|

市場調查報告書

商品編碼

1846184

熱噴塗塗層:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)Thermal Spray Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

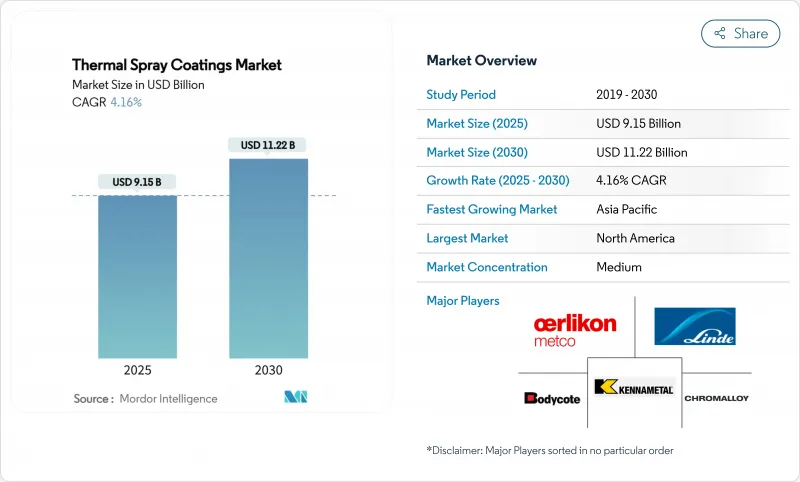

預計到 2025 年,熱噴塗塗層市場規模將達到 91.5 億美元,到 2030 年將達到 112.2 億美元,預測期(2025-2030 年)複合年成長率為 4.16%。

推動市場需求的因素包括:可延長零件壽命的混合積層製造+噴塗修復方法;需要生物活性表面的醫療應用不斷擴展;以及依賴先進隔熱層來應對引擎溫度上升的航太項目。數位化「智慧」噴塗單元正在增強製程控制並縮短開發週期。從區域來看,亞太地區的生產能力提升正在縮小與北美的差距,而美國更嚴格的VOC法規正在加速向低排放氣體的電能熱噴塗製程轉型。

全球熱噴塗塗層市場趨勢與洞察

在醫療植入和義肢的應用日益廣泛

醫用級等離子噴塗羥基磷灰石仍然是目前唯一獲得FDA批准用於大規模生產的整形外科植入物的塗層技術,而近期使用B相鈦合金的研究表明,其與骨骼的模量差異較小。高功率脈衝磁控濺鍍和高速火焰噴塗(HVOF)技術正被結合到層狀結構中,以提供抗菌表面,同時又不影響骨整合。隨著3D列印晶格植入物的規模化應用,噴塗生物陶瓷塗層使得客製化幾何形狀的植入物能夠更快地通過認證,儘管監管機構仍在最終確定測試通訊協定。能夠證明其表面粗糙度和相組成可重複性的塗層供應商正在贏得新的多年供應合約。

在航太渦輪機和機身部件中的應用日益廣泛

引擎預熱階段不斷提高渦輪進口溫度,對智慧工廠提出了更高的要求,即每個試樣的厚度範圍必須更嚴格。歐瑞康和MTU航空引擎公司開發的數位化噴塗單元採用閉合迴路流診斷技術,可將返工率降低25%。冷噴塗已成為領先的維修技術,能夠修復鋁製飛行控制殼體和鎂製齒輪箱蓋,而不會因熱效應而變形。具有抗氧化中階延長了引擎大修時間,使航空公司能夠延長窄體飛機的服役時間。

塗層品質問題的可靠性和可重複性

大型原始設備製造商 (OEM) 目前規定的統計製程窗口,小型製造工廠難以滿足。顆粒尺寸變化、羽流動力學和基材預熱都會影響氧化物含量和孔隙率,進而影響使用過程中的磨損。自動化視覺和線上聲波感測器有助於檢測超出規格的情況,但對於小批量應用而言,整合成本仍然很高。由於缺乏即時監控的全球標準,認證週期很長,尤其是在航太和醫療設備專案中。

細分市場分析

到2024年,陶瓷氧化物將佔總收入的30.15%,並以5.12%的複合年成長率快速成長。這一優勢源於其卓越的高溫穩定性和生物相容性,使氧化物成為渦輪機、醫療和氫能基礎設施計劃的首選材料。碳化物混合物則適用於石油和天然氣閥門以及採礦工具等極端磨損應用。鎳鉻鉬合金等金屬有助於防止海洋結構腐蝕,而聚合物基覆層則應用於介電性能至關重要的電子領域。懸浮等離子噴塗法製備的奈米結構氧化物可提高熱循環壽命,為未來的推進系統架構釋放。將稀土元素摻雜氧化鋯與功能梯度黏結層結合的製造商,如今宣稱其產品具有5萬小時的耐久性保證,從而將熱噴塗塗層市場從防護提升至性能。

新型粉末霧化技術也降低了碳化鎢供應風險。一些亞洲鋼廠已開始將硬質合金廢料回收製成團聚碳化鎢鈷原料,從而減少了對中國原生鎢的依賴。同時,混合放電等離子燒結棒材的出現拓寬了原料選擇範圍。這些轉變透過降低原料成本波動性並為局部粉末中心的發展打開大門,從而增強了熱噴塗市場。

區域分析

北美擁有成熟的航太、國防和醫療設備生態系統,預計2024年將以34.27%的收入佔比領先。獲得美國聯邦航空管理局(FAA)認證的維修店正在使用冷噴塗技術將材料重新黏合到鎂合金齒輪箱上,避免了昂貴的零件更換。儘管加州的空氣品質檢測對合規性造成了不確定性,但該地區在智慧噴塗單元方面的先發優勢應該會使其在整個預測期內保持領先地位。

由於汽車電氣化、消費性電子產品產能和燃氣燃氣渦輪機建設的快速擴張,亞太地區預計將以6.21%的複合年成長率實現快速成長。中國粉末回收企業已開始向當地塗料公司供應碳化物原料,以規避美國地質調查局(USGS)指出的鎢礦風險。日本半導體工廠正在擴大用於5奈米以下蝕刻腔的耐等離子氧化鋁塗層的生產規模,而印度鐵路公司則指定在高速鐵路軌道部件上使用電弧噴塗鋼板。這些計劃表明,熱噴塗市場已滲透到該地區製造業的各個環節。

在歐洲,更嚴格的VOC(揮發性有機化合物)法規正推動閉迴路等離子噴塗室和水性黏合劑的普及,並展現出穩定的進展。北海離岸風力發電電場目前指定在單樁內部噴塗鋁鋅熱噴塗犧牲陽極,從而將其使用壽命延長至25年或更久。歐盟委員會的「Fit-for-55」計畫間接促進了對工業燃氣渦輪機高效阻隔塗層的需求。儘管在中東和非洲,此類塗層仍處於小眾市場,但隨著煉油廠維修和海水淡化廠尋求持久的防腐蝕保護層,預計未來需求將會增加。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 在醫療植入和義肢的應用日益廣泛

- 在航太渦輪機和機身部件中的應用日益廣泛

- 人們越來越偏好選擇陶瓷氧化物阻隔塗層

- 用於電動車零件的冷噴塗電磁干擾屏蔽

- 超合金零件的積層製造修復

- 市場限制

- 塗層品質問題的可靠性和可重複性

- 更嚴格的VOC/粉塵排放法規

- 關鍵粉末(碳化鎢、稀有碳化物)供應波動

- 價值鏈分析

- 五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 粉末塗料

- 陶瓷氧化物

- 碳化物

- 金屬

- 聚合物和其他材料

- 透過流程

- 燃燒

- 電能

- 按最終用戶產業

- 航太

- 工業用燃氣渦輪機

- 車

- 電子設備

- 醫療設備

- 能源和電力

- 石油和天然氣

- 其他(紙漿和造紙、採礦等)

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略舉措

- 市佔率分析

- 公司簡介

- Abakan Inc.

- APS Materials Inc.

- Bodycote

- Chromalloy Gas Turbine LLC

- Curtiss-Wright Corporation(FW Gartner)

- Fisher Barton

- Flame Spray Technologies BV

- Hannecard Roller Coatings, Inc-ASB Industries

- Kennametal Inc.

- Linde

- OC Oerlikon Management AG

- Steel Goode Products, LLC

- Sulzer Ltd

- Thermion

- Tocalo Co. Ltd.

- TST LLC

第7章 市場機會與未來展望

The Thermal Spray Coatings Market size is estimated at USD 9.15 billion in 2025, and is expected to reach USD 11.22 billion by 2030, at a CAGR of 4.16% during the forecast period (2025-2030).

Demand is fueled by hybrid additive-plus-spray repair methods that extend component life, widening medical applications that require bio-active surfaces, and aerospace programs that rely on advanced thermal-barrier stacks for higher engine temperatures. Growth also reflects rising adoption of cold-spray EMI shielding in e-mobility electronics, while digitalized "smart" spray cells are tightening process control and shortening development cycles. Regionally, Asia-Pacific's manufacturing build-out is closing the gap with North America, even as tightening VOC rules in the United States accelerate the shift to low-emission electric-energy spray routes.

Global Thermal Spray Coatings Market Trends and Insights

Increased Usage in Medical Implants and Prosthetics

Medical-grade plasma-sprayed hydroxyapatite continues to be the only FDA-cleared coating technology for mass-produced orthopedic implants, and recent work with B-phase Ti alloys is reducing elastic-modulus mismatch to bone. High-power impulse magnetron sputtering and HVOF overlays are now being combined in layered constructs that supply antibacterial surfaces without compromising osseointegration. As 3-D printed lattice implants scale up, spray-applied bio-ceramic finishes allow patient-specific geometries to move through qualification more quickly, though regulators are still finalizing test protocols. Coating providers able to certify repeatable roughness and phase composition are winning new multi-year supply contracts.

Growing Adoption in Aerospace Turbine & Air-Frame Parts

Engine primes are raising turbine inlet temperatures and demanding smart factories that deliver tight thickness windows on every coupon. Digitalized spray cells developed by Oerlikon and MTU Aero Engines now employ closed-loop plume diagnostics that cut rework rates by 25%. Cold-spray has become a frontline depot-repair tool, allowing aluminum flight-control housings and magnesium gearbox covers to be rebuilt without heat-affected distortion. Multilayer ceramic-oxide barrier stacks with oxidation-resistant inter-layers are extending engine overhaul intervals, enabling airlines to keep narrow-body fleets in service longer.

Reliability & Coating-Quality Repeatability Issues

Large OEMs now specify statistical process windows that smaller job shops struggle to meet. Particle size variance, plume dynamics, and substrate pre-heat all influence oxide content and porosity, which in turn dictate in-service wear. Automated vision and inline acoustic sensors are helping detect off-nominal conditions, but integration costs remain high for low-volume applications. Without global standards on real-time monitoring, qualification cycles lengthen, especially in aerospace and medical device programs.

Other drivers and restraints analyzed in the detailed report include:

- Rising Preference for Ceramic-Oxide Barrier Coatings

- Cold-Spray EMI Shielding for E-Mobility Components

- Tightening VOC / Dust-Emission Regulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Ceramic oxides recorded 30.15% of 2024 revenue and will grow fastest at 5.12% CAGR. This dominance arises from outstanding high-temperature stability and bio-compatibility, making oxides the default for turbine, medical, and hydrogen infrastructure projects. Carbide blends follow for extreme wear tasks on oil-and-gas valves and mining tools. Metals such as Ni-Cr-Mo alloys serve corrosion defense of marine structures, while polymer-based overlays target electronics where dielectric properties matter. Nanostructured oxides fabricated via suspension plasma spray tighten thermal-cycling life and are unlocking future propulsion architectures. Manufacturers combining rare-earth-doped zirconia with functionally graded bond coats now market 50 000-hour durability guarantees, lifting the thermal spray coating market perception from protective to performance-enabling.

New powder atomization methods are also trimming tungsten carbide supply risk. Several Asian plants have begun recycling hard-metal scrap into agglomerated WC-Co feedstock, lessening exposure to Chinese primary tungsten. At the same time, hybrid spark-plasma-sintered rod stock is widening the choice of feed materials. These shifts will strengthen the thermal spray coating market by easing raw-material cost swings and opening the door to localized powder hubs.

The Thermal Spray Coating Market Report is Segmented by Powder Coating Materials (Ceramic Oxides, Carbides, Metals, Polymers & Other Materials), Process (Combustion, Electric Energy), End-User Industry (Aerospace, Industrial Gas Turbines, Automotive, Electronics, Medical Devices, and More), and Geography (Asia-Pacific, North America, Europe, South America, , and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America led with 34.27% revenue in 2024 on the back of entrenched aerospace, defense, and medical device ecosystems. FAA-class repair shops now rely on cold-spray to redeposit material on magnesium gearboxes, avoiding costly part replacement, while the Department of Energy funds oxide-coating research for hydrogen-ready turbines. California's air-quality probes add compliance uncertainty, but the region's first-mover advantage in smart spray cells should preserve leadership during the forecast window.

Asia-Pacific is projected to grow fastest at 6.21% CAGR as automotive electrification, consumer-electronics capacity, and gas-turbine build-outs surge. Chinese powder recyclers already supply carbide feedstock to local coaters, hedging tungsten risks identified by USGS. Japanese semiconductor plants are scaling plasma-resistant alumina coatings for sub-5 nm etch chambers, while Indian railways specify arc-sprayed steel overlays on high-speed track components. These projects illustrate how the thermal spray coating market is embedding itself across the region's manufacturing spectrum.

Europe shows steady progress as tougher VOC caps push operators toward closed-loop plasma booths and water-borne binders. Offshore wind farms in the North Sea now specify Al-Zn thermally sprayed sacrificial anodes on monopile interiors, lengthening service life beyond 25 years. The European Commission's "Fit-for-55" package indirectly boosts demand for efficiency-raising barrier coatings on industrial gas turbines. Middle East and Africa remain niche today but will see higher uptake as refinery revamps and desalination plants pursue long-life corrosion shields.

- Abakan Inc.

- APS Materials Inc.

- Bodycote

- Chromalloy Gas Turbine LLC

- Curtiss-Wright Corporation (FW Gartner)

- Fisher Barton

- Flame Spray Technologies BV

- Hannecard Roller Coatings, Inc - ASB Industries

- Kennametal Inc.

- Linde

- OC Oerlikon Management AG

- Steel Goode Products, LLC

- Sulzer Ltd

- Thermion

- Tocalo Co. Ltd.

- TST LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increased usage in medical implants & prosthetics

- 4.2.2 Growing adoption in aerospace turbine & air-frame parts

- 4.2.3 Rising preference for ceramic-oxide barrier coatings

- 4.2.4 Cold-spray EMI shielding for e-mobility components

- 4.2.5 Additive-manufacturing repair of super-alloy parts

- 4.3 Market Restraints

- 4.3.1 Reliability & coating-quality repeatability issues

- 4.3.2 Tightening VOC / dust-emission regulations

- 4.3.3 Critical-powder supply volatility (WC, rare carbides)

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size & Growth Forecasts (Value)

- 5.1 By Powder Coating Materials

- 5.1.1 Ceramic Oxides

- 5.1.2 Carbides

- 5.1.3 Metals

- 5.1.4 Polymers & Other Materials

- 5.2 By Process

- 5.2.1 Combustion

- 5.2.2 Electric Energy

- 5.3 By End-user Industry

- 5.3.1 Aerospace

- 5.3.2 Industrial Gas Turbines

- 5.3.3 Automotive

- 5.3.4 Electronics

- 5.3.5 Medical Devices

- 5.3.6 Energy and Power

- 5.3.7 Oil and Gas

- 5.3.8 Others (Pulp and Paper, Mining, etc.)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 Abakan Inc.

- 6.4.2 APS Materials Inc.

- 6.4.3 Bodycote

- 6.4.4 Chromalloy Gas Turbine LLC

- 6.4.5 Curtiss-Wright Corporation (FW Gartner)

- 6.4.6 Fisher Barton

- 6.4.7 Flame Spray Technologies BV

- 6.4.8 Hannecard Roller Coatings, Inc - ASB Industries

- 6.4.9 Kennametal Inc.

- 6.4.10 Linde

- 6.4.11 OC Oerlikon Management AG

- 6.4.12 Steel Goode Products, LLC

- 6.4.13 Sulzer Ltd

- 6.4.14 Thermion

- 6.4.15 Tocalo Co. Ltd.

- 6.4.16 TST LLC

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

熱噴塗市場:按製程、材料、應用和最終用途產業分類-2026-2032年全球市場預測

熱噴塗市場:按製程、材料、應用和最終用途產業分類-2026-2032年全球市場預測 熱噴塗塗層市場規模、佔有率、趨勢和預測:按產品、技術、應用和地區分類,2026-2034年熱噴塗設備及服務市場:依產品、技術、製程及終端應用產業分類-2026-2032年全球預測熱噴塗粉末市場:依材料類型、塗覆製程、塗層功能及最終用途產業分類-2026-2032年全球預測日本熱噴塗塗料市場報告:按產品、技術、應用和地區分類(2026-2034年)

熱噴塗塗層市場規模、佔有率、趨勢和預測:按產品、技術、應用和地區分類,2026-2034年熱噴塗設備及服務市場:依產品、技術、製程及終端應用產業分類-2026-2032年全球預測熱噴塗粉末市場:依材料類型、塗覆製程、塗層功能及最終用途產業分類-2026-2032年全球預測日本熱噴塗塗料市場報告:按產品、技術、應用和地區分類(2026-2034年) 熱噴塗塗層市場規模、佔有率和趨勢分析報告:按材料、技術、應用、地區和細分市場預測(2026-2033 年)

熱噴塗塗層市場規模、佔有率和趨勢分析報告:按材料、技術、應用、地區和細分市場預測(2026-2033 年) 熱噴塗塗層市場-全球產業規模、佔有率、趨勢、機會和預測,依材料、最終用戶、地區和競爭格局分類,2020-2030年預測

熱噴塗塗層市場-全球產業規模、佔有率、趨勢、機會和預測,依材料、最終用戶、地區和競爭格局分類,2020-2030年預測 熱噴塗塗料市場,按產品類型、按技術、按應用、按國家和地區 - 2025 年至 2032 年全球行業分析、市場規模、市場佔有率和預測

熱噴塗塗料市場,按產品類型、按技術、按應用、按國家和地區 - 2025 年至 2032 年全球行業分析、市場規模、市場佔有率和預測 熱噴塗塗層市場:按材料、製程、應用和地區分類

熱噴塗塗層市場:按材料、製程、應用和地區分類 熱噴塗塗料市場規模、佔有率和成長分析(按工藝、材料、技術、最終用途行業和地區)- 2025-2032 年行業預測

熱噴塗塗料市場規模、佔有率和成長分析(按工藝、材料、技術、最終用途行業和地區)- 2025-2032 年行業預測