|

市場調查報告書

商品編碼

1846152

乙烯-四氟乙烯(ETFE):市場佔有率分析、產業趨勢、統計數據、成長預測(2025-2030)Ethylene Tetrafluoroethylene (ETFE) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

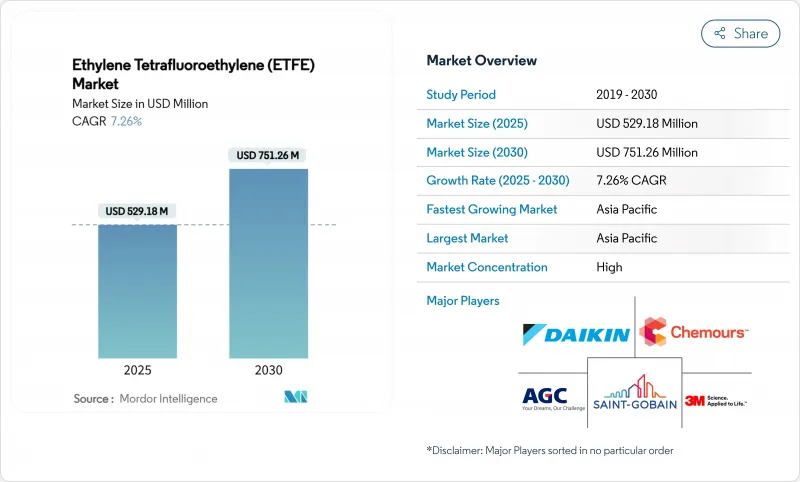

乙烯-四氟乙烯(ETFE) 市場規模預計在 2025 年為 5.2918 億美元,預計到 2030 年將達到 7.5126 億美元,預測期內(2025-2030 年)的複合年成長率為 7.26%。

由於 ETFE 比傳統玻璃和聚合物替代品具有更出色的透明度、化學惰性和拉伸強度,因此建築膜、航太佈線和透明光伏層壓板是關鍵的成長動力。北美和歐洲的體育場屋頂繼續展示 ETFE 的輕質和採光優勢,而航空公司和電動垂直起降 (eVTOL) 製造商則指定使用能夠承受熱循環和液壓油侵蝕的 ETFE 絕緣電纜。太陽能電池組件製造商正在採用透明 ETFE 層壓板將陽光轉化為電能,同時保持建築幕牆美觀,將 ETFE 市場擴展到建築一體化光伏領域。亞太地區不斷提高的生產能力支持了供應安全,而歐洲和北美的全氟烷基物質 (PFAS) 法規也可能推動對更綠色化學和本地化價值鏈的投資。

全球乙烯-四氟乙烯(ETFE) 市場趨勢與洞察

作為體育場類建築的屋頂覆蓋材料越來越受歡迎

體育場設計師擴大指定使用 ETFE 屋頂,因為它可以提供自然採光,而不是像傳統玻璃座艙罩那樣增加結構重量。 Intuit Dome 的 277,000 平方英尺傾斜屋頂結構使用透明的 ETFE 薄膜,可實現自然通風,因此無需在某些區域使用空調,同時還獲得了能源與環境設計先鋒獎 (LEED) 白金認證。 ETFE 的自熄特性消除了火災風險,這傳統上限制了它在高運轉率設施中的應用。除了其功能之外,ETFE 還能散射陽光,防止溫室效應,同時保持 95% 的太陽透射率,從而創造出傳統屋頂材料無法實現的最佳比賽環境。隨著場館營運商認知到 ETFE 的長期成本優勢,這一趨勢正在加速,與頻繁更換玻璃面板相比,ETFE 的維護只需每兩到三年清潔一次。

航太航太佈線對乙烯-四氟乙烯(ETFE) 電纜的需求不斷增加

航太製造商擴大採用 ETFE 電纜,因為它們可以承受極端的溫度循環和化學物質的侵蝕,而這些會劣化傳統絕緣材料的性能。 《2025 年航太與國防展望》預測,全球航空客運量將成長 11.6%,國防費用將超過 2.4 兆美元,這將對高性能電纜解決方案產生持續的需求。 ETFE 的耐液壓油性和熱穩定性對於下一代飛機系統至關重要,特別是電動垂直起降 (eVTOL) 飛行器,因為輕量化結構至關重要。軍事應用推高了 ETFE 電纜的價格,因為它們符合戰鬥機和太空船熱控制表面的嚴格規格。向更多電動飛機架構的轉變正在將 ETFE 的作用從傳統電纜擴展到電源管理系統,在電源管理系統中,它的熱穩定性允許高電流密度而不會發生絕緣故障。

環境問題和對全氟烷基物質 (PFAS)/含氟聚合物日益嚴格的監管

歐盟提案的全氟和多氟烷基物質 (PFAS) 法規可能禁止超過 10,000 種濃度超過規定限值的物質,包括 ETFE,實施時間表延長至 2029 年。這種監管壓力迫使製造商制定 PFAS 管理策略,包括供應鏈審核和採購替代品,但合適的替代品通常性能較低或成本較高。大金已投資超過 3 億美元用於捕獲 PFAS排放,目標是到 2030 年實現製程廢水中 99.9% 的 PFAS 回收率,同時過渡到永續製造技術。歐洲環境署強調,PFAS 聚合物佔歐盟 (EU) 市場 PFAS 總量的 24-40%,其持久性和潛在毒性會在從生產到處置的整個生命週期中造成污染。歐洲的集中式方法與美國各州法規之間的監管分散增加了營運成本並產生了合規複雜性,限制了 ETFE 產品的市場准入。

細分分析

到2024年,擠出成型將佔總收入的61.76%,凸顯了連續薄膜、片材和電線塗層的效率。隨著體育場館和溫室計劃的推進,ETFE擠出級產品的市場規模預計將穩定成長。射出成型的複合年成長率為8.09%,反映了對精密零件(例如複雜纜線連接器和半導體腔體組件)日益成長的需求。由於加工商希望在不擁有多項固定資產的情況下滿足航太航太和電子行業的利基訂單,能夠同時進行擠出和射出成型的混合成型機正日益普及。

NEOFLON ETFE-TX 等最佳化樹脂等級可增強兩種製程的拉伸性能,從而實現更薄的壁厚和更輕的零件重量,且不影響其耐用性。製程設備製造商正在推出針對 ETFE 高熔點特性而客製化的螺桿幾何和熱流道系統,以幫助加工商避免劣化和表面缺陷。

到2024年,顆粒材料將佔據56.14%的市場佔有率,因為顆粒狀材料能夠確保擠出和注射過程中的穩定流動。電線電纜製造商更青睞顆粒材料,因為它們能夠實現精確計量,從而最大限度地減少介電缺陷。粉末材料市場以8.57%的複合年成長率成長,適用於需要薄而均勻塗層的噴塗和積層製造應用。隨著航太為粉末床熔合和冷噴塗修復做好準備,粉末ETFE的市場佔有率將持續上升。

製造商正在將奈米填料添加到粉末等級中,以提高製程管道和燃料裝置的表面硬度。混合形式、微粒和高堆積密度粉末彌補了傳統顆粒和超細顆粒之間的差距,使轉換器能夠靈活地在擠出和塗層生產線之間切換,並最大限度地減少轉換。

區域分析

預計到2024年,亞太地區將佔全球市場收益的47.24%,到2030年,複合年成長率將達到8.66%,這得益於中國乙烯產能的不斷擴大以及日本在高純度氟聚合物領域的專業技術。 ETFE屋頂材料常用於政府支持的體育場和高鐵站,推動了該地區的建設。當地加工商正為半導體和鋰電池工廠擴建粉末塗料生產線,深化國內價值取得。

北美仍然是ETFE的主要消費市場,美國國家橄欖球聯盟(NFL)和美國職業足球大聯盟的場館都使用ETFE膜來獲得清晰的視野並全年保護草坪。從華盛頓州到魁北克省的航太叢集正在推動電線絕緣材料的需求,而墨西哥灣沿岸的可再生燃料煉油廠則使用ETFE管材進行防腐。區域清潔能源激勵措施正在推動BIPV(建築一體化光伏)建築幕牆的資金投入,這些外牆充分利用了ETFE的光學特性。

在歐洲應對PFAS監管舉步維艱之際,ETFE正被用於標誌性建築和離岸風力發電電纜。德國汽車製造商正在800V動力傳動系統中使用ETFE線束,北歐國家正在溫室中安裝ETFE層壓農業太陽能屋頂,以延長日照時間有限的生產週期。乙烯的合理化調整導致供應緊張,但特種ETFE牌號仍保持定價優勢。

雖然南美、中東和非洲仍在發展中,但即將舉行的錦標賽的體育場維修和機場擴建已開始使用ETFE建築幕牆。儘管當地樹脂短缺促使進口,但區域工程公司正在與現有供應商合作,以促進技術轉移和建築專業知識的累積。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場狀況

- 市場概況

- 市場促進因素

- 作為體育場類建築的屋頂覆蓋材料越來越受歡迎

- 航太航太佈線對乙烯-四氟乙烯(ETFE) 電纜的需求不斷增加

- 傳統玻璃建築幕牆的輕盈耐用替代品

- 推出透明乙烯-四氟乙烯(ETFE) 太陽能電池層壓板

- 可再生航空燃料工廠所需的耐化學腐蝕管路

- 市場限制

- 環境問題以及對全氟和多氟烷基物質 (PFAS)/含氟聚合物的更嚴格監管

- 單層乙烯-四氟乙烯(ETFE) 墊的防火安全要求更加嚴格

- 全球乙烯-四氟乙烯(ETFE)樹脂產能已達極限

- 價值鏈分析

- 五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章市場規模及成長預測

- 依技術

- 擠壓成型

- 射出成型

- 依產品類型

- 粉末

- 顆粒

- 其他產品類型(例如顆粒)

- 按用途

- 薄膜和片材

- 電線電纜

- 管子

- 塗層

- 其他應用(例如 3D 列印零件)

- 按最終用途行業

- 建築/施工

- 航太/國防

- 汽車和電動交通

- 電氣和電子

- 太陽能發電

- 工業和化學加工

- 按地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 東南亞國協

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭態勢

- 市場集中度

- 策略舉措

- 市佔率(%)/排名分析

- 公司簡介

- 3M

- AGC Inc.

- Arkema

- DAIKIN INDUSTRIES, Ltd.

- Denise Chemical Co., Limited

- Everflon Fluoropolymers

- Ganzhou Lichang New Materials Co., Ltd.

- Guarniflon SpA

- HaloPolymer, OJSC

- NOWOFOL Kunststoffprodukte GmbH & Co. KG

- SABIC

- Saint-Gobain

- The Chemours Company

- Vector Foiltec

- Zeus Company LLC

第7章 市場機會與未來展望

The Ethylene Tetrafluoroethylene Market size is estimated at USD 529.18 Million in 2025, and is expected to reach USD 751.26 Million by 2030, at a CAGR of 7.26% during the forecast period (2025-2030).

Architectural membranes, aerospace wiring, and transparent photovoltaic laminates are the principal growth engines, as the material's clarity, chemical inertness, and tensile strength outperform conventional glass and polymer alternatives. Stadium roofing projects across North America and Europe continue to showcase ETFE's weight savings and daylighting advantages, while airlines and Electric Vertical Take-off and Landing (eVTOL) manufacturers specify ETFE-insulated cables to withstand thermal cycling and hydraulic-fluid exposure. Solar module producers are deploying transparent ETFE laminates that preserve facade aesthetics and convert sunlight into power, expanding the ETFE market into building-integrated photovoltaics. Regional production capacity additions in Asia-Pacific underpin supply security, although Per- and polyfluoroalkyl substances (PFAS) regulations in Europe and North America could redirect investment toward greener chemistries and localized value chains.

Global Ethylene Tetrafluoroethylene (ETFE) Market Trends and Insights

Gaining Popularity as Roof-cover Material for Stadium-type Structures

Stadium architects are increasingly specifying ETFE roofing systems because they deliver natural lighting while eliminating the structural weight penalties of traditional glass canopies. The Intuit Dome's 277,000 square foot diagrid roof structure incorporates clear ETFE membranes that allow natural airflow, eliminating air conditioning requirements in certain areas while achieving Leadership in Energy and Environmental Design (LEED) Platinum certification. The material's self-extinguishing properties address fire safety concerns that have historically limited membrane adoption in high-occupancy venues. Beyond functionality, ETFE's ability to scatter sunlight prevents greenhouse effects while maintaining 95% daylight transmission, creating optimal playing conditions that traditional roofing cannot match. This trend is accelerating as venue operators recognize ETFE's long-term cost advantages, with maintenance requirements limited to cleaning every 2-3 years compared to frequent glass panel replacements.

Rising Demand for Ethylene Tetrafluoroethylene (ETFE) Cables in Aerospace Wiring

Aerospace manufacturers are expanding ETFE cable adoption because the material withstands extreme temperature cycles and chemical exposure that would degrade conventional insulation materials. The 2025 Aerospace and Defense Industry Outlook projects 11.6% growth in global air passenger traffic, with defense spending surpassing USD 2.4 Trillion, creating sustained demand for high-performance wiring solutions. ETFE's resistance to hydraulic fluids and thermal stability make it essential for next-generation aircraft systems, particularly in electric vertical takeoff and landing (eVTOL) aircraft where weight reduction is critical. Military applications drive premium pricing, as ETFE cables meet stringent specifications for combat aircraft and spacecraft thermal control surfaces. The shift toward more electric aircraft architectures is expanding ETFE's role beyond traditional wiring to power management systems, where its thermal stability enables higher current densities without insulation failure.

Environmental Concerns and Stricter Per- and Polyfluoroalkyl Substances (PFAS)/Fluoropolymer Regulations

The European Union's proposed Per- and Polyfluoroalkyl Substances (PFAS) restrictions could ban over 10,000 substances, including ETFE, in concentrations exceeding specified limits, with implementation timelines extending to 2029. This regulatory pressure is forcing manufacturers to develop PFAS management strategies, including supply chain audits and sourcing alternatives, though suitable replacements often underperform or carry higher costs. Daikin has responded by investing over USD 300 Million to capture PFAS emissions, targeting a 99.9% capture rate in process water discharges while transitioning to sustainable manufacturing technologies by 2030. The European Environment Agency emphasizes that PFAS polymers constitute 24-40% of total PFAS volume in European Union (EU) markets, with their persistence and potential toxicity creating pollution throughout their lifecycle from production to disposal. The regulatory fragmentation between Europe's centralized approach and the United States' (US) state-by-state restrictions creates compliance complexities that increase operational costs and limit market access for ETFE products.

Other drivers and restraints analyzed in the detailed report include:

- Light-weight, Durable Facades Replacing Conventional Glass

- Emergence of Transparent Ethylene Tetrafluoroethylene (ETFE) Photovoltaic Laminates

- Fire-safety Scrutiny on Single-skin Ethylene Tetrafluoroethylene (ETFE) Cushions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Extrusion molding generated 61.76% of 2024 revenue, highlighting its efficiency for continuous films, sheets, and wire coatings. The ETFE market size for extrusion-grade products is set to grow steadily alongside stadium and greenhouse projects. Injection molding's 8.09% CAGR reflects rising demand for precision parts such as complex cable connectors and semiconductor chamber components. Hybrid machines capable of both extrusion and injection are gaining traction as converters aim to serve niche aerospace and electronics orders without multiple capital assets.

Optimized resin grades like NEOFLON ETFE-TX strengthen tensile performance for both processes, enabling thinner walls and lower part weight without sacrificing durability. Processing-equipment makers are introducing screw geometries and hot-runner systems tailored to ETFE's high melt temperature, helping processors avoid degradation and surface defects.

Granules accounted for 56.14% of the 2024 market value share because pelletized form assures consistent flow during extrusion and injection. Wire & cable producers favor granules for precise metering that minimizes dielectric defects. Powder grades, expanding at 8.57% CAGR, cater to spray-coating and additive-manufacturing uses where thin, uniform layers are mandatory. The ETFE market share for powders will rise as aerospace primes qualify powder-bed fusion and cold-spray repairs.

Manufacturers are blending nano-fillers into powder grades to raise surface hardness for process piping and fuel plants. Hybrid formats, micro-granules and high-bulk-density powders bridge the gap between conventional pellets and ultrafine particles, giving converters flexibility to switch between extrusion and coating lines with minimal changeovers.

The Ethylene Tetrafluoroethylene (ETFE) Market Report is Segmented by Technology (Extrusion Molding and Injection Molding), Product Type (Powder, Granule, and More), Application (Coatings, Tubes, and More), End-Use Industry (Aerospace and Defense, Solar Photovoltaics, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific generated 47.24% of global market revenue in 2024 and is advancing at an 8.66% CAGR through 2030, benefiting from China's expanding ethylene capacity and Japan's expertise in high-purity fluoropolymers. Government-backed stadium and high-speed-rail stations frequently adopt ETFE roofs, reinforcing regional construction pull. Local converters scale powder-coating lines to serve semiconductor fabs and lithium-battery plants, deepening domestic value capture.

North America remains a prime consumer as National Football League (NFL) and Major League Soccer venues adopt ETFE membranes that deliver clear sightlines and year-round turf protection Axios. The aerospace cluster from Washington State to Quebec drives wire-insulation demand, while renewable-fuel refineries along the Gulf Coast integrate ETFE tubing for corrosion control. Regional clean-energy incentives funnel capital toward Building-Integrated Photovoltaics (BIPV) facades that capitalize on ETFE's optical properties.

Europe grapples with PFAS regulation but still embraces ETFE for iconic structures and offshore wind farm cables. German carmakers deploy ETFE wire harnesses in 800-V drivetrains, whereas Nordic countries integrate ETFE-laminated agrivoltaic roofs across greenhouses to stretch production seasons under limited sunlight. Ethylene rationalization tightens supply, yet specialty ETFE grades retain pricing power.

South America and the Middle East & Africa remain nascent, yet stadium upgrades for upcoming tournaments and airport expansions are beginning to spec ETFE facades. Local resin shortages prompt imports, but regional engineering firms partner with established suppliers to accelerate technology transfer and installation expertise.

- 3M

- AGC Inc.

- Arkema

- DAIKIN INDUSTRIES, Ltd.

- Denise Chemical Co., Limited

- Everflon Fluoropolymers

- Ganzhou Lichang New Materials Co., Ltd.

- Guarniflon S.p.A

- HaloPolymer, OJSC

- NOWOFOL Kunststoffprodukte GmbH & Co. KG

- SABIC

- Saint-Gobain

- The Chemours Company

- Vector Foiltec

- Zeus Company LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Gaining Popularity as Roof-cover Material for Stadium-type Structures

- 4.2.2 Rising Demand for Ethylene Tetrafluoroethylene (ETFE) Cables in Aerospace Wiring

- 4.2.3 Light-weight, Durable Facades Replacing Conventional Glass

- 4.2.4 Emergence of Transparent Ethylene Tetrafluoroethylene (ETFE) Photovoltaic Laminates

- 4.2.5 Chemical-resistant Tubing Demand in Renewable Aviation-fuel Plants

- 4.3 Market Restraints

- 4.3.1 Environmental Concerns and Stricter Per- and polyfluoroalkyl substances (PFAS)/fluoropolymer Regulations

- 4.3.2 Fire-safety Scrutiny on Single-skin Ethylene Tetrafluoroethylene (ETFE) Cushions

- 4.3.3 Limited Global Ethylene Tetrafluoroethylene (ETFE)-resin Capacity

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Technology

- 5.1.1 Extrusion Molding

- 5.1.2 Injection Molding

- 5.2 By Product Type

- 5.2.1 Powder

- 5.2.2 Granule

- 5.2.3 Other Product Types (Pellet, etc.)

- 5.3 By Application

- 5.3.1 Film and Sheet

- 5.3.2 Wire and Cable

- 5.3.3 Tubes

- 5.3.4 Coatings

- 5.3.5 Other Applications (3D-Printed Components, etc.)

- 5.4 By End-use Industry

- 5.4.1 Building and Construction

- 5.4.2 Aerospace and Defense

- 5.4.3 Automotive and E-Mobility

- 5.4.4 Electrical and Electronics

- 5.4.5 Solar Photovoltaics

- 5.4.6 Industrial and Chemical Processing

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 Japan

- 5.5.1.3 India

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 NORDIC Countries

- 5.5.3.8 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 3M

- 6.4.2 AGC Inc.

- 6.4.3 Arkema

- 6.4.4 DAIKIN INDUSTRIES, Ltd.

- 6.4.5 Denise Chemical Co., Limited

- 6.4.6 Everflon Fluoropolymers

- 6.4.7 Ganzhou Lichang New Materials Co., Ltd.

- 6.4.8 Guarniflon S.p.A

- 6.4.9 HaloPolymer, OJSC

- 6.4.10 NOWOFOL Kunststoffprodukte GmbH & Co. KG

- 6.4.11 SABIC

- 6.4.12 Saint-Gobain

- 6.4.13 The Chemours Company

- 6.4.14 Vector Foiltec

- 6.4.15 Zeus Company LLC

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Investment in Ethylene Tetrafluoroethylene (ETFE) Recycling Technologies

乙烯-四氟乙烯市場按產品類型、銷售管道和最終用途行業分類 - 全球預測 2025-2032

乙烯-四氟乙烯市場按產品類型、銷售管道和最終用途行業分類 - 全球預測 2025-2032 乙烯-四氟乙烯市場規模、佔有率和成長分析(按形狀、技術、應用、最終用途、地區):產業預測(2024-2031)

乙烯-四氟乙烯市場規模、佔有率和成長分析(按形狀、技術、應用、最終用途、地區):產業預測(2024-2031) 乙烯四氟乙烯 (ETFE) 市場機會、成長動力、產業趨勢分析和 2025 年至 2034 年預測

乙烯四氟乙烯 (ETFE) 市場機會、成長動力、產業趨勢分析和 2025 年至 2034 年預測 乙烯-四氟乙烯(ETFE)的全球市場(2024-2028)

乙烯-四氟乙烯(ETFE)的全球市場(2024-2028) 全球 ETFE 市場規模:按類型、技術、應用、最終用途產業、地區、範圍和預測乙烯-四氟乙烯市場規模、佔有率、趨勢分析報告:按類型、技術、最終用途、地區、細分市場預測,2024-2030 年

全球 ETFE 市場規模:按類型、技術、應用、最終用途產業、地區、範圍和預測乙烯-四氟乙烯市場規模、佔有率、趨勢分析報告:按類型、技術、最終用途、地區、細分市場預測,2024-2030 年