected to reach USD 36.24 billion by 2030, at a CAGR of 4.66% during the forecast period (2025-2030).

Strong demand from lightweight electric-vehicle (EV) components, rapid urbanization in Asia-Pacific, and stringent global packaging rules sustain growth despite feedstock volatility and tightening chemical regulations. Asia-Pacific accounts for 54% of global revenue as China and India scale specialty-chemical output. Processing aids are the fastest-rising additive type, gaining from the move to PFAS-free chemistries, while consumer-goods applications outpace all other end-uses as brands prioritize safer ingredients. Producers are shifting portfolios toward bio-based and PFAS-free grades; BASF and Clariant finished their PFAS exits in 2024 to stay ahead of new EU and U.S. restrictions.

Global Plastic Additives Market Trends and Insights

Shift to Lightweight EV Components

Growing EV adoption is lifting demand for additives that can withstand heat, voltage, and vibration. BASF's non-halogen flame-retardant Ultramid T6000 PPA enables thinner, lighter terminal blocks and reduces corrosion risk in humid environments. Automakers currently use plastic for roughly 15% of average vehicle weight; design targets for next-generation EVs push that ratio toward 25%, magnifying additive volumes. Parallel innovations such as SABIC's NORYL GTX LMX310 resin cut charging-port carbon footprints by 30% while Avient's Hydrocerol foaming agents shave 20% from door-panel mass. As battery packs grow heavier, every kilogram saved in structural parts becomes more valuable, cementing EVs as a long-run catalyst for the plastic additives market.

Replacement of Conventional Materials

Plastics are displacing wood, steel, and concrete in construction owing to cost and longevity. BASF stabilizers extend the outdoor life of PVC roofing sheets and composite siding, reducing repaint cycles and maintenance costs. Similar shifts appear in electrical housings where flame-retardant additives allow thinner polymer casings that meet IEC standards. This material swap boosts the plastic additives market because each new polymer application needs antioxidants, UV stabilizers, and impact modifiers to match incumbent performance.

Volatility in Feedstock Prices

Tin and phosphorous prices swung sharply in 2024-2025 as mining disruptions hit Asia and Latin America, tightening the supply of organotin stabilizers and phosphite antioxidants. Smaller formulators lack hedging tools, forcing ad-hoc surcharges that erode buyer confidence and slow contract renewals. Some producers are redesigning stabilizers around calcium-zinc or hindered amine alternatives, though drop-in replacement is seldom seamless.

Other drivers and restraints analyzed in the detailed report include:

- Mandatory Compostable-Packaging Laws

- Growth of Antimicrobial Surfaces

- Phase-Out of Phthalate Plasticizers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Processing aids represent the fastest-advancing category, forecast at 4.71% CAGR through 2030. Rising PFAS restrictions push converters toward new fluoro-free chemistries like Baerlocher's Baerolub AID, which improves extrusion stability without legacy environmental baggage. The "Others" group, including antioxidants, flame retardants, and impact modifiers, dominated 70% of the plastic additives market share in 2024, reflecting diverse end-use needs across packaging, construction, and mobility. Novel slip and antifog agents fitting demanding recycled-content films further widen the application scope.

Polyethylene sustained a 17% revenue share in 2024, underpinned by large packaging and pipe demand, anchoring the plastic additives market size for commodity resins. Recycled-content mandates amplify needs for compatibilizers and chain extenders that restore melt strength in rPE streams. In contrast, long constrained by recycling hurdles, polystyrene is rebounding on chemical-recycling breakthroughs that turn waste PS into ethylbenzene for sustainable aviation-fuel additives.

Polyvinyl chloride remains entrenched in window profiles and wire coatings yet faces scrutiny over residual phthalates. Innovations in bio-attributed PVC stabilizers allow producers to decouple from fossil-based feedstocks and comply with green-building labels.

The Plastic Additives Market Report Segments the Industry by Type (Lubricants, Processing Aids, Flow Improvers, Slip Additives, and More), Plastic Type (Polyethylene (PE), Polypropylene (PP), Polyvinyl Chloride (PVC), Polystyrene (PS), and More), Form (Masterbatch, Powder, and Liquid Concentrate), Application (Packaging, Consumer Goods, Construction, and More), and Geography (Asia-Pacific, North America, Europe, and More).

Geography Analysis

Asia-Pacific continues to anchor global volume, holding 54% of revenue in 2024 and expanding the region's plastic additives market size at 5.23% CAGR. China's stimulus for petrochemical self-reliance and India's relaxation of foreign-investment ceilings invite fresh capacity in performance stabilizers and color concentrates, securing domestic supply chains.

North America remains a mature but innovative market. U.S. automakers prioritizing EV platforms spur flame-retardant and high-flow additives for thermal-management parts, while Canada's single-use plastics ban boosts demand for compostable masterbatches that meet ASTM D6400 criteria. Mexico benefits from near-shoring, attracting extruders who source masterbatch locally to shorten lead times. The combined region posts modest growth yet commands premium margins.

Europe's policy landscape is the world's most stringent. The Packaging and Packaging Waste Regulation dictates recyclability by 2030, pushing converters to certify additive compliance through accredited labs. South America and the Middle-East and Africa are smaller in value but show healthy upside. Brazil's bio-polymer push aligns with additives that support starch and PLA blends,

- BASF

- ADEKA CORPORATION

- Albemarle Corporation

- Arkema

- Avient Corporation

- Baerlocher GmbH

- Clariant

- Croda International Plc

- Dow

- Emery Oleochemicals

- Evonik Industries AG

- Exxon Mobil Corporation

- KANEKA CORPORATION

- LANXESS

- Mitsui & Co.Plastics Ltd.

- Nouryon

- Peter Greven GmbH & Co. KG

- SABO S.p.A.

- Songwon Industrial Co. Ltd.

- Struktol Company of America, LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Shift to Lightweight EV Components Stimulating High-Performance Additive Demand

- 4.2.2 Replacement of Conventional Materials by Plastic in Several Applications

- 4.2.3 Increasing Demand for Plastic Due to Rapid Urbanization and Rising Purchasing Power Among Consumers

- 4.2.4 Mandatory Compostable-Packaging Laws Accelerating Bio-Based Additive Masterbatches

- 4.2.5 Rapid Growth of Antimicrobial Surfaces in Healthcare and Food-Contact Plastics

- 4.3 Market Restraints

- 4.3.1 Volatility in Tin and Phosphorous Feedstock Prices Compressing Margins

- 4.3.2 Europe nad North America Phase-Out of Phthalate Plasticizers Reducing Addressable Volume

- 4.3.3 Regulatory Scrutiny on PFAS-Based Processing Aids Limiting Adoption

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Lubricants

- 5.1.2 Processing Aids (Fluro-polymer-based)

- 5.1.3 Flow Improvers

- 5.1.4 Slip Additives

- 5.1.5 Antistatic Additives

- 5.1.6 Pigment Wetting Agents

- 5.1.7 Filler Dispersants

- 5.1.8 Antifog Additives

- 5.1.9 Plasticizers

- 5.1.10 Other Types (Blowing Agent, Anti-blocking Agents, Coupling agents, etc.)

- 5.2 By Plastic Type

- 5.2.1 Polyethylene (PE)

- 5.2.2 Polypropylene (PP)

- 5.2.3 Polyvinyl Chloride (PVC)

- 5.2.4 Polystyrene (PS)

- 5.2.5 Polyethylene Terephthalate (PET)

- 5.2.6 Polycarbonate (PC)

- 5.2.7 Polyamides (PA)

- 5.2.8 Other Plastic Types

- 5.3 By Form

- 5.3.1 Masterbatch

- 5.3.2 Powder

- 5.3.3 Liquid Concentrate

- 5.4 By Application

- 5.4.1 Packaging

- 5.4.2 Consumer Goods

- 5.4.3 Construction

- 5.4.4 Automotive

- 5.4.5 Others (Medical, 3D Printing)

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Nordics

- 5.5.3.6 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments}

- 6.4.1 BASF

- 6.4.2 ADEKA CORPORATION

- 6.4.3 Albemarle Corporation

- 6.4.4 Arkema

- 6.4.5 Avient Corporation

- 6.4.6 Baerlocher GmbH

- 6.4.7 Clariant

- 6.4.8 Croda International Plc

- 6.4.9 Dow

- 6.4.10 Emery Oleochemicals

- 6.4.11 Evonik Industries AG

- 6.4.12 Exxon Mobil Corporation

- 6.4.13 KANEKA CORPORATION

- 6.4.14 LANXESS

- 6.4.15 Mitsui & Co.Plastics Ltd.

- 6.4.16 Nouryon

- 6.4.17 Peter Greven GmbH & Co. KG

- 6.4.18 SABO S.p.A.

- 6.4.19 Songwon Industrial Co. Ltd.

- 6.4.20 Struktol Company of America, LLC

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

- 7.2 Rising Research Activities Research to Develop Bio-based Plastics

塑膠添加劑市場分析及預測(至2035年):類型、產品、應用、形態、材料類型、技術、最終用戶、功能、安裝類型

塑膠添加劑市場分析及預測(至2035年):類型、產品、應用、形態、材料類型、技術、最終用戶、功能、安裝類型 塑膠添加劑市場規模、佔有率和成長分析(按塑膠添加劑類型、塑膠類型、形態、應用和地區分類)—2026-2033年產業預測

塑膠添加劑市場規模、佔有率和成長分析(按塑膠添加劑類型、塑膠類型、形態、應用和地區分類)—2026-2033年產業預測 全球塑膠添加劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球塑膠添加劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026年全球塑膠添加劑市場報告

2026年全球塑膠添加劑市場報告 塑膠添加劑市場-全球產業規模、佔有率、趨勢、機會及按類型、最終用途、地區和競爭格局分類的預測(2021-2031年)汽車塑膠添加劑市場-全球產業規模、佔有率、趨勢、機會及預測(按汽車應用、車輛類型、塑膠類型、塑膠添加劑、地區和競爭格局分類,2021-2031年)

塑膠添加劑市場-全球產業規模、佔有率、趨勢、機會及按類型、最終用途、地區和競爭格局分類的預測(2021-2031年)汽車塑膠添加劑市場-全球產業規模、佔有率、趨勢、機會及預測(按汽車應用、車輛類型、塑膠類型、塑膠添加劑、地區和競爭格局分類,2021-2031年) 單體水解穩定劑市場按應用、終端用戶產業、產品類型、通路和技術分類-2026-2032年全球預測水解穩定劑市場:依應用、產品類型、最終用戶、等級、通路和技術分類-2026-2032年全球預測聚合物水解穩定劑市場按類型、載體形式、最終用途產業、應用和化學類型分類-2026-2032年全球預測聚烯回收添加劑市場:依聚合物類型、添加劑類型、產品形式、加工應用和最終用途產業分類,全球預測,2026-2032年

單體水解穩定劑市場按應用、終端用戶產業、產品類型、通路和技術分類-2026-2032年全球預測水解穩定劑市場:依應用、產品類型、最終用戶、等級、通路和技術分類-2026-2032年全球預測聚合物水解穩定劑市場按類型、載體形式、最終用途產業、應用和化學類型分類-2026-2032年全球預測聚烯回收添加劑市場:依聚合物類型、添加劑類型、產品形式、加工應用和最終用途產業分類,全球預測,2026-2032年