|

市場調查報告書

商品編碼

1844652

自密實混凝土(SCC):市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030)Self-Consolidating Concrete (SCC) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

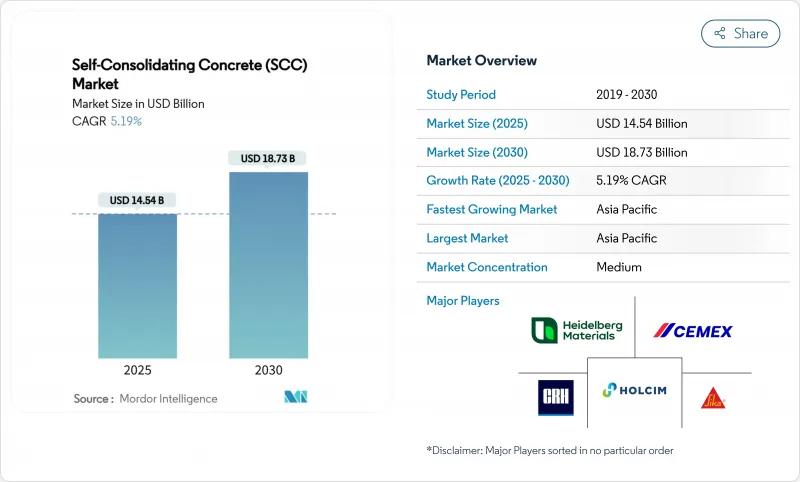

自密實混凝土 (SCC) 市場規模預計在 2025 年為 145.4 億美元,預計到 2030 年將達到 187.3 億美元,預測期內(2025-2030 年)的複合年成長率為 5.19%。

強勁的需求源自於承包商需要在澆築複雜的鋼筋籠時避免產生機械振動,這項要求與日益嚴格的勞動法規和自動化目標相符。尤其是在北美和歐洲,限制混凝土碳排放的監管壓力正在加速向添加更多膠凝材料的混合物的轉變。現有的外加劑製造商正在利用聚羧酸鹽的化學特性來提高較低水膠比下的流動性,而數位監控平台則提供即時強度數據,有助於降低水泥用量。這些因素共同作用,形成了性能提升、勞動強度降低和永續性要求的良性循環,有利於自密實混凝土 (SCC) 市場的發展。

全球自密實混凝土(SCC)市場趨勢與洞察

預製和現澆施工節省勞力

長期的勞動力短缺促使建築公司採用無振動澆注方法,這種方法可將週期縮短高達73%,並減少工人數量。預製工廠透過整合纖維增強自密實混合料,生產率提高了28%,目前在北美和日本均有體現。更快的周轉速度使其成本與傳統混凝土持平,儘管材料成本高出15-25%。在鋼筋密集、無法進行振動或物理上無法進行振動的應用中,其優勢更為顯著,這使得自密實混凝土 (SCC) 市場成為高層建築和橋樑建設的核心。

對低碳供應鏈管理豐富組合的需求

紐約州的「購買清潔能源」法規對公共計劃混凝土的碳排放總量設定了上限,這促使生產商增加礦渣和飛灰的用量,這些材料能夠與高流動性混合料自然結合。加州的「加州綠建築」法規和法國的「再生能源2020」框架也對二氧化碳排放量比「I類」混合料減少30-50%的混合料徵收溢價。現代聚羧酸塑化劑在降低熟料係數的同時保持了所需的流動性,正在加強自凝混凝土市場,使其成為永續性的槓桿,而不僅僅是勞動力的解決方案。

高混合設計和材料成本溢價

在薪資低廉且計劃業主抵制溢價的情況下,與傳統混凝土相比15-25%的成本差異仍然是一個不利因素。東南亞和拉丁美洲部分地區對混合骨材和進口外加劑的需求推高了成本,儘管表面上節省了勞動力,但這可能會抑制自凝混凝土市場的成長。承包商需要平衡前期成本和下游效率,這限制了自凝混凝土在小型專案中的應用。

細分分析

2024年,水泥將佔自密實混凝土 (SCC) 市場的37.18%,其驅動力來自產量而非成長動能。外加劑的複合年成長率將達到7.18%,這得益於第四代聚羧酸醚的快速普及。這種材料能夠在不犧牲流動性的情況下,將水膠比提升至接近0.30。這些化學品與黏度調節劑相結合,可實現更高的SCM替代水平,幫助生產者遵守日益嚴格的二氧化碳排放法規。骨材的價值排名第二,這得益於對低結垢間隙級配石材的需求不斷成長,以減少在最小上舉力下發生堵塞的情況。由於生產商更重視性能而非水泥噸位,外加劑正朝著化學最佳化的方向發展,這也凸顯了全球主要企業為何優先考慮在外加劑領域建立研發合作夥伴關係並進行收購。

向供應鏈管理 (SCM) 整合的轉變正在重塑供應商層級結構。在西方市場,燃煤發電量的下降導致飛灰供應不確定,從而引發了人們對煅燒粘土和磨碎玻璃火山灰的興趣。纖維在預製應用的添加量不斷增加,其裂縫控制功能與無振動澆注相輔相成。 SikaGrind-400 展示了針對性助磨劑如何提高早期強度,並在熟料模量降低的情況下拓展可尋址自硬混凝土市場。水泥製造商正努力將自己的外加劑產品線與低碳黏合劑捆綁銷售,以保持市場佔有率,這表明未來的競爭優勢將更多地取決於全面的化學解決方案,而非原料噸位。

區域分析

預計到2024年,亞太地區將佔全球總收入的49.55%,複合年成長率為7.45%。在中國的高鐵高架橋和印度的智慧城市計畫中,採用密實鋼筋籠的防振混凝土正逐漸成為常規做法。日本的加班規定限制了現場工時,這增強了預製場和現澆應用中自動化澆築的商業可行性。兩黨在基礎設施方面的支出為橋面和高速公路的修復帶來了機遇,這與紐約州的隱含碳排放上限規定相一致。

歐洲是一個成熟又富有創新的產業。法國再生能源2020計畫和愛爾蘭的水泥熟料減量指令下的二氧化碳排放法規將加速SCM的採用,並刺激外加劑的需求。中東/非洲和南美洲的規模較小,但隨著技術服務網路的擴展和大型計劃的增加,人們對其的興趣日益濃厚。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場狀況

- 市場概況

- 市場促進因素

- 預製和現場施工中節省勞力的放置

- 對低碳、富含供應鏈管理的能源組合的需求不斷增加

- 自動化/機器人混凝土澆築線快速增加

- 在複雜、高層和大型基礎設施的應用

- 政府綠建築指令

- 市場限制

- 高混合設計和材料成本溢價

- 新興地區的現場專業知識有限

- 混合物敏感性導致質量變化

- 價值鏈分析

- 五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章市場規模及成長預測

- 按成分

- 水泥

- 總計的

- 外加劑和添加劑

- 其他成分

- 按用途

- 預製混凝土產品

- 建築材料

- 住宅結構

- 基礎建設(橋樑、隧道等)

- 其他用途

- 按地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 東南亞國協

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭態勢

- 市場集中度

- 策略舉措

- 市佔率(%)/排名分析

- 公司簡介

- BASF

- Breedon Group plc

- Cemex SAB de CV

- CRH

- GCP Applied Technologies

- Heidelberg Materials

- Holcim

- Saint-Gobain

- Sika AG

- Tarmac Ltd.

- UltraTech Cement Ltd.

- Unibeton Ready Mix

- Vicat Group

第7章 市場機會與未來展望

The Self-Consolidating Concrete Market size is estimated at USD 14.54 billion in 2025, and is expected to reach USD 18.73 billion by 2030, at a CAGR of 5.19% during the forecast period (2025-2030).

Robust demand arises from contractors' need to pour intricate reinforcement cages without mechanical vibration, a requirement that lines up with tightening labor regulations and automation goals. Regulatory pressure to curb embodied carbon, especially in North America and Europe, accelerates the shift toward supplementary-cementitious-material-rich mixes. Established admixture producers leverage polycarboxylate chemistry to enhance flow at lower water-binder ratios, while digital monitoring platforms provide real-time strength data that helps reduce cement content. Collectively, these factors reinforce a virtuous cycle in which better performance, lower labor intensity and sustainability mandates all favor the self-consolidating concrete market.

Global Self-Consolidating Concrete (SCC) Market Trends and Insights

Labor-saving placement in precast and in-situ works

Chronic craft-worker shortages prompt builders to adopt vibration-free placement methods that cut cycle times by up to 73% and permit leaner crew sizes. Precast plants record 28% productivity gains when integrating fiber-reinforced self-consolidating mixes, a figure now observable across North America and Japan. Faster turnarounds yield cost parity against conventional concrete despite a 15-25% materials premium. The benefit multiplies on congested rebars where vibration is either impractical or physically impossible, placing the self-consolidating concrete market at the center of high-rise and bridge work.

Demand for low-carbon SCM-rich mixes

State-level "Buy Clean" rules in New York enforce embodied-carbon ceilings for concrete supplied to public projects, pushing producers toward high slag and fly-ash dosages that pair naturally with flowable mixes. Similar thresholds under California's CALGreen code and France's RE2020 framework create a price premium for formulations that deliver 30-50% CO2 cuts relative to Type I blends. Modern polycarboxylate superplasticizers sustain required flow at reduced clinker factors, reinforcing the self-consolidating concrete market as a sustainability lever rather than just a labor solution.

High mix-design & material cost premium

A 15-25% cost delta over conventional concrete remains a headwind wherever wages are low and project owners resist premium pricing. The need for well-graded aggregates and imported admixtures can inflate costs in Southeast Asia and parts of Latin America, dampening self-consolidating concrete market growth despite clear labor savings. Contractors must balance up-front expense against downstream efficiencies, limiting uptake in small-scale jobs.

Other drivers and restraints analyzed in the detailed report include:

- Surge in automated robotic casting lines

- Adoption in complex high-rise and mega-infrastructure

- Limited field know-how in emerging regions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cement accounted for 37.18% of the self-consolidating concrete market in 2024, a lead attributable to structural volume rather than growth momentum. Admixtures now post a 7.18% CAGR, underpinned by the rapid uptake of fourth-generation polycarboxylate ethers that enable water-binder ratios near 0.30 without sacrificing flow. Paired with viscosity modifiers, these chemistries unlock higher SCM replacement levels that help producers comply with tightening CO2 caps. Aggregates rank second by value; demand intensifies for gap-graded stone with low flakiness to mitigate blocking under minimal head pressure. The constituent mix tilts toward chemical optimization as producers emphasize performance over cement tonnage, underscoring why global majors prioritize R&D alliances and acquisitions in the admixture space.

The pivot toward SCM integration reshapes supplier hierarchies. Fly-ash availability remains volatile in Western markets due to declining coal power, spurring interest in calcined clay and ground-glass pozzolans. Fiber additions grow in precast applications, offering crack control that complements vibration-free casting. SikaGrind-400 illustrates how targeted grinding aids elevate early strength when clinker factors drop, widening the addressable self-consolidating concrete market. Cement producers counter by bundling low-carbon binders with in-house admixture lines to retain share, signaling that future competitive advantage depends less on raw tonnage and more on integrated chemical solutions.

The Self-Consolidating Concrete Market Report is Segmented by Constituent (Cement, Aggregates, Admixtures & Additives, Other Constituents), Application (Precast Concrete Products, Architectural Elements, Residential Structures, Infrastructure, Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific controlled 49.55% of global revenue in 2024 and is projected to expand at a 7.45% CAGR, reflecting massive infrastructure outlays coupled with acute labor shortages. China's high-speed-rail viaducts and India's smart-cities program routinely specify vibration-free concrete for dense reinforcement cages. Japan's overtime legislation caps site hours, strengthening the business case for automated placement in both precast yards and cast-in-place work. North America ranks second by value; bipartisan infrastructure spending unlocks bridge-deck and highway rehabilitation opportunities that align with New York's embodied-carbon caps.

Europe remains a mature yet innovative arena. Embodied-carbon ceilings under RE2020 in France and Ireland's clinker-reduction mandate accelerate SCM adoption, thereby boosting admixture demand. Middle East & Africa and South America start from smaller bases but display rising interest as technical service networks expand and megaprojects proliferate.

- BASF

- Breedon Group plc

- Cemex SAB de CV

- CRH

- GCP Applied Technologies

- Heidelberg Materials

- Holcim

- Saint-Gobain

- Sika AG

- Tarmac Ltd.

- UltraTech Cement Ltd.

- Unibeton Ready Mix

- Vicat Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Labor-saving placement in precast and in-situ works

- 4.2.2 Accelerating demand for low-carbon, SCM-rich mixes

- 4.2.3 Surge in automated/robotic casting lines

- 4.2.4 Adoption in complex, high-rise & mega-infrastructure

- 4.2.5 Government green-building mandates

- 4.3 Market Restraints

- 4.3.1 High mix-design & material cost premium

- 4.3.2 Limited field know-how in emerging regions

- 4.3.3 Admixture-sensitivity causing quality variability

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size & Growth Forecasts (Value)

- 5.1 By Constituent

- 5.1.1 Cement

- 5.1.2 Aggregates

- 5.1.3 Admixtures and Additives

- 5.1.4 Other Constituents

- 5.2 By Application

- 5.2.1 Precast Concrete Products

- 5.2.2 Architectural Elements

- 5.2.3 Residential Structures

- 5.2.4 Infrastructure (Bridges, Tunnels, etc.)

- 5.2.5 Other Applications

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 Japan

- 5.3.1.3 India

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 NORDIC Countries

- 5.3.3.8 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 BASF

- 6.4.2 Breedon Group plc

- 6.4.3 Cemex SAB de CV

- 6.4.4 CRH

- 6.4.5 GCP Applied Technologies

- 6.4.6 Heidelberg Materials

- 6.4.7 Holcim

- 6.4.8 Saint-Gobain

- 6.4.9 Sika AG

- 6.4.10 Tarmac Ltd.

- 6.4.11 UltraTech Cement Ltd.

- 6.4.12 Unibeton Ready Mix

- 6.4.13 Vicat Group

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment