|

市場調查報告書

商品編碼

1846189

導電聚合物:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)Conductive Polymers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

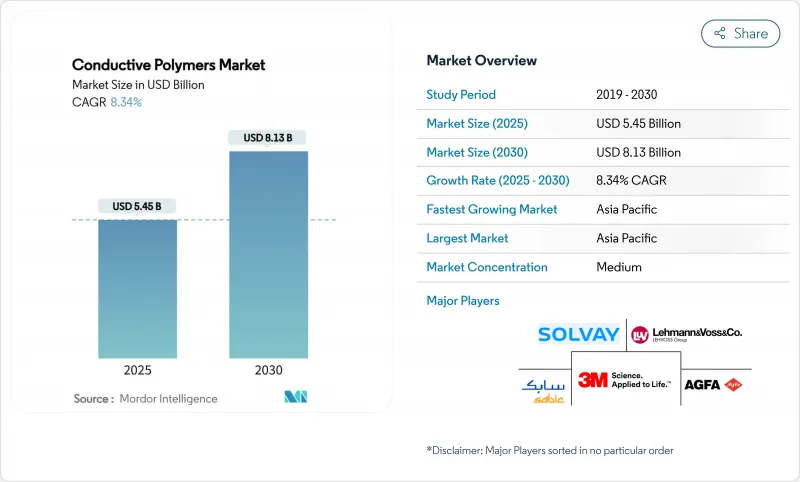

預計到 2025 年,導電聚合物市場規模將達到 54.5 億美元,到 2030 年將達到 81.3 億美元,預測期(2025-2030 年)複合年成長率為 8.34%。

導電聚合物市場的成長主要得益於下一代電子產品中金屬導體向輕質聚合物的轉變、汽車電氣化以及軟性設備的快速普及。汽車製造商正用聚合物取代金屬電磁干擾屏蔽層以提升續航里程,而電子產品品牌則在不犧牲訊號完整性的前提下,優先考慮更小的外形規格。導電聚合物的研發創新使其電導率提升至 4000 S/cm 以上,同時保持了柔韌性,這縮短了研發週期,並促使設計工程師更早地指定使用導電聚合物。同時,亞太地區的供應鏈在地化努力,以及政府對電動車的激勵措施,正在鞏固該地區在生產和消費方面的領先地位。儘管原料價格有所波動,但這些市場促進因素共同推動導電聚合物市場保持了穩健的成長動能。

全球導電聚合物市場趨勢與洞察

電動車和家用電器對輕型電磁干擾屏蔽的需求正在迅速成長。

電動車產生的電磁干擾比內燃機汽車更高。傳統的金屬屏蔽會增加重量並縮短續航里程,因此,原始設備製造商 (OEM) 開始採用輕質導電聚合物,這種材料可以在保持相當屏蔽效果的同時,將組件重量減輕高達 28%。在智慧型手機中,5G 電路靠近天線,因此製造商選擇使用聚合物屏蔽,這樣可以在不影響訊號品質的前提下,實現更薄的設備外殼。亞太地區將從中受益最多,因為該地區擁有全球大部分電動車電池和行動電話組裝線。歐洲汽車製造商也正在採用類似的解決方案來滿足車輛排放目標。為消費性電子設備創建的設計庫現在正被移植到汽車平台,加速了跨產業的應用。

電子商務促使防靜電包裝廣泛應用。

線上履約中心每年運送數十億件電子設備,增加了對防靜電包裝的需求。物流供應商報告稱,採用聚合物內襯的郵寄包裝後,靜電相關的退貨率降低了37%,這推動了北美地區的需求,該地區的小包裹量持續成長。物流地區的出口商也正在採用此類方法以滿足買家的特定要求,進一步擴大了導電聚合物的市場。

加工成本高,機械強度有限

在聚合物中實現金屬般的導電性通常需要酸洗和溶劑交換等後處理步驟,與傳統塑膠相比,這會使製造成本增加高達23%。機械疲勞仍然是一個挑戰,因為重摻雜結構在反覆彎曲下容易開裂。雖然汽車製造商會指定添加增強添加劑,但這會增加重量並抵消部分優勢。研究團隊正在探索將導電區域封裝在彈性體基體中以平衡性能,但大規模應用取決於成本降低藍圖。

細分市場分析

到2024年,導電塑膠將佔導電聚合物市場45.25%的佔有率,因為擠出和射出成型成型設備已完成折舊,且經濟高效的千噸級生產成為可能。這些聚合物符合筆記型電腦機殼和汽車感測器支架的電磁干擾(EMI)標準,從而支持其在成熟應用領域的拓展。穿戴式醫療設備和共形天線需要高導電率,因此到2030年,導電聚合物將以8.77%的複合年成長率(CAGR)實現最快成長。氣相聚合等創新加工技術降低了缺陷密度,縮小了與金屬的性能差距。

固有耗散性聚合物在工廠車間和半導體生產線上佔有一席之地,其快速的靜電釋放可防止微損傷。其他類型的聚合物包括將奈米碳填料與熱塑性聚氨酯結合的混合複合材料,這種材料可製成可拉伸電路。持續的改進表明,導電聚合物市場將逐漸從一般塑膠塑膠轉向更高價值的ICP配方,同時保持對價格敏感的廣泛應用。

由於其可靠的合成通訊協定和在環境條件下的穩定性,共軛導電聚合物預計將在 2024 年佔據導電聚合物市場 40.66% 的佔有率。它們可用作顯示器中的透明電極和用於照護現場診斷的有機電化學電晶體中的活性層。

儘管離子導電聚合物的基數較小,但其複合年成長率仍將達到9.01%。這是因為它們同時具有電子和離子電荷,使其成為生物界面和固態電池的關鍵材料。電荷轉移聚合物可用於需要特定氧化還原電位的感測器。在對導電性要求不高的防靜電托盤中,導電填充聚合物仍具有成本競爭力。

導電聚合物報告按聚合物類型(固有導電聚合物、固有耗散聚合物、其他)、類別(共軛導電聚合物、電荷轉移聚合物、其他)、應用(產品組件、防靜電包裝、物料輸送、其他)、最終用途行業(電氣和電子、汽車和電動交通、其他)以及地區(亞太地區、北美、其他)進行細分。

區域分析

亞太地區預計到2024年將佔據導電聚合物市場46.11%的佔有率,並在2030年之前以9.34%的複合年成長率成長,這主要得益於密集的電子製造群和政府對電動車的補貼。中國是組裝和電動車電池組的主要生產國,而日本則在高純度聚合物的研發方面處於領先地位。

在北美,美國正透過聯邦稅收優惠政策刺激國內電動車生產,從而提振對輕量屏蔽組件的需求。國防開支正資助共形天線項目,該項目指定使用特殊的導電聚合物。加拿大航太業正將可拉伸電路應用於客艙安全系統,而墨西哥則透過出口電動車組裝來提升區域需求。促進跨境材料流動的貿易協定有助於維持市場的穩定性。

歐洲市場呈現穩定成長態勢,這得益於日益嚴格的車輛排放法規鼓勵輕量化設計。德國在高階電動車領域率先應用富含聚合物的電磁干擾(EMI)解決方案。法國航太業對用於機載天線的高性能材料需求旺盛。斯堪的納維亞半島的循環經濟計劃提倡使用可回收的導電塑膠。歐盟的REACH法規鼓勵採用低揮發性有機化合物(VOC)聚合物製程。東歐的電子產品製造地正在採用防靜電地板材料以滿足全球客戶的審核,從而擴大了該地區導電聚合物市場的規模。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 電動車和家用電器對輕型電磁干擾屏蔽的需求正在迅速成長。

- 電子商務促使防靜電包裝廣泛應用。

- 2025年以後軟性熱電穿戴裝置的應用

- 採用本徵導電聚合物(ICP)的軍用級共形天線

- 透過設計靈活性和客製化,蘊藏著巨大的創新和產品開發潛力。

- 市場限制

- 加工成本高,機械強度有限

- 苯胺和特殊單體價格不穩定

- 混合複合材料報廢回收面臨的挑戰

- 價值鏈分析

- 五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 按聚合物類型

- 本徵導電聚合物(ICPs)

- 固有耗散聚合物(IDP)

- 導電塑膠

- 其他聚合物類型

- 按班級

- 共軛導電聚合物

- 電荷轉移聚合物

- 離子導電聚合物

- 導電填充聚合物

- 透過使用

- 產品組件(EMI外殼、感測器等)

- 防靜電包裝

- 物料輸送(托盤、托特包)

- 工作檯面和地板材料

- 其他

- 按最終用戶產業

- 電氣和電子

- 汽車出行和電動交通

- 航太/國防

- 醫療保健穿戴式裝置

- 其他(工業包裝和物流)

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 北歐的

- 俄羅斯

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略舉措

- 市佔率分析

- 公司簡介

- 3M

- Agfa-Gevaert Group

- Arkema

- Cabot Corporation

- Celanese Corporation

- Covestro AG

- Dupont

- Eeonyx

- Heraeus Holding

- Lehmann&Voss&Co.

- Parker Hannifin Corp

- Parker Hannifin Corp.

- PolyOne Corporation

- Premix Group

- RTP Company

- SABIC

- Solvay

- The Lubrizol Corporation

- The Lubrizol Corporation

- Westlake Plastics

第7章 市場機會與未來展望

The Conductive Polymers Market size is estimated at USD 5.45 billion in 2025, and is expected to reach USD 8.13 billion by 2030, at a CAGR of 8.34% during the forecast period (2025-2030).

The expansion is underpinned by the shift from metal conductors to lightweight polymers in next-generation electronics, the electrification of vehicles, and the rapid adoption of flexible devices. Automakers are replacing metal EMI shields with polymer alternatives to extend driving range, while electronics brands prioritise form-factor reduction without sacrificing signal integrity. Processing innovations that raise conductivity beyond 4,000 S/cm and retain flexibility have shortened development cycles, encouraging design engineers to specify conductive polymers at an earlier stage. At the same time, supply-chain localisation efforts in Asia Pacific have combined with government incentives for electric mobility to reinforce regional leadership in production and consumption. The cumulative effect of these drivers places the conductive polymer market on a resilient growth path despite raw-material price swings.

Global Conductive Polymers Market Trends and Insights

Lightweight EMI-Shielding Demand Surging in EV and Consumer Electronics

Electric vehicles emit higher electromagnetic interference than internal-combustion cars. Traditional metal shields add weight that curtails range, prompting OEMs to specify lightweight conductive polymers, which cut component mass by up to 28% while achieving comparable shielding effectiveness. In smartphones, 5G circuitry sits closer to antennas; thus, manufacturers select polymer shields that thin device walls without compromising signal quality. Asia Pacific benefits most because it hosts the bulk of global EV battery and handset assembly lines. European automakers are adopting similar solutions to meet fleet-emission targets. Design libraries created for consumer devices now transfer to automotive platforms, accelerating cross-sector adoption.

E-Commerce-Driven Uptake of Antistatic Packaging

Online fulfilment centres ship billions of electronics each year, heightening the need for static-safe packaging. Logistics providers report 37% fewer static-related product returns after adopting polymer-lined mailers, boosting demand in North America, where parcel volumes continue to rise. Asia Pacific exporters replicate these practices to satisfy buyer specifications, further expanding the conductive polymer market.

High Processing Cost and Limited Mechanical Robustness

Achieving metal-like conductivity in polymers typically requires post-treatment steps such as acid washing or solvent exchange, which lift production costs by as much as 23% relative to conventional plastics. Mechanical fatigue remains a challenge because highly doped structures can crack under repeated flexing. Automakers specify reinforcement additives, but these raise weight and erase some advantages. Research groups are exploring elastomeric matrices that encapsulate conductive domains to balance properties, yet mass-scale adoption hinges on cost-down roadmaps.

Other drivers and restraints analyzed in the detailed report include:

- Flexible Thermoelectric Wearables Adoption Post-2025

- Military-Grade Conformal Antennas Using Inherently Conductive Polymers

- Volatile Aniline and Specialty Monomer Prices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Conductive plastics held 45.25% of the conductive polymer market size in 2024 because extrusion and injection-moulding assets are already amortised, allowing economic output at multi-kiloton scale. These polymers meet EMI standards for laptop housings and automotive sensor brackets, supporting expansion across mature applications. Inherently conductive polymers post the fastest 8.77% CAGR through 2030 as wearable healthcare devices and conformal antennas demand elevated conductivity per gram. Processing breakthroughs such as vapor-phase polymerisation lower defect density, narrowing the property gap with metals.

Inherently dissipative polymers maintain a niche in factory floors and semiconductor lines where rapid static bleed-off prevents micro-damage. Other polymer types include hybrid composites that marry nano-carbon fillers with thermoplastic polyurethane, enabling stretchable circuits. Continuous improvements suggest the conductive polymer market will gradually shift from commodity plastics toward higher-value ICP formulations while maintaining a broad base of price-sensitive applications.

Conjugated conducting polymers captured 40.66% of the conductive polymer market share in 2024 due to reliable synthesis protocols and stability under ambient conditions. They function as transparent electrodes in displays and as active layers in organic electrochemical transistors used for point-of-care diagnostics.

Despite their smaller base, ionically conducting polymers expand at a 9.01% CAGR because they carry both electronic and ionic charges, critical for biointerfaces and solid-state batteries. Charge-transfer polymers cater to sensors requiring specific redox potentials. Conductively filled polymers remain cost-competitive for antistatic trays where moderate conductivity suffices.

The Conductive Polymer Report is Segmented by Polymer Type (Inherently Conductive Polymers, Inherently Dissipative Polymers, and More), Class (Conjugated Conducting Polymers, Charge-Transfer Polymers, and More), Application (Product Components, Antistatic Packaging, Material Handling, and More), End-Use Industry (Electrical and Electronics, Automotive and E-Mobility, and More), and Geography (Asia-Pacific, North America, and More)

Geography Analysis

Asia Pacific held 46.11% share of the conductive polymer market in 2024 and is growing at a 9.34% CAGR through 2030, driven by its dense electronics manufacturing clusters and government subsidies for electric mobility. China commands bulk volume in smartphone assembly and EV battery packs, while Japan spearheads high-purity polymer research and development.

In North America the United States accelerates domestic EV production with federal tax incentives, creating upward demand for lightweight shield components. Defence spending channels funds into conformal antenna programmes that specify inherently conductive polymers. Canada's aerospace industry integrates stretchable circuits into cabin safety systems, while Mexico's EV assembly exports augment regional demand. Trade accords facilitating materials flow across borders support market coherence.

Europe exhibits steady uptake supported by stringent vehicle emission limits that reward weight reduction. Germany pioneers polymer-rich EMI solutions in premium EVs. France's aerospace sector demands high-performance grades for in-flight antennas. Nordic initiatives in circular economy favour recyclable conductive plastics. The EU's REACH framework incentivises low-VOC polymer processes. Eastern European electronics manufacturing hubs adopt antistatic flooring to meet global customer audits, expanding the conductive polymer market perimeter within the continent.

- 3M

- Agfa-Gevaert Group

- Arkema

- Cabot Corporation

- Celanese Corporation

- Covestro AG

- Dupont

- Eeonyx

- Heraeus Holding

- Lehmann&Voss&Co.

- Parker Hannifin Corp

- Parker Hannifin Corp.

- PolyOne Corporation

- Premix Group

- RTP Company

- SABIC

- Solvay

- The Lubrizol Corporation

- The Lubrizol Corporation

- Westlake Plastics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Lightweight EMI-Shielding Demand Surging in EV And Consumer Electronics

- 4.2.2 E-Commerce-Driven Uptake of Antistatic Packaging

- 4.2.3 Flexible Thermoelectric Wearables Adoption Post-2025

- 4.2.4 Military-Grade Conformal Antennas Using Inherently Conductive Polymers (ICPs)

- 4.2.5 Design Flexibility and Huge Scope of Innovation and Product Development Through Customization

- 4.3 Market Restraints

- 4.3.1 High Processing Cost and Limited Mechanical Robustness

- 4.3.2 Volatile Aniline and Specialty Monomer Prices

- 4.3.3 End-Of-Life Recycling Challenges of Hybrid Composites

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Polymer Type

- 5.1.1 Inherently Conductive Polymers (ICPs)

- 5.1.2 Inherently Dissipative Polymers (IDPs)

- 5.1.3 Conductive Plastics

- 5.1.4 Other Polymer Types

- 5.2 By Class

- 5.2.1 Conjugated Conducting Polymers

- 5.2.2 Charge-Transfer Polymers

- 5.2.3 Ionically Conducting Polymers

- 5.2.4 Conductively Filled Polymers

- 5.3 By Application

- 5.3.1 Product Components (e.g., EMI housings, sensors)

- 5.3.2 Antistatic Packaging

- 5.3.3 Material Handling (trays, totes)

- 5.3.4 Work-surface and Flooring

- 5.3.5 Others

- 5.4 By End-user Industry

- 5.4.1 Electrical and Electronics

- 5.4.2 Automotive and E-Mobility

- 5.4.3 Aerospace and Defense

- 5.4.4 Healthcare and Wearables

- 5.4.5 Others (Industrial Packaging and Logistics)

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 NORDIC

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 South Africa

- 5.5.5.4 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 3M

- 6.4.2 Agfa-Gevaert Group

- 6.4.3 Arkema

- 6.4.4 Cabot Corporation

- 6.4.5 Celanese Corporation

- 6.4.6 Covestro AG

- 6.4.7 Dupont

- 6.4.8 Eeonyx

- 6.4.9 Heraeus Holding

- 6.4.10 Lehmann&Voss&Co.

- 6.4.11 Parker Hannifin Corp

- 6.4.12 Parker Hannifin Corp.

- 6.4.13 PolyOne Corporation

- 6.4.14 Premix Group

- 6.4.15 RTP Company

- 6.4.16 SABIC

- 6.4.17 Solvay

- 6.4.18 The Lubrizol Corporation

- 6.4.19 The Lubrizol Corporation

- 6.4.20 Westlake Plastics

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

- 7.2 Growth in smart textiles and IoT devices fuels need for flexible, conductive materials.

導電聚合物市場:按類型、導電材料、形態、等級、製造技術、應用和最終用途產業分類-2026-2032年全球市場預測

導電聚合物市場:按類型、導電材料、形態、等級、製造技術、應用和最終用途產業分類-2026-2032年全球市場預測 全球導電聚合物市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球導電聚合物市場規模、佔有率、趨勢和成長分析報告(2026-2034) 2026年全球導電聚合物市場報告

2026年全球導電聚合物市場報告 導電聚合物市場-全球產業規模、佔有率、趨勢、機會及按類型、應用、地區和競爭格局分類的預測(2021-2031年)導電聚合物鉭固體電容器市場(依最終用途產業、應用、容量、額定電壓和封裝分類),全球預測(2026-2032年)石墨聚四氟乙烯絲填料市場按材料類型、應用、終端用戶產業、形式和銷售管道分類-2026-2032年全球預測

導電聚合物市場-全球產業規模、佔有率、趨勢、機會及按類型、應用、地區和競爭格局分類的預測(2021-2031年)導電聚合物鉭固體電容器市場(依最終用途產業、應用、容量、額定電壓和封裝分類),全球預測(2026-2032年)石墨聚四氟乙烯絲填料市場按材料類型、應用、終端用戶產業、形式和銷售管道分類-2026-2032年全球預測 導電聚合物市場預測至2032年:按產品類型、導電機制、應用、最終用戶和地區分類的全球分析

導電聚合物市場預測至2032年:按產品類型、導電機制、應用、最終用戶和地區分類的全球分析 導電聚合物市場規模、佔有率及成長分析(按類型及地區分類)-2026-2033年產業預測

導電聚合物市場規模、佔有率及成長分析(按類型及地區分類)-2026-2033年產業預測 石墨烯增強導電聚合物市場規模、佔有率和趨勢分析報告:按產品、應用、地區和細分市場預測(2025-2033 年)離子導電聚合物市場規模、佔有率和趨勢分析報告:按產品、應用、地區和細分市場預測(2025-2033 年)

石墨烯增強導電聚合物市場規模、佔有率和趨勢分析報告:按產品、應用、地區和細分市場預測(2025-2033 年)離子導電聚合物市場規模、佔有率和趨勢分析報告:按產品、應用、地區和細分市場預測(2025-2033 年)