|

市場調查報告書

商品編碼

1844698

擴增實境和混合實境:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030)Augmented Reality And Mixed Reality - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

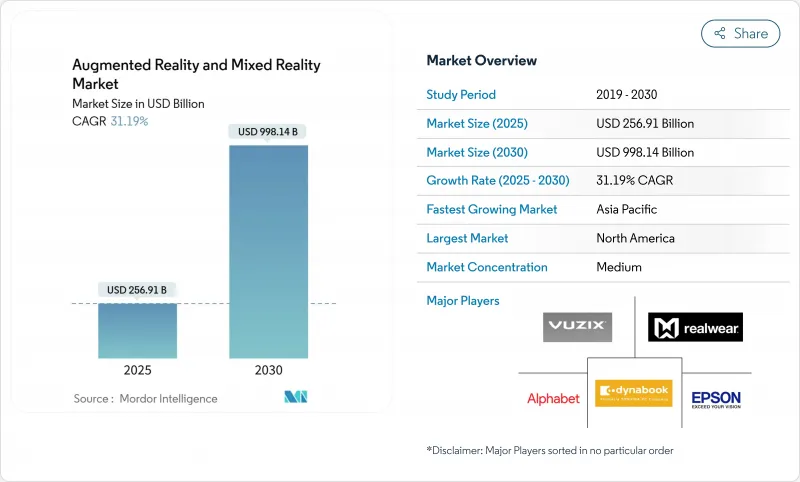

擴增實境和混合實境市場預計在 2025 年價值 2,569.1 億美元,預計到 2030 年將達到 9,981.4 億美元,預測期內(2025-2030 年)的複合年成長率為 31.19%。

5G 網路的商用部署、持續的企業數位轉型預算以及微 OLED 和波導管顯示器成本的快速下降,正在將空間運算試點轉化為大規模部署。例如,瑪氏寵物護理公司將 RealWear HMT-1 穿戴式裝置與 Microsoft Teams 結合,將教練差旅成本降低了 35%。 Meta 彌補了 Reality Labs 多年的虧損,蘋果將 Vision Pro 定位於高階空間運算領域,三星與Google和高通的合作則在 2025 年 Android XR 推出之前增強了其競爭地位。擴增實境和混合實境市場目前正處於硬體創新、人工智慧驅動的 3D 內容管道以及推動經常性收益模式的託管服務成長的十字路口。

全球擴增實境和混合實境市場趨勢和洞察

5G 和邊緣運算低延遲體驗

通訊業者目前正在支援雲端渲染視覺效果,提供低於 20 毫秒的延遲、更輕的頭戴裝置和更長的電池續航力。邊緣卸載技術使輕量眼鏡能夠處理功能豐富的內容,而不會出現熱過載。高通的分散式運算專利使設備能夠在本地和遠端處理之間無縫切換,並根據網路狀況調整功耗需求。多人混合實境遊戲現在要求每位玩家高達 50 Mbps 的通訊,這推動了向 AR 特定服務層級的轉變。時間敏感的工業任務(例如遠端設備重置)受益於近乎即時的全像導航,從而為企業與網路供應商簽訂新的合約創造了條件。

遊戲和零售領域以行動優先的 AR 應用

智慧型手機上的擴增實境 (AR) 降低了進入門檻,Pokemon GO 的累積收益超過 80 億美元就是明證。絲芙蘭的臉部辨識虛擬藝術家提高了購物車轉換率,同時降低了退貨率。宜家的“Place”應用程式允許購物者評估家具在實際房間中的合適度,從而減少了因尺寸相關的退貨。谷歌將 AR 美妝試穿功能擴展到行動瀏覽器,使超過 50 個品牌的互動率提升了 10%。行動管道可以提升用戶熟悉度,隨後過渡到頭戴式耳機的普及,並強化了擴增實境和混合實境市場從手機到穿戴式裝置的轉換管道。

商用HMD 的初始成本高

高昂的價格限制了其大規模應用。 Apple Vision Pro 售價超過 3,000 美元,迫使企業只能試用。SONY降低了 PlayStation VR2 的價格,但由於庫存過剩凸顯了成本敏感性,該公司暫停了生產。 HTC 瞄準的是利基企業用戶群,並透過投資回報率分析證明了其 999 美元 Vive Focus Vision 的合理性。 Meta 的 Reality Labs 的累積虧損表明,該公司難以將技術雄心與價格實惠的消費級產品相結合。供應商專注於光學和系統級晶片 (SoC) 的規模經濟,以突破關鍵的定價門檻,從而開拓更廣闊的潛在市場。

細分分析

高階頭戴裝置和光學元件仍然是資本密集產品,到2024年,硬體將佔總收入的61%。就以金額為準,擴增實境和混合實境硬體市場規模接近1,560億美元,這反映了企業在Vision Pro、Quest Pro和HoloLens上的持續支出。同時,服務業的複合年成長率最高,達到32.5%,這反映了向訂閱式支援、內容創作和設備管理服務的轉變。

託管服務的成長反映了雲端軟體的發展軌跡。 ArborXR 提供多品牌 VR 裝置管理訂閱服務,降低了大規模部署的 IT 複雜性。系統整合正在將內容庫、分析和隨叫隨到的故障排除服務捆綁到可預測的營運成本中,將成本討論從硬體支出轉向整體解決方案的回報。隨著微型 OLED 成本的下降,硬體收益可能會相應稀釋,但服務收入將實現複合成長,擴增實境(AR) 和混合實境(MR) 市場很可能將保持經常性收益基礎。

到2024年,獨立式頭戴裝置將佔擴增擴增實境實境和混合實境境設備市場規模的一半。然而,隨著波導管的小型化,智慧眼鏡的重量將與日常眼鏡產品的重量相近,其複合年成長率將達到33%。像Meta Orion這樣的行業原型產品正達到臨界點,實現了70度的視場角,同時重量控制在85克以下,適合全天佩戴。

三星-谷歌的 Project Moohan 將透明顯示器與 Gemini AI 融合,強調外形規格訊息而非完全沉浸式體驗。消費者傾向於在社交場合佩戴更輕巧的眼鏡,而企業則青睞將安全頭盔與眼動追蹤工作流程相結合的眼鏡。隨著供應鏈趨於穩定,眼鏡將成為主流,再形成擴增實境和混合實境市場的開發者優先事項和行銷敘事。

擴增實境和混合實境市場報告按組件(硬體、軟體、服務)、設備類型(獨立頭戴式顯示器 [HMD]、系留/主機連結 HMD 等)、最終用戶行業(遊戲和娛樂、醫療保健、教育和培訓、零售和電子商務等)、應用(遠端協作和協助、設計和視覺化等)和地區進行細分。

區域分析

北美繼續提供大部分平台軟體和創業投資。儘管宏觀經濟不確定性,但物流、現場服務和醫療保健領域的早期部署已獲得投資回報,並已獲得複購訂單。出口管制和智慧財產權保護的法規日趨明確,鼓勵海外公司在矽谷和西雅圖建立研發中心。然而,隨著首波採用者的成熟以及採購轉向更換,銷售成長正在放緩。

亞太地區的擴張速度超過全球平均。有利於創新的產業政策和集中式顯示器製造正在縮短新型光學元件的上市時間。韓國和日本的電信業者正在將基於5G的XR合約收益,並提升消費者認知度。新興企業正在享受政府補貼,最高可達50%的測試成本,加速了公司的概念驗證。中產階級消費者可支配收入的增加進一步推動了AR購物和遊戲的普及。

在歐洲,機會與謹慎之間需要平衡。工業企業正在利用擴增實境技術在現有的自動化架構中進行預測性維護,醫療保健系統正在試點將視覺化技術應用於遠端手術。然而,GDPR主導的知情同意工作流程會增加開發成本。那些在設計上注重隱私的公司能夠贏得信任,並在鐵路、能源和國防領域贏得競標。 「數位歐洲」計畫的津貼旨在促進跨國標準協調,從而在未來十年減少碎片化。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場狀況

- 市場概況

- 市場促進因素

- 5G 和邊緣運算實現低延遲體驗

- 遊戲和零售領域以行動優先的 AR 應用

- 企業對身臨其境型培訓和遠端支援的需求

- 使用 Vision Pro 投資空間計算

- Micro OLED/OLEDoS成本突破

- 基於生成式人工智慧的 3D 內容自動化

- 市場限制

- 商用HMD的初始成本很高

- 隱私和資料安全問題

- 平台間空間標準差距

- 波導管與微型OLED供應瓶頸

- 價值/供應鏈分析

- 監管狀況

- 技術展望

- 波特五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭強度

- 新冠疫情的影響與疫情後的重啟

- 投資分析

第5章市場規模與成長預測

- 按組件

- 硬體

- 軟體

- 服務

- 依設備類型

- 獨立頭戴式顯示器(HMD)

- 系留/主機連結 HMD

- 智慧眼鏡和HUD

- 手持/移動 AR

- 按最終用戶產業

- 遊戲和娛樂

- 衛生保健

- 教育和培訓

- 零售與電子商務

- 工業和製造業

- 汽車和運輸

- 軍事/國防

- 其他

- 按用途

- 遠距協作與援助

- 設計與視覺化

- 維護和維修

- 模擬與訓練

- 航海與旅遊

- 行銷和廣告

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 澳洲

- 其他亞太地區

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 土耳其

- 其他中東和非洲地區

- 北美洲

第6章 競爭態勢

- 市場集中度

- 策略舉措

- 市佔率分析

- 公司簡介

- Meta Platforms Inc.

- Microsoft Corporation

- Apple Inc.

- Google LLC

- Samsung Electronics Co. Ltd.

- Sony Group Corporation

- Magic Leap Inc.

- Vuzix Corporation

- Niantic Inc.

- PTC Inc.

- Ultraleap Ltd.

- HTC Corporation

- RealWear Inc.

- Lenovo Group Ltd.

- Seiko Epson Corporation

- Atheer Inc.

- Varjo Technologies Oy

- Pico Interactive(BYTdance)

- HP Development Company LP

- AsusTek Computer Inc.

- Acer Inc.

- Dell Technologies Inc.

- Qualcomm Technologies Inc.

- Trimble Inc.

- Snap Inc.

第7章 市場機會與未來展望

The Augmented Reality And Mixed Reality Market size is estimated at USD 256.91 billion in 2025, and is expected to reach USD 998.14 billion by 2030, at a CAGR of 31.19% during the forecast period (2025-2030).

Commercial deployment of 5G networks, sustained enterprise digital-transformation budgets, and rapid cost erosion in micro-OLED and waveguide displays are converting spatial-computing pilots into scaled roll-outs. Enterprises report measurable efficiency gains; for example, Mars Petcare cut coaching travel costs by 35% after pairing RealWear HMT-1 wearables with Microsoft Teams. Competitive momentum intensifies as Meta absorbs multi-year Reality Labs losses, Apple positions Vision Pro for premium spatial-computing, and a Samsung-Google-Qualcomm alliance races to a 2025 Android XR launch. The augmented reality and mixed reality market now sits at the intersection of hardware innovation, AI-assisted 3D content pipelines, and managed-services growth that encourages recurring-revenue models.

Global Augmented Reality And Mixed Reality Market Trends and Insights

5G and Edge-enabled Low-latency Experiences

Telcos now deliver sub-20 ms latency, enabling cloud-rendered visuals that lighten headsets and prolong battery life. Edge offloading lets lightweight glasses handle feature-rich content without thermal overload. Qualcomm's distributed compute patents allow devices to switch seamlessly between local and remote processing, matching power needs to network conditions. Multiplayer mixed-reality games now require up to 50 Mbps per player, pushing operators toward AR-specific service tiers. Time-sensitive industrial tasks such as remote equipment resets benefit from near-instant holographic guidance, unlocking new enterprise contracts for network providers.

Mobile-first AR Adoption in Gaming and Retail

Smartphone AR lowers entry barriers, evidenced by Pokemon GO surpassing USD 8 billion lifetime revenue. Retailers leverage virtual try-ons; Sephora's facial-recognition-enabled Virtual Artist drives higher cart conversion while lowering return rates. IKEA's Place app lets buyers assess furniture fit in actual rooms, reducing size-related returns. Google broadened AR beauty try-ons to mobile browsers, lifting interaction rates for 50+ brands by 10%. The mobile channel nurtures user familiarity that later transitions to headset adoption, reinforcing the augmented reality and mixed reality market's funnel from phones to wearables.

High Upfront Cost of Professional HMDs

Premium pricing restricts volume deployment. Apple Vision Pro's tag surpasses USD 3,000, forcing firms to stage adoption in pilot waves. Sony trimmed PlayStation VR2 prices yet paused production after excess inventory underscored sensitivity to cost. HTC targets niche enterprise users willing to justify USD 999 Vive Focus Vision through ROI analytics. Meta's cumulative Reality Labs losses signal the struggle to pair technological ambition with affordable consumer SKUs. Vendors focus on scale economies in optics and SoCs to cross critical pricing thresholds that unlock wider addressable markets.

Other drivers and restraints analyzed in the detailed report include:

- Enterprise Demand for Immersive Training and Remote Support

- Vision Pro-driven Spatial-computing Investment

- Privacy and Data-Security Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware retained 61% of revenue in 2024 as premium headsets and optics remain capital-heavy. In monetary terms, the augmented reality and mixed reality market size for hardware approached USD 156 billion, reflecting continued enterprise spending on Vision Pro, Quest Pro, and HoloLens. Meanwhile, services posted the highest 32.5% CAGR, underlining migration to subscription-oriented support, content-authoring, and device-management offerings.

Growth in managed services mirrors cloud-software trajectories. ArborXR offers fleet-management subscriptions across multi-brand VR, reducing IT complexity for large roll-outs. System integrators bundle content libraries, analytics, and on-call troubleshooting into predictable OPEX, shifting cost discussions from hardware outlay to total-solution payback. As micro-OLED costs fall, hardware revenue may dilute proportionally, yet services will compound, keeping the augmented reality and mixed reality market on a recurring-revenue footing.

Stand-alone HMDs commanded 48% of spend in 2024, equivalent to nearly half of the augmented reality and mixed reality market size for devices. However, smart glasses are forecast at a 33% CAGR as waveguide miniaturization moves products toward everyday eyewear weight. Industry prototypes such as Meta Orion deliver 70-degree FOV while meeting under-85-gram targets, a tipping point for day-long wearability.

Samsung-Google's Project Moohan blends transparent displays with Gemini AI, focusing on heads-up information rather than full-occlusion immersion. Consumers gravitate to lighter form factors in social settings, while enterprises favor glasses for safety-helmet integration and line-of-sight workflows. As supply chains stabilize, the mix will pivot toward glasses, reshaping developer priorities and marketing narratives across the augmented reality and mixed reality market.

The Augmented Reality and Mixed Reality Market Report is Segmented by Component (Hardware, Software, and Services), Device Type (Stand-Alone Head-Mounted Display [HMD], Tethered/Console-linked HMD, and More), End-User Industry (Gaming and Entertainment, Healthcare, Education and Training, Retail and E-Commerce, and More), Application (Remote Collaboration and Assistance, Design and Visualization, and More), and Geography.

Geography Analysis

North America continues to supply the bulk of platform software and venture capital. Early enterprise roll-outs confirmed ROI in logistics, field service, and healthcare, anchoring repeat orders despite macro uncertainty. Regulatory clarity on export controls and IP safeguards attracts overseas firms to form R&D centers in Silicon Valley and Seattle. Yet unit growth has slowed as first-wave adopters mature and procurement moves into replacement cycles.

Asia Pacific's expansion outpaces the global average. Pro-innovation industrial policies and concentrated display manufacturing compress time-to-market for new optics. Telcos in South Korea and Japan monetize 5G-based XR subscriptions, fueling consumer awareness. Start-ups enjoy government grants that cover up to 50% of pilot costs, accelerating enterprise proof-of-concepts. Rising disposable income among middle-class consumers further elevates AR shopping and gaming uptake.

Europe balances opportunity with caution. Industrial companies leverage AR for predictive maintenance within established automation architectures, while healthcare systems pilot remote-surgery visualization. However, GDPR-driven consent workflows add development overhead. Firms that demonstrate privacy-by-design earn trust and win tenders across rail, energy, and defense. Subsidies from the Digital Europe Programme target cross-border standards alignment, aiming to lower fragmentation over the coming decade.

- Meta Platforms Inc.

- Microsoft Corporation

- Apple Inc.

- Google LLC

- Samsung Electronics Co. Ltd.

- Sony Group Corporation

- Magic Leap Inc.

- Vuzix Corporation

- Niantic Inc.

- PTC Inc.

- Ultraleap Ltd.

- HTC Corporation

- RealWear Inc.

- Lenovo Group Ltd.

- Seiko Epson Corporation

- Atheer Inc.

- Varjo Technologies Oy

- Pico Interactive (BYTdance)

- HP Development Company LP

- AsusTek Computer Inc.

- Acer Inc.

- Dell Technologies Inc.

- Qualcomm Technologies Inc.

- Trimble Inc.

- Snap Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 5G and Edge-enabled low-latency experiences

- 4.2.2 Mobile-first AR adoption in gaming and retail

- 4.2.3 Enterprise demand for immersive training and remote support

- 4.2.4 Vision Pro-driven spatial-computing investments

- 4.2.5 Micro-OLED/OLEDoS cost breakthroughs

- 4.2.6 Generative-AI-based 3D content automation

- 4.3 Market Restraints

- 4.3.1 High upfront cost of professional HMDs

- 4.3.2 Privacy and data-security concerns

- 4.3.3 Inter-platform spatial-standards gap

- 4.3.4 Waveguide and micro-OLED supply bottlenecks

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of COVID-19 and Post-Pandemic Reset

- 4.9 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.2 Software

- 5.1.3 Services

- 5.2 By Device Type

- 5.2.1 Stand-alone Head-Mounted Display (HMD)

- 5.2.2 Tethered/Console-linked HMD

- 5.2.3 Smart Glasses and HUD

- 5.2.4 Handheld/Mobile AR

- 5.3 By End-user Industry

- 5.3.1 Gaming and Entertainment

- 5.3.2 Healthcare

- 5.3.3 Education and Training

- 5.3.4 Retail and E-commerce

- 5.3.5 Industrial and Manufacturing

- 5.3.6 Automotive and Transportation

- 5.3.7 Military and Defense

- 5.3.8 Others

- 5.4 By Application

- 5.4.1 Remote Collaboration and Assistance

- 5.4.2 Design and Visualization

- 5.4.3 Maintenance and Repair

- 5.4.4 Simulation and Training

- 5.4.5 Navigation and Tourism

- 5.4.6 Marketing and Advertising

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Russia

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 India

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 South Africa

- 5.5.5.4 Turkey

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Meta Platforms Inc.

- 6.4.2 Microsoft Corporation

- 6.4.3 Apple Inc.

- 6.4.4 Google LLC

- 6.4.5 Samsung Electronics Co. Ltd.

- 6.4.6 Sony Group Corporation

- 6.4.7 Magic Leap Inc.

- 6.4.8 Vuzix Corporation

- 6.4.9 Niantic Inc.

- 6.4.10 PTC Inc.

- 6.4.11 Ultraleap Ltd.

- 6.4.12 HTC Corporation

- 6.4.13 RealWear Inc.

- 6.4.14 Lenovo Group Ltd.

- 6.4.15 Seiko Epson Corporation

- 6.4.16 Atheer Inc.

- 6.4.17 Varjo Technologies Oy

- 6.4.18 Pico Interactive (BYTdance)

- 6.4.19 HP Development Company LP

- 6.4.20 AsusTek Computer Inc.

- 6.4.21 Acer Inc.

- 6.4.22 Dell Technologies Inc.

- 6.4.23 Qualcomm Technologies Inc.

- 6.4.24 Trimble Inc.

- 6.4.25 Snap Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment