|

市場調查報告書

商品編碼

1844738

有機矽添加劑:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)Silicone Additives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

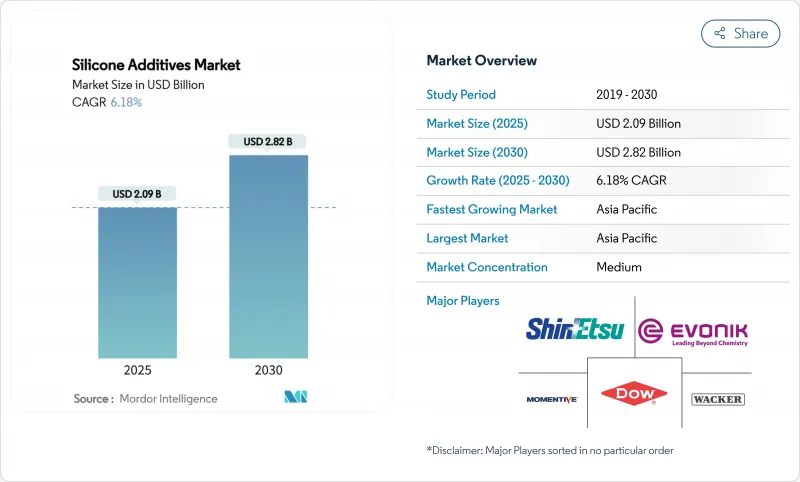

預計 2025 年有機矽添加劑市場規模為 20.9 億美元,到 2030 年預計將達到 28.2 億美元,預測期內(2025-2030 年)的複合年成長率為 6.18%。

強勁的需求源自於製造商尋求能夠保持被覆劑、聚合物和流體在高溫、化學品和惡劣天氣條件下穩定的添加劑。減少揮發性有機化合物 (VOC)排放的監管壓力正推動配方師轉向兼顧性能和合規性的富含有機矽的系統。成長動能也體現在電動車的溫度控管、生物基個人保健產品的推出以及新興經濟體食品加工自動化程度的提高。產業整合,尤其是 KCC 於 2024 年收購邁圖 (Momentive),標誌著產業向規模優勢、垂直整合和更快創新管道的轉變。

全球有機矽添加劑市場趨勢與洞察

個人護理行業的需求不斷成長

隨著消費者越來越青睞無油輕盈的質地,配方師開始轉向矽油,尋求其絲滑的延展性和持久的保濕效果。例如,信越化學的油包彈性體產品系列能夠生產穩定的油包水乳化,在保持理想膚感的同時,滿足區域性環狀矽氧烷禁令。供應商正在部署植物來源C13-15烷烴載體,例如埃肯的PURESIL ORG Gel,這證明了感官性能與天然定位可以共存。亞太地區的化妝品製造商正在利用這些特性來彌補與全球高階品牌的差距,並拓展彩妝品和防曬產品中有機矽添加劑的市場。

油漆和塗料中低VOC產品日益受到關注

歐洲和北美的立法已對允許的溶劑含量作出限制,使低VOC合規性成為先決條件而非一項特性。贏創的TEGO Guard 9000可為外牆塗料提供早期耐候性,且不違反生態標章的閾值。 Siltec公司證明,長鏈烷基有機矽可以提高固態含量,同時降低VOC,使配方設計師在保持耐久性的同時達到綠色印章和LEED標準。這種連鎖反應也蔓延到了新興市場,建築商正在指定使用添加了有機矽表面添加劑的水性塗料,以實現耐污性和持久的色彩。

高溫下的添加劑遷移

溫度超過200 度C時,低分子量矽氧烷會滲出到表面,降低光學透明度,並可能削弱附著力。高苯基矽橡膠的研究表明,其熱穩定性有所提高,在478 度C時重量損失僅為5%,但優質等級會增加成本。電動車牽引馬達和航太管路需要降低揮發性的配方,這會對研發預算造成壓力。

細分分析

2024年,矽油將佔有機矽添加劑市場收入的39.44%,這得益於其在塗料、個人護理和潤滑劑等領域的廣泛應用,例如增滑劑、流平劑和傳熱劑。低表面張力和寬溫度穩定性支撐了強勁的需求。乳化和樹脂可作為矽油的補充,用於水性系統和結構飾面,尤其是在建築密封膠領域。相較之下,彈性體則服務於需要持久彈性的細分領域,例如墊圈、密封件和醫用導管。

粉末和顆粒佔總收入的不到四分之一,但到2030年,其複合年成長率最高,可達7.65%。乾粉形狀可用於配製3D列印原料和母粒,使配方師能夠實現精細的流變控制和無塵配料。新型紫外光固化聚矽氧烷粉末簡化了快速原型製造的按需交聯,縮短了從設計到零件的週期,並拓展了積層製造領域有機矽添加劑的市場。隨著印表機的應用範圍從航太擴展到牙科和消費品,粉末有機矽將開闢新的成長途徑。

區域分析

亞太地區將在2024年引領有機矽添加劑市場,營收佔有率將達47.34%,預計到2030年複合年成長率將達到7.10%。中國張家港和南京叢集為瓦克和埃肯的上游矽氧烷產能提供支持,確保其能夠接近性供應主要電子和電動汽車電池公司。印度的「印度製造」計畫正在刺激國內對高品質被覆劑和黏合劑的需求,鼓勵國內複合材料生產商加入有機矽添加劑,以實現優質的表面處理和耐用性。日本和韓國也在推動有機矽添加劑在高頻電子、光電和特殊薄膜領域的先進研發。

北美是一個成熟且蓬勃發展的創新地區。美國憑藉著符合FDA/USP標準的矽膠體系,在醫療設備和航太複合材料的應用方面處於領先地位。陶氏在密西根州開展的矽膠回收試點計畫旨在將聚二甲基矽氧烷(PDMS)的碳排放減少50%,這與ESG(環境、社會和治理)要求下的買家產生了共鳴。加拿大對電動車電池的投資以及墨西哥的汽車產業叢集正在推動溫度控管添加劑的進一步應用。

歐洲規模位居第三,但在永續性嚴格程度方面位居第一。 REACH法規和即將訂定的PFAS禁令將加強對不含環狀化合物的生物基有機矽替代品的研發。贏創的Smart Effects業務線將矽氧烷與有機特殊產品結合,以滿足輕量化、電動車和數位健康市場的需求。德國和法國正致力於汽車電氣化補貼,而英國則專注於生命科學領域的塗料。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場狀況

- 市場概況

- 市場促進因素

- 個人護理行業的需求不斷成長

- 低VOC油漆和塗料日益受到關注

- 食品加工產業的需求不斷成長

- 拓展醫療保健領域的應用

- 汽車業的高使用率

- 市場限制

- 高溫下的添加劑遷移

- 原物料成本不穩定

- 遷移和黏附問題等技術挑戰

- 價值鏈分析

- 五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章市場規模及成長預測

- 按產品形態

- 液體和油

- 彈性體和橡膠

- 樹脂

- 粉末/顆粒

- 乳劑

- 按用途

- 消泡劑

- 流變改質劑

- 界面活性劑

- 潤濕劑和分散劑

- 潤滑劑

- 附著力促進劑

- 其他用途(例如脫模劑)

- 按最終用戶產業

- 飲食

- 塑膠和複合材料

- 油漆和塗料

- 個人護理

- 黏合劑和密封劑

- 紙和紙漿

- 石油和天然氣

- 其他終端用戶產業(電子、半導體等)

- 地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 東南亞國協

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭態勢

- 市場集中度

- 策略舉措

- 市佔率(%)/排名分析

- 公司簡介

- AB Specialty Silicones

- Altana AG

- Bluestar Silicones

- BRB International

- Clariant AG

- Dow

- Elkem ASA

- Evonik Industries AG

- Jiangsu Maysta Chemical

- KCC SILICONE CORPORATION

- Momentive

- Shin-Etsu Chemical Co., Ltd.

- Silibase Silicone

- Siltech Corporation

- Supreme Silicones India Pvt. Ltd.

- The Lubrizol Corporation

- Wacker Chemie AG

第7章 市場機會與未來展望

The Silicone Additives Market size is estimated at USD 2.09 billion in 2025, and is expected to reach USD 2.82 billion by 2030, at a CAGR of 6.18% during the forecast period (2025-2030).

Robust demand stems from manufacturers seeking additives that keep coatings, polymers, and fluids stable under heat, chemicals, and harsh weather. Regulatory pressure to cut volatile-organic-compound (VOC) emissions is steering formulators toward silicone-rich systems that match performance with compliance . Growth momentum also reflects deeper penetration in thermal management for electric vehicles, bio-based personal-care launches, and rising food-processing automation across emerging economies. Industry consolidation-most notably KCC's take-over of Momentive in 2024-signals a shift toward scale advantages, vertical integration, and faster innovation pipelines.

Global Silicone Additives Market Trends and Insights

Increase in Demand from Personal Care Industry

Consumers gravitate toward light, non-oily textures, prompting formulators to favor silicone fluids for silky spread and lasting moisture. Shin-Etsu's elastomer-in-oil line, for example, builds stable oil-in-water emulsions that meet regional bans on cyclic siloxanes while sustaining the desired skin-feel. Suppliers are rolling out plant-origin C13-15 alkane carriers such as Elkem's PURESIL ORG gels, proving that sensory performance and natural positioning can coexist. Asia-Pacific labels are leveraging these attributes to bridge gaps with global premium brands, widening the silicone additives market in color cosmetics and sun care.

Growing Focus on Low-VOC Products in Paints and Coatings

Legislators in Europe and North America cap allowable solvent content, making low-VOC compliance a prerequisite rather than a feature. Evonik's TEGO Guard 9000 delivers early-rain resistance in exterior coatings without breaching eco-label thresholds. Siltech has shown that long-chain alkyl silicones lift solids content yet cut VOC totals, letting formulators maintain durability while meeting Green Seal or LEED targets. The ripple effect extends to emerging markets, where builders increasingly specify water-based paints fortified with silicone surface additives for stain repellence and long-term color retention.

Additive Migration at High Temperatures

Above 200 °C, low-molecular-weight siloxanes can bleed to surfaces, dulling optical clarity or weakening adhesion. Studies on high-phenyl silicone rubbers reveal improved thermal stability, with only 5% weight loss at 478 °C, yet premium grades raise costs. EV traction motors and aerospace ducting need formulations that curb volatilization, pressuring R&D budgets.

Other drivers and restraints analyzed in the detailed report include:

- Growing Demand from Food-Processing Industry

- Increasing Usage in Medical and Healthcare Applications

- Volatile Raw-Material Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Silicone fluids accounted for 39.44% of the silicone additives market in 2024 by revenue, riding on wide use as slip, leveling, and heat-transfer agents in coatings, personal care, and lubricants. Their low surface tension and broad temperature stability underpin a resilient demand base. Emulsions and resins complement fluids by enabling water-borne systems and structural finishes, particularly in construction sealants. In contrast, elastomers address gasket, seal, and medical-tube niches needing lasting elasticity.

Powders and granules, although less than one-quarter of sales, post the fastest 7.65% CAGR through 2030. Their dry format aids 3D printing feedstocks and masterbatch compounding, granting formulators fine rheology control and dust-free dosing. Emerging UV-curable polysiloxane powders simplify on-demand cross-linking for rapid prototypes, shrinking design-to-part cycles and enlarging the silicone additives market size for additive manufacturing. As printer fleets spread beyond aerospace into dental and consumer goods, powdered silicones capture fresh avenues for growth.

The Silicone Additives Market Report is Segmented by Product Form (Fluids and Oils, Elastomers and Gums, and More), Application (Defoamers, Rheology Modifiers, and More), End-User Industry (Food and Beverage, Plastics and Composites, and More), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific sat atop the silicone additives market with 47.34% revenue share in 2024 and is marching at a 7.10% CAGR toward 2030. China's Zhangjiagang and Nanjing clusters anchor upstream siloxane capacity for Wacker and Elkem, ensuring supply proximity to electronics and EV battery giants. India's "Make in India" policy stokes domestic demand for quality-driven coatings and adhesives, compelling local formulators to incorporate silicone additives for premium finish and durability. Japan and South Korea each foster advanced R&D, channeling silicone additives into high-frequency electronics, photonics, and specialty films.

North America follows as a mature but innovation-rich arena. The United States leads adoption in medical devices and aerospace composites, relying on FDA/USP compliant silicone systems. Dow's silicone recycling pilot in Michigan aims to trim polydimethylsiloxane (PDMS) carbon footprints by 50% and resonates with buyers under ESG mandates. Canada's EV-battery investments and Mexico's automotive clusters promise incremental pull-through for thermal-management additives.

Europe ranks third in size yet first in sustainability stringency. REACH and impending PFAS bans intensify R&D for cyclic-free and bio-based silicone alternatives. Evonik's Smart Effects business line combines siloxane and organic specialties to tackle lightweighting, e-mobility, and digital health markets. Germany and France concentrate vehicle electrification grants, while the United Kingdom emphasizes life-science coatings, collectively protecting a steady flow of high-margin orders.

- AB Specialty Silicones

- Altana AG

- Bluestar Silicones

- BRB International

- Clariant AG

- Dow

- Elkem ASA

- Evonik Industries AG

- Jiangsu Maysta Chemical

- KCC SILICONE CORPORATION

- Momentive

- Shin-Etsu Chemical Co., Ltd.

- Silibase Silicone

- Siltech Corporation

- Supreme Silicones India Pvt. Ltd.

- The Lubrizol Corporation

- Wacker Chemie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increase in Demand from Personal Care Industry

- 4.2.2 Growing Focus on Low-VOC Products in Paints and Coatings

- 4.2.3 Growing Demand from Food-Processing Industry

- 4.2.4 Increasing Usage in Medical and Healthcare Applications

- 4.2.5 High Utilization from the Automotive Industry

- 4.3 Market Restraints

- 4.3.1 Additive Migration at High Temperatures

- 4.3.2 Volatile Raw-material Costs

- 4.3.3 Technical Challenges such as Migration and Adhesion Issues

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts

- 5.1 By Product Form

- 5.1.1 Fluids and Oils

- 5.1.2 Elastomers and Gums

- 5.1.3 Resins

- 5.1.4 Powders and Granules

- 5.1.5 Emulsions

- 5.2 By Application

- 5.2.1 Defoamers

- 5.2.2 Rheology Modifiers

- 5.2.3 Surfactants

- 5.2.4 Wetting and Dispersing Agents

- 5.2.5 Lubricating Agents

- 5.2.6 Adhesion Promoters

- 5.2.7 Other Applications (Release Agents, etc.)

- 5.3 By End-User Industry

- 5.3.1 Food and Beverage

- 5.3.2 Plastics and Composites

- 5.3.3 Paints and Coatings

- 5.3.4 Personal Care

- 5.3.5 Adhesives and Sealants

- 5.3.6 Paper and Pulp

- 5.3.7 Oil and Gas

- 5.3.8 Other End-User Industries (Electronics and Semiconductor, etc.)

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 AB Specialty Silicones

- 6.4.2 Altana AG

- 6.4.3 Bluestar Silicones

- 6.4.4 BRB International

- 6.4.5 Clariant AG

- 6.4.6 Dow

- 6.4.7 Elkem ASA

- 6.4.8 Evonik Industries AG

- 6.4.9 Jiangsu Maysta Chemical

- 6.4.10 KCC SILICONE CORPORATION

- 6.4.11 Momentive

- 6.4.12 Shin-Etsu Chemical Co., Ltd.

- 6.4.13 Silibase Silicone

- 6.4.14 Siltech Corporation

- 6.4.15 Supreme Silicones India Pvt. Ltd.

- 6.4.16 The Lubrizol Corporation

- 6.4.17 Wacker Chemie AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Analysis

- 7.2 Growing Research and Development to Improve the Sustainability of Silicones

矽酮添加劑市場-2026-2032年全球市場預測

矽酮添加劑市場-2026-2032年全球市場預測 矽酮改質劑市場規模、佔有率和成長分析:按產品類型、配方類型、應用、最終用途行業、銷售管道和地區分類 - 2026-2033 年行業預測

矽酮改質劑市場規模、佔有率和成長分析:按產品類型、配方類型、應用、最終用途行業、銷售管道和地區分類 - 2026-2033 年行業預測 全球矽酮添加劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球矽酮添加劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 矽酮添加劑市場-全球產業規模、佔有率、趨勢、機會及按功能、應用、地區和競爭格局分類的預測(2021-2031年)矽膠拖鞋市場按類型、應用、終端用戶產業及銷售管道分類-2026-2032年全球預測

矽酮添加劑市場-全球產業規模、佔有率、趨勢、機會及按功能、應用、地區和競爭格局分類的預測(2021-2031年)矽膠拖鞋市場按類型、應用、終端用戶產業及銷售管道分類-2026-2032年全球預測 全球有機矽添加劑市場規模研究與預測:依功能、最終用途產業和區域預測 2025-2035

全球有機矽添加劑市場規模研究與預測:依功能、最終用途產業和區域預測 2025-2035