|

市場調查報告書

商品編碼

1846251

硬脂酸鎂:市場佔有率分析、產業趨勢、統計數據、成長預測(2025-2030 年)Magnesium Stearate - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

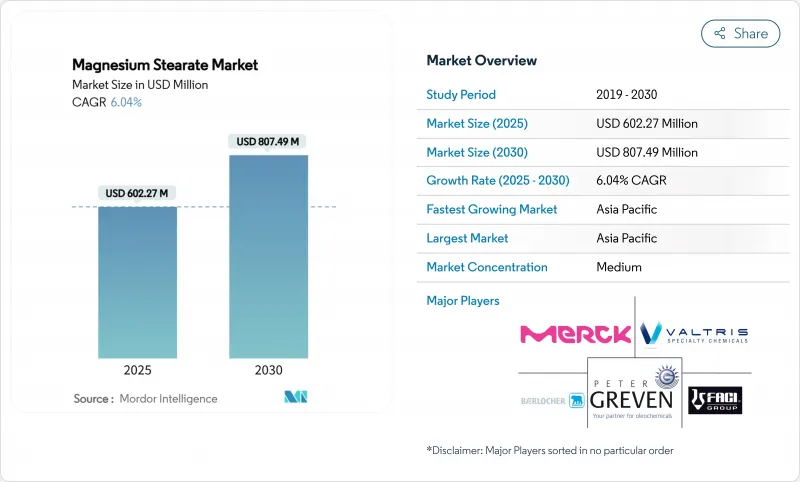

預計到 2025 年,硬脂酸鎂市場規模將達到 6.0227 億美元,到 2030 年將達到 8.0749 億美元,預測期(2025-2030 年)複合年成長率為 6.04%。

目前的成長動能反映了該化合物在藥物壓片、個人護理黏合劑、食品防結塊系統和聚合物熱穩定劑等領域的成熟應用。需求旺盛,尤其是在北美和歐洲,因為對連續口服固體製劑生產的投資促使設備製造商指定使用能夠在高通量條件下保持潤滑性的輔料。同時,潔淨標示的需求正推動供應商推出植物來源或不含棕櫚油的等級產品,在不降低核心產品銷售量的情況下提供更高價格的替代品。在亞太地區,學名藥生產的擴張和人均藥品攝取量的成長正在推動大眾消費,而電動車線束的出現則為硬脂酸穩定PVC開闢了一個雖小但具有重要戰略意義的市場。競爭的核心在於分析一致性、脂肪酸鏈檢驗和可追溯性計劃,以確保注重品質的買家放心。

全球硬脂酸鎂市場趨勢及洞察

固態製劑生產加速向連續生產線轉型

輝瑞和禮來等領先製造商目前已運作商業性的連續生產營運,在一體化撬裝設備上完成片劑的混合、壓片和包衣,從而消除了以往因停機而掩蓋輔料差異的情況。能確保粒徑分佈窄、脂肪酸比例穩定的硬脂酸鎂市場參與企業,正鞏固其作為首選供應商的地位。監管機構透過縮短連續加工廠的核准時間來鼓勵這種轉變,進一步強化了對高規格輔料的需求。連續生產放大了每種原料對關鍵品質屬性的影響,促使一級採購商將供應商名單縮減至擁有強大隨線分析工具的公司。

潔淨標示膳食補充劑的純素/無棕櫚油等級產品的出現

隨著消費者對輔料來源的關注程度與對活性成分的關注程度不相上下,膳食補充劑配方師正盡可能避免使用動物性或棕櫚基硬脂酸鹽。像Biogrund這樣的供應商已將CompactCel LUB商業化,這是一種植物性產品,其性能與傳統潤滑劑相當,但符合純素標籤標準和永續棕櫚油圓桌會議(RSPO)的承諾。雖然功能等效性降低了改良的門檻,但製造商仍會在測試中檢驗產品的流動性、永續和溶解度,從而維持實驗室測試的收益。零售商正在透過強制要求自有品牌補充劑的輔料成分透明化來推動這一趨勢,這促使即使是注重成本的自有品牌製造商也使用經過認證的純素成分。

更嚴格的棕櫚油可追溯性法規推高了原料成本

歐盟的森林砍伐法規和美國海關的審核要求硬脂酸生產商記錄每一噸棕櫚油衍生的硬脂酸。合規需要衛星監測、同位素指紋圖譜和區塊鏈記錄,這增加了小型工廠難以承受的採購成本。馬來西亞棕櫚油局等機構的分析要求提高了檢測頻率,增加了實驗室的資本成本,並延長了前置作業時間。然而,大型跨國公司可以透過向優先考慮道德採購的個人護理品牌出售溢價的經認證的永續輔料來收回成本。

細分市場分析

到2024年,醫藥應用將佔硬脂酸鎂市場收益的44.18%,這得益於其數十年來獲得的監管認可和成本效益。片劑、膠囊和顆粒劑通常含有濃度低於2%的輔料,但由於口服固體製劑的銷量龐大,累積銷量仍可觀。由於對現有產品進行重新配方需要新的生物等效性證明文件,品牌藥和非專利生產商都在保留現有的硬脂酸鹽等級,從而保護該領域免受短期替代風險的影響。同時,在壓製粉末和乾洗髮的推動下,個人護理業務正以6.45%的複合年成長率呈現最快成長動能。這一成長將使高階化妝品級產品在較小的基數上實現銷售成長。

食品和飲料製造商將硬脂酸鎂粉末用作糖粉、烘焙混合料和粉狀飲料基料中的抗結塊劑和流動劑。即使在低添加量下,硬脂酸鎂也能可靠地控制水分,這使其成為兼顧輸送機吞吐量和消費者傾倒體驗的關鍵因素。塑膠加工商已為耐熱聚氯乙烯(PVC) 開闢了一片市場,尤其是在電動車線束領域,因為電動車的引擎室溫度可能很高。這類產品雖然規模不大,但卻能使收益來源多元化,並減少對醫藥週期的依賴。總而言之,這些因素共同保護了硬脂酸鎂市場免受任何單一產業需求衝擊的影響。

該報告涵蓋了硬脂酸鎂市場參與者,並根據最終用戶產業(製藥、食品飲料、個人護理、塑膠及其他最終用戶產業)和地區(亞太、北美、南美以及中東和非洲)對其進行細分。報告以收益為單位,提供了上述所有細分市場的硬脂酸鎂市場規模和預測。

區域分析

亞太地區是硬脂酸鎂市場的主要驅動力,預計2024年將佔全球營收的41.65%,並有望在2030年前以6.32%的複合年成長率成長。中國鎂金屬產能預計在2024年成長24.5%,超過102萬噸,進而緩解區域原料供應緊張的局面。同時,印度合約開發和製造企業大幅提高了片劑產量,以出口到非洲和拉丁美洲,進一步提振了對潤滑劑的需求。東南亞國家作為消費和二次加工中心也從中受益,其中越南和印尼為鄰近的東協市場提供具成本效益的配方服務。

北美仍然是技術領先者,其多家獲得美國食品藥物管理局(FDA) 批准的連續生產工廠為嚴格的輔料規格樹立了標竿。買家堅持要求完全符合美國藥典 (USP)、歐洲藥典 (EP) 和日本藥典 (JP) 的專論,迫使供應商維護統一的文檔資料包。在美國,清潔標籤聲明更為普遍,供應商正致力於推出純素認證產品線,因為天然產品零售商已將動物性硬脂酸鹽列入黑名單。歐洲也提出了類似的品質要求,加強了對永續性的審查,並強制要求在採購決策前進行棕櫚油供應鏈審核和生命週期評估。

棕櫚油在南美洲、中東和非洲的使用量較低,但在全球範圍內呈上升趨勢。巴西國家衛生監督局 (ANVISA) 致力於加快學名藥的核准,沙烏地阿拉伯和南非的公開競標競標優先考慮在地採購。然而,當地的生產能力較為分散,且往往缺乏先進的分析設備,這為提供承包優質服務的跨國在地採購創造了機會。儘管產量較低,但隨著人均醫療保健支出的成長,這些地區能夠提供風險分散和長期成長潛力。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 加速固態製劑連續生產線的轉型

- 純素/無棕櫚油等級的出現瞄準了潔淨標示膳食補充劑市場。

- 提高低收入國家口服固體製劑的攝取量

- 電動車線束中聚氯乙烯(PVC)熱穩定性的需求

- 化妝品粉餅產品線的快速擴張

- 市場限制

- 由於棕櫚油可追溯性法規嚴格,投入成本上升。

- 採用硬脂醯富馬酸鈉作為高性能潔淨標示替代品

- 小型供應商帶來的品質波動風險

- 價值鏈分析

- 五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 按最終用戶產業

- 製藥

- 飲食

- 個人護理

- 塑膠

- 其他終端用戶產業(油漆等)

- 按地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 東南亞國協

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略舉措

- 市佔率(%)/排名分析

- 公司簡介

- Baerlocher GmbH

- FACI Corporate SpA

- Huzhou City Linghu Xinwang Chemical Co., Ltd

- IRRH Specialty Chemicals

- James M. Brown Ltd.

- Kemipex

- Kirsch Pharma GmbH

- Merck KGaA

- MLA Group of Industries

- NB Entrepreneurs

- Nimbasia

- Peter Greven GmbH & Co. KG

- Roquette Freres

- Struktol Company of America, LLC

- Thermo Fisher Scientific Inc.

- Valtris Specialty Chemicals

第7章 市場機會與未來展望

The Magnesium Stearate Market size is estimated at USD 602.27 Million in 2025, and is expected to reach USD 807.49 Million by 2030, at a CAGR of 6.04% during the forecast period (2025-2030).

Current growth momentum mirrors the compound's entrenched role in pharmaceutical compression, personal care binding, anti-caking food systems, and polymer heat stabilization. Heightened investment in continuous oral-solid-dose manufacturing, especially across North America and Europe, keeps demand buoyant as equipment makers specify excipients that sustain lubrication under high-throughput conditions. Clean-label imperatives have simultaneously pushed suppliers to introduce plant-based or palm-free grades, adding premium-priced alternatives without displacing core volumes. Asia-Pacific's expanding generic production and rising per-capita medicine intake anchor bulk consumption, while the advent of electric-vehicle wire harnesses opens a small yet strategically significant outlet for stearate-stabilized PVC. Competitive intensity revolves around analytical consistency, fatty-acid-chain verification, and traceability programs that reassure quality-focused buyers.

Global Magnesium Stearate Market Trends and Insights

Accelerated Shift to Continuous-manufacturing Lines in Solid-dose Pharma

Large producers such as Pfizer and Eli Lilly now run commercial continuous-manufacturing assets that blend, compress, and coat tablets in integrated skids, eliminating stoppages that once masked excipient variability. Magnesium stearate market participants able to guarantee narrow particle-size distributions and stable fatty-acid ratios secure preferred-supplier status because any deviation escalates the risk of lubrication overshoot that damages tensile strength. Regulators back the switch by shortening approval review times for continuous plants, further entrenching high-specification excipient demand. Continuous processing magnifies every input's contribution to critical-quality attributes, encouraging tier-one buyers to pare their vendor lists to firms with robust in-line analytical tools.

Emergence of Vegan / Palm-free Grades Targeting Clean-label Nutraceuticals

Consumers scrutinize excipient origins as closely as active ingredients, prompting nutraceutical formulators to abandon animal-derived or palm-based stearates where feasible. Suppliers such as Biogrund commercialized CompactCel LUB, a vegetable-sourced grade that matches traditional lubrication yet aligns with vegan labeling and Roundtable on Sustainable Palm Oil commitments . While functional equivalence lowers reformulation hurdles, manufacturers still validate flow, compressibility, and dissolution in pilot runs, sustaining testing revenues for analytical houses. Retailers amplify momentum by mandating excipient transparency for store-brand supplements, nudging even cost-sensitive private-labelers toward certified vegan inputs.

Stringent Palm-oil Traceability Regulations Increasing Input Costs

The European Union's deforestation regulation and parallel the United States Customs audits oblige stearate producers to document every tonne of palm-derived stearic acid. Compliance entails satellite monitoring, isotopic fingerprinting, and blockchain recordkeeping, driving procurement overheads that smaller mills struggle to absorb. Analytical mandates from bodies like the Malaysian Palm Oil Board have raised testing frequency, adding laboratory capital expense and elongating lead times . Larger multinationals, however, recoup costs by marketing certified-sustainable excipients at premiums to personal-care brands prioritizing ethical sourcing.

Other drivers and restraints analyzed in the detailed report include:

- Rising Intake of Oral-Solid-Dosage Forms in Low-income Economies

- Rapid Expansion of Cosmetic Pressed-powder Lines

- Adoption of Sodium Stearyl Fumarate as a High-performance Clean-label Alternative

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2024, pharmaceutical applications accounted for 44.18% of the Magnesium Stearate market revenue, underscoring decades of regulatory acceptance and cost-efficient performance. Tablets, capsules, and granules integrate the excipient at concentrations usually below 2%, yet cumulative volumes remain high due to sheer output of oral-solid doses. Because reformulating legacy products demands new bioequivalence dossiers, brand and generic manufacturers retain existing stearate grades, insulating this segment from short-term substitution risk. Meanwhile, the personal care business, anchored by pressed-powder and dry shampoo launches, shows the fastest trajectory at a 6.45% CAGR. This growth adds premium-priced, cosmetic-grade volumes, albeit from a smaller base.

Food and beverage formulators employ the powder as an anti-caking and flow agent in icing sugar, baking mixes, and powdered drink bases. Even at low inclusion rates, dependable moisture control renders magnesium stearate indispensable where conveyor throughput and consumer pour-ability intersect. Plastics processors have carved a niche in heat-stabilized Polyvinyl Chloride (PVC), particularly for electric-vehicle wiring that experiences higher under-hood temperatures. Although representing a modest slice, this outlet diversifies revenue streams and lowers reliance on pharmaceutical cycles. Collectively, these patterns safeguard the broader magnesium stearate market against demand shocks in any single vertical.

The Report Covers Magnesium Stearate Market Companies and is Segmented by End-User Industry (Pharmaceutical, Food & Beverage, Personal Care, Plastics, and Other End-User Industries) and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Size and Forecasts for Magnesium Stearate Market are Provided in Revenue (USD Million) for all the Above Segments.

Geography Analysis

Asia-Pacific led with 41.65% revenue in 2024 and is on track for a 6.32% CAGR through 2030, making it the linchpin of the magnesium stearate market. China's magnesium-metal capacity surged 24.5% in 2024, surpassing 1.02 Million tonnes and cushioning regional raw-material supply. Concurrently, India's contract-development and manufacturing organizations ramped tablet output for exports to Africa and Latin America, further lifting lubricant demand. Southeast Asian nations benefit as both consumption and secondary processing hubs, with Vietnam and Indonesia offering cost-advantaged blending services that feed neighboring Association of Southeast Asian Nations (ASEAN) markets.

North America remains a technology pacesetter, hosting several Food and Drug Administration (FDA)-approved continuous-manufacturing plants that set stringent excipient specification benchmarks. Buyers insist on full United States Pharmacopeia (USP), European Pharmacopoeia (EP), and Japanese Pharmacopoeia (JP) monograph compliance, compelling vendors to maintain harmonized documentation packs. Clean-label advocacy is more pronounced in the United States, where natural-product retailers blacklist animal-derived stearates, nudging suppliers toward certified vegan lines. Europe mirrors these quality demands and intensifies sustainability scrutiny, compelling palm-supply chain audits and life-cycle assessments before purchasing decisions.

South America, the Middle East, and Africa collectively contribute a smaller but rising parcel of global uptake. Brazil's Agencia Nacional de Vigilancia Sanitaria (ANVISA) fast-track for generic approvals fuels tablet output, while Saudi Arabian and South African public tenders prioritize local sourcing where feasible. However, fragmented local production capacity often lacks advanced analytical instruments, creating opportunity for multinational suppliers offering turnkey quality services. Despite lower volume, these geographies offer risk diversification and long-run upside as healthcare spend per capita climbs.

- Baerlocher GmbH

- FACI Corporate S.p.A.

- Huzhou City Linghu Xinwang Chemical Co., Ltd

- IRRH Specialty Chemicals

- James M. Brown Ltd.

- Kemipex

- Kirsch Pharma GmbH

- Merck KGaA

- MLA Group of Industries

- NB Entrepreneurs

- Nimbasia

- Peter Greven GmbH & Co. KG

- Roquette Freres

- Struktol Company of America, LLC

- Thermo Fisher Scientific Inc.

- Valtris Specialty Chemicals

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated Shift to Continuous-manufacturing Lines in Solid-dose Pharma

- 4.2.2 Emergence of Vegan/palm-free Grades Targeting Clean-label Nutraceuticals

- 4.2.3 Rising Intake of Oral Solid Dosage Forms in Low-income Economies

- 4.2.4 Polyvinyl Chloride (PVC) Heat-stabilization Demand in Electric-vehicle Wire Harnesses

- 4.2.5 Rapid Expansion of Cosmetic Pressed-powder Lines

- 4.3 Market Restraints

- 4.3.1 Stringent Palm-oil Traceability Regulations Increasing Input Costs

- 4.3.2 Adoption of Sodium Stearyl Fumarate as a High-performance Clean-label Alternative

- 4.3.3 Quality-variance Risk From Micro-scale Suppliers

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products and Services

- 4.5.5 Degree of Competition

5 Market Size & Growth Forecasts (Value)

- 5.1 By End-User Industry

- 5.1.1 Pharmaceutical

- 5.1.2 Food & Beverage

- 5.1.3 Personal Care

- 5.1.4 Plastics

- 5.1.5 Other End-iser Industries (Paints & Coatings, etc.)

- 5.2 By Geography

- 5.2.1 Asia-Pacific

- 5.2.1.1 China

- 5.2.1.2 Japan

- 5.2.1.3 India

- 5.2.1.4 South Korea

- 5.2.1.5 ASEAN Countries

- 5.2.1.6 Rest of Asia-Pacific

- 5.2.2 North America

- 5.2.2.1 United States

- 5.2.2.2 Canada

- 5.2.2.3 Mexico

- 5.2.3 Europe

- 5.2.3.1 Germany

- 5.2.3.2 United Kingdom

- 5.2.3.3 France

- 5.2.3.4 Italy

- 5.2.3.5 Spain

- 5.2.3.6 Russia

- 5.2.3.7 NORDIC Countries

- 5.2.3.8 Rest of Europe

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Rest of South America

- 5.2.5 Middle East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 South Africa

- 5.2.5.3 Rest of Middle East and Africa

- 5.2.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Baerlocher GmbH

- 6.4.2 FACI Corporate S.p.A.

- 6.4.3 Huzhou City Linghu Xinwang Chemical Co., Ltd

- 6.4.4 IRRH Specialty Chemicals

- 6.4.5 James M. Brown Ltd.

- 6.4.6 Kemipex

- 6.4.7 Kirsch Pharma GmbH

- 6.4.8 Merck KGaA

- 6.4.9 MLA Group of Industries

- 6.4.10 NB Entrepreneurs

- 6.4.11 Nimbasia

- 6.4.12 Peter Greven GmbH & Co. KG

- 6.4.13 Roquette Freres

- 6.4.14 Struktol Company of America, LLC

- 6.4.15 Thermo Fisher Scientific Inc.

- 6.4.16 Valtris Specialty Chemicals

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

- 7.2 Microencapsulation Technology Enhancing Magnesium Stearate's Performance