|

市場調查報告書

商品編碼

1846226

異戊二烯:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)Isoprene - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

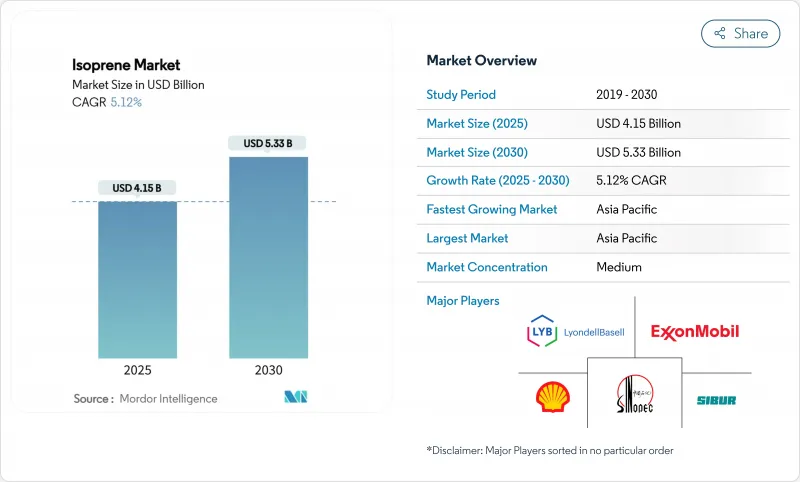

預計到 2025 年,異戊二烯市場規模將達到 41.5 億美元,到 2030 年將達到 53.3 億美元,在此期間的複合年成長率為 5.12%。

汽車製造商轉向使用高性能合成彈性體製造電動汽車輪胎、生物基原料測試的擴展以及亞太地區(佔全球產量一半以上)的生產,共同推動了成長。由於輪胎製造商優先考慮硫化率的穩定性,聚合物級材料保持溢價;同時,醫療設備創新推動了醫療保健產業對超純聚異戊二烯的需求加速成長。隨著石化製造商透過整合可再生能源來規避原油價格波動風險,生物發酵路線的戰略重要性日益凸顯,近期大量資金流入發酵新興企業也為此提供了支持。發酵專家和替代橡膠創新者對傳統C5裂解的經濟效益提出質疑,導致競爭加劇,促使現有企業轉向合資和原料多元化。

全球異戊二烯市場趨勢與洞察

電動車推動高性能輪胎對合成橡膠的需求激增

電動車的高扭矩負載要求使用具有卓越拉伸強度和更低滾動阻力的聚合物,這促使輪胎製造商尋求天然橡膠無法保證的穩定異戊二烯配方。美國環保署 (EPA) 指出,每年生產超過 30 億條輪胎,而電動車專用配方需要更高的耐久性以維持電池續航里程。米其林對生物基合成橡膠的探索凸顯了輪胎配方重新設計的必要性。亞太地區電動車製造的集中度提高了該地區對異戊二烯的需求,從而維持了超越典型更換週期的結構性需求。

投資生物基異戊二烯可降低石油基風險

諸如IFPEN的Atol和BioButterfly計劃等發酵技術證實了將可再生乙醇轉化為聚合物級異戊二烯的技術可行性。 Global Bioenergies的工業異丁烯生產以及Insempra的2000萬美元資金籌措凸顯了投資者對可再生C5化學品日益成長的需求。成本持平預測表明,在預測期內,發酵製程的成本將接近石油路線,尤其是在生質乙醇過剩的地區。

原油原料價格波動擴大了生產商的淨利率。

煉油廠運轉率的波動會影響C5餾分油的供應,推高非一體化加工商的投入成本,並在原油價格高企時期擠壓利潤空間。雖然生物基路線價格穩定,但目前甘蔗衍生的C5餾分油價格比化石燃料路線高出280%至752%,構成短期競爭挑戰。

細分市場分析

到2024年,聚合物級產品將佔總收益的62.95%,預計到2030年將以6.19%的複合年成長率成長。生產商正採用先進的聚合技術來實現低支化和高分子量,從而減少熱量積聚,並延長輪胎壽命。化學級產品繼續供應特定領域的中間體,但隨著汽車和醫療保健產業對聚合物一致性的日益重視,其市場佔有率正逐漸下降。外科器械對純度要求的不斷提高支撐了其高價,並使供應合約與週期性的汽車需求脫鉤。

區域分析

預計到2025年,亞太地區異戊二烯市場規模將達到21.5億美元,得益於其與汽車原始設備製造商(OEM)的地理位置接近,可節省運輸成本並增強區域供應安全。中國正透過加工技術的進步,縮小天然橡膠和合成橡膠之間的產能差距,進而投資實現彈性體自給自足。印度蓬勃發展的化學工業將擴大下游需求,而泰國的生物乙烯中心將為可再生C5燃料的整合提供跳板。

北美製造商將生物聚合物產能擴大至每年26萬噸,反映出企業對永續輪胎和醫療設備的需求日益成長。歐盟的脫碳政策指導著對發酵和催化轉化平台的投資。加拿大衛生署的致癌性分類影響原料採購,原始設備製造商更傾向於選擇擁有完善安全通訊協定的供應商。隨著成本溢價的下降,南美的甘蔗價值鏈展現出戰略機會。中東的綜合設施將廉價的石腦油原料與出口物流連接起來,以供應非洲新興的汽車產業中心。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 電動車推動高性能輪胎用合成橡膠需求激增

- 投資生物基異戊二烯以降低石油基風險

- 醫療保健產業對超純聚異戊二烯醫療設備的需求不斷成長

- 亞太地區汽車產能擴張促進C5提取

- 在3D列印鞋中使用異戊二烯基熱可塑性橡膠

- 改用低氣味聚異戊二烯作為低VOC室內黏合劑

- 市場限制

- 原油價格波動導致生產商利潤率上升

- 加強異戊二烯單體(致癌性)職場接觸法規

- 發酵規模化瓶頸延緩了生物異戊二烯的商業化過程

- 來自銀膠菊和蒲公英橡膠替代品的競爭

- 價值鏈分析

- 五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 按年級

- 聚合物級

- 化學級

- 透過製造路線

- 石油化工C5分解

- 生物基發酵

- 生質乙醇的催化轉化

- 透過使用

- 胎

- 衛生保健

- 服飾和鞋類

- 其他用途

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略舉措

- 市佔率(%)/排名分析

- 公司簡介

- Braskem

- Chevron Phillips Chemical Company LLC.

- China Petrochemical Corporation

- ENEOS Corporation

- Exxon Mobil Corporation

- JSR Corporation

- Kraton Corporation

- KURARAY CO., LTD.

- LLC Tolyattikauchuk

- LOTTE Chemical CORPORATION

- LyondellBasell Industries Holdings BV

- PJSC SIBUR Holding

- Shell plc

- The Goodyear Tire & Rubber Company

- Zeon Corporation

第7章 市場機會與未來展望

The isoprene market is valued at USD 4.15 billion in 2025 and is forecast to reach USD 5.33 billion in 2030, reflecting a 5.12% CAGR over the period.

Growth is propelled by automakers' shift toward high-performance synthetic elastomers for electric-vehicle (EV) tires, expanding bio-based feedstock trials, and Asia-Pacific's dominance in manufacturing that supplies over half of global volumes. Polymer-grade materials retain a premium as tire manufacturers prioritize consistent cure rates, while healthcare demand for ultra-pure polyisoprene accelerates on the back of medical-device innovation. Bio-fermentation routes gain strategic importance as petrochemical producers hedge crude-oil volatility through renewable integration, supported by recent capital flows into fermentation start-ups. Competitive intensity rises as fermentation specialists and alternative-rubber innovators challenge conventional C5-cracking economics, nudging incumbents toward joint ventures and feedstock diversification.

Global Isoprene Market Trends and Insights

EV-Led Surge in Synthetic-Rubber Demand for High-Performance Tires

Higher torque loads in EVs mandate polymers with superior tensile strength and reduced rolling resistance, directing tire makers toward consistent isoprene formulations that natural rubber cannot guarantee. The US EPA notes over 3 billion tires produced annually, with EV-specific compounds requiring enhanced durability for battery-range preservation. Michelin's exploration of bio-based synthetic rubber underscores the redesign imperative facing tire compounds. Asia-Pacific's EV manufacturing concentration magnifies regional pull for isoprene, thereby sustaining a structural uplift in demand beyond the typical replacement cycle.

Investments in Bio-Based Isoprene Routes to Cut Petro-Feedstock Risk

Fermentation technologies such as IFPEN's Atol and the BioButterfly project confirm the technical feasibility of converting renewable ethanol into polymer-grade isoprene. Global Bioenergies' industrial isobutene output and Insempra's USD 20 million funding round highlight the growing investor appetite for renewable C5 chemistry. Cost-parity forecasts indicate fermentation will approach petro-routes within the forecast window, particularly in regions with surplus bio-ethanol.

Crude-Oil Feedstock Price Volatility Widening Producer Margins

Refinery utilization swings alter C5 fraction availability, pushing input costs higher for non-integrated processors and squeezing margins during crude-price spikes. Although bio-based routes offer price stability, current sugarcane-derived options command premiums between 280% and 752% over fossil routes, challenging near-term competitiveness.

Other drivers and restraints analyzed in the detailed report include:

- Rising Healthcare Demand for Ultra-Pure Polyisoprene Medical Devices

- Asia-Pacific Automotive Capacity Expansion Boosting C5 Extraction

- Stricter Workplace Exposure Limits for Isoprene Monomer (Carcinogen)

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polymer grade commanded 62.95% of 2024 revenue and is forecast to advance at 6.19% CAGR to 2030, mirroring demand for uniform cure rates in EV tires. Producers deploy advanced polymerization to achieve lower branching and higher molecular weights that curb heat build-up, benefiting tire longevity. Chemical grade continues serving niche intermediates but faces gradual share erosion as automotive and healthcare sectors value polymer consistency. Elevated purity requirements for surgical devices sustain premium pricing and insulate supply contracts from cyclical auto demand.

The Isoprene Market Report is Segmented by Grade (Polymer Grade and Chemical Grade), Production Route (Petrochemical C5 Cracking, Bio-Based Fermentation, and Catalytic Conversion of Bio-Ethanol), Application (Tyres, Healthcare, Apparels and Footwear, and Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific's isoprene market size hit USD 2.15 billion in 2025, and proximity to automotive OEMs offers freight savings that strengthen regional supply stability. China invests in elastomer self-sufficiency through processing advancements that bridge natural and synthetic rubber capability gaps. India's chemical-industrial growth broadens downstream demand, while Thailand's bio-ethylene hub creates a springboard for renewable C5 integration.

North American producers expand bio-polymer capacity to 260 kt per year, reflecting corporate attention to consumer pressure for sustainable tires and medical devices. The European Union's decarbonization policies steer investment toward fermentation and catalytic conversion platforms. Health Canada's carcinogen classification influences procurement, prompting OEMs to favor suppliers with robust safety protocols. South America's sugarcane value chain presents a strategic opportunity once cost premiums shrink. Middle Eastern complexes bundle inexpensive Naphtha feed with export logistics that reach Africa's emerging automotive hubs, while African demand growth hinges on vehicle assembly expansion and infrastructure improvement.

- Braskem

- Chevron Phillips Chemical Company LLC.

- China Petrochemical Corporation

- ENEOS Corporation

- Exxon Mobil Corporation

- JSR Corporation

- Kraton Corporation

- KURARAY CO., LTD.

- LLC Tolyattikauchuk

- LOTTE Chemical CORPORATION

- LyondellBasell Industries Holdings B.V.

- PJSC SIBUR Holding

- Shell plc

- The Goodyear Tire & Rubber Company

- Zeon Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 EV-led surge in synthetic-rubber demand for high-performance tyres

- 4.2.2 Investments in bio-based isoprene routes to cut petro-feedstock risk

- 4.2.3 Rising healthcare demand for ultra-pure polyisoprene medical devices

- 4.2.4 Asia-Pacific automotive capacity expansion boosting C5 extraction

- 4.2.5 3-D-printed footwear adopting isoprene-based thermoplastic elastomers

- 4.2.6 Low-VOC interior adhesives shifting towards low-odor polyisoprene

- 4.3 Market Restraints

- 4.3.1 Crude-oil feedstock price volatility widening producer margins

- 4.3.2 Stricter workplace exposure limits for isoprene monomer (carcinogen)

- 4.3.3 Fermentation scale-up bottlenecks delaying commercial BioIsoprene

- 4.3.4 Competition from guayule & dandelion natural-rubber alternatives

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size & Growth Forecasts (Value)

- 5.1 By Grade

- 5.1.1 Polymer Grade

- 5.1.2 Chemical Grade

- 5.2 By Production Route

- 5.2.1 Petrochemical C5 Cracking

- 5.2.2 Bio-based Fermentation

- 5.2.3 Catalytic Conversion of Bio-Ethanol

- 5.3 By Application

- 5.3.1 Tyres

- 5.3.2 Heathcare

- 5.3.3 Apparels and Footwear

- 5.3.4 Other Applications

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Braskem

- 6.4.2 Chevron Phillips Chemical Company LLC.

- 6.4.3 China Petrochemical Corporation

- 6.4.4 ENEOS Corporation

- 6.4.5 Exxon Mobil Corporation

- 6.4.6 JSR Corporation

- 6.4.7 Kraton Corporation

- 6.4.8 KURARAY CO., LTD.

- 6.4.9 LLC Tolyattikauchuk

- 6.4.10 LOTTE Chemical CORPORATION

- 6.4.11 LyondellBasell Industries Holdings B.V.

- 6.4.12 PJSC SIBUR Holding

- 6.4.13 Shell plc

- 6.4.14 The Goodyear Tire & Rubber Company

- 6.4.15 Zeon Corporation

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-needs assessment

- 7.2 Introducing New Manufacturing Techniques to Reduce Hazardous Waste