|

市場調查報告書

商品編碼

1846269

覆膜標籤:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)Laminated Labels - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

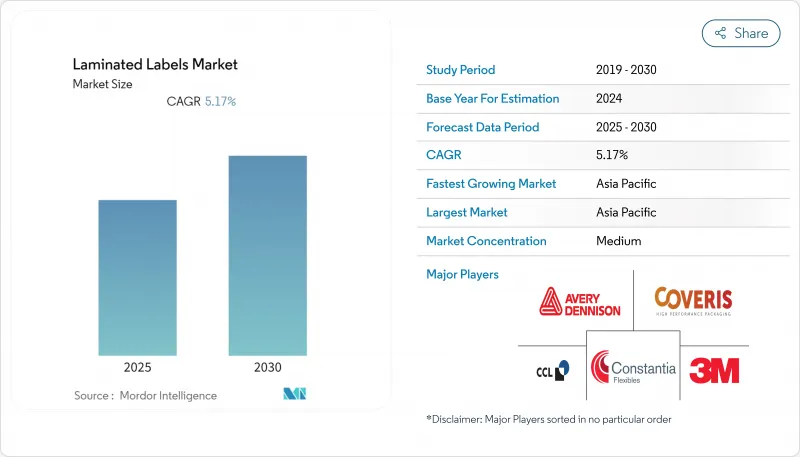

預計到 2025 年,複合標籤市場規模將達到 365 億美元,到 2030 年將達到 483 億美元,複合年成長率為 5.8%。

儘管電子商務出貨量不斷成長、食品安全標準日益嚴格以及藥品序列化要求等因素推動了包裝可回收性和碳排放披露法規的日益完善,但複合標籤市場仍在持續擴張。對能夠承受自動化分類的耐用面材以及減少廢棄物的無底紙包裝的需求,正在擴大能夠提供高性能合規產品的加工商的利潤空間。雖然聚酯仍佔據最大的市場佔有率,但聚丙烯的低成本和良好的印刷性能正推動其在食品飲料行業的應用。從區域來看,亞太地區擁有規模優勢,而北美在高階和監管敏感型應用領域發展最快。

全球覆膜標籤市場趨勢與洞察

電子商務的蓬勃發展推動了耐用型運輸標籤的發展

線上零售的激增使小包裹處理強度提高了 60% 以上,導致普通標籤更容易受到溫度變化和機械衝擊的影響,從而出現分層現象。 ASTM D4169-22 標準強制要求進行順序危險測試,敦促加工商設計能夠在整個分銷週期中牢固粘附在紙箱上的基材。永續性目標還包括清潔剝離的要求,以確保標籤不會干擾紡織品回收流程。像 OptiCut WashOff 這樣的無底紙捲材可將標籤產量比率提高 50%,並減少運輸排放,從而吸引那些關注其範圍 3 碳足跡的物流營運商。加工商報告稱,採用專為電子商務設計的標籤結構可提高 15% 至 20% 的利潤率,而數位印刷技術則允許托運人嵌入即時代碼,以便進行追蹤和退貨管理。

包裝食品和飲料的需求激增。

都市區生活方式和單份包裝偏好正在推動包裝食品的銷售量,隨著中產階級消費群體的不斷壯大,各大品牌在印度的包裝支出正以26.7%的複合年成長率成長。印度食品安全與標準局(FSSAI)現已禁止在食品接觸油墨中使用甲苯,促使標籤製造商轉向低遷移化學品並進行嚴格的遷移測試。高階零食和飲料品牌正在尋求具有亮麗貨架外觀和阻隔保護功能的金屬化壓敏薄膜。透過與賽卡-億滋國際(Saica-Mondelez)等夥伴關係,紙基複合材料的目標是在不降低熱封性能的前提下,減少25%的原生塑膠用量。區域供應多元化,尤其是在亞太地區,正在降低供應中斷風險,並鼓勵新增本地產能。

原物料價格波動

隨著煉油廠的合理化進程不斷推進,預計到2025年中期,丙烯原料價格將超過每磅40美分,推高聚酯和聚丙烯薄膜的成本。 2024年12月合約的交易價格已達每磅35.75美分,顯示通膨趨勢將持續到2026年。 Braidy公司已宣布,原物料成本上漲將嚴重拖累其2024會計年度的利潤率。加工商正在探索使用再生樹脂和生物基樹脂,但目前用量仍然較低,但溢價很高。多供應商策略和區域庫存緩衝正逐漸成為標準的風險管理手段。

細分市場分析

到2024年,聚酯材料將佔據複合標籤市場35.45%的最大佔有率,這主要得益於其優異的耐化學腐蝕性能,這對於製藥、化工桶以及戶外應用至關重要。聚丙烯材料預計到2030年將以7.48%的複合年成長率成長,這主要得益於其低密度、高產量比率和光滑的印刷表面,這些特性使其深受食品飲料加工商的青睞。歐盟法規要求2030年包裝必須使用30%的再生PET,增加了再生PET面材的需求,但供應無法滿足需求,導致價格居高不下。受REACH法規對微塑膠的限制,乙烯基材料的市佔率持續下降。生物膜目前仍屬於小眾市場,但正吸引那些尋求可堆肥和生物基訊息的品牌。

展望未來,再生材料含量強制要求可能會收緊聚酯纖維的供應,推高價格,並加速對成本敏感的產品中聚丙烯的替代。同時,生物基PET和化學再生樹脂的研發一旦規模化,將為未來的大規模生產奠定基礎。由於複合標籤市場青睞低碳足跡產品,那些能夠在不犧牲透明度或挺度的前提下合格再生材料含量要求的供應商有望獲得市場佔有率。

由於飲料、製藥和物流的自動化施用器依賴連續捲筒紙供料,捲筒標籤將在2024年佔據複合標籤市場58.35%的佔有率。而片狀標籤的市佔率僅41.65%,年複合成長率為6.54%,主要得益於手工食品、化妝品和季節性宣傳活動的小批量印刷的數位印刷機的普及。像Unisplice413這樣的自動化拼接系統可以將生產線運作提高10%,進一步凸顯了捲筒紙的生產效率優勢。

另一方面,單張紙可以讓品牌所有者在多個 SKU 上使用不同的圖案而無需模具,從而避免庫存浪費。隨著電商微型品牌的激增,單張紙在 1000 件以下的訂單中將需求旺盛,因為這類訂單無需承擔柔版印刷的設置成本。無底紙技術提升了捲筒紙的吸引力,但對接裁切所需的印刷機維修最初可能僅限於大型印刷廠。

複合標籤市場按材料類型(聚酯、聚丙烯(BOPP、CPP)、乙烯基及其他)、形態(卷材、片材)、結構(面材、黏合劑)、印刷技術(柔版印刷、數位噴墨印刷及其他)、終端用戶產業(食品飲料、製造及工業、電子及家電及其他)及地區進行細分。市場預測以美元計價。

區域分析

到2024年,亞太地區將佔據複合標籤市場41.34%的佔有率,這主要得益於中國工業生產成長6%以及化學製造業成長12.7%,後者為薄膜生產提供了原料。印度的生產連結獎勵計畫旨在2025年使先進製造業對GDP的貢獻達到25%,從而擴大國內需求並提升出口能力。像安姆科這樣的跨國公司已在古吉拉突邦增設產能,以滿足當地零食和個人護理品牌的需求,這進一步印證了該地區的規模和成本優勢。日本和韓國擁有精密塗層技術,而東南亞則受益於供應鏈多元化。

受DSCSA序列化、EPA溶劑法規以及小包裹運輸快速成長的推動,北美預計將以8.32%的複合年成長率成長。 ASTM運輸標準和消費者對優質影像的偏好將推動該地區高附加價值產品的銷售成長。 ProMach收購Etiflex將增強墨西哥在近岸外包領域的地位,並擴展其RFID和可變數據產品線。

歐洲透過《包裝及包裝廢棄物法規》維持其監管領先地位。該法規要求在2028年實現包裝完全可回收,並透過設定再生材料含量閾值來再形成材料選擇。 FINAT的襯紙回收計畫以及德國向植物來源油墨的轉型,凸顯了永續性作為提升競爭力的關鍵因素。隨著西方加工商尋求低成本且符合歐盟標準的生產基地,東歐可望吸引新的塗佈生產線。

中東、非洲和南美洲等規模較小的複合標籤市場正快速發展,食品加工商和農產品出口商紛紛採用可追溯標籤。基礎設施不足和外匯波動目前限制市場規模,但隨著各國政府呼籲投資以減少進口依賴,本地產量可望成長。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 電子商務的蓬勃發展推動了耐用型運輸標籤的發展

- 加工食品和飲料的需求激增

- 藥品強制序列化

- 無底紙層壓標籤

- 碳足跡揭露標籤

- 市場限制

- 原物料價格波動

- 改用金屬化箔和熱縮套管

- 溶劑型油墨和黏合劑法規

- 閉迴路閉合迴路,不含塑膠標籤

- 供應鏈分析

- 監管狀況

- 技術展望

- 波特五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

- 環境足跡分析

第5章 市場規模與成長預測

- 依材料類型

- 聚酯纖維

- 聚丙烯(雙向拉伸聚丙烯 (BOPP)、共聚聚丙烯 (CPP))

- 乙烯基塑膠

- 可生物分解薄膜

- 其他成分

- 按形式

- 卷

- 床單

- 按成分

- Facestock

- 黏合劑

- 離型膜

- 透過印刷技術

- 柔版印刷

- 數位噴墨

- 數位 - 靜電攝影

- 凹版印刷

- 抵銷

- 螢幕/報告

- 按最終用戶產業

- 飲食

- 製造業和工業

- 電子產品和家用電器

- 製藥和醫療保健

- 個人護理和化妝品

- 零售和物流

- 其他終端用戶產業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 法國

- 義大利

- 西班牙

- 英國

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 其他亞太地區

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 其他非洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略舉措

- 市佔率分析

- 公司簡介

- Avery Dennison Corporation

- CCL Industries Inc.

- 3M Company

- Coveris Holdings SA

- Torraspapel Adestor

- Constantia Flexibles Group GmbH

- RR Donnelley & Sons Company

- Flexcon Company Inc.

- Stickythings Ltd.

- Gipako Ltd.

- Hub Labels Inc.

- Cenveo Corporation

- Ravenwood Packaging Ltd.

- Reflex Labels Ltd.

- UPM Raflatac Oy

- Amcor plc

- Multi-Color Corporation

- Fuji Seal International Inc.

- SATO Holdings Corp.

- Lintec Corporation

- Zebra Technologies Corp.

- Brady Corporation

第7章 市場機會與未來展望

The laminated label market size stood at USD 36.5 billion in 2025 and is forecast to reach USD 48.3 billion by 2030, advancing at a 5.8% CAGR.

Rising e-commerce shipping volumes, tougher food-safety codes, and pharmaceutical serialization mandates are expanding the laminated label market, even as packaging rules tighten around recyclability and carbon disclosures. Demand for durable facestocks that endure automated sortation, together with linerless formats that reduce waste, is widening profit margins for converters that can supply high-performance, regulation-compliant products. Polyester retains the largest material slice, yet polypropylene's lower cost and printability are lifting its uptake in food and beverage lines. Regionally, Asia-Pacific enjoys scale advantages, while North America is moving fastest on premium, regulation-driven applications.

Global Laminated Labels Market Trends and Insights

E-commerce boom driving durable shipping labels

Surging online retail volumes have pushed parcel handling intensity up by more than 60%, exposing ordinary labels to temperature swings and mechanical shocks that cause delamination. ASTM D4169-22 now requires sequential hazard testing, prompting converters to engineer substrates that stay bonded to corrugate throughout distribution cycles. Sustainability goals add a removal-cleanly prerequisite so that labels do not disrupt fiber recycling streams. Linerless rolls such as OptiCut WashOff increase label yield by 50% and slash transport emissions, attracting logistics operators that track Scope 3 footprints. Converters report 15-20% higher margins on e-commerce-specific constructions, while digital print lets shippers embed real-time codes for tracking and returns management.

Packaged food and beverage demand surge

Urban lifestyles and single-serve preferences are lifting packaged food volumes, with India's packaging spend growing at 26.7% CAGR as brands court rising middle-class consumers. India's FSSAI now bans toluene in food-contact inks, pushing label makers toward low-migration chemistries and rigorous migration testing. Premium snack and beverage lines want metalized pressure-sensitive films that give brighter shelf appeal and barrier protection. Paper-based laminates from partnerships such as Saica-Mondelez target a 25% virgin-plastic cutback without losing heat-sealability. Regional supply diversification, especially within Asia-Pacific, is mitigating disruption risks and stimulating new local capacity additions.

Raw-material price volatility

Propylene feedstock is forecast to top 40 cents/lb by mid-2025 following refinery rationalizations, raising polyester and polypropylene film costs. December 2024 contracts already traded at 35.75 cents, telegraphing lasting inflation into 2026. Brady Corporation disclosed raw-material spikes as a chief drag on FY 2024 margins. Converters are exploring recycled or bio-based resins, yet volumes remain low and premiums high. Multi-supplier strategies and regional inventory buffers are becoming standard risk-management playbooks.

Other drivers and restraints analyzed in the detailed report include:

- Pharmaceutical serialization mandates

- Linerless laminated labels adoption

- Shift to metallized foils and shrink sleeves

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polyester delivered the largest slice of the laminated label market at 35.45% in 2024 thanks to chemical resistance vital for pharma, chemical drum, and outdoor-exposure uses. Polypropylene's 7.48% CAGR through 2030 reflects food and beverage converters embracing its lower density, higher yield, and smoother print surface. EU rules dictating 30% recycled PET in packaging by 2030 are pushing buyers to recycled PET facestocks, though supply lags demand and prices remain elevated. Vinyl continues to decline amid REACH microplastics curbs. Bio-films are a niche today but attract brands pursuing compostable or bio-sourced messaging.

Looking ahead, recycled content mandates should tighten polyester's availability and buoy prices, possibly accelerating polypropylene's replacement rate in cost-sensitive SKUs. Simultaneously, R&D around bio-based PET and chemically recycled resins promises future volumes once scale materializes. Suppliers that can qualify recycled inputs without sacrificing clarity or stiffness will seize share as the laminated label market rewards low-carbon footprints.

Roll configurations dominated 58.35% of laminated label market share in 2024 because automated applicators in beverages, pharmaceuticals, and logistics depend on continuous web feeds. Sheet labels, though only 41.65%, clock a 6.54% CAGR on the back of digital presses that handle short runs for craft food, cosmetics, and seasonal campaigns. Automatic splicing systems like Unisplice 413 raised line uptime by 10%, reinforcing rolls' productivity advantage.

Sheets, however, let brand owners vary artwork across multiple SKUs without tooling, cutting inventory waste. As e-commerce microbrands proliferate, sheet demand will intensify for orders under 1,000 units where flexo setup costs are untenable. Linerless technology reinforces rolls' appeal, yet printer retrofits required for butt-cut webs may limit adoption to large fleet owners initially.

Laminated Labels Market is Segmented by Material Type (Polyester, Polypropylene (BOPP, CPP), Vinyl, and More), Form (Rolls, Sheets), Composition (Facestock, Adhesive), Printing Technology (Flexographic, Digital - Ink-Jet, and More), End-User Industry (Food and Beverage, Manufacturing and Industrial, Electronics and Appliances, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific held 41.34% of the laminated label market in 2024, buoyed by China's 6% industrial output rise and 12.7% jump in chemical manufacturing that secures film feedstocks. India's production-linked incentives aim for 25% GDP contribution from advanced manufacturing by 2025, enlarging domestic demand and export capacity. Multinationals such as Amcor added Gujarat capacity to serve regional snack and personal-care brands, confirming the region's scale and cost edge. Japan and South Korea contribute high-precision coating know-how, whereas Southeast Asia gains from supply-chain diversification.

North America, projected at an 8.32% CAGR, is propelled by DSCSA serialization, EPA solvent regulations, and rapid parcel-shipping growth. ASTM shipping standards and consumer preference for premium graphics position the region for value-added volumes. Mexico's role in near-shoring strengthens, illustrated by ProMach's Etiflex acquisition that expands RFID and variable-data offerings.

Europe maintains regulatory leadership through the Packaging and Packaging Waste Regulation, obliging full recyclability by 2028 and recycled-content thresholds that reshape material menus. FINAT's liner recycling drive and Germany's plant-based-ink transition underscore sustainability as the prime competitive lever. Eastern Europe may attract new coating lines as Western converters seek low-cost yet EU-compliant production bases.

Middle East & Africa and South America together form a smaller slice of the laminated label market but register brisk uptake as food-processing and agro-exporters adopt traceability stickers. Infrastructure gaps and currency swings restrain scale for now, though localized manufacturing might rise as governments court investment to cut import dependence.

- Avery Dennison Corporation

- CCL Industries Inc.

- 3M Company

- Coveris Holdings S.A.

- Torraspapel Adestor

- Constantia Flexibles Group GmbH

- R.R. Donnelley & Sons Company

- Flexcon Company Inc.

- Stickythings Ltd.

- Gipako Ltd.

- Hub Labels Inc.

- Cenveo Corporation

- Ravenwood Packaging Ltd.

- Reflex Labels Ltd.

- UPM Raflatac Oy

- Amcor plc

- Multi-Color Corporation

- Fuji Seal International Inc.

- SATO Holdings Corp.

- Lintec Corporation

- Zebra Technologies Corp.

- Brady Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 E-commerce boom driving durable shipping labels

- 4.2.2 Packaged food and beverage demand surge

- 4.2.3 Pharmaceutical serialization mandates

- 4.2.4 Linerless laminated labels adoption

- 4.2.5 "Carbon-footprint" disclosure labels

- 4.3 Market Restraints

- 4.3.1 Raw-material price volatility

- 4.3.2 Shift to metallized foils and shrink sleeves

- 4.3.3 Solvent-borne ink and adhesive regulation

- 4.3.4 Closed-loop paper packs eliminating plastic labels

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Environmental Footprint Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Polyester

- 5.1.2 Polypropylene (BOPP, CPP)

- 5.1.3 Vinyl

- 5.1.4 Biodegradable Films

- 5.1.5 Other Material Type

- 5.2 By Form

- 5.2.1 Rolls

- 5.2.2 Sheets

- 5.3 By Composition

- 5.3.1 Facestock

- 5.3.2 Adhesive

- 5.3.3 Release Liner

- 5.4 By Printing Technology

- 5.4.1 Flexographic

- 5.4.2 Digital - Ink-jet

- 5.4.3 Digital - Electrophotography

- 5.4.4 Gravure

- 5.4.5 Offset

- 5.4.6 Screen / Letterpress

- 5.5 By End-user Industry

- 5.5.1 Food and Beverage

- 5.5.2 Manufacturing and Industrial

- 5.5.3 Electronics and Appliances

- 5.5.4 Pharmaceuticals and Healthcare

- 5.5.5 Personal Care and Cosmetics

- 5.5.6 Retail and Logistics

- 5.5.7 Other End-user Industry

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 France

- 5.6.2.3 Italy

- 5.6.2.4 Spain

- 5.6.2.5 United Kingdom

- 5.6.2.6 Russia

- 5.6.2.7 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 Middle East

- 5.6.4.1.1 Saudi Arabia

- 5.6.4.1.2 United Arab Emirates

- 5.6.4.1.3 Turkey

- 5.6.4.1.4 Rest of Middle East

- 5.6.4.2 Africa

- 5.6.4.2.1 South Africa

- 5.6.4.2.2 Nigeria

- 5.6.4.2.3 Rest of Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Avery Dennison Corporation

- 6.4.2 CCL Industries Inc.

- 6.4.3 3M Company

- 6.4.4 Coveris Holdings S.A.

- 6.4.5 Torraspapel Adestor

- 6.4.6 Constantia Flexibles Group GmbH

- 6.4.7 R.R. Donnelley & Sons Company

- 6.4.8 Flexcon Company Inc.

- 6.4.9 Stickythings Ltd.

- 6.4.10 Gipako Ltd.

- 6.4.11 Hub Labels Inc.

- 6.4.12 Cenveo Corporation

- 6.4.13 Ravenwood Packaging Ltd.

- 6.4.14 Reflex Labels Ltd.

- 6.4.15 UPM Raflatac Oy

- 6.4.16 Amcor plc

- 6.4.17 Multi-Color Corporation

- 6.4.18 Fuji Seal International Inc.

- 6.4.19 SATO Holdings Corp.

- 6.4.20 Lintec Corporation

- 6.4.21 Zebra Technologies Corp.

- 6.4.22 Brady Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment