|

市場調查報告書

商品編碼

1844626

無晶片 RFID:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)Chipless RFID - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

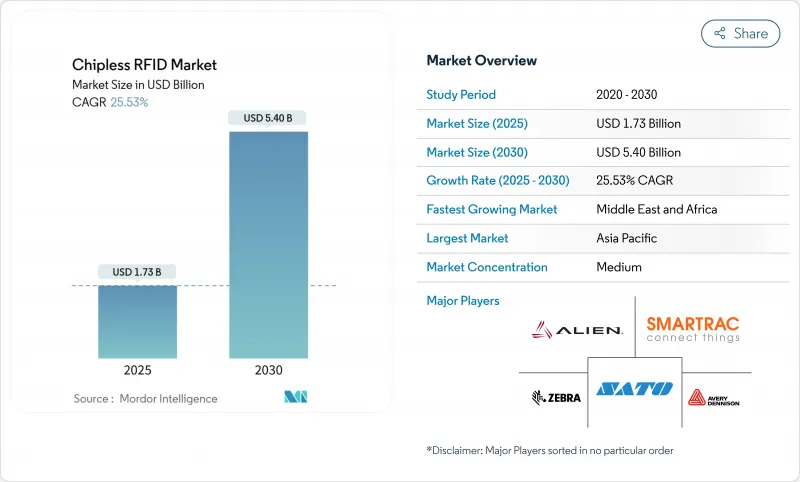

無晶片 RFID 市場預計在 2025 年達到 17.3 億美元,在 2030 年達到 54 億美元,複合年成長率為 25.53%。

亞洲快速消費品包裝的蓬勃發展、歐洲和中東地區更嚴格的身份驗證法規以及可印刷導電油墨的進步(使每個標籤的製造成本降至0.05美元以下)推動了需求的成長。低成本的身份驗證解決方案、更長的讀取距離天線設計以及領先的被動溫度感測技術正在再形成競爭優勢。供應商正在垂直擴展至油墨、基板和中間件領域,以保護利潤並提供一站式解決方案。區塊鏈與低溫運輸監控平台的整合正在為受監管產業開闢新的收益來源。

全球無晶片 RFID 市場趨勢與洞察

低成本批量生產用於亞洲快速消費品包裝的無 IC 標籤

中國和東南亞的製造商正在將軟式電路板與銀奈米漿料結合,以實現低於五美分的標籤,從而為無晶片RFID市場在消費品多包裝中的大規模應用奠定了基礎。合約印刷商正在運作多通道柔版印刷生產線,速度超過120公尺/分鐘,每家工廠每年可印製超過20億張標籤。更快的維修投資回報以及與包裝加工商的地理位置優勢正在加速其應用。供應商正在試用可回收的纖維素基材,以符合品牌的永續性目標。隨著成本下降,一次性標籤也正在擴展到一次性電子產品和藥品單劑量包裝領域。

政府消費稅/印花稅義務

歐盟因仿冒品造成的損失估計高達160億歐元(173億美元),促使歐盟訂定了2024/1640號指令,該指令支持使用具有獨特射頻簽名的防篡改標識符。義大利、西班牙和沙烏地阿拉伯財政部目前正在為酒類和菸草印花稅票指定無晶片格式,允許印刷商將安全機制融入單張通行證中。長期合約鼓勵建立端到端可追溯平台,並開放高解析度讀取器的更換週期。東協正在考慮類似的立法,這意味著到2028年將出現第二波需求。

讀取範圍和晶片有限的超高頻系統

無晶片標籤在自由空氣中的峰值覆蓋範圍通常為3米,而晶片式超高頻標籤的覆蓋範圍可達10米或更遠,這迫使倉庫必須提高讀取器密度,並可能使基礎設施預算翻倍。目前正在研發的多層超材料天線可增加40%的覆蓋範圍,但金屬貨架和液體物品仍會衰減訊號。整合商正在採用基於區域的門戶和混合部署方案來應對這一挑戰,將無晶片標籤保留用於包裹級物品,同時繼續在托盤上使用晶片式嵌體。

細分分析

這凸顯了標籤在無晶片RFID市場所有部署場景中的重要性。亞洲合約印表機正利用其規模優勢來降低單位成本,而歐洲安全印表機則專注於高價值的身份驗證器。中介軟體收入目前規模較小,但將以26.4%的複合年成長率快速成長,因為企業需要雲端連接器、資料清理和分析功能,將原始射頻回波轉換為可操作的儀表板。

中間件的加速成長正在改變市場議價能力。軟體供應商如今正在影響硬體設計藍圖,並推動開放 API 的發展。因此,標籤製造商正在投資資訊服務團隊,以維護其市場佔有率。這一趨勢將中間件定位為未來功能的安全隔離網閘,例如預測性維護和基於人工智慧的簽章匹配。

到2024年,網版印刷將佔據38%的市場佔有率,這得益於其長期的生產力和成熟的供應鏈,尤其是在食品和飲料包裝領域。在無晶片RFID市場,噴墨列印製程正以27.7%的複合年成長率擴張,因為按需噴墨印表機可以製造出適用於高密度簽章編碼的細線天線。

採用噴墨技術也支援現場客製化。品牌商可以在產品發布前幾天印製限量版真品標識,從而降低產品過時的風險。對於大批量SKU來說,網版印刷生產線仍然佔據主導地位,因為模具攤銷可以抵消轉換成本。從用於接地層的網版印刷到用於微天線的噴墨印刷的混合生產線正日益普及,但這反映出一個過渡時期,而非徹底的替代。

區域分析

亞太地區將引領無晶片RFID市場,預計到2024年將占到總營收的40%。中國加工商正在運作整合式網版印刷和柔版印刷生產線,為國內外快速消費品品牌提供服務。澳洲郵政正在跨境小包裹上試用無晶片標籤,以減少申報詐騙。地方政府正在共同資助可生物分解基材的研究,以符合「零塑膠指令」。

北美也緊隨其後,憑藉強大的智慧財產權組合以及醫療保健和航太的早期採用者基本客群。大學正在與新興企業合作,將石墨烯油墨商業化;聯邦政府津貼支持生技藥品和關鍵備件的安全供應鏈;超級市場正在引入無晶片標籤,以減少生鮮產品的浪費,並將單品級數據與 ESG 報告掛鉤。

歐洲則位居第三,但在防偽法規的推動下,歐洲正經歷穩定成長。義大利和波蘭的稅票計畫規定了無晶片射頻安全層。北歐包裝公司正在整合紙質嵌體以實現循環經濟目標,德國機器製造商正在向亞洲原始設備製造商提供模組化噴墨頭。中東和非洲地區目前規模較小,但成長速度最快,海灣合作理事會各國央行已將紙幣的射頻認證標準化,南非海關正在對高價值出口商品引入無晶片封條。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 調查結果

- 調查前提

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場狀況

- 市場概況

- 市場促進因素

- 低成本批量生產用於亞洲快速消費品包裝的無 IC 標籤

- 政府消費稅/稅票強制令(歐盟防偽)

- 北美標籤加工產業可印刷導電油墨的進展

- 低溫運輸醫療物流中的被動式感測器

- 紙幣和安全文件認證需求(中東)

- 市場限制

- 與晶片式超高頻系統相比,讀取範圍有限

- ISO/IEC 編碼標準不一致

- 領導基礎設施維修費用

- 印刷天線易受潮濕和磨損的影響

- 價值/供應鏈分析

- 技術展望

- 印刷技術

- 噴墨

- 螢幕

- 柔版印刷

- 凹版印刷

- 印刷技術

- 監理展望

- 五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

- 投資分析

第5章市場規模及成長預測

- 依產品類型

- 標籤

- 領導者

- 中介軟體

- 按運作頻率

- LF(125-134 kHz)

- HF(13.56 MHz)

- UHF(860-960 MHz)

- 按材質

- 銀奈米墨水

- 銅基油墨

- 石墨烯/碳墨水

- 按用途

- 智慧卡

- 智慧票

- 品牌和文件認證

- 資產追蹤

- 按最終用戶產業

- 零售與電子商務

- 醫療保健和製藥

- 物流/運輸

- 銀行、金融服務和保險(BFSI)

- 政府及公共機構

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 澳洲

- 其他亞太地區

- 中東和非洲

- GCC

- 南非

- 其他中東和非洲地區

- 北美洲

第6章 競爭態勢

- 市場集中度

- 策略舉措

- 市佔率分析

- 公司簡介

- Alien Technology

- Avery Dennison

- Zebra Technologies

- SATO Holdings

- Smartrac Technology

- NXP Semiconductors

- Thinfilm Electronics ASA

- PragmatIC Semiconductor

- Impinj Inc.

- Stora Enso

- Spectra Systems Corp.

- Linxens

- TagSense

- Tageos SA

- Variuscard GmbH

- IDTRONIC GmbH

- SML Group

- Toppan Printing Co.

第7章 市場機會與未來展望

The chipless RFID market size is valued at USD 1.73 billion in 2025 and is forecast to grow to USD 5.40 billion by 2030, advancing at a 25.53% CAGR.

Demand acceleration stems from fast-moving consumer-goods packaging in Asia, stricter authentication regulations in Europe and the Middle East, and advances in printable conductive inks that have cut per-tag manufacturing costs below USD 0.05. Leadership in low-cost authentication solutions, longer read-range antenna designs, and passive temperature-sensing features is reshaping competitive priorities. Suppliers are expanding vertically into inks, substrates, and middleware in order to safeguard margins and offer one-stop solutions. Convergence with blockchain and cold-chain monitoring platforms is opening additional revenue streams in regulated industries.

Global Chipless RFID Market Trends and Insights

Lower-cost Mass Production of IC-less Tags in Asian FMCG Packaging

Manufacturers in China and Southeast Asia have combined flexible substrates with silver-nano paste to reach sub-5-cent tags, positioning the chipless RFID market for high-volume adoption in consumer-goods multipacks. Contract printers are running multi-lane flexographic lines at speeds above 120 m/min, allowing over 2 billion units per plant annually. Fast payback on retrofits and geographic proximity to packaging converters accelerate uptake. Suppliers are piloting recyclable cellulose substrates to align with brand sustainability targets. As costs fall, single-use tags are extending into disposable electronics and unit-dose pharmaceutical packs.

Government Excise / Tax-stamp Mandates

EU loss estimates of EUR 16 billion (USD 17.3 billion) in counterfeited goods prompted Directive 2024/1640, which endorses tamper-evident identifiers with unique RF signatures. Ministries of finance in Italy, Spain, and Saudi Arabia now specify chipless formats for alcohol and tobacco stamps so printers can embed security in a single press pass. Long-run contracts incentivise end-to-end traceability platforms and open replacement cycles for high-resolution readers. Similar legislation is under review in ASEAN, suggesting a second wave of demand by 2028.

Limited Read Range versus Chipped UHF Systems

Chipless tags typically peak at 3 m in free air, compared with over 10 m for chipped UHF tags, forcing warehouses to increase reader density, which can double infrastructure budgets. Multi-layer metamaterial antennas now in prototype add 40% range, yet metallic racks and liquid contents still attenuate signals. Integrators respond with zone-based portals and hybrid deployments, reserving chipless tags for package-level items while pallets continue to carry chipped inlays.

Other drivers and restraints analyzed in the detailed report include:

- Printable Conductive-Ink Advances in North American Label Converting

- Passive Sensor Adoption for Cold-chain Healthcare Logistics

- Absence of Harmonised ISO / IEC Encoding Standards

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Tag sales generated 71% of 2024 revenue, underscoring their indispensability across every deployment scenario in the chipless RFID market. Asian contract printers leverage scale to drive unit costs down, while European security printers focus on high-value authenticators. Middleware revenues, although smaller today, are set to climb faster at a 26.4% CAGR because enterprises require cloud connectors, data cleansing, and analytics to turn raw RF echoes into actionable dashboards.

Accelerated middleware growth alters bargaining power; software vendors now influence hardware design road maps and push for open APIs. As a result, tag manufacturers invest in data-services teams to defend share. The trend positions middleware as a gatekeeper for future functionality such as predictive maintenance and AI-based signature matching.

Screen printing held a 38% share in 2024 thanks to long-run productivity and mature supply chains, especially within food and beverage packaging. The chipless RFID market now sees ink-jet processes expanding at 27.7% CAGR because droplet-on-demand heads create fine-line antennas suitable for high-density signature encoding.

Ink-jet adoption also supports on-site customisation. Brand owners can print limited-edition authenticity marks days before product launch, cutting obsolescence risk. Screen lines keep their advantage in very high-volume SKUs where tooling amortisation offsets changeover costs. Hybrid lines that start with screen for ground planes and finish with ink-jet for micro-antennas are gaining traction, reflecting a transition phase rather than outright displacement.

The Chipless RFID Market is Segmented by Product Type (Tag, Reader, Middleware), Printing Technology (Ink-Jet, Screen, and More), Operating Frequency (LF 125-134 KHz, and More), Material (Silver-Nano Ink, Copper-Based Ink, and More), Application (Smart Cards, Smart Tickets, and More), End-User Industry (Retail and E-Commerce, Healthcare and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific led the chipless RFID market with 40% revenue in 2024. China's converters run integrated screen and flexographic lines, serving domestic and export FMCG brands, while Japanese rail operators extend RFID-enabled fare systems to rural routes. Australia's postal service is trialling chipless tags on cross-border parcels to cut declaration fraud. Regional governments co-fund research into biodegradable substrates, aligning with zero-plastic directives.

North America follows with strong intellectual-property portfolios and an early-adopter customer base in healthcare and aerospace. Universities collaborate with start-ups to commercialise graphene inks, and federal grants support secure supply chains for biologics and critical spare parts. Supermarket chains deploy chipless tags to reduce perishables wastage and tie item-level data into ESG reporting.

Europe ranks third yet posts steady gains driven by anti-counterfeiting mandates. Tax-stamp programs in Italy and Poland stipulate chipless RF security layers. Nordic packaging firms integrate paper inlays to meet circular-economy targets, and German machine builders ship modular ink-jet heads to Asian OEMs. The Middle East & Africa region, while smaller today, is the fastest growing; GCC central banks standardise banknote RF authentication and South African customs rolls out chipless seals on high-value exports.

- Alien Technology

- Avery Dennison

- Zebra Technologies

- SATO Holdings

- Smartrac Technology

- NXP Semiconductors

- Thinfilm Electronics ASA

- PragmatIC Semiconductor

- Impinj Inc.

- Stora Enso

- Spectra Systems Corp.

- Linxens

- TagSense

- Tageos SA

- Variuscard GmbH

- IDTRONIC GmbH

- SML Group

- Toppan Printing Co.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Lower-cost Mass-production of IC-less Tags in Asian FMCG Packaging

- 4.2.2 Government Excise/Tax-stamp Mandates (EU Counter-feiting)

- 4.2.3 Printable Conductive-Ink Advances in North American Label Converting

- 4.2.4 Passive Sensor Adoption for Cold-chain Healthcare Logistics

- 4.2.5 Banknote and Secure-Document Authentication Demand (Middle East)

- 4.3 Market Restraints

- 4.3.1 Limited Read Range vs. Chipped UHF Systems

- 4.3.2 Absence of Harmonised ISO/IEC Encoding Standards

- 4.3.3 Retrofit Cost of Reader Infrastructure

- 4.3.4 Moisture and Abrasion Vulnerability of Printed Antennas

- 4.4 Value / Supply-Chain Analysis

- 4.5 Technological Outlook

- 4.5.1 Printing Technologies

- 4.5.1.1 Ink-jet

- 4.5.1.2 Screen

- 4.5.1.3 Flexographic

- 4.5.1.4 Gravure

- 4.5.1 Printing Technologies

- 4.6 Regulatory Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Tag

- 5.1.2 Reader

- 5.1.3 Middleware

- 5.2 By Operating Frequency

- 5.2.1 LF (125-134 kHz)

- 5.2.2 HF (13.56 MHz)

- 5.2.3 UHF (860-960 MHz)

- 5.3 By Material

- 5.3.1 Silver-nano Ink

- 5.3.2 Copper-based Ink

- 5.3.3 Graphene/Carbon Ink

- 5.4 By Application

- 5.4.1 Smart Cards

- 5.4.2 Smart Tickets

- 5.4.3 Brand and Document Authentication

- 5.4.4 Asset Tracking

- 5.5 By End-user Industry

- 5.5.1 Retail and E-commerce

- 5.5.2 Healthcare and Pharmaceuticals

- 5.5.3 Logistics and Transportation

- 5.5.4 Banking, Financial Services and Insurance (BFSI)

- 5.5.5 Government and Public Sector

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 South Korea

- 5.6.4.4 India

- 5.6.4.5 Australia

- 5.6.4.6 Rest of Asia Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 GCC

- 5.6.5.2 South Africa

- 5.6.5.3 Rest of Middle East and Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Alien Technology

- 6.4.2 Avery Dennison

- 6.4.3 Zebra Technologies

- 6.4.4 SATO Holdings

- 6.4.5 Smartrac Technology

- 6.4.6 NXP Semiconductors

- 6.4.7 Thinfilm Electronics ASA

- 6.4.8 PragmatIC Semiconductor

- 6.4.9 Impinj Inc.

- 6.4.10 Stora Enso

- 6.4.11 Spectra Systems Corp.

- 6.4.12 Linxens

- 6.4.13 TagSense

- 6.4.14 Tageos SA

- 6.4.15 Variuscard GmbH

- 6.4.16 IDTRONIC GmbH

- 6.4.17 SML Group

- 6.4.18 Toppan Printing Co.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

2025年全球醫療保健智慧卡讀卡機市場報告

2025年全球醫療保健智慧卡讀卡機市場報告 無晶片 RFID 市場(按組件類型、行業垂直和地區分類)2025年印刷無晶片RFID全球市場報告

無晶片 RFID 市場(按組件類型、行業垂直和地區分類)2025年印刷無晶片RFID全球市場報告 無晶片RFID市場分析及預測(至2034年):類型、產品、技術、應用、組件、材料類型、部署、最終用戶、功能

無晶片RFID市場分析及預測(至2034年):類型、產品、技術、應用、組件、材料類型、部署、最終用戶、功能 無晶片 RFID 市場規模、佔有率和成長分析(按產品類型、頻段、應用、最終用戶和地區)- 產業預測 2025-2032全球醫療保健智慧卡讀卡機市場醫療保健智慧卡讀卡機市場機會、成長動力、產業趨勢分析和 2025 年至 2034 年預測無晶片 RFID 的全球市場

無晶片 RFID 市場規模、佔有率和成長分析(按產品類型、頻段、應用、最終用戶和地區)- 產業預測 2025-2032全球醫療保健智慧卡讀卡機市場醫療保健智慧卡讀卡機市場機會、成長動力、產業趨勢分析和 2025 年至 2034 年預測無晶片 RFID 的全球市場 無晶片 RFID 市場 – 2024 年至 2029 年預測印刷式和無晶片 RFID 市場規模、佔有率和趨勢分析報告:按類型、按應用、按地區、細分市場預測,2024-2030 年

無晶片 RFID 市場 – 2024 年至 2029 年預測印刷式和無晶片 RFID 市場規模、佔有率和趨勢分析報告:按類型、按應用、按地區、細分市場預測,2024-2030 年