|

市場調查報告書

商品編碼

1846159

指紋模組:市場佔有率分析、產業趨勢、統計數據、成長預測(2025-2030 年)Fingerprint Module - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

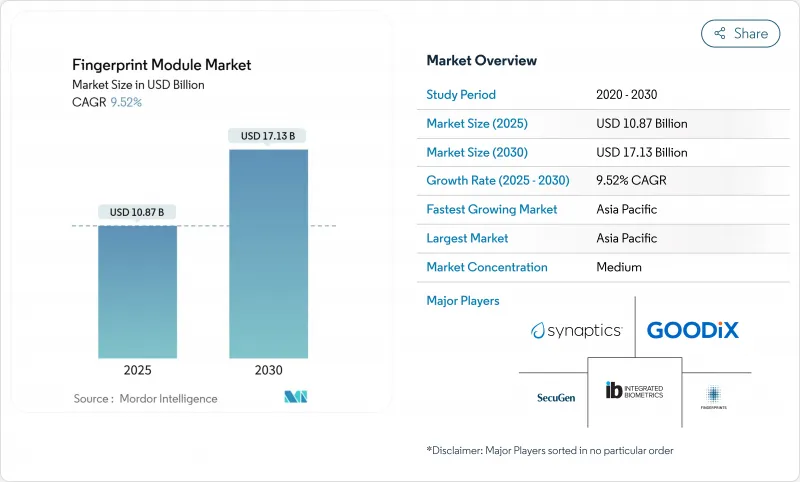

預計到 2025 年,指紋模組市場規模將達到 108.7 億美元,到 2030 年將達到 171.3 億美元,複合年成長率為 9.52%。

這一成長動能主要得益於主權數位身分計劃、智慧型手機認證技術的快速升級以及生物辨識支付卡的商業化部署。儘管電容式感測器仍佔據大部分市場佔有率,但隨著高階設備對更高防偽性能的需求,超音波技術正以最快的速度擴張。系統晶片(SoC) 整合降低了設備尺寸和物料清單 (BOM) 成本,而屏下模組則有助於推動無邊框設備設計。在亞太地區政府專案的大批量採購、平均售價下降以及汽車行業的廣泛應用等因素的共同推動下,指紋模組市場保持著多年的成長動能。

全球指紋模組市場趨勢與洞察

政府生物辨識身分識別大型企劃激增

大規模國家身分識別計畫正在重塑基礎需求。衣索比亞的「法伊達」(Fayda)計畫獲得了3.5億美元的多邊資金支持,目標是在2030年前為9,000萬人註冊。奈及利亞耗資4.3億美元的數位身分識別計劃旨在為超過2億公民提供全民覆蓋。此類合約明確規定使用耐用、長壽命的模組,從而產生多年的持續供貨收入。模組的銷售遠超消費電子設備的周期,確保了供應商的可預測需求,並穩定了整個指紋模組市場的工廠使用率。

智慧型手機與裝置端身份驗證的爆炸性整合

旗艦和中階行動電話現在都將指紋生物識別作為標配功能。屏下指紋辨識模組實現了全面屏設計,而超音波單元則透過對皮膚下紋路進行成像來增強安全性。北美和中國的安卓設備製造商正在採用雙感應區設計,以加快解鎖速度並提高單機平均容量。這一趨勢正在推動市場規模的擴大,並迫使供應商在厚度和功耗方面做出更嚴格的控制。

資料隱私與侵權訴訟風險

基於伊利諾伊州《生物識別資訊隱私法案》(BIPA)等法規的集體訴訟已導致數百萬美元的和解金,原因是指紋採集不當,這增加了企業的合規成本。企業買家現在要求設備端儲存範本和可撤銷的授權流程,這延長了設計週期和監管諮詢時間。銷售指紋模組解決方案的供應商必須增加加密、安全因素分離和第三方審核,這推高了材料和認證成本。

細分市場分析

超音波辨識器在2025年的收入佔比將較小,但成長迅速,預計到2030年將以10.2%的複合年成長率成長,超過所有其他類別。電容式指紋辨識器仍將佔據出貨量的大部分,到2024年將佔指紋模組市場佔有率的58%。電容式指紋辨識器市場規模的成長得益於低成本安卓手機的普及,而超音波指紋辨識器的應用則與高階智慧型手機和金融級穿戴裝置密切相關。

開發者盛讚超音波技術能夠對汗孔和皮下毛細血管結構進行成像,從而避免使用超薄螢幕保護膜和局部污染。高通第三代 3D Sonic 封裝技術實現了 Z 軸堆疊高度小於 200 微米,使 OEM 廠商能夠實現全螢幕玻璃電容式。電容式感測器不斷提升空間解析度,並將待機功耗降低至 5µA 以下,使其在量販店行動電話和消費物聯網領域保持重要地位。同時,光學模組正被應用於中階設備中,它們可以重複使用顯示引擎的背光,從而降低成本。

到2024年,面積/觸控模組將佔據61%的市場佔有率,這主要得益於其在消費性電子設備和企業門鎖領域久經考驗的可靠性。然而,屏下感測器預計到2030年將以每年11.5%的速度成長,這反映了行動電話製造商競相開發無縫OLED面板的趨勢。指紋模組市場規模,加上螢幕下方設計,將受益於較高的平均售價,從而彌補單一設備指紋模組密度較低的劣勢。

滑動式指紋辨識感應器仍應用於銷售點終端和窄邊框的加強型手持裝置。混合式觸控加壓力感應技術無需增加機身尺寸即可整合到機殼,從而提升了筆記型電腦廠商對該技術的品牌吸引力。多種感測器類型的結合凸顯了指紋識別模組產業向隱形生物識別的轉變,這與工業設計目標相契合。

區域分析

亞太地區擁有全球最大的生產基地和最大的部署計劃,預計2024年將佔據全球41%的市場佔有率,到2030年將維持9.8%的複合年成長率。中國行動電話OEM生態系統每月吸收數千萬個感測器,而印度的「數位之旅」(Digi Yatra)計畫的擴展和機場電子閘門競標正在推動國內民用需求的成長。東協致力於建造可互通的數位公共基礎設施,這正在協調相關標準,使供應商能夠跨多個司法管轄區交付通用模組。

北美市場呈現出成熟且前景良好的態勢:手機更換週期、穿戴式設備升級以及企業安全措施的維修,共同支撐著市場銷量的穩定;而日益嚴格的隱私保護法規,則促使消費者傾向於選擇設備端模板存儲,從而推高了平均售價。指紋模組市場持續受惠於美國汽車生物辨識技術的發展,而北卡羅來納州石英礦停產事件威脅到晶圓生產後,高階品牌紛紛轉向在地採購採購,以避免供應鏈風險。

歐洲正憑藉符合GDPR的國家電子識別計畫和銀行主導的生物辨識卡的推出,穩步推進電子身分識別。中東和非洲的潛在需求正日益凸顯,例如喀麥隆計劃在2025年根據一項為期15年的特許經營推出生物識別卡,這些項目都屬於國家識別計劃。隨著智慧型手機在中產階級的普及以及各國政府對社會福利發放平台的現代化改造,南美洲也呈現出逐步成長的趨勢,但宏觀經濟波動正在延長採購週期。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 調查結果

- 調查前提

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 政府生物辨識身分識別大型企劃激增

- 智慧型手機與裝置端身份驗證的爆炸性整合

- 電容式和光模組平均售價下降推動了其普及

- 汽車和智慧型槍支製造商都採用了指紋啟動/觸發模組。

- 生物辨識支付卡進入大規模發行階段

- 市場限制

- 資料隱私和資料外洩訴訟風險

- 後疫情時代,人們對觸摸感應器的衛生擔憂日益加劇

- MEMS/ IC封裝產能緊張限制了供應彈性。

- 價值/供應鏈分析

- 監管狀況

- 技術展望

- 五力分析

- 新進入者的威脅

- 買方/消費者的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭強度

第5章 市場規模與成長預測

- 依技術

- 光學的

- 電容式

- 超音波

- 熱

- 頻譜

- 依感測器類型

- 區域/觸摸

- 滑動

- 在顯示幕上

- 混合/組合

- 按外形規格

- 獨立模組

- 系統晶片(SoC) 整合

- 嵌入式ASIC/板級

- 按最終用戶產業

- 政府和執法部門

- 消費性電子產品

- BFSI

- 衛生保健

- 航空

- 車

- 智慧家庭和物聯網

- 其他行業

- 透過使用

- 身分和存取管理

- 支付和交易認證

- 考勤管理

- 邊境和移民管制

- 解鎖裝置

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- APAC

- 中國

- 日本

- 韓國

- 印度

- 澳洲和紐西蘭

- ASEAN-5

- 亞太地區的其他國家

- 中東和非洲

- 中東

- UAE

- 沙烏地阿拉伯

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 肯亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略舉措

- 市佔率分析

- 公司簡介

- Fingerprint Cards AB

- GOODIX Technology Inc.

- Synaptics Incorporated

- Integrated Biometrics LLC

- SecuGen Corporation

- HID Global Corporation

- Qualcomm Technologies Inc.

- Suprema Inc.

- Apple Inc.

- NITGEN Co., Ltd.

- NEC Corporation

- NEXT Biometrics ASA

- Anviz Global

- IDEMIA France SAS

- Thales Group

- Egis Technology Inc.

- IDEX Biometrics ASA

- Infineon Technologies AG

- Samsung Electronics Co., Ltd.

- ZKTeco Co., Ltd.

- Precise Biometrics AB

- Shenzhen SYNOCHEM Microelectronics

第7章 市場機會與未來展望

The fingerprint module market size is valued at USD 10.87 billion in 2025 and is forecast to reach USD 17.13 billion by 2030, reflecting a 9.52% CAGR.

Momentum stems from sovereign digital-identity projects, rapid smartphone authentication upgrades, and the commercial roll-out of biometric payment cards. Capacitive sensors still dominate volume demand, yet ultrasonic technology is expanding fastest as premium devices seek higher spoof-resistance. System-on-chip (SoC) integration is shrinking footprint and bill-of-materials costs, while in-display modules underpin the push for bezel-less handset designs. Volume procurement for Asia-Pacific government programs, falling average selling prices, and automotive adoption together keep the fingerprint module market on a multi-year growth arc.

Global Fingerprint Module Market Trends and Insights

Government Biometric ID Megaprojects Surge

Large-scale national identity programs are rewriting baseline demand. Ethiopia's Fayda scheme targets 90 million registrations by 2030, backed by USD 350 million in multilateral funding.Nigeria's USD 430 million digital ID project pursues universal coverage for more than 200 million citizens. Such contracts specify robust, long-life modules and create multi-year replenishment revenue. The volume sheerly outstrips consumer-device cycles, ensuring predictable pull for suppliers and stabilizing factory utilization across the fingerprint module market.

Explosive Smartphone Integration for On-Device Authentication

Flagship and mid-tier handsets now treat fingerprint biometrics as baseline functionality. Under-display modules permit full-screen designs, while ultrasonic units lift security by imaging sub-epidermal ridges. Android handset makers in North America and China have embedded dual sensing zones to quicken unlock speed, raising average content per device. This trend expands addressable volume and pressures suppliers to meet tighter thickness and power-budget envelopes.

Data-Privacy & Breach Litigation Risk

Class actions under statutes such as Illinois' BIPA have generated multimillion-dollar settlements for improper fingerprint capture, raising compliance overheads for enterprises. Corporate buyers now demand on-device template storage and revocable consent flows, extending design-in cycles and regulatory consultations. Vendors marketing the fingerprint module market solutions must add encryption, secure-element isolation, and third-party audits, which inflate the bill-of-materials and certification costs.

Other drivers and restraints analyzed in the detailed report include:

- Falling ASP of Capacitive & Optical Modules Broadens Adoption

- Biometric Payment Cards Reach Mass-Issuance Stage

- Hygiene Backlash on Touch Sensors in Post-Pandemic Settings

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Ultrasonic units contributed a minor yet fast-advancing slice of 2025 revenue and should expand at 10.2% CAGR to 2030, outpacing all other categories. Capacitive solutions still delivered the bulk of shipments, anchoring 58% fingerprint module market share in 2024. The fingerprint module market size for capacitive sensors rose on the back of low-cost Android models, whereas ultrasonic adoption correlated with premium ASP smartphones and finance-grade wearables.

Developers prize ultrasonic technology for its capacity to image sweat pores and sub-dermal capillary structures, defeating thin-film screen protectors and partial contaminants. Qualcomm's third-generation 3D Sonic packages achieve sub-200-micron Z-stack height, freeing OEMs to pursue edge-to-edge glass builds. Capacitive incumbents continue to raise spatial resolution and cut idle power below 5 µA, preserving relevance in mass-market phones and consumer IoT. Optical modules, meanwhile, land in mid-tier devices where backlighting can be reused from display engines to trim costs.

Area/touch modules accounted for 61% of 2024 due to proven reliability across consumer devices and enterprise door locks. Nonetheless, in-display sensors are forecast to climb 11.5% annually to 2030, reflecting handset makers' race for uninterrupted OLED panels. The fingerprint module market size linked to in-display designs will benefit from premium ASPs, offsetting lower density per handset.

Swipe sensors linger in point-of-sale terminals and rugged handhelds where narrow bezels remain. Hybrid touch-plus-pressure packages are gaining brand traction among notebook PC vendors, enabling palm-rest integration without enlarging the chassis. The sensor-type mix underlines the fingerprint module industry shift toward invisible biometrics that harmonize with industrial design goals.

The Fingerprint Module Market is Segmented by Technology (Optical, Capacitive, Ultrasonic, and More), Sensor Type (Area/Touch, Swipe, and More), Form Factor (Stand-Alone Module, System-On-Chip Integrated, and More), End-User Industry (Government and Law Enforcement, Consumer Electronics, and More), Application (Identity and Access Management, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific combined the world's biggest production basin with the largest deployment programs, holding 41% market share in 2024 and tracking a 9.8% CAGR to 2030. China's handset OEM ecosystem absorbs tens of millions of sensors monthly, while India's Digi Yatra expansion and airport e-gate tenders elevate domestic civil demand. ASEAN's commitment to interoperable digital public infrastructure harmonizes standards, letting suppliers ship common module footprints across multiple jurisdictions.

North America shows mature yet lucrative conditions: handset replacement cycles, wearables upgrades, and enterprise security retrofits keep volumes stable, whereas stringent privacy legislation prompts buyers to favor on-device template storage, lifting ASPs. The fingerprint module market continues to profit from U.S. automotive biometrics, where luxury brands localize sourcing to hedge supply-chain risk after North Carolina quartz mine disruptions threatened wafer output.

Europe advances on the back of GDPR-aligned national e-ID plans and bank-driven biometric card launches. Middle East & Africa's latent demand crystallizes in national ID projects such as Cameroon's 2025 biometric card roll-out under a 15-year concession. South America provides incremental gains as smartphones penetrate mid-income cohorts and governments modernize social-benefits disbursement platforms, though macro volatility elongates procurement cycles.

- Fingerprint Cards AB

- GOODIX Technology Inc.

- Synaptics Incorporated

- Integrated Biometrics LLC

- SecuGen Corporation

- HID Global Corporation

- Qualcomm Technologies Inc.

- Suprema Inc.

- Apple Inc.

- NITGEN Co., Ltd.

- NEC Corporation

- NEXT Biometrics ASA

- Anviz Global

- IDEMIA France SAS

- Thales Group

- Egis Technology Inc.

- IDEX Biometrics ASA

- Infineon Technologies AG

- Samsung Electronics Co., Ltd.

- ZKTeco Co., Ltd.

- Precise Biometrics AB

- Shenzhen SYNOCHEM Microelectronics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government biometric ID megaprojects surge

- 4.2.2 Explosive smartphone integration for on-device authentication

- 4.2.3 Falling ASP of capacitive and optical modules broadens adoption

- 4.2.4 Automotive and smart-gun makers embed fingerprint start/trigger modules

- 4.2.5 Biometric payment cards reach mass-issuance stage

- 4.3 Market Restraints

- 4.3.1 Data-privacy and breach litigation risk

- 4.3.2 Hygiene backlash on touch sensors in post-pandemic settings

- 4.3.3 Tight MEMS / IC packaging capacity limits supply elasticity

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Technology

- 5.1.1 Optical

- 5.1.2 Capacitive

- 5.1.3 Ultrasonic

- 5.1.4 Thermal

- 5.1.5 Multispectral

- 5.2 By Sensor Type

- 5.2.1 Area/Touch

- 5.2.2 Swipe

- 5.2.3 In-display

- 5.2.4 Hybrid/Combo

- 5.3 By Form Factor

- 5.3.1 Stand-alone Module

- 5.3.2 System-on-Chip (SoC) Integrated

- 5.3.3 Embedded ASIC/Board-level

- 5.4 By End-user Industry

- 5.4.1 Government and Law Enforcement

- 5.4.2 Consumer Electronics

- 5.4.3 BFSI

- 5.4.4 Healthcare

- 5.4.5 Aviation

- 5.4.6 Automotive

- 5.4.7 Smart Home and IoT

- 5.4.8 Other Industrial

- 5.5 By Application

- 5.5.1 Identity and Access Management

- 5.5.2 Payment and Transaction Authentication

- 5.5.3 Time and Attendance

- 5.5.4 Border Control and Immigration

- 5.5.5 Device Unlocking

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 APAC

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 South Korea

- 5.6.4.4 India

- 5.6.4.5 Australia and New Zealand

- 5.6.4.6 ASEAN-5

- 5.6.4.7 Rest of APAC

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 UAE

- 5.6.5.1.2 Saudi Arabia

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Kenya

- 5.6.5.2.4 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Fingerprint Cards AB

- 6.4.2 GOODIX Technology Inc.

- 6.4.3 Synaptics Incorporated

- 6.4.4 Integrated Biometrics LLC

- 6.4.5 SecuGen Corporation

- 6.4.6 HID Global Corporation

- 6.4.7 Qualcomm Technologies Inc.

- 6.4.8 Suprema Inc.

- 6.4.9 Apple Inc.

- 6.4.10 NITGEN Co., Ltd.

- 6.4.11 NEC Corporation

- 6.4.12 NEXT Biometrics ASA

- 6.4.13 Anviz Global

- 6.4.14 IDEMIA France SAS

- 6.4.15 Thales Group

- 6.4.16 Egis Technology Inc.

- 6.4.17 IDEX Biometrics ASA

- 6.4.18 Infineon Technologies AG

- 6.4.19 Samsung Electronics Co., Ltd.

- 6.4.20 ZKTeco Co., Ltd.

- 6.4.21 Precise Biometrics AB

- 6.4.22 Shenzhen SYNOCHEM Microelectronics

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment