|

市場調查報告書

商品編碼

1848035

英國農業機械:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)United Kingdom Agricultural Machinery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

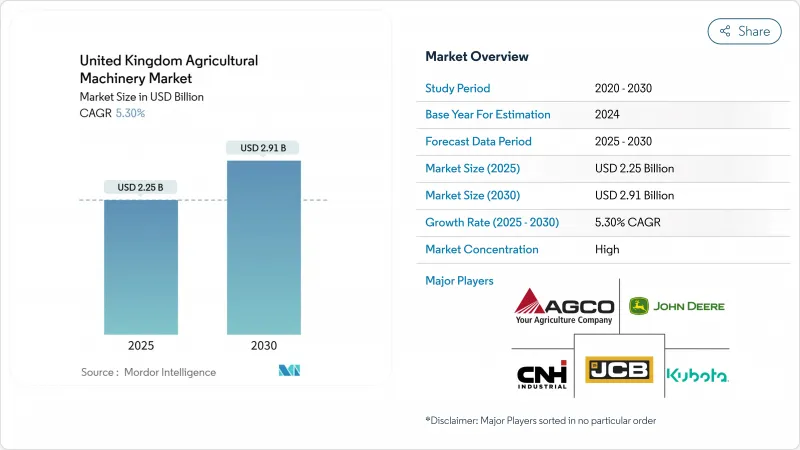

英國農業機械市場預計到 2025 年將達到 22.5 億美元,到 2030 年將達到 29.1 億美元,在預測期內將以 5.3% 的強勁複合年成長率成長。

這一上升趨勢凸顯了該行業在英國脫歐後的限制、持續的勞動力短缺以及農場自動化加速發展等挑戰下的韌性。未來五年,農業設備和技術基金將促進機械採購。該基金是一項5,000萬英鎊(約6,300萬美元)的津貼計劃,可直接抵銷提高生產力機械的購買成本。清潔能源2030行動計畫也將影響需求,對低排放氣體和氫動力曳引機的投資將協助英國在2030年實現淨零排放目標。同時,在智慧機器2035策略的支持下,農業機器人測試基地的擴建正在促進快速原型開發,並吸引各研究叢集之間的技術合作。

英國農業機械市場趨勢與洞察

勞動力短缺加速了機械化進程

英國超過40%的農場報告勞動力短缺,這一數字推動了對可替代人工的自主和半自動機器的資本支出。季節性工人簽證已延長至2029年,惠及4.5萬名工人,同時政府政策也投資5,000萬英鎊(約6,300萬美元)用於自動化,以減少對移民勞工的長期依賴。 Fieldwork Robotics公司的覆盆子採摘系統展示了連續運作和媲美人類的作業效率如何改變商業格局,使機器人技術更具優勢。不斷上漲的勞動成本促使人們對能夠長時間運作且只需少量人工干預的設備提出更高的要求,從而增強了英國農業機械市場的需求。

政府對農業機械的補貼和稅收優惠

農業設備與技術基金將為每位申請者提供1,000至25,000英鎊(1,250至31,250美元)的資助,而提高農場生產力計劃將為機器人和精準系統津貼高達500,000英鎊(625,000美元)的資助。每項津貼項目必須使用五年,從而為設備供應商提供可預測的需求週期。津貼評分框架優先考慮碳減排和動物福利指標,引導採購傾向於配備豐富感測器的農機具、自動導航系統和低壓縮解決方案。這些獎勵將直接促進英國農業機械市場的整體設備周轉率,尤其有利於那些歷來推遲大額投資的中小農。

較高的初始投資和維護成本

英格蘭及威爾斯特許會計師協會指出,儘管現金流良好,大型生產商仍在推遲機械採購,反映出單位成本上升和資金籌措收緊。 AGCO公司2025年第一季營收下降30%,顯示注重成本的買家正在削減資本預算。由於現代聯合收割機和曳引機需要專用診斷軟體、雲端服務訂閱和專業技術人員,維護負擔日益加重。即使有津貼,生命週期成本對許多小型企業來說仍然難以承受,這導致英國農業機械市場擴張的預期下降。

細分市場分析

到2024年,曳引機將佔英國農業機械市場的55.2%。該細分市場的成長仍然與設備更換和馬力升級密切相關,自動駕駛和遠端資訊處理技術的整合將成為標配。在曳引機市場中,100馬力以下的車型佔據了大部分銷量,但馬力更高的車型(150馬力以上)由於其高價和全端式技術,獲得了不成比例的收入佔有率。迪爾公司所佔的多數市佔率凸顯了整合導航、互聯互通和售後服務網路對於降低英國農業機械市場整體擁有成本的重要性。

預計到2030年,灌溉設備將以8.2%的複合年成長率實現最強勁的成長,這直接源自於降雨量的不確定性和日益嚴格的取水許可製度。中心支軸式噴灌系統結合土壤濕度感測器,有助於農場遵守英國環境署的水資源管理指令,而滴灌技術在高價值園藝領域也日益普及。精準灌溉透過減少徑流和投入浪費,協助實現生態再生目標,凸顯了氣候變遷如何推動英國農業機械市場的產品多元化。收割機、牧草設備和耕耘機的需求也保持穩定,但農場日益重視水資源管理才是推動灌溉設備成長的主要動力。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 勞動力短缺加速了機械化進程

- 政府對農業機械的補貼和稅收優惠

- 精密農業數位化需求

- 可再生農業獎勵推動對低壓縮設備的需求

- 擴大農業機器人測試場地將促進原型的應用。

- 淨零排放電氣化政策推動電動曳引機銷售

- 市場限制

- 高昂的初始成本和維修成本

- 互聯機械的網路安全與資料隱私風險

- 由於農村地區電網容量有限,導致電氣設備引進延遲

- 英國脫歐後認證的差距可能會增加合規成本。

- 監管狀態

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭強度

第5章 市場規模與成長預測

- 按機器類型

- 聯結機

- 不到50馬力

- 50-100馬力

- 100-150馬力

- 150馬力或以上

- 裝置

- 犁

- 光環

- 耕耘機和耕耘機

- 其他設備(播種機、滾筒等)

- 灌溉機械

- 噴水灌溉

- 滴灌

- 其他灌溉設備(中心支軸式噴灌系統、微型噴灌等)

- 收割機

- 聯合收割機

- 飼料收割機

- 其他收割機(馬鈴薯收割機、甜菜收割機等)

- 乾草和飼料機械

- 割草機和壓扁機

- 打包機

- 其他乾草飼料機械(耙草機、翻曬機)

- 其他機械

- 聯結機

第6章 競爭情勢

- 市場集中度

- 策略舉措

- 市佔率分析

- 公司簡介

- Deere & Company

- CNH Industrial NV

- AGCO Corporation

- Kubota Corporation

- Claas KGaA mbH

- JC Bamford Excavators Ltd.

- Kuhn Group(Bucher Industries AG)

- SDF Group SpA

- Bernard Krone Holding SE & Co. KG

- Horsch Maschinen GmbH

- Amazone-Werke H. Dreyer SE & Co. KG

- GRIMME Landmaschinenfabrik GmbH & Co. KG

- LEMKEN GmbH & Co. KG

- Vaderstad Group

第7章 市場機會與未來展望

The United Kingdom agricultural machinery market size stands at USD 2.25 billion in 2025 and is projected to advance to USD 2.91 billion by 2030, delivering a steady 5.3% CAGR during the forecast period.

This upward trajectory underscores the sector's resilience amid post-Brexit regulation, persistent labor shortages, and accelerating on-farm automation. Over the next five years, equipment purchases will be buoyed by the Farming Equipment and Technology Fund, a GBP 50 million (USD 63 million) grant program that directly offsets capital costs for productivity-enhancing machinery. Demand is also influenced by the Clean Power 2030 Action Plan, which channels investment toward low-emission electric and hydrogen tractors that help farms meet the national net-zero target for 2030. Meanwhile, the Expansion of agri-robotics testbeds, supported by the Smart Machines Strategy 2035, is fostering rapid prototype adoption and attracting technology partnerships across research clusters.

United Kingdom Agricultural Machinery Market Trends and Insights

Shortage of labor accelerating mechanization

More than 40% of British farms report an insufficient workforce, a figure that has intensified capital outlays toward autonomous and semi-autonomous machinery capable of substituting manual labor. Seasonal-worker visas have been extended to 45,000 positions through 2029, yet government policy is simultaneously investing GBP 50 million (USD 63 million) in automation to reduce long-term reliance on migrant labor. Fieldwork Robotics' raspberry-picking system exemplifies how continuous operation and human-comparable throughput shift return-on-investment calculations in favor of robotics. As labor costs rise, specification requirements move toward equipment that can work longer hours with limited oversight, reinforcing demand across the United Kingdom agricultural machinery market.

Government grant schemes and tax relief on farm machinery

The Farming Equipment and Technology Fund awards between GBP 1,000 and GBP 25,000 (USD 1,250 to USD 31,250) per applicant, while the Improving Farm Productivity program finances up to GBP 500,000 (USD 625,000) for robotics and precision systems. Each funded item must remain in use for five years, providing equipment suppliers with predictable demand cycles. Grant scoring frameworks prioritize carbon reduction and animal welfare metrics, steering purchases toward sensor-rich implements, autonomous guidance, and low-compaction solutions. These incentives directly lift overall equipment turnover within the United Kingdom agricultural machinery market, especially for small and mid-sized farms that historically delayed high-ticket investments.

High upfront and maintenance costs

The Institute of Chartered Accountants in England and Wales notes that large producers are delaying equipment purchases despite healthy cash flows, reflecting rising unit prices and tighter financing. AGCO Corporation's Q1 2025 revenue fell 30%, a signal that cost-sensitive buyers are pruning capital budgets. Maintenance burdens compound the hurdle modern combines and tractors require proprietary diagnostic software, cloud subscriptions, and specialized technicians. Even with grant offsets, many small operations find lifecycle costs prohibitive, trimming projected expansion of the United Kingdom agricultural machinery market.

Other drivers and restraints analyzed in the detailed report include:

- Regenerative-farming incentives driving low-compaction equipment demand

- Net-Zero electrification mandates catalyzing electric tractor purchases

- Cybersecurity and data privacy risks in connected machinery

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Tractors accounted for a 55.2% share of the United Kingdom agricultural machinery market in 2024. Segment expansion remains tethered to replacement cycles and horsepower upgrades, with autonomous and telematics integration becoming default specifications. Within tractors, models under 100 horsepower dominate volume, yet high-horsepower units above 150 horsepower capture disproportionate revenue due to their premium pricing and full-stack technology. Deere & Company's majority share highlights the importance of integrated guidance, connectivity, and after-sales networks that lower the total cost of ownership across the United Kingdom agricultural machinery market.

Irrigation equipment posted an 8.2% CAGR outlook through 2030, the strongest among all categories, and a direct response to unpredictable rainfall and tightening abstraction permits. Pivot systems coupled with soil-moisture sensors help farms align with the Environment Agency's water-management directives, while drip technology gains traction in high-value horticulture. Precision irrigation supports regenerative objectives by reducing runoff and input waste, underscoring how climate volatility drives product diversification within the United Kingdom agricultural machinery market size framework. Harvesters, forage machinery, and tillage implements also report steady demand, but their growth trails irrigation as water stewardship rises on farm agendas.

The United Kingdom Agricultural Machinery Market Report is Segmented by Machinery Type (Tractor, Equipment, Irrigation Machinery, Harvesting Machinery, Haying and Forage Machinery, and Other Machinery Types). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Deere & Company

- CNH Industrial N.V.

- AGCO Corporation

- Kubota Corporation

- Claas KGaA mbH

- J.C. Bamford Excavators Ltd.

- Kuhn Group (Bucher Industries AG)

- SDF Group S.p.A.

- Bernard Krone Holding SE & Co. KG

- Horsch Maschinen GmbH

- Amazone-Werke H. Dreyer SE & Co. KG

- GRIMME Landmaschinenfabrik GmbH & Co. KG

- LEMKEN GmbH & Co. KG

- Vaderstad Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Shortage of labor accelerating mechanization

- 4.2.2 Government grant schemes and tax relief on farm machinery

- 4.2.3 Demand for precision agriculture and digitalization

- 4.2.4 Regenerative-farming incentives driving low-compaction equipment demand

- 4.2.5 Expansion of agri-robotics testbeds boosting prototype uptake

- 4.2.6 Net-Zero electrification mandates catalyzing electric tractor purchases

- 4.3 Market Restraints

- 4.3.1 High upfront and maintenance costs

- 4.3.2 Cybersecurity and data privacy risks in connected machinery

- 4.3.3 Rural grid-capacity limits slowing electric-equipment adoption

- 4.3.4 Post-Brexit certification divergence escalating compliance costs

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Machinery Type

- 5.1.1 Tractor

- 5.1.1.1 Less than 50 HP

- 5.1.1.2 50 to 100 HP

- 5.1.1.3 100 to 150 HP

- 5.1.1.4 Above 150 HP

- 5.1.2 Equipment

- 5.1.2.1 Plows

- 5.1.2.2 Harrows

- 5.1.2.3 Cultivators and Tillers

- 5.1.2.4 Other Equipment (Seed Drills, Rollers, etc.)

- 5.1.3 Irrigation Machinery

- 5.1.3.1 Sprinkler Irrigation

- 5.1.3.2 Drip Irrigation

- 5.1.3.3 Other Irrigation Machinery (Center Pivot Systems, Micro Sprinklers, etc.)

- 5.1.4 Harvesting Machinery

- 5.1.4.1 Combine Harvesters

- 5.1.4.2 Forage Harvesters

- 5.1.4.3 Other Harvesting Machinery (Potato Harvesters, Beet Harvesters, etc.)

- 5.1.5 Haying and Forage Machinery

- 5.1.5.1 Mowers and Conditioners

- 5.1.5.2 Balers

- 5.1.5.3 Other Haying and Forage Machinery (Rakes, Tedders)

- 5.1.6 Other Machinery Types

- 5.1.1 Tractor

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Deere & Company

- 6.4.2 CNH Industrial N.V.

- 6.4.3 AGCO Corporation

- 6.4.4 Kubota Corporation

- 6.4.5 Claas KGaA mbH

- 6.4.6 J.C. Bamford Excavators Ltd.

- 6.4.7 Kuhn Group (Bucher Industries AG)

- 6.4.8 SDF Group S.p.A.

- 6.4.9 Bernard Krone Holding SE & Co. KG

- 6.4.10 Horsch Maschinen GmbH

- 6.4.11 Amazone-Werke H. Dreyer SE & Co. KG

- 6.4.12 GRIMME Landmaschinenfabrik GmbH & Co. KG

- 6.4.13 LEMKEN GmbH & Co. KG

- 6.4.14 Vaderstad Group

7 Market Opportunities and Future Outlook

農業和施工機械市場:按產品類型、功率範圍、引擎類型、應用、最終用戶和分銷管道分類——2026-2032年全球預測穀物螺旋輸送機市場:按類型、動力來源、容量、應用、最終用戶和分銷管道分類-2026-2032年全球預測紅外線瀝青加熱器市場:按產品類型、電源、移動性、應用、最終用戶、分銷管道分類,全球預測(2026-2032年)堆高機升降臂市場:按類型、容量、應用和最終用戶分類,全球預測,2026-2032年挖土機底盤零件市場:按產品類型、應用、分銷管道和最終用途分類,全球預測,2026-2032年重型設備底盤零件市場:按零件類型、設備類型、銷售管道、最終用途產業和材料分類,全球預測,2026-2032年

農業和施工機械市場:按產品類型、功率範圍、引擎類型、應用、最終用戶和分銷管道分類——2026-2032年全球預測穀物螺旋輸送機市場:按類型、動力來源、容量、應用、最終用戶和分銷管道分類-2026-2032年全球預測紅外線瀝青加熱器市場:按產品類型、電源、移動性、應用、最終用戶、分銷管道分類,全球預測(2026-2032年)堆高機升降臂市場:按類型、容量、應用和最終用戶分類,全球預測,2026-2032年挖土機底盤零件市場:按產品類型、應用、分銷管道和最終用途分類,全球預測,2026-2032年重型設備底盤零件市場:按零件類型、設備類型、銷售管道、最終用途產業和材料分類,全球預測,2026-2032年 農業機械市場規模、佔有率和成長分析(按動力、傳動系統、功能、推進、設備類型和地區分類)-2026-2033年產業預測

農業機械市場規模、佔有率和成長分析(按動力、傳動系統、功能、推進、設備類型和地區分類)-2026-2033年產業預測 2026-2030年全球農業機械市場

2026-2030年全球農業機械市場 美國農業機械:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)越南農業機械:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

美國農業機械:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)越南農業機械:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)