|

市場調查報告書

商品編碼

1844709

汽車安全系統:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)Automotive Safety Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

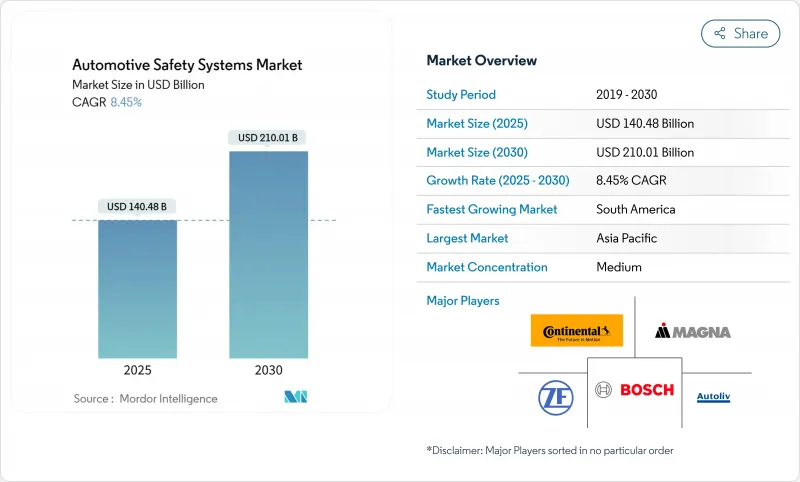

預計 2025 年汽車安全系統市場規模為 1,404.8 億美元,到 2030 年將達到 2,100.1 億美元,預測期內(2025-2030 年)的複合年成長率為 8.45%。

需求反映了全球安全法規的同步演變、感測器成本的快速下降以及可透過無線升級的軟體定義汽車的興起。從純硬體約束系統到整合感測器和軟體平台的轉變,使汽車能夠即時預測、避免和減輕碰撞。汽車製造商現在已將主動煞車、車道維持、駕駛員監控和網路安全更新路徑作為標準配備。

全球汽車安全系統市場趨勢與洞察

加強全球NCAP和聯合國歐洲經濟委員會的安全義務

2026 年歐洲新車安全評估協會 (Euro NCAP)通訊協定將強制所有車型配備行人自動緊急煞車和駕駛員監控功能,從而建立通用的合規基準。中國工業和資訊化部於 2025 年訂定法規,要求對涉及安全功能的每次軟體更新進行型式核准。歐盟通用安全法規 II 將於 2024 年 7 月生效,要求所有新車配備智慧速度援助和緊急車道維持功能。美國國家公路交通安全管理局 (NHTSA) 更新了其新車評估程序,將盲點警告、車道維持輔助和行人 AEB 納入 2026 年車型。全球協調使製造商能夠將開發成本分攤到更多車輛上,從而促進先進功能的快速採用。

感測器成本快速下降推動ADAS標準化

汽車雷達價格每年下降近 18%,而處理器性能每 18 個月加倍,從而能夠以入門級價格分佈實現高性能感知。 4D 成像雷達以接近傳統3D裝置的成本提供公分級的偵測精度,將應用範圍擴展到主動式車距維持定速系統之外。影像感測器受益於智慧型手機供應鏈:帶有 HDR 的 8 兆像素汽車晶片售價不到 10 美元。 NITI Aayog 預測,在 ADAS 內容的推動下,到 2030 年每輛汽車的半導體價值將加倍,達到 1,200 美元。成本下降將使汽車安全系統市場能夠將 1 級和 2 級功能擴展到在亞洲和拉丁美洲銷售的小型車。

為滿足多個國家法規,驗證和認證成本高昂

製造商必須將中國C-NCAP 2024的測試矩陣與歐洲NCAP 2026的要求進行協調,通常在類似場景下重複進行檢驗和軟體檢驗。 TÜV南德意志集團目前根據歐盟法規執行強制性滲透測試,並在上市前增加數月的網路安全審查。 ISO/SAE 21434要求在車輛的整個生命週期內進行威脅分析,這延長了開發週期,並增加了小型汽車製造商的成本。這些因素減緩了成本敏感型市場對尖端功能的採用,並在協調性改善之前限制了部分汽車安全系統市場的發展。

細分分析

主動式安全系統預計將佔據汽車安全系統市場的最大佔有率,到2024年將佔市場規模的67.13%。隨著歐洲新車安全評估協會(Euro NCAP)和美國國家公路交通安全管理局(NHTSA)的通訊協定日益嚴格,自動緊急煞車、自我調整巡航、車道維持和駕駛員監控等功能現已開始應用於中階車型。隨著供應商透過即時運行機器學習模型的網域控制器整合雷達、攝影機和雷射雷達數據,競爭將更加激烈。該領域也受益於車隊需求,保險公司為配備防撞技術的卡車提供保費折扣。

車載生物辨識平台是成長最快的細分市場,到2030年複合年成長率將達到8.11%。這些解決方案可以追蹤駕駛者的警覺性、心率甚至血氧飽和度,以便在危險情況出現之前發出預警。座艙感知器與主動煞車控制器相連,為乘客提供可預測外部和內部威脅的閉合迴路安全保護。被動安全領域仍然很重要,例如智慧安全氣囊和自我調整安全帶,它們可以適應自動駕駛汽車的新座椅佈局,但成長速度較慢。

雷達模組採用經濟高效的77GHz晶片組,可在雨雪和霧天可靠運行,到2024年將佔據汽車安全系統市場的34.36%。轉向4D成像雷達將透過提高角度解析度、降低物料清單成本來實現物體分類,縮小與LiDAR的性能差距。相機系統將繼續利用智慧型手機的經濟性,使OEM能夠為停車和低速操控添加360度全景視野。

LiDAR (LiDAR) 成長最快,複合年成長率達 8.75%,這得益於固態架構,可減少移動部件並降低單一感測器的成本。高階轎車的 L3 級高速公路自動駕駛依靠前向LiDAR進行冗餘深度感知和道路碎片檢測,從而加速了其普及。控制單元將煞車、轉向和感知數據整合到單一晶片上,從而減少了佈線並減輕了重量。隨著汽車安全系統市場朝向預測性安全邁進,將自學習演算法應用於邊緣處理器的軟體創新將使供應商脫穎而出。

區域分析

到2024年,亞太地區將以39.84%的市佔率繼續保持在汽車安全系統市場的最大地位。中國工信部法規要求每次ADAS軟體更新都必須核准,從而建構了一個強大的合規生態系統,加速了功能的部署。科技與汽車的融合體現在華為和小鵬汽車等夥伴關係中,他們共同開發了一款網域控制器,將雷達、攝影機和雷射雷達整合在一個通用軟體堆疊上。日本正在培育人工智慧主導的新興企業,在城市中心試運行自動駕駛班車;而印度日益嚴格的碰撞法規則推動了緊湊型汽車對成本最佳化的安全氣囊和自動緊急煞車系統(AEB)的需求。

南美洲將達到最高成長,到2030年複合年成長率將達到8.77%。 Stellantis將在2025年至2030年期間投資56億歐元,在當地工廠推出40多款符合歐洲新車安全評鑑協會(Euro NCAP)測試通訊協定的車款。巴西、阿根廷及其周邊市場的安全法規將實現協調,允許全球供應商複製高效的感測器套件,而無需進行客製化調校。生物混合動力傳動系統將結合乙醇引擎和電池組,其熱安全系統和電氣安全系統將迎來新的整合工作。

北美和歐洲憑藉較高的單車配置率和軟體定義汽車法規,保持成熟的市場地位。雖然這些地區的汽車安全系統市場佔有率保持穩定,但由於聯合國歐洲經濟委員會第155號法規要求全面網路安全,並要求所有安全電子控制單元(ECU)符合反駭客標準,其單位價值正在上升。在基礎設施擴張的推動下,中東和非洲地區正從低基準邁進,而當地極端氣候條件也推動了對堅固耐用的感測器外殼和防塵雷達外殼的需求。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場狀況

- 市場概況

- 市場促進因素

- 加強全球NCAP和UNECE安全指令

- 感測器成本快速下降推動ADAS標準化

- 軟體定義汽車的繁榮(OTA安全功能升級)

- 商用車輛轉向 2 級以上自動駕駛(車隊 TCO Play)

- 基於人工智慧的車載生物安全分析(疲勞、生命徵象)的興起

- 將車輛安全資料捆綁到應用程式中

- 市場限制

- 為符合各國法規,驗證及認證成本高昂

- 晶片組供應不確定性延後OEM安全推出

- 安全 ECU 和感測器匯流排遭受網路物理攻擊的風險

- 800V電池電力中的高壓電磁干擾(EMI)與熱負荷

- 價值/供應鏈分析

- 監管狀況

- 技術展望

- 五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭強度

第5章市場規模及成長預測

- 依系統類型

- 主動安全系統

- 防撞(AEB、FCW)

- 駕駛員監控和 HMI 警報

- 底盤控制(ESC、ABS)

- 被動安全系統

- 安全氣囊(前部、側面、窗簾、遠端)

- 安全帶和預張力器

- 主動安全系統

- 按下技術組件

- 感應器

- 雷達

- 相機

- LiDAR/超音波

- 控制單元和網域控制器

- 軟體和演算法

- 按最終用戶

- OEM工廠適配

- 售後市場/改裝

- 按車輛類型

- 搭乘用車

- 輕型商用車

- 大型商用車和公車

- 透過推進力

- 內燃機(ICE)

- 純電動車(BEV)

- 混合動力電動車(HEV)

- 燃料電池電動車(FCEV)

- 按地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 其他亞太地區

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 南非

- 其他中東和非洲地區

- 北美洲

第6章 競爭態勢

- 市場集中度

- 策略舉措

- 市佔率分析

- 公司簡介

- Robert Bosch GmbH

- Continental AG

- ZF Friedrichshafen AG

- Autoliv Inc.

- Denso Corporation

- Aptiv PLC

- Magna International Inc.

- Joyson Safety Systems

- Mobileye NV

- Valeo SA

- Hitachi Astemo

- Hyundai Mobis

- NXP Semiconductors

- Infineon Technologies AG

- Texas Instruments Inc.

- Renesas Electronics Corp.

- Veoneer AB

- WABCO(ZF CV Systems)

- Bendix Commercial Vehicle Systems

- Lear Corporation(E-Systems)

第7章 市場機會與未來展望

The Automotive Safety Systems Market size is estimated at USD 140.48 billion in 2025, and is expected to reach USD 210.01 billion by 2030, at a CAGR of 8.45% during the forecast period (2025-2030).

Demand reflects simultaneous progress in global safety regulation, rapid sensor price erosion, and the rise of software-defined vehicles that permit over-the-air upgrades. The shift from hardware-only restraint devices toward integrated sensor-plus-software platforms allows vehicles to predict, avoid, and mitigate collisions in real time. Automakers now package active braking, lane keeping, driver monitoring, and cyber-secure update pathways as standard content, especially in markets where star-rating programs influence buying behavior.

Global Automotive Safety Systems Market Trends and Insights

Tightening Global NCAP & UNECE Safety Mandates

Euro NCAP protocols for 2026 require pedestrian automatic emergency braking and driver monitoring across all model classes, creating a common compliance baseline. China's Ministry of Industry and Information Technology introduced rules in 2025 that obligate type approval for every software update touching safety functions. The EU General Safety Regulation II, in force since July 2024, obliges intelligent speed assistance and emergency lane keeping on every new vehicle. NHTSA updated its New Car Assessment Program to add blind-spot warning, lane keeping assistance, and pedestrian AEB for 2026 models, signaling a decade-long push for active safety. Global alignment lets manufacturers spread development cost across larger volumes and catalyzes faster diffusion of advanced functions.

Rapid Sensor-Cost Deflation Enabling ADAS Standardisation

Automotive radar prices now fall nearly 18% each year, while processor capability doubles every 18 months, permitting high-performance perception at entry-segment price points. Four-dimensional imaging radar brings centimeter-grade detection accuracy at cost levels close to legacy 3-D units, broadening use beyond adaptive cruise control. Image sensors benefit from smartphone supply chains: 8-megapixel automotive chips with HDR are available below USD 10. NITI Aayog projects semiconductor value per vehicle to double to USD 1,200 by 2030, led by ADAS content. The declining cost curve allows the automotive safety system market to extend Level-1 and Level-2 features to compact cars sold in Asia and Latin America.

High Validation & Homologation Cost for Multicountry Compliance

Manufacturers must reconcile China's C-NCAP 2024 test matrix with Euro NCAP 2026 requirements, often repeating crash and software validation for similar scenarios. TUV SUD now runs mandatory penetration testing under EU rules, adding months of cybersecurity reviews before market release. ISO/SAE 21434 demands threat analysis across the full vehicle lifecycle, lengthening development schedules and raising costs for small automakers. These factors slow the spread of cutting-edge features in cost-sensitive markets, restraining part of the automotive safety system market until harmonisation improves.

Other drivers and restraints analyzed in the detailed report include:

- Boom in Software-Defined Vehicles (OTA Safety Feature Upgrades)

- Shift Toward Level-2+ Autonomy in Commercial Vehicles (Fleet TCO Play)

- Chip-Set Supply Volatility Delaying OEM Safety Roll-Outs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Active Safety Systems generated the largest slice of the automotive safety system market size at 67.13% in 2024. Automated emergency braking, adaptive cruise, lane keeping, and driver monitoring now appear in mid-range trims as Euro NCAP and NHTSA protocols grow stricter. Competitive intensity rises as suppliers integrate radar, camera, and LiDAR data through domain controllers that run machine-learning models in real time. The segment also benefits from fleet demand, with insurers offering premium discounts for trucks equipped with crash-avoidance technology.

In-cabin biometric platforms stand out as the fastest subsegment, advancing at an 8.11% CAGR to 2030. These solutions track driver alertness, heart rate, and even oxygen saturation, issuing proactive warnings before dangerous conditions emerge. As cabin sensors link with active braking controllers, occupants receive a closed-loop safety envelope that anticipates both external and internal threats. Passive safety remains relevant through smart airbags and adaptive seat belts that fit new seat layouts in autonomous vehicles, yet growth stays moderate.

Radar modules accounted for 34.36% of the automotive safety system market in 2024, underpinned by cost-effective 77-GHz chipsets that function reliably in rain, snow, and fog. The move to 4-D imaging radar sharpens angle resolution and permits object classification, narrowing the performance gap with LiDAR at a lower bill of materials. Camera systems continue to leverage smartphone economics, letting OEMs add 360-degree vision for parking and low-speed manoeuvres.

LiDAR registers the quickest expansion at an 8.75% CAGR, supported by solid-state architectures that trim moving parts and cut price per sensor. Level-3 highway-pilot launches in premium sedans rely on forward-facing LiDAR for redundant depth perception and road debris detection, accelerating adoption. Control units merge braking, steering, and perception data into single chips, reducing wiring and weight. Software innovations that apply self-learning algorithms on edge processors differentiate suppliers as the automotive safety system market transitions toward predictive safety.

The Automotive Safety System Market Report is Segmented by System Type (Active Safety Systems and Passive Safety Systems), Technology Component (Sensors, Radar, Camera, and More), End User (OEM and Aftermarket), Vehicle Type (Passenger Car, Light Commercial Vehicle, and More), Propulsion (ICE, Battery-Electric Vehicles, and More), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific retained the largest regional position with 39.84% share of the automotive safety system market in 2024. China's MIIT rules compelling approval for every ADAS software update foster a robust compliance ecosystem that speeds feature rollout. Technology - auto convergence appears in partnerships such as Huawei and Xpeng, which co-develop domain controllers integrating radar, camera, and LiDAR on a common software stack. Japan nurtures AI-driven start-ups that pilot autonomous shuttles for urban centres, while India's tighter crash regulations boost demand for cost-optimised airbags and AEB in compact cars.

South America posts the highest growth, advancing at an 8.77% CAGR through 2030. Stellantis committed EUR 5.6 billion between 2025 and 2030 to launch more than 40 models from local plants, each aligned with Euro NCAP test protocols. Brazil, Argentina, and neighbouring markets harmonise safety laws, letting global suppliers replicate validated sensor suites without custom tuning. Bio-hybrid powertrains that blend ethanol engines with battery packs open fresh integration tasks for thermal and electrical safety systems.

North America and Europe uphold mature positions with high per-vehicle content and software-defined vehicle regulations. The automotive safety system market share in these regions remains stable, yet value per unit rises as UNECE Regulation 155 enforces full cybersecurity, obliging every safety ECU to meet anti-hacking standards. The Middle East and Africa progress from low baselines, stimulated by infrastructure expansion, yet local climate extremes drive demand for robust sensor housings and dust-proof radar enclosures.

- Robert Bosch GmbH

- Continental AG

- ZF Friedrichshafen AG

- Autoliv Inc.

- Denso Corporation

- Aptiv PLC

- Magna International Inc.

- Joyson Safety Systems

- Mobileye N.V.

- Valeo SA

- Hitachi Astemo

- Hyundai Mobis

- NXP Semiconductors

- Infineon Technologies AG

- Texas Instruments Inc.

- Renesas Electronics Corp.

- Veoneer AB

- WABCO (ZF CV Systems)

- Bendix Commercial Vehicle Systems

- Lear Corporation (E-Systems)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Tightening global NCAP & UNECE safety mandates

- 4.2.2 Rapid sensor-cost deflation enabling ADAS standardisation

- 4.2.3 Boom in software-defined vehicles (OTA safety feature upgrades)

- 4.2.4 Shift toward Level-2+ autonomy in commercial vehicles (fleet TCO play)

- 4.2.5 Rise of AI-based in-cabin biometric safety analytics (fatigue, vitals)

- 4.2.6 Bundling of vehicle-safety data into Usage

- 4.3 Market Restraints

- 4.3.1 High validation & homologation cost for multicountry compliance

- 4.3.2 Chip-set supply volatility delaying OEM safety roll-outs

- 4.3.3 Cyber-physical attack risk on safety ECUs & sensor buses

- 4.3.4 High-voltage electromagnetic interference (EMI) and thermal loads in 800-V battery-electric

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By System Type

- 5.1.1 Active Safety Systems

- 5.1.1.1 Collision-Avoidance (AEB, FCW)

- 5.1.1.2 Driver Monitoring & HMI Alerts

- 5.1.1.3 Chassis Control (ESC, ABS)

- 5.1.2 Passive Safety Systems

- 5.1.2.1 Airbags (Frontal, Side, Curtain, Far-side)

- 5.1.2.2 Seat-belt & Pretensioners

- 5.1.1 Active Safety Systems

- 5.2 By Technology Component

- 5.2.1 Sensors

- 5.2.2 Radar

- 5.2.3 Camera

- 5.2.4 LiDAR/Ultrasonic

- 5.2.5 Control Units and Domain Controllers

- 5.2.6 Software & Algorithms

- 5.3 By End-User

- 5.3.1 OEM Factory-Fit

- 5.3.2 Aftermarket / Retrofit

- 5.4 By Vehicle Type

- 5.4.1 Passenger Cars

- 5.4.2 Light Commercial Vehicles

- 5.4.3 Heavy Commercial Vehicles & Buses

- 5.5 By Propulsion

- 5.5.1 Internal Combustion Engine (ICE)

- 5.5.2 Battery-Electric Vehicles (BEV)

- 5.5.3 Hybrid Electric Vehicle (HEV)

- 5.5.4 Fuel-Cell Electric Vehicle (FCEV)

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Russia

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Turkey

- 5.6.5.4 South Africa

- 5.6.5.5 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Robert Bosch GmbH

- 6.4.2 Continental AG

- 6.4.3 ZF Friedrichshafen AG

- 6.4.4 Autoliv Inc.

- 6.4.5 Denso Corporation

- 6.4.6 Aptiv PLC

- 6.4.7 Magna International Inc.

- 6.4.8 Joyson Safety Systems

- 6.4.9 Mobileye N.V.

- 6.4.10 Valeo SA

- 6.4.11 Hitachi Astemo

- 6.4.12 Hyundai Mobis

- 6.4.13 NXP Semiconductors

- 6.4.14 Infineon Technologies AG

- 6.4.15 Texas Instruments Inc.

- 6.4.16 Renesas Electronics Corp.

- 6.4.17 Veoneer AB

- 6.4.18 WABCO (ZF CV Systems)

- 6.4.19 Bendix Commercial Vehicle Systems

- 6.4.20 Lear Corporation (E-Systems)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

汽車安全系統市場:按組件、技術、車輛類型和應用分類-2026-2032年全球市場預測汽車安全市場:按系統、車輛類型、燃料類型和最終用戶分類-2026-2032年全球市場預測

汽車安全系統市場:按組件、技術、車輛類型和應用分類-2026-2032年全球市場預測汽車安全市場:按系統、車輛類型、燃料類型和最終用戶分類-2026-2032年全球市場預測 2026年全球汽車安全系統市場報告2026年全球防滾籠市場報告汽車安全逃生系統市場:按車輛類型、技術、應用和銷售管道分類-2026-2032年全球市場預測汽車零件反光背心市場:按產品類型、材料類型、價格範圍、分銷管道和最終用戶分類 - 全球預測 2026-2032 年

2026年全球汽車安全系統市場報告2026年全球防滾籠市場報告汽車安全逃生系統市場:按車輛類型、技術、應用和銷售管道分類-2026-2032年全球市場預測汽車零件反光背心市場:按產品類型、材料類型、價格範圍、分銷管道和最終用戶分類 - 全球預測 2026-2032 年 日本汽車安全系統市場規模、佔有率、趨勢及預測(依系統類型、車輛類型、最終用戶及地區分類),2026-2034年

日本汽車安全系統市場規模、佔有率、趨勢及預測(依系統類型、車輛類型、最終用戶及地區分類),2026-2034年 汽車安全下車輔助市場-全球產業規模、佔有率、趨勢、機會和預測:按車輛類型、技術類型、銷售管道、地區和競爭格局分類,2021-2031年汽車安全系統市場 - 全球產業規模、佔有率、趨勢、機會及預測(依製程、主動技術、車輛類型、地區及競爭格局分類,2021-2031年)兒童限制座椅市場按產品類型、安裝類型、年齡層、分銷管道和最終用戶分類-2026-2032年全球預測

汽車安全下車輔助市場-全球產業規模、佔有率、趨勢、機會和預測:按車輛類型、技術類型、銷售管道、地區和競爭格局分類,2021-2031年汽車安全系統市場 - 全球產業規模、佔有率、趨勢、機會及預測(依製程、主動技術、車輛類型、地區及競爭格局分類,2021-2031年)兒童限制座椅市場按產品類型、安裝類型、年齡層、分銷管道和最終用戶分類-2026-2032年全球預測