|

市場調查報告書

商品編碼

1844730

氧化鎂奈米粉末:市場佔有率分析、產業趨勢、統計數據、成長預測(2025-2030)Magnesium Oxide Nanopowder - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

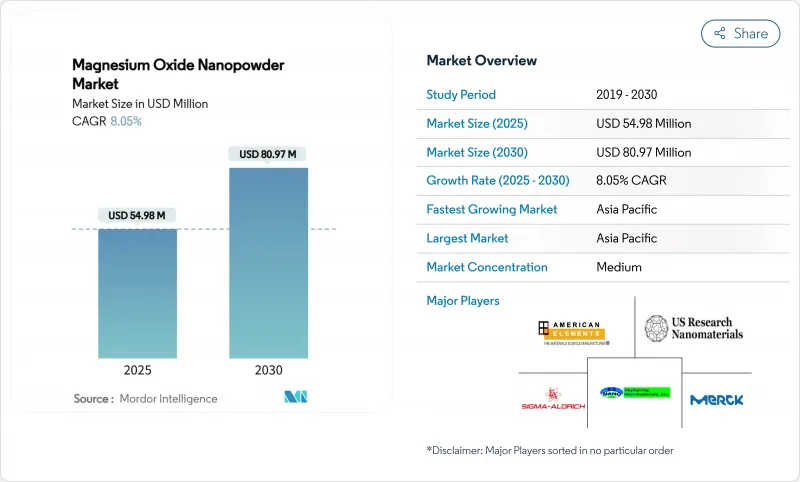

預計 2025 年氧化鎂奈米粉末市場規模為 5,498 萬美元,到 2030 年將達到 8,097 萬美元,預測期內(2025-2030 年)的複合年成長率為 8.05%。

雖然大部分收益仍來自傳統的耐火材料需求,但發展勢頭明顯轉向更高價值的應用,例如燃料添加劑、電絕緣材料、阻燃聚合物化合物以及早期固態電池原型。到2024年,中國原鎂產量的佔有率將達到52%,這將為亞洲加工商帶來成本優勢,但也使全球買家面臨政策驅動的市場波動。競爭優勢越來越依賴專有的合成路線,以實現先進複合材料和電解質所需的窄粒度分佈和功能化表面。最後,北美和歐盟對職場接觸工程奈米材料的監管日益嚴格,這增加了合規成本,但有利於擁有認證品質系統的成熟製造商。

全球氧化鎂奈米粉市場趨勢與洞察

耐火材料產業需求不斷成長

添加了奈米氧化鎂的鎂碳磚在鹼性氧氣轉爐和電弧爐中表現出更高的緻密性,並減少了因孔隙率而導致的破損。中國、日本和韓國的鋼鐵製造商已將奈米粉末等級標準化,用於鋼包、中間包和連鑄機的內襯,以承受快速熱循環。綜合性鋼鐵製造商之間的整合意味著更少的買家擁有更大的購買力,但他們願意為避免意外停機的可靠性支付額外費用。隨著亞太地區電弧爐產能的擴大,市場對氧化鎂奈米粉末的需求與廢鋼產量的成長密切相關。擁有垂直整合生產和耐火材料配方專業知識的產業供應商能夠獲得以合作研發協議為基礎的長期合約。

電氣絕緣應用的成長

含有 1 wt% 氧化鎂奈米顆粒的環氧系統在 230 度C時的介電常數為 13,熱傳導率是未填充樹脂的兩倍。這些特性解決了碳化矽功率模組和牽引逆變器中散熱和電阻率之間長期存在的矛盾。超過 800 V 的電動車傳動系統電壓加上較小的外形規格,推動了對即使在局部放電條件下也具有化學惰性的高溫絕緣填料的需求。亞太地區電纜製造商正在擴大填充冷凍乾燥氧化鎂泡沫的聚乙烯化合物的規模,這可以抑制空間電荷的積聚。隨著風力發電機逆變器容量的增加,歐洲公用事業公司也開始為離岸變電站指定填充奈米顆粒的灌封膠。

製造和精煉成本高

一個日產1,425公斤的溶膠-凝膠工廠需要超過4.5萬美元的資本支出,在現行定價結構下,投資回收期超過三年。能源密集的熱液和脫碳製程增加了對歐盟和美國某些州碳定價的敏感度。純度規格嚴格於99.8 wt%會增加試劑和過濾成本,而這些成本無法在產品產量上攤提。亞太地區以外的小型生產商面臨規模劣勢,限制了它們競標大型耐火材料競標和汽車添加劑供應合約的能力。

細分分析

到2024年,耐火材料將佔氧化鎂奈米粉末市場規模的42.65%,主要用於鎂碳磚以及用於鋼和鋁熔體加工的中間包襯裡。改良的電弧爐技術有利於細顆粒分佈,使磚塊的微觀結構更加緻密。隨著廢鋼在亞洲的普及,節能襯裡對生產力仍然至關重要。雖然預計耐火材料市場領導地位將持續到2030年,但隨著新應用的擴展,其佔有率將下降。

到2030年,燃油添加劑類別的複合年成長率將達到8.86%,這反映出前所未有的監管壓力,即要求減少公路和非公路車輛的顆粒物和氮氧化物排放。奈米顆粒分散體可改善霧化效果,提高火焰溫度均勻性,並減少煙灰前驅物,同時不會影響引擎硬體的保固。歐盟和中國的試點車隊測試報告顯示,燃油經濟性提升超過2%。雖然該細分基準的起步規模較小,但其成長速度正成為那些瞄準尋求即插即用解決方案的汽車客戶的製造商的焦點。

區域分析

預計到2024年,亞太地區將佔氧化鎂奈米粉末市場收益的52.18%,到2030年,複合年成長率將達到8.76%。該地區的需求主要由中國推動,而日本的陶瓷專業知識和韓國的半導體生態系統將進一步推動超高純度等級的需求。政府針對能源轉型硬體的獎勵策略將推動電動車溫度控管和固態電池中試線產量的增加。

北美面積雖小,但技術含量卻十分豐富,其高規格粉末廣泛應用於航太、國防和先進電力電子領域。美國已強制要求國內供應安全,像Magratia這樣的新興企業正在試行從海水中提取碳中和中性的鎂。加拿大的關鍵礦產策略包括提供津貼,以降低奈米粉末精整線的資本門檻,這可能會使該地區從特種粉末進口國轉變為出口國。

隨著建築法規收緊阻燃標準,以及汽車製造商採用富含鎂的電動車零件,歐洲市場保持穩定成長。德國憑藉其汽車和化學工業引領鎂的消費,而英國則在航太和國防計劃率先推出需要高溫隔熱。歐盟循環經濟法規鼓勵使用礦物基阻燃填料而非鹵素替代品,這為氧化鎂奈米粉末市場提供了監管方面的推動。歐盟能源戰略指令也正在推動固態電池聯盟的資金投入,而氧化鎂在其中扮演關鍵的介面角色。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場狀況

- 市場概況

- 市場促進因素

- 耐火材料產業需求不斷成長

- 電氣絕緣應用的成長

- 擴大作為燃料添加劑的用途

- 擴大在阻燃聚合物複合材料的應用

- 固態電池電解質的新作用

- 市場限制

- 製造和精煉成本高

- 凝結和絮凝問題

- 加強職場奈米顆粒暴露監管

- 揮發性鎂原料供應

- 價值鏈分析

- 五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章市場規模及成長預測

- 按用途

- 耐火材料

- 電絕緣

- 燃料添加劑

- 阻燃劑

- 磁性設備

- 其他(催化劑、吸附劑、生物醫學等)

- 依合成方法

- 物理方法

- 化學沉澱法

- 綠色/生物基合成

- 按最終用戶產業

- 冶金

- 建造

- 石油和天然氣

- 車

- 電氣和電子

- 其他終端用戶產業(化學品和石化產品、醫療保健和製藥等)

- 按地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 東南亞國協

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭態勢

- 市場集中度

- 策略舉措

- 市佔率(%)/排名分析

- 公司簡介

- Alfa Aesar(Thermo Fisher)

- American Elements

- Ascensus

- Grecian Magnesite

- High Purity Laboratory Chemicals Pvt. Ltd.

- Hongwu International Group Ltd

- Inframat Advanced Materials

- Martin Marietta Magnesia Specialties

- Merck KGaA

- Nanografi Advanced Materials.

- Nanoshel LLC

- Nanostructured & Amorphous Materials, Inc.

- Platonic Nanotech

- Sigma-Aldrich(MilliporeSigma)

- SkySpring Nanomaterials, Inc.

- Tateho Chemical Industries Co.,Ltd.

- US Research Nanomaterials, Inc.

第7章 市場機會與未來展望

The Magnesium Oxide Nanopowder Market size is estimated at USD 54.98 Million in 2025, and is expected to reach USD 80.97 Million by 2030, at a CAGR of 8.05% during the forecast period (2025-2030).

Most revenue still flows from legacy refractory demand, yet momentum is clearly shifting toward high-value applications in fuel additives, electrical insulation, flame-retardant polymer compounds and early solid-state battery prototypes. Supply security is shaped by China's 52% share of primary magnesium production in 2024, which delivers cost advantages for Asian processors but exposes global buyers to policy-driven volatility. Competitive positioning increasingly depends on proprietary synthesis routes that deliver narrow particle-size distributions and functionalized surfaces needed in advanced composites and electrolytes. Finally, tightening workplace-exposure limits for engineered nanomaterials in North America and the EU are raising compliance costs, but they also favour established producers with certified quality systems.

Global Magnesium Oxide Nanopowder Market Trends and Insights

Rising Demand from Refractory Industry

Magnesia-carbon bricks incorporating nanoscale magnesium oxide show higher densification that lowers porosity-induced failure in basic oxygen and electric arc furnaces. Steelmakers in China, Japan and South Korea have standardised nanopowder grades in ladle, tundish and continuous-caster linings to withstand rapid thermal cycling. Consolidation among integrated steel producers means fewer buyers wield greater purchasing power, but they pay premiums for reliability that avoids unplanned shutdowns. As electric arc furnace capacity expands across Asia-Pacific, magnesium oxide nanopowder market demand remains closely correlated with rising scrap-based steel output. Suppliers with vertically integrated production and refractory formulation expertise can capture long-term contracts anchored in joint R&D agreements.

Growth in Electrical Insulation Applications

Epoxy systems loaded with 1 wt% magnesium oxide nanoparticles maintain a dielectric constant of 13 at 230 °C and double the thermal conductivity versus neat resin. These attributes solve the chronic trade-off between heat dissipation and electrical resistivity in silicon carbide power modules and traction inverters. Electric-vehicle drive-train voltages above 800 V, combined with miniaturised form factors, amplify the need for high-temperature insulation fillers that stay chemically inert under partial discharge. Asia-Pacific cable makers are scaling polyethylene compounds filled with freeze-dried magnesium oxide foams that suppress space-charge accumulation. As wind-turbine inverters grow in capacity, European utilities are also specifying nanoparticle-filled potting compounds for offshore substations.

High Production and Purification Costs

Sol-gel plants capable of 1,425 kg day-1 output require capital spending above USD 45,000 and return on investment stretches beyond three years under today's price structure. Energy-intensive hydrothermal and calcination steps heighten sensitivity to carbon-pricing trajectories in the EU and selected US states. Purity specifications tighter than 99.8 wt% raise reagent and filtration costs that cannot be amortised across commodity volumes. Smaller producers outside Asia-Pacific face scale disadvantages, which limits their ability to bid for large refractory tenders or automotive additive supply contracts.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Use as Fuel Additive

- Expanding Adoption in Flame-Retardant Polymer Composites

- Aggregation and Agglomeration Issues

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Refractory materials generated 42.65% of the magnesium oxide nanopowder market size in 2024, anchored in magnesia-carbon bricks and tundish linings for steel and aluminium melt processing. Technical upgrades in electric arc furnaces favour finer particle distributions that densify brick microstructures. As scrap-based steel makes deeper inroads across Asia, energy-efficient linings remain critical for productivity. Market leadership is expected to persist through 2030, though its proportional share will slip as newer uses scale.

The fuel-additive category shows an 8.86% CAGR to 2030, reflecting unprecedented regulatory pressure to cut particulate and NOx emissions in both on-road and off-road fleets. Nanoparticle dispersions improve atomisation, raise flame temperature uniformity and reduce soot precursors without compromising engine hardware warranties. Pilot fleet tests in the EU and China report fuel-economy gains above 2%. Although the segment starts from a small baseline, its growth pace makes it a focal point for producers targeting automotive clients seeking drop-in solutions.

The Magnesium Oxide Nanopowder Market Report is Segmented by Application (Refractory Materials, Electric Insulation, Fuel Additive and More), Synthesis Method (Physical Method, Chemical Precipitation, and More), End-User Industry (Auto Metallurgy, Construction, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific owned 52.18% of 2024 revenue in the magnesium oxide nanopowder market and is forecast to advance at an 8.76% CAGR through 2030, underpinned by integrated supply chains, cost-advantaged feedstock and dense clusters of steel, electronics and battery manufacturers. China anchors regional demand, yet Japan's ceramics expertise and South Korea's semiconductor ecosystem provide incremental pull for ultra-high-purity grades. Government stimulus aimed at energy-transition hardware drives additional volume in electric-vehicle thermal management and solid-state battery pilot lines.

North America is a smaller but technologically rich arena in which aerospace, defence and advanced power electronics consume high-spec powders. The United States requisitioned domestic supply security measures, and start-ups such as Magrathea are piloting carbon-neutral magnesium extraction from seawater, which could de-risk feedstock procurement and reinforce local value chains by the late 2020s. Canada's critical-minerals strategy includes grants that lower capital hurdles for nanopowder finishing lines, potentially repositioning the region as an exporter of specialty grades rather than an importer.

Europe maintains steady growth as building codes tighten flame-retardancy thresholds and automakers adopt magnesium-rich e-mobility components. Germany leads consumption due to its automotive and chemical base, whereas the United Kingdom taps aerospace and defence projects requiring high-temperature insulation. EU circular-economy regulations encourage mineral-based fire-retardant fillers over halogenated alternatives, offering regulatory tailwinds for magnesium oxide nanopowder market expansion. The bloc's energy-strategy directives also channel funds into solid-state battery consortia where MgO plays a critical interface role.

- Alfa Aesar (Thermo Fisher)

- American Elements

- Ascensus

- Grecian Magnesite

- High Purity Laboratory Chemicals Pvt. Ltd.

- Hongwu International Group Ltd

- Inframat Advanced Materials

- Martin Marietta Magnesia Specialties

- Merck KGaA

- Nanografi Advanced Materials.

- Nanoshel LLC

- Nanostructured & Amorphous Materials, Inc.

- Platonic Nanotech

- Sigma-Aldrich (MilliporeSigma)

- SkySpring Nanomaterials, Inc.

- Tateho Chemical Industries Co.,Ltd.

- US Research Nanomaterials, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand from refractory industry

- 4.2.2 Growth in electrical insulation applications

- 4.2.3 Increasing use as fuel additive

- 4.2.4 Expanding adoption in flame-retardant polymer composites

- 4.2.5 Emergent role in solid-state battery electrolytes

- 4.3 Market Restraints

- 4.3.1 High production and purification costs

- 4.3.2 Aggregation and agglomeration issues

- 4.3.3 Tightening workplace exposure regulations for nanoparticles

- 4.3.4 Volatile magnesium feedstock supply

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size & Growth Forecasts (Value)

- 5.1 By Application

- 5.1.1 Refractory Materials

- 5.1.2 Electric Insulation

- 5.1.3 Fuel Additive

- 5.1.4 Fire Retardent

- 5.1.5 Magnetic Devices

- 5.1.6 Others (Catalysts & Adsorbents,Biomedical, etc.)

- 5.2 By Synthesis Method

- 5.2.1 Physical Methods

- 5.2.2 Chemical Precipitation

- 5.2.3 Green/Bio-based Synthesis

- 5.3 By End-user Industry

- 5.3.1 Metallurgy

- 5.3.2 Construction

- 5.3.3 Oil & Gas

- 5.3.4 Automotive

- 5.3.5 Electrical & Electronics

- 5.3.6 Other End-user Industries (Chemical & Petrochemical,Healthcare & Pharmaceuticals, etc.)

- 5.4 By Geography (Value)

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Alfa Aesar (Thermo Fisher)

- 6.4.2 American Elements

- 6.4.3 Ascensus

- 6.4.4 Grecian Magnesite

- 6.4.5 High Purity Laboratory Chemicals Pvt. Ltd.

- 6.4.6 Hongwu International Group Ltd

- 6.4.7 Inframat Advanced Materials

- 6.4.8 Martin Marietta Magnesia Specialties

- 6.4.9 Merck KGaA

- 6.4.10 Nanografi Advanced Materials.

- 6.4.11 Nanoshel LLC

- 6.4.12 Nanostructured & Amorphous Materials, Inc.

- 6.4.13 Platonic Nanotech

- 6.4.14 Sigma-Aldrich (MilliporeSigma)

- 6.4.15 SkySpring Nanomaterials, Inc.

- 6.4.16 Tateho Chemical Industries Co.,Ltd.

- 6.4.17 US Research Nanomaterials, Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

全球氧化鎂奈米粉市場報告(2026 年)

全球氧化鎂奈米粉市場報告(2026 年) 氧化鎂奈米粉市場規模、佔有率及成長分析(依產品類型、粒徑、應用、終端用戶產業及地區分類)-2026-2033年產業預測

氧化鎂奈米粉市場規模、佔有率及成長分析(依產品類型、粒徑、應用、終端用戶產業及地區分類)-2026-2033年產業預測 全球氧化鎂奈米粉市場:產業分析、規模、佔有率、成長、趨勢與預測(2025-2032)

全球氧化鎂奈米粉市場:產業分析、規模、佔有率、成長、趨勢與預測(2025-2032)