|

市場調查報告書

商品編碼

1844701

疏水性塗料:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)Hydrophobic Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

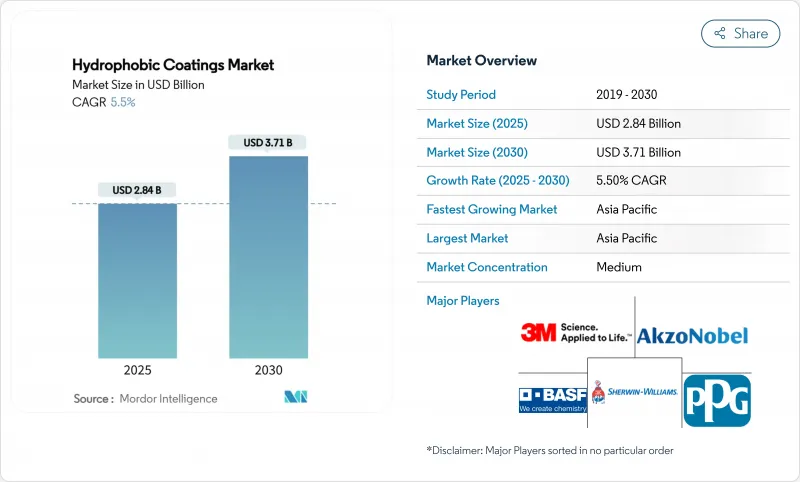

疏水性塗料市場規模預計在 2025 年為 28.4 億美元,預計到 2030 年將達到 37.1 億美元,預測期內(2025-2030 年)的複合年成長率為 5.5%。

監管壓力正在加速向無氟化學的轉變,而持續的基礎設施投資、電子產品的小型化以及日益成長的醫療保健需求都在推動產量成長。如今,技術差異化主要集中在矽基、生物基和奈米結構解決方案上,這些解決方案的性能堪比甚至超越了傳統的氟聚合物。大型買家優先考慮兼具防水性、防腐、抗菌和防凍等特性的多功能產品,這一趨勢有利於擁有豐富配方專業知識的供應商。競爭較為溫和,全球工巨頭正透過資產剝離、策略聯盟和快速專利申請等方式,與敏捷的奈米塗層專家爭奪市場佔有率。

全球疏水性塗料市場趨勢與洞察

建築業強勁成長

持續的都市化和基礎設施更新繼續支撐疏水塗料的需求。矽烷和矽氧烷基混凝土浸漬已成為橋樑、隧道和沿海結構中氯離子防護的標準,可延長其使用壽命並降低維護成本。符合綠色建築認證的生物基疏水處理技術已成為注重永續性的公共計劃的首選解決方案。亞太地區的智慧城市規劃明確規定並擴大使用防水屏障來防止天氣引起的劣化。建築業在2024年的收入佔有率將達到29.64%,這反映了防護塗層在大型土木工程項目中的重要性,因為這些項目的資產壽命直接影響國家基礎設施預算。

汽車產業需求增加

汽車製造商正在轉向疏水多功能塗料,以提供漆面保護、自清潔和防腐功能。自修復奈米複合材料可提高塗層的耐久性,這對於渴望保留剩餘價值的高階汽車品牌來說至關重要。電氣化為機殼和電力電子設備機殼增加了新的保護點,這些外殼必須能夠承受濕氣侵入和熱循環。揮發性有機化合物(VOC)排放法規正在加速水性疏水化學品的發展,迫使供應商在不犧牲產量的情況下複製溶劑型產品的性能。高級駕駛輔助感應器和資訊娛樂顯示器的整合進一步拓展了車內超薄、光學透明防水層的應用前景。

流程複雜,初始投資成本高

製造超疏水層需要精確控制表面粗糙度和化學性質,通常涉及多步驟紋理化、功能化以及在惰性氣體中固化。等離子反應器、雷射圖形化設備和精密品質控制設備的資本投資可能會對中小型公司的財務帶來巨大壓力。下游用戶也面臨學習曲線:必須最佳化基板清潔、環境濕度和固化曲線,才能達到已發表的接觸角規格。這種複雜性可能會限制新參與企業的擴張速度,限制市場競爭,並減緩成本敏感型終端應用領域對技術創新的採用。

細分分析

到2024年,防腐劑將佔據疏水塗料市場佔有率的39.18%,這反映了海洋、石油天然氣和運輸業長期以來對保護鋼鐵和鋁資產的需求。橋樑維修和離岸風力發電安裝計劃的強勁需求將進一步支撐該領域的收益。相較之下,「其他產品類型」叢集中的自清潔防冰產品預計將以6.92%的複合年成長率成長,這得益於太陽能運維公司的支持,這些公司已檢驗在光伏組件上應用奈米塗層後,能源產量可提高高達15%。航太原始設備製造商也在評估低冰黏附表面,以減少除冰液的使用。

防腐子子部門的價格競爭依然激烈,但由於監管部門對高鋅底漆和溶劑型面漆的壓力,採購方正轉向嵌入石墨烯和陶瓷薄片的水性混合塗料。專用自清潔產品透過減少乾旱地區太陽能發電廠的人工清潔工作,獲得了高淨利率。同時,疏水性塗料產業正在興起光熱疏水塗料,這種塗料將被動防水與主動太陽能加熱結合。

區域分析

受中國製造業規模、印度基礎建設規劃以及日本材料科學實力的推動,亞太地區將在2024年維持48.15%的收入佔有率。政府要求公共建築符合綠建築標準,這推動了低VOC疏水產品的採用。該地區的專業電子代工製造商正在指定亞微米防水層,以確保獲得全球智慧型手機品牌的出口訂單。東南亞的太陽能模組工廠持續擴大產能,持續對可延長工廠運作的自清潔光伏塗層的需求。

北美是技術先鋒。美國正在開拓高性能航太和國防應用,其中超疏水防冰層可降低航空公司和軍用飛機的營運成本。加拿大逐步淘汰PFAS將刺激國內對無氟化學品的需求,並鼓勵區域供應商加速有機矽和聚氨酯替代品的認證。墨西哥的汽車出口中心將把疏水處理技術融入電動車電池機殼,加強原料和應用設備的跨境供應鏈。

歐洲正在平衡嚴格的環境政策與產業競爭力。歐洲化學品管理局提案限制超過10,000種PFAS物質,促使配方師加快對生物基替代品的檢驗。一家德國一級汽車供應商共同開發了一種石墨烯增強型水性面漆,既符合耐腐蝕性能,也滿足了噴漆車間的排放目標。北歐國家對循環經濟模式的偏好刺激了包裝領域對可生物分解疏水屏障的需求,並推動了纖維素基解決方案的創新。因此,疏水塗料市場擁有多元化的區域驅動力,這些驅動力正在維持其全球成長動能。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場狀況

- 市場概況

- 市場促進因素

- 建築業強勁成長

- 汽車產業需求增加

- 在家電領域採用率不斷提高

- 3D列印超防水錶面

- 公共基礎設施對抗病毒塗層的需求不斷增加

- 市場限制

- 流程複雜,初始投資成本高

- 磨蝕環境中的耐久性問題

- 禁止使用長鏈氟樹脂迫在眉睫

- 價值鏈分析

- 五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

- 專利分析

- 定價分析

第5章市場規模及成長預測

- 依產品類型

- 防鏽

- 抗菌

- 防污

- 防潮

- 其他產品類型(自清潔、防冰等)

- 按基材

- 金屬

- 陶瓷

- 玻璃

- 具體的

- 塑膠和聚合物

- 其他基材(紡織品、紙張、紙板等)

- 按最終用戶產業

- 建造

- 車

- 航太

- 電子產品

- 衛生保健

- 海洋

- 其他終端用戶產業(石油和天然氣、可再生能源等)

- 按地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 東南亞國協

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭態勢

- 市場集中度

- 策略舉措

- 市佔率(%)/排名分析

- 公司簡介

- 3M

- AccuCoat Inc.

- Aculon Inc.

- Advanced Nanotech Lab

- AkzoNobel NV

- Arkema

- Artekya Teknoloji

- BASF SE

- COTEC GmbH

- Cytonix, LLC

- Nanofilm

- NeverWet, LLC.

- Nukote Coating Systems International

- P2i Ltd.

- PPG Industries, Inc.

- The Sherwin-Williams Company

- UltraTech International, Inc.

第7章 市場機會與未來展望

The Hydrophobic Coatings Market size is estimated at USD 2.84 billion in 2025, and is expected to reach USD 3.71 billion by 2030, at a CAGR of 5.5% during the forecast period (2025-2030).

Regulatory pressure has accelerated the transition toward fluorine-free chemistries, while sustained infrastructure investment, electronics miniaturization, and growing healthcare demand collectively reinforce volume growth. Technology differentiation now centers on silicone-, bio-based, and nanostructured solutions that match or exceed legacy fluoropolymer performance. Large buyers are prioritizing multifunctional products that combine water-repellency with anti-corrosion, antimicrobial, and anti-icing attributes, a trend that favors suppliers with broad formulation expertise. Competitive intensity is moderate as global chemical majors defend share against agile nanocoating specialists through divestment, strategic partnerships, and rapid patent filings.

Global Hydrophobic Coatings Market Trends and Insights

Robust Growth of Construction Sector

Sustained urbanization and infrastructure renewal continue to anchor demand in the hydrophobic coatings market. Silane- and siloxane-based concrete impregnation has become standard for chloride-ion protection of bridges, tunnels, and coastal structures, extending service life and lowering maintenance costs. Alignment with green-building certifications positions bio-based hydrophobic treatments as preferred solutions for public projects that emphasize sustainability. Asia-Pacific smart-city programs are amplifying volumes by specifying water-repellent barriers against climate-induced deterioration. The construction segment's 29.64% 2024 revenue share reflects the indispensability of protective coatings in large civil works, where asset longevity directly influences national infrastructure budgets.

Rising Demand from Automotive Industry

Automotive manufacturers have shifted toward hydrophobic multifunctional coatings that deliver paint protection, self-cleaning, and anti-corrosion benefits. Self-healing nanocomposites improve finish durability, an attribute valued by luxury car brands keen on residual-value preservation. Electrification adds new protection points as battery enclosures and power-electronics housings must resist moisture ingress and thermal cycling. Regulatory caps on VOC emissions accelerate water-borne hydrophobic chemistries, pressing suppliers to replicate solvent-based performance without sacrificing throughput. Integration of advanced driver-assistance sensors and infotainment displays further widens opportunities for ultra-thin, optically clear waterproof layers inside vehicles.

Complex Process and High Initial Investment Cost

Producing superhydrophobic layers demands precise control of surface roughness and chemistry, often involving multi-step texturing, functionalization, and curing in inert atmospheres. Capital expenditure on plasma reactors, laser patterning units, and sophisticated QC instrumentation strains the finances of small and mid-size enterprises. Down-line users also face learning curves: substrate cleaning, ambient humidity, and cure profiles must all be optimized to achieve published contact-angle specifications. These complexities restrict the pace at which new entrants can scale, limiting market competition and potentially slowing innovation diffusion in cost-sensitive end-use sectors.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Adoption in Consumer Electronics

- 3-D Printed Retro-fit Superhydrophobic Surfaces

- Durability Challenges Under Abrasive Environments

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Anti-corrosion formulations maintained a 39.18% hydrophobic coatings market share in 2024, reflecting the perennial need to safeguard steel and aluminum assets in marine, oil-and-gas, and transport sectors. Robust demand from bridge refurbishment and offshore wind installation projects further anchored segment revenues. In contrast, self-cleaning and ice-phobic products within the "Other Product Types" cluster are forecast to post a 6.92% CAGR, buoyed by solar O&M firms that have validated up to 15% energy-yield gains after applying nanocoatings to PV modules. Aerospace OEMs likewise value low-ice-adhesion surfaces that cut anti-icing fluid usage.

The anti-corrosion sub-sector remains price competitive, yet regulatory pressure on zinc-rich primers and solvent-borne top-coats is shifting procurement toward water-borne hybrids with embedded graphene or ceramic flakes. Specialty self-cleaning products command higher margins due to their ability to reduce manual cleaning labor for solar farms located in arid regions. Meanwhile, the hydrophobic coatings industry is witnessing the emergence of photothermal ice-phobic layers that combine passive water repellence with active sunlight-driven heating, a hybrid approach that resonates with airlines pursuing fuel-saving de-icing strategies.

The Hydrophobic Coatings Market Report is Segmented by Product Type (Anti-Corrosion, Anti-Microbial, Anti-Fouling, Anti-Wetting, and More), Substrate (Metals, Ceramics, Glass, Concrete, and More), End-User Industry (Construction, Automotive, Aerospace, Electronics, and More), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific retained 48.15% revenue share in 2024, driven by China's manufacturing scale, India's infrastructure pipeline, and Japan's material-science prowess. Government mandates that public buildings meet green-construction benchmarks have boosted uptake of low-VOC hydrophobic products. Electronics contract manufacturers across the region specify sub-micron waterproof layers to secure export contracts from global smartphone brands. Continued capacity additions in Southeast Asian solar module plants sustain demand for self-cleaning PV coatings that increase plant uptime.

North America stands as a technological bellwether. The United States cultivates high-performance aerospace and defense applications, where superhydrophobic anti-icing layers reduce operational costs for airlines and military fleets. Canada's phased PFAS prohibition elevates domestic demand for fluorine-free chemistries, compelling regional suppliers to accelerate the qualification of silicone and polyurethane alternatives. Mexico's automotive export hubs integrate hydrophobic treatments in electric-vehicle battery enclosures, reinforcing cross-border supply chains for raw materials and application equipment.

Europe balances strict environmental policy with industrial competitiveness. The European Chemicals Agency proposal to restrict over 10,000 PFAS substances has triggered a rush among formulators to validate bio-based replacements. Germany's automotive Tier-1 suppliers co-develop graphene-reinforced water-borne top-coats that satisfy both corrosion-resistance and paint-shop emission targets. Nordic nations' preference for circular-economy models stimulates demand for biodegradable hydrophobic barriers in packaging, pushing innovation toward cellulose-based solutions. The hydrophobic coatings market is thus experiencing geographically diverse pull factors that collectively sustain global growth momentum.

- 3M

- AccuCoat Inc.

- Aculon Inc.

- Advanced Nanotech Lab

- AkzoNobel N.V.

- Arkema

- Artekya Teknoloji

- BASF SE

- COTEC GmbH

- Cytonix, LLC

- Nanofilm

- NeverWet, LLC.

- Nukote Coating Systems International

- P2i Ltd.

- PPG Industries, Inc.

- The Sherwin-Williams Company

- UltraTech International, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Robust growth of construction sector

- 4.2.2 Rising demand from automotive industry

- 4.2.3 Increasing adoption in consumer electronics

- 4.2.4 3-D printed retro-fit superhydrophobic surfaces

- 4.2.5 Increasing demand for anti-viral public-infrastructure coatings

- 4.3 Market Restraints

- 4.3.1 Complex process and high intial investment cost

- 4.3.2 Durability challenges under abrasive environments

- 4.3.3 Impending bans on long-chain fluoropolymers

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

- 4.6 Patent Analysis

- 4.7 Pricing Analysis

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Anti-corrosion

- 5.1.2 Anti-microbial

- 5.1.3 Anti-fouling

- 5.1.4 Anti-wetting

- 5.1.5 Other Product Types (Self-cleaning, Ice-phobic, etc.)

- 5.2 By Substrate

- 5.2.1 Metals

- 5.2.2 Ceramics

- 5.2.3 Glass

- 5.2.4 Concrete

- 5.2.5 Plastics and Polymers

- 5.2.6 Other Substrates (Textiles, Paper and Cardboard, etc.)

- 5.3 By End-user Industry

- 5.3.1 Construction

- 5.3.2 Automotive

- 5.3.3 Aerospace

- 5.3.4 Electronics

- 5.3.5 Healthcare

- 5.3.6 Marine

- 5.3.7 Other End-user Industries (Oil and Gas, Renewable Energy, etc.)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 3M

- 6.4.2 AccuCoat Inc.

- 6.4.3 Aculon Inc.

- 6.4.4 Advanced Nanotech Lab

- 6.4.5 AkzoNobel N.V.

- 6.4.6 Arkema

- 6.4.7 Artekya Teknoloji

- 6.4.8 BASF SE

- 6.4.9 COTEC GmbH

- 6.4.10 Cytonix, LLC

- 6.4.11 Nanofilm

- 6.4.12 NeverWet, LLC.

- 6.4.13 Nukote Coating Systems International

- 6.4.14 P2i Ltd.

- 6.4.15 PPG Industries, Inc.

- 6.4.16 The Sherwin-Williams Company

- 6.4.17 UltraTech International, Inc.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

防水塗料市場:依技術、塗料類型、最終用途、應用和銷售管道分類-2026-2032年全球市場預測瀝青防水塗料市場:2026-2032年全球市場預測(按產品類型、配方類型、應用、最終用戶和分銷管道分類)乳液型防水塗料市場:類型、包裝、通路、應用、最終用途-2026-2032年全球市場預測

防水塗料市場:依技術、塗料類型、最終用途、應用和銷售管道分類-2026-2032年全球市場預測瀝青防水塗料市場:2026-2032年全球市場預測(按產品類型、配方類型、應用、最終用戶和分銷管道分類)乳液型防水塗料市場:類型、包裝、通路、應用、最終用途-2026-2032年全球市場預測 2026年全球建築防水維修市場報告

2026年全球建築防水維修市場報告 全球防水塗料市場規模、佔有率、趨勢和成長分析報告(2026-2034年)2026年全球疏水性塗料市場報告抗垂流劑市場按應用、終端用戶產業、產品類型和分銷管道分類,全球預測(2026-2032年)

全球防水塗料市場規模、佔有率、趨勢和成長分析報告(2026-2034年)2026年全球疏水性塗料市場報告抗垂流劑市場按應用、終端用戶產業、產品類型和分銷管道分類,全球預測(2026-2032年) 全球疏水性塗料市場預測(至2032年):依材料類型、製造方法、功能、基材種類、最終使用者及地區分類

全球疏水性塗料市場預測(至2032年):依材料類型、製造方法、功能、基材種類、最終使用者及地區分類 疏水塗料市場規模、佔有率和成長分析(按性能、基材類型、材料、製造方法、最終用途產業和地區分類)- 產業預測(2026-2033 年)

疏水塗料市場規模、佔有率和成長分析(按性能、基材類型、材料、製造方法、最終用途產業和地區分類)- 產業預測(2026-2033 年) 全球疏水劑市場

全球疏水劑市場