|

市場調查報告書

商品編碼

1846227

珍珠岩:市場佔有率分析、產業趨勢、統計數據、成長預測(2025-2030)Perlite - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

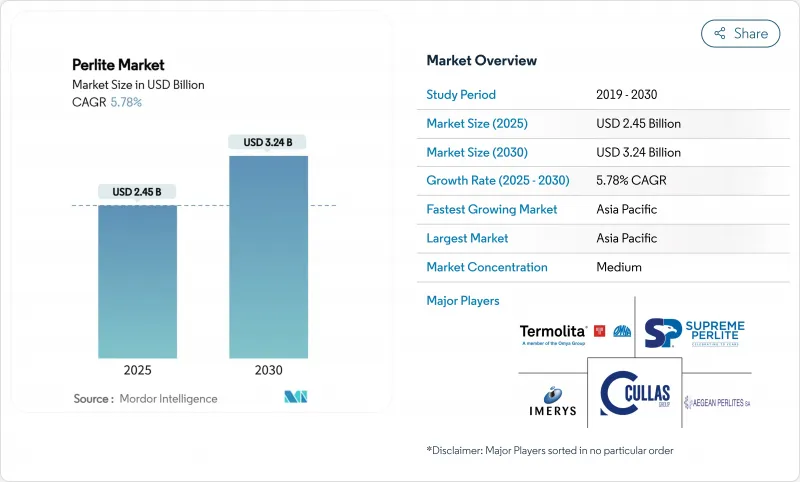

珍珠岩市場規模預計在 2025 年為 24.5 億美元,預計到 2030 年將達到 32.4 億美元,預測期內(2025-2030 年)的複合年成長率為 5.78%。

這一前景反映了節能建築、園藝、微過濾和隔熱材料領域對輕質骨材的強勁需求。建築規範對熱性能基準的嚴格要求正在推動產量成長,尤其是在歐洲和北美,而亞太地區的快速都市化正在創造大規模的基礎設施需求。用於低溫儲存、精釀飲料過濾和化妝品的特殊骨材淨利率更高,並支持產品創新。儘管土耳其和美國由於火山礦石資源豐富,供應仍然充足,但物流成本正在影響地區價格差異。

全球珍珠岩市場趨勢與見解

輕型結構的需求不斷成長

珍珠岩混凝土和灰泥可在不犧牲熱工性能的情況下降低結構負荷,從而以較小的地基建造更高的建築。膨脹顆粒比沙子和礫石輕高達80%,節省運輸成本。模組化建築工廠擴大指定使用珍珠岩增強板,以減少現場組裝時間並滿足嚴格的熱感橋限制。預製生產線受益於珍珠岩的一致性,從而提高了批次精度並減少了廢品。中國、印度和東協地區的長期都市化使珍珠岩市場成為永續高層建築的首選輕質骨材來源。

園藝和水耕技術應用熱潮

受控環境農場重視珍珠岩,認為它是一種無菌、pH值中性、可重複使用的基材鎖住水分並防止根腐病。美國和荷蘭的商業溫室報告稱,用珍珠岩取代泥炭含量較高的混合料後,產量增加。業內人士更傾向於使用粗粒級珍珠岩,以便自動灌溉系統能夠精確地維持氧氣水平。專業的醫用大麻種植者願意為獲得藥用種植認證的超潔淨級珍珠岩支付高價。東南亞城市農業的蓬勃發展,使當地加工商能夠以較低的運輸成本供應新鮮介質,從而支撐了該地區珍珠岩市場的需求。

現成的替代方案

蛭石、岩絨和膨脹粘土在重量和R值方面直接競爭。再生發泡聚苯乙烯(EPS)珠粒在無需高溫施工的輕砂漿中的佔有率正在不斷成長。在過濾,合成介質的截止閾值更窄,威脅珍珠岩在無菌藥品生產線的地位。在園藝領域,珍珠岩面臨椰殼纖維等生物基材料的競爭,這些材料聲稱永續性。產品創新和應用支援對於珍珠岩供應商在價格敏感的細分市場中保持佔有率仍然至關重要。

細分分析

膨脹珍珠岩在建築灰泥、園藝混合料和工業鬆散填充隔熱材料中廣泛應用,2024年佔據了珍珠岩市場67.56%的佔有率。成熟的應用使其價格保持競爭力,供應商也專注於提高物流效率和礦石精煉以確保淨利率。特種產品製造商目前正在推廣能夠承受低溫罐中粉塵產生的高密度電子煙和塗料級產品,而化妝品製造商則需要用於臉部磨砂膏的細粒度粉末。預計2030年,新興的特種級產品市場將以6.45%的複合年成長率擴張,吸收專注於表面功能化的研發支出。

Vapex 和特殊等級產品在醫藥過濾和空間受限的液化天然氣模組領域提供了不成比例的附加價值,這些領域的核准取決於技術閾值。處理供應商採用矽烷和聚合物處理,使單價比通用膨脹珍珠岩高出數倍。 Agroperlite 因其均衡的持水能力和中性 pH 值而在溫室中保持穩定產量。其他產品類型,包括用於鑄造爐渣清除的塊礦,佔據較小的市場,但受益於固定客群關係。產品組合構成顯示珍珠岩市場呈現兩極化:一方面是產量大的通用隔熱材料,另一方面是產量小、價值高的工程級珍珠岩。

區域分析

到2024年,亞太地區將佔全球輕質骨材消費量的48.75%,到2030年,複合年成長率將達到6.88%。中國「十四五」規劃強調裝配式住宅和綠色建築,這兩者都是輕質骨材的主要消費領域。印度的「智慧城市計畫」正在資助使用珍珠岩板的混合用途開發項目,以減少靜態和維修時間。日本、韓國和台灣的電子工廠和高科技溫室都需要超淨級珍珠岩。印尼和菲律賓的國內加工企業正在後向整合礦石開採業務,以減少對進口的依賴。

北美仍然是技術和特種等級材料的大本營。德克薩斯州和路易斯安那州的液化天然氣出口終端使用鬆散填充珍珠岩來建造1億加侖的儲存槽,加拿大的大麻種植者則大量購買園藝級珍珠岩。美國暖氣、冷氣與空調工程師美國(ASHRAE)90.1-2025等能源標準正在推動更深層的隔熱維修,包括珍珠岩空腔填充。歐洲正受惠於歐盟的零排放建築指令,德國、法國和義大利的維修計畫正在加速礦物隔熱材料的採用。儘管人事費用不斷上升,但來自希臘和土耳其的地中海礦石供應在到岸成本方面仍具有競爭力。

南美、中東和非洲雖小,但具有戰略意義。巴西受保護的亞馬遜地區允許城市中心垂直擴張,因此更青睞輕質、低能耗的骨材。智利的鋰鹵水作業使用珍珠岩助濾劑,在蒸發前去除細小顆粒。波灣合作理事會國家正在為液化天然氣轉運樞紐加裝隔熱層,以緩解沙漠高溫;南非新興的溫室叢集正在採購園藝珍珠岩,以應對水資源短缺問題。儘管物流和規模化挑戰仍然存在,但這些地區為早期市場參與企業提供了長期的上升空間。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場狀況

- 市場概況

- 市場促進因素

- 輕型結構的需求不斷成長

- 園藝和水耕技術應用熱潮

- 對冶金隔熱材料的要求日益提高

- 加強節能建築標準

- 擴大精釀飲料的過濾

- 市場限制

- 現成的替代方案

- 散裝運輸成本變動

- 高等級礦石區域性枯竭

- 價值鏈分析

- 五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章市場規模及成長預測

- 依產品類型

- 膨脹珍珠岩

- 農珍珠岩

- Vapex 和特種等級

- 其他產品類型

- 按用途

- 隔熱材料

- 填充材

- 耐火材料

- 過濾和過濾

- 磨料

- 土壤改良園藝

- 按行業

- 建築和基礎設施

- 園藝和農業

- 工業製造

- 食品和飲料加工

- 石油和天然氣/冷藏

- 其他

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- ASEAN

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 北歐

- 俄羅斯

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭態勢

- 市場集中度

- 策略舉措

- 市佔率(%)/排名分析

- 公司簡介

- Aegean Perlites SA

- Ausperl Pty Ltd

- Azer Perlite Corporation

- Blue Pacific Minerals

- Carolina Perlite Co., Inc.

- Cullas Construction Materials Industry and Foreign Trade Inc.

- Dupre Minerals Ltd.

- Genper Group

- Imerys

- Keltech Energies Ltd.

- Omya AG

- Perlite Canada Inc.

- Profilytra BV

- Resonac

- Silbrico Corporation

- Supreme Perlite

- Omya International AG

- The Schundler Company

第7章 市場機會與未來展望

The Perlite Market size is estimated at USD 2.45 Billion in 2025, and is expected to reach USD 3.24 Billion by 2030, at a CAGR of 5.78% during the forecast period (2025-2030).

The outlook reflects strong demand for lightweight aggregates in energy-efficient construction, horticulture, precision filtration and cryogenic insulation. Construction codes that tighten thermal-performance benchmarks, especially in Europe and North America, reinforce volume growth, while rapid urbanization in the Asia Pacific creates large-scale infrastructure demand. Specialty grades for cryogenic storage, craft-beverage filtration and cosmetics deliver higher margins and anchor product innovation. Supply remains adequate because of abundant volcanic ore in Turkey and the United States, yet logistics costs influence regional pricing differentials.

Global Perlite Market Trends and Insights

Growth in Lightweight Construction Demand

Perlite concrete and plasters lower structural load without sacrificing thermal performance, enabling taller buildings on smaller foundations . Transportation savings arise because expanded particles weigh up to 80% less than sand and gravel. Modular building factories increasingly specify Perlite-enhanced panels to shorten on-site assembly time and meet stringent thermal-bridge limits. Prefabrication lines benefit from the mineral's consistency, which improves batching accuracy and reduces rejects. Long-term urbanization in China, India and the ASEAN bloc positions the Perlite market as a preferred source of lightweight aggregates for sustainable, high-rise construction.

Horticulture & Hydroponics Adoption Boom

Controlled-environment farms value Perlite for sterile, pH-neutral, reusable substrates that retain moisture while preventing root rot. Commercial greenhouses in the United States and the Netherlands report yield gains when Perlite replaces peat-heavy mixes. Vertical-farm operators choose coarse grades that allow automated fertigation systems to maintain precise oxygen levels. Specialty growers of medical cannabis pay premium prices for ultra-clean grades certified for pharmaceutical cultivation. Expanding urban agriculture in Southeast Asia positions local processors to supply fresh media without high freight costs, underpinning regional Perlite market demand.

Readily Available Substitutes

Vermiculite, rock wool, and expanded clay compete directly on weight and R-value, while glass wool often offers a lower installed cost in large-scale commercial projects. Recycled expanded polystyrene (EPS) beads gain share in light screeds that do not require high service temperatures. In filtration, engineered synthetic media achieve narrower cut-off thresholds, threatening Perlite's position in sterile pharmaceutical lines. Horticulture faces bio-based rivals such as coconut coir that claim superior sustainability credentials. Product innovation and application support remain crucial for Perlite suppliers to defend their share in price-sensitive niches.

Other drivers and restraints analyzed in the detailed report include:

- Rising Metallurgical Insulation Requirements

- Energy-efficient Building Codes Tightening

- Volatile Bulk-shipping Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Expanded Perlite secured a 67.56% share of the Perlite market in 2024, reflecting broad acceptance in construction plasters, horticultural mixes, and industrial loose-fill insulation. Mature adoption keeps prices competitive, and suppliers emphasize logistics efficiency and ore purification to safeguard margins. Specialty producers now promote higher-density Vapex and coated grades that resist dusting inside cryogenic tanks, while cosmetic manufacturers demand finely classified powders for facial scrubs. The emerging specialty tier is projected to expand at a 6.45% CAGR to 2030, absorbing research and development (R&D) spend focused on surface functionalization.

Vapex & Specialty Grades add disproportionate value because technical thresholds govern approval in pharmaceutical filtration and space-constrained LNG modules. Processors apply silane or polymeric treatments that raise unit pricing several-fold relative to commodity expanded Perlite. Agro-Perlite maintains steady volumes in greenhouses that appreciate its balanced water-holding capacity and neutral pH. Other product types, including lump ore for foundry slag removal, occupy smaller niches yet benefit from captive customer relationships. The portfolio mix indicates a Perlite market trend toward bifurcation, high-volume commoditized insulation on one flank and low-volume, high-value engineered grades on the other.

The Perlite Market Report is Segmented by Product Type (Expanded Perlite, Agro-Perlite, and More), Application (Insulation, Fire-Proofing & Refractory, and More), End-Use Industry (Construction & Infrastructure, Horticulture & Agriculture, Industrial Manufacturing, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific accounted for 48.75% consumption in 2024 and is set to expand at a 6.88% CAGR through 2030. China's 14th Five-Year Plan emphasizes prefabricated housing and green buildings, both heavy consumers of lightweight aggregates. India's Smart Cities Mission funds mixed-use developments that use Perlite panels to reduce dead load and renovation timelines. Japan, South Korea, and Taiwan demand ultra-clean grades for electronics fabs and high-tech greenhouses. Domestic processors in Indonesia and the Philippines back-integrate into ore mining to reduce import reliance.

North America remains a technology and specialty-grade stronghold. United States LNG-export terminals in Texas and Louisiana consume loose-fill Perlite for 100-million-gal storage tanks, while Canadian cannabis producers buy horticultural grades in bulk. Energy codes such as American Society of Heating, Refrigerating and Air-Conditioning Engineers (ASHRAE) 90.1-2025 trigger deeper insulation retrofits, including Perlite cavity fills. Europe benefits from the EU zero-emission-building directive, with retrofit programs in Germany, France, and Italy accelerating mineral-based insulation uptake. Mediterranean ore supply from Greece and Turkey keeps landed cost competitive despite higher labor expenses.

South America and the Middle East & Africa together deliver a smaller yet strategic share. Brazil's protected Amazon region prompts urban centers to expand vertically, favoring lightweight, low-transport-energy aggregates. Chilean lithium brine operations adopt Perlite filter aids to remove fine particulates before evaporation. Gulf Cooperation Council countries insulate LNG transshipment hubs to mitigate desert heat, and South Africa's emerging greenhouse cluster sources horticultural Perlite to offset water scarcity. Although logistics and scale challenges persist, these regions present long-term upside for market participants that invest early.

- Aegean Perlites SA

- Ausperl Pty Ltd

- Azer Perlite Corporation

- Blue Pacific Minerals

- Carolina Perlite Co., Inc.

- Cullas Construction Materials Industry and Foreign Trade Inc.

- Dupre Minerals Ltd.

- Genper Group

- Imerys

- Keltech Energies Ltd.

- Omya AG

- Perlite Canada Inc.

- Profilytra BV

- Resonac

- Silbrico Corporation

- Supreme Perlite

- Omya International AG

- The Schundler Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growth in Lightweight Construction Demand

- 4.2.2 Horticulture & Hydroponics Adoption Boom

- 4.2.3 Rising Metallurgical Insulation Requirements

- 4.2.4 Energy-efficient Building Codes Tightening

- 4.2.5 Expansion of Craft-beverage Filtration

- 4.3 Market Restraints

- 4.3.1 Readily Available Substitutes

- 4.3.2 Volatile Bulk-shipping Costs

- 4.3.3 Regional Depletion of High-grade Ore

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Expanded Perlite

- 5.1.2 Agro-Perlite

- 5.1.3 Vapex & Specialty Grades

- 5.1.4 Other Product Types

- 5.2 By Application

- 5.2.1 Insulation

- 5.2.2 Fillers

- 5.2.3 Fire-Proofing & Refractory

- 5.2.4 Filtration & Filter-Aid

- 5.2.5 Abrasives & Polishing

- 5.2.6 Soil Amendment/Horticulture

- 5.3 By End-Use Industry

- 5.3.1 Construction & Infrastructure

- 5.3.2 Horticulture & Agriculture

- 5.3.3 Industrial Manufacturing

- 5.3.4 Food & Beverage Processing

- 5.3.5 Oil & Gas/Cryogenic Storage

- 5.3.6 Others

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 NORDIAC

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 South Africa

- 5.4.5.4 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/ Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Aegean Perlites SA

- 6.4.2 Ausperl Pty Ltd

- 6.4.3 Azer Perlite Corporation

- 6.4.4 Blue Pacific Minerals

- 6.4.5 Carolina Perlite Co., Inc.

- 6.4.6 Cullas Construction Materials Industry and Foreign Trade Inc.

- 6.4.7 Dupre Minerals Ltd.

- 6.4.8 Genper Group

- 6.4.9 Imerys

- 6.4.10 Keltech Energies Ltd.

- 6.4.11 Omya AG

- 6.4.12 Perlite Canada Inc.

- 6.4.13 Profilytra BV

- 6.4.14 Resonac

- 6.4.15 Silbrico Corporation

- 6.4.16 Supreme Perlite

- 6.4.17 Omya International AG

- 6.4.18 The Schundler Company

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment

- 7.2 Government Certification for its Consumption

珍珠岩市場規模、佔有率和趨勢分析報告:按應用、地區和細分市場預測(2026-2033 年)

珍珠岩市場規模、佔有率和趨勢分析報告:按應用、地區和細分市場預測(2026-2033 年) 珍珠岩市場:2026-2032年全球市場預測(按類型、產品形態、粒徑、應用、最終用戶和銷售管道)蛭石市場:依形態、等級、應用和分銷管道分類-2026-2032年全球市場預測

珍珠岩市場:2026-2032年全球市場預測(按類型、產品形態、粒徑、應用、最終用戶和銷售管道)蛭石市場:依形態、等級、應用和分銷管道分類-2026-2032年全球市場預測 膨脹珍珠岩市場:依形態、應用和地區分類發泡珍珠岩市場拓展:依等級、形態、應用及通路分類-2026-2032年全球市場預測

膨脹珍珠岩市場:依形態、應用和地區分類發泡珍珠岩市場拓展:依等級、形態、應用及通路分類-2026-2032年全球市場預測 2026年全球珍珠岩市場報告2026年全球蛭石市場報告全球膨脹珍珠岩材料市場(依產品等級、形狀、應用、終端用戶產業及通路分類)預測(2026-2032年)

2026年全球珍珠岩市場報告2026年全球蛭石市場報告全球膨脹珍珠岩材料市場(依產品等級、形狀、應用、終端用戶產業及通路分類)預測(2026-2032年) 膨脹珍珠岩市場規模、佔有率、成長分析(按類型、應用、最終用戶和地區分類)產業預測(2026-2033年)

膨脹珍珠岩市場規模、佔有率、成長分析(按類型、應用、最終用戶和地區分類)產業預測(2026-2033年) 珍珠岩市場-全球產業規模、佔有率、趨勢、機會和預測(細分、按產品類型、按應用、按地區和競爭,2020-2030 年)

珍珠岩市場-全球產業規模、佔有率、趨勢、機會和預測(細分、按產品類型、按應用、按地區和競爭,2020-2030 年)