|

市場調查報告書

商品編碼

1844586

奈米塗料和塗層:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)Nano Paints And Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

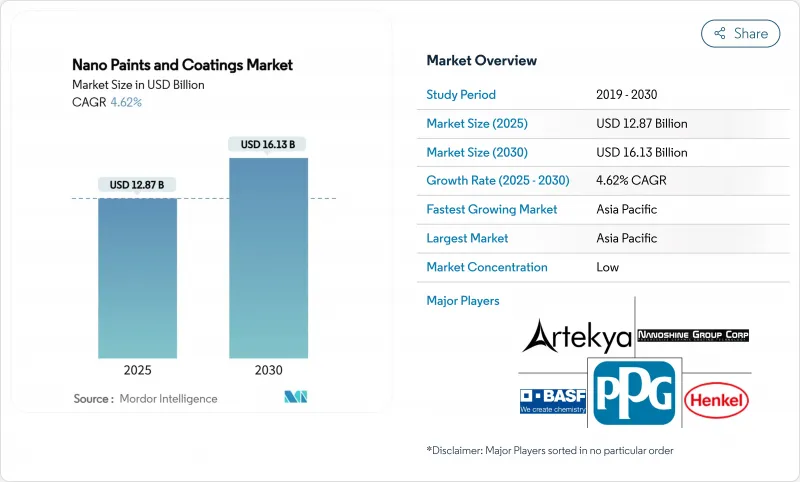

預計 2025 年奈米油漆和塗料市場規模將達到 128.7 億美元,預計到 2030 年將達到 161.3 億美元,預測期內(2025-2030 年)的複合年成長率為 4.62%。

航太對防腐輕量化解決方案的需求不斷成長,電動車的消防安全要求不斷提高,基礎設施的耐久性需求不斷增加,這些因素推動著市場穩步上升。奈米二氧化鈦占主導地位,市佔率達 39.17%,加之石墨烯以 5.17% 的複合年成長率快速成長,展現了先進奈米材料在維持競爭優勢的核心作用。亞太地區發展動能依然強勁,佔全球銷售額的近一半,是成長最快的地區。化學氣相沉積 (CVD) 材料的進步以及向集防腐、溫度控管和抗菌性能於一體的多功能配方的轉變正在創造新的機遇,而高昂的製造成本和不斷變化的奈米毒性法規則阻礙了快速擴大規模。

全球奈米塗料和塗料市場趨勢和洞察

航太和國防領域的腐蝕-輕量化的推動力

美國估計,軍事裝備的腐蝕每年對軍方造成230億美元的損失,這推動了奈米塗層的應用,兼具結構輕盈性和卓越防護性能。現場數據顯示,奈米工程塗層可縮短海軍飛機機身的維修週期,其防冰特性可提高飛機在極端氣候條件下的戰備能力。美國SBIR(小規模創新研究)計畫正在從實驗室研究轉向艦隊試驗,這表明嚴格的認證障礙限制了新進入者,同時確保了對可靠供應商的持續需求。由於國防籌資策略傾向於降低總擁有成本的平台,因此,能夠解決重量、耐久性和環境暴露挑戰的一次性奈米配方的需求日益成長。

電動車隔熱和防火塗料的需求不斷成長

快速電氣化正在推動電池系統朝向更高的能量密度和更嚴格的安全標準邁進。專用奈米層可快速散熱並形成阻燃屏障,保護電芯和相鄰組件。 Resonac 用於電動車電池組的隔熱產品凸顯了其積極的商業化發展。碳和石墨烯分散體在不犧牲介電強度的情況下提供導熱性,符合 OEM 安全通訊協定。同時,像現代的奈米冷卻膜這樣的乘客舒適解決方案可將車內溫度降低 10°C,展現出輔助應用的潛力。納入熱失控抑制的法律規範將加速大規模採用,尤其是在電池產能最高的亞太地區。

奈米材料製造成本高

專用CVD反應器、低產量比率批量製程以及嚴格的純度要求導致單位成本居高不下。儘管技術性能優勢明顯,但資金需求阻礙了消費家具等價格敏感應用的採用。儘管創業投資持續注入,例如Forge Nano的4000萬美元融資,但許多規模化項目仍處於試點階段,這意味著成本下降將是漸進而非快速的。生產商正在尋求在線計量、前體回收和混合濕化學技術來降低成本,但盈虧平衡的經濟效益仍依賴高階應用。

細分分析

到 2024 年,奈米二氧化鈦將在奈米油漆和塗料市場保持 39.17% 的佔有率。其穩定的製造、光催化自清潔性能和成本效益正在推動其在建築幕牆、汽車裝飾和室內防霧板的應用。韓國一條試驗生產線使用二氧化鈦奈米顆粒生產超大透明螢幕,價格僅為 OLED 玻璃的十分之一,證實了該材料的擴充性。石墨烯仍然是一種適度的參與者,但隨著對電池散熱器和電磁屏蔽的需求成長,到 2030 年其複合年成長率將達到 5.17%。奈米碳管仍將是航太和高階消費性電子產品的利基選擇,這些產品兼具結構剛性、導電性和輕量化。奈米 SiO2 將在水泥添加劑中佔據突出地位,以延長基礎設施的使用壽命,而奈米 ZnO 將確保醫療設備和智慧型手機的紫外線阻隔塗層。未來的成長預計將來自於結合多種奈米粒子以產生協同效應的混合配方。

預計用於二氧化鈦樹脂的奈米塗料和塗層市場規模將穩定成長,而由於供應鏈的自由化和反應器產能的擴大,石墨烯的佔有率也將迅速擴大。為了配合這一發展軌跡,正在同步推廣使用生物基前驅物和無溶劑分散體的綠色合成路線,以減少碳排放。

區域分析

亞太地區將維持領先地位,到2024年將佔全球銷售額的45.43%,預計複合年成長率為4.91%。中國的電子供應鏈、日本的材料科學叢集以及韓國的顯示器工廠將確保基準的穩定性。中國的「中國製造2025」計畫和日本的「登月計畫」研發目標等獎勵將加速奈米生產能力的提升並縮短前置作業時間。本地CVD反應器供應商將把該技術推廣到頂級企業集團之外,使中型塗層工廠能夠認證奈米產品。

北美的需求集中在航太、國防和醫療設備領域。美國保障司令部和航太運載火箭主管機關將奈米塗層視為降低維修成本的戰略途徑。墨西哥蓬勃發展的電動車組裝生態系統進口熱感熱膜和電池塗層系統,並與當地供應商無縫整合。歐洲對生態設計和工人安全的重視,正在推動符合 REACH 和綠色建築標籤標準的奈米配方水性被覆劑的應用。一家德國一級汽車供應商和一家法國航太原始設備製造商已與奈米塗層專家簽署了多年期框架協議。

在南美洲,巴西交通走廊和阿根廷頁岩油氣資源的基礎設施修復工作正在蓬勃發展。鹽霧、高濕度和紫外線的暴露使得高性能塗料變得至關重要,當地塗料製造商正在與日本和德國的奈米材料製造商合作,以實現塗料混合物的本地化。中東的能源產業正在地下泵浦和出口管道上試驗奈米層,以抵抗酸性腐蝕。同時,非洲的成長故事在於供水網路,其中內部應用的奈米密封劑可以降低高溫環境下的洩漏率。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場狀況

- 市場概況

- 市場促進因素

- 航太和國防領域的腐蝕-輕量化的推動力

- 電動車對耐熱和防火塗料的需求不斷增加

- 對高性能塗料的需求不斷增加

- 基礎設施領域需求增加

- 電子產品和消費品的使用增加

- 市場限制

- 奈米材料製造成本高

- 奈米毒性監管的不確定性

- 石墨烯CVD反應器供應瓶頸

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章市場規模及成長預測

- 依樹脂類型

- 石墨烯

- 奈米碳管

- 奈米 TiO2(二氧化鈦)

- 奈米SiO2(二氧化矽)

- 奈米氧化鋅

- 奈米銀

- 依方法

- 電灑/靜電紡絲

- 化學氣相沉積(CVD)

- 物理氣相沉積(PVD)

- 原子層沉澱(ALD)

- 氣溶膠塗層

- 自組織

- 溶膠-凝膠

- 按最終用戶產業

- 航太/國防

- 車

- 電子學和光學

- 生物醫學

- 食品/包裝

- 海洋

- 石油和天然氣

- 其他終端用戶產業(能源/電力、建築/基礎設施等)

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭態勢

- 市場集中度

- 策略舉措

- 市佔率(%)/排名分析

- 公司簡介

- Aculon

- Artekya Teknoloji

- BASF

- Europlasma NV

- Graphene NanoChem

- GVD Corporation

- Henkel AG and Co. KGaA

- I-CanNano

- Nanofilm

- Nanoshine Group Corp

- Pearl Global Ltd.

- Pellucere

- PPG Industries, Inc.

- SIA Naco Technologies

- Starshield Technologies Pvt Ltd

- Tesla NanoCoatings Inc.

第7章 市場機會與未來展望

The Nano Paints & Coatings Market size is estimated at USD 12.87 billion in 2025, and is expected to reach USD 16.13 billion by 2030, at a CAGR of 4.62% during the forecast period (2025-2030).

Growing aerospace demand for corrosion-lightweight solutions, electric vehicle fire-safety requirements, and infrastructure durability needs keep the market on a steady upward course. A dominant 39.17% nano-TiO2 share combined with graphene's rapid 5.17% CAGR underlines the core role of advanced nanomaterials in sustaining competitive advantage. Regional momentum remains firmly with Asia-Pacific, which controls almost half of global revenues and commands the fastest regional growth. Supply advances in chemical vapor deposition (CVD) and a shift toward multifunctional formulations that merge corrosion protection, thermal management, and antimicrobial performance are shaping new business opportunities, while high production costs and evolving nano-toxicity rules restrain rapid scale-up.

Global Nano Paints And Coatings Market Trends and Insights

Aerospace and defense corrosion-light-weight push

Pentagon estimates that corrosion costs USD 23 billion each year across military equipment, intensifying the adoption of nano coatings that combine structural lightness with superior protection. Field data show nano-engineered layers lowering maintenance cycles on naval airframes, while icephobic properties enhance aircraft readiness in extreme climates. Programs under the U.S. Navy SBIR banner are moving from bench research to fleet trials, illustrating that rigorous certification barriers simultaneously limit new entrants and guarantee durable demand for validated suppliers. As defense procurement strategies favor platforms with reduced total ownership cost, single-application nano formulations that solve weight, durability, and environmental exposure challenges are increasingly specified.

Increase in demand for EV thermal-fire-safety coating

Rapid electrification pushes battery systems toward higher energy density and stricter safety standards. Specialized nano layers dissipate heat swiftly and form fire-retardant barriers, protecting cells and adjacent components. Resonac's thermal insulation product for EV packs highlights active commercial development. Carbon and graphene dispersions deliver thermal conductivity without sacrificing dielectric strength, matching OEM safety protocols. In parallel, passenger-comfort solutions such as Hyundai's nano cooling film that cuts cabin temperature by 10 °C demonstrate spill-over into ancillary applications. Regulatory frameworks that incorporate thermal runaway containment accelerate volume adoption, especially in Asia-Pacific, where battery production capacity is highest.

High production cost of nanomaterials

Specialized CVD reactors, low-yield batch processes, and stringent purity requirements keep unit costs elevated. Capital requirements delay adoption in price-sensitive uses such as consumer furniture, despite technical performance benefits. Venture capital continues to inject funds-Forge Nano's USD 40 million raise underscored private backing-but many scale-up programs remain in pilot phase, pointing to gradual cost attrition rather than abrupt drops. Producers pursue inline metrology, precursor recycling, and hybrid wet-chemistry steps to cut expenses, yet breakeven economics still hinge on premium applications.

Other drivers and restraints analyzed in the detailed report include:

- Growing requirement for high performance coatings

- Increasing demand from infrastructure sector

- Nano-toxicity regulatory uncertainty

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Nano-TiO2 kept its 39.17% hold on the nano paints & coatings market in 2024. Stable manufacturing, photocatalytic self-cleaning performance, and cost efficiency drive its acceptance on facades, automotive trims, and indoor anti-smog panels. Korean pilot lines producing ultra-large transparent screens using TiO2 nanoparticles at one-tenth the price of OLED glass underscore this material's scalability. Graphene, although capped at a modest base, posts a 5.17% CAGR through 2030 as demand from battery heat spreaders and electromagnetic shielding intensifies. Carbon nanotubes remain a niche choice for aerospace and high-end consumer electronics where structural stiffness, conductivity, and weight savings converge. Nano-SiO2 extends its presence in cement additions that lengthen infrastructure life, and nano-ZnO secures UV-blocking coatings for medical devices and smartphones. Future growth leans on hybrid recipes pairing multiple nanoparticles to secure synergistic properties.

The nano paints & coatings market size for titanium dioxide resin applications is projected to widen steadily, while graphene's share expands faster under supply chain releases and reactor capacity additions. Complementing that trajectory is a parallel push for green synthesis routes that use bio-derived precursors or solvent-free dispersion to cut carbon footprint.

The Nano Paints & Coatings Market Report is Segmented by Resin Type (Graphene, Carbon Nanotubes, Nano-TiO2, and More), Method (Electrospray and Electrospinning, Chemical Vapor Deposition, and More), End-User Industry (Aerospace and Defense, Automotive, Biomedical, and More), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific anchored 45.43% of global revenue in 2024, keeping the lead with a 4.91% CAGR outlook. China's electronics supply chains, Japan's materials science clusters, and South Korea's display fabs guarantee a stable baseline. Policy incentives, such as China's Made-in-China 2025 priorities and Japan's Moonshot R&D goals, accelerate nano production capability, shortening lead times. Local CVD reactor suppliers help diffuse technology beyond top-tier conglomerates, enabling mid-size coating shops to certify nano offerings.

North America's demand profile centers on aerospace, defense, and medical devices. U.S. Air Force sustainment commands and space launch primes view nano-layering as strategic maintenance cost reducers. Mexico's ascending EV assembly ecosystem imports nano thermal films and battery coating systems, integrating seamlessly with regional supply. Europe champions eco-design and worker safety, thus driving the adoption of nano-formulated water-borne coatings that satisfy REACH and green building labels. Germany's automotive Tier-1 suppliers and France's aerospace OEMs lock up multi-year framework agreements with nano-coating specialists.

South America injects momentum from infrastructure rehabilitation commitments in Brazil's transport corridors and Argentina's shale play servicing. Exposure to salt spray, high humidity, and UV intensity places a premium on high-performance coatings, and local paint majors partner with Japanese and German nanomaterial producers to localize blends. The Middle East's energy sector trials nano layers on downhole pumps and export pipelines to combat sour corrosion, while Africa's growth story lies in water networks, where internally applied nano sealants cut leak rates under high ambient heat.

- Aculon

- Artekya Teknoloji

- BASF

- Europlasma NV

- Graphene NanoChem

- GVD Corporation

- Henkel AG and Co. KGaA

- I-CanNano

- Nanofilm

- Nanoshine Group Corp

- Pearl Global Ltd.

- Pellucere

- PPG Industries, Inc.

- SIA Naco Technologies

- Starshield Technologies Pvt Ltd

- Tesla NanoCoatings Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Aerospace and defense corrosion-light-weight push

- 4.2.2 Increase in demand for EV thermal-fire-safety coating

- 4.2.3 Growing requirement for high performance coatings

- 4.2.4 Inceasing demand from infrastructure sector

- 4.2.5 Rise in utilization from electronics and consumer goods

- 4.3 Market Restraints

- 4.3.1 High production cost of nanomaterials

- 4.3.2 Nano-toxicity regulatory uncertainty

- 4.3.3 Graphene CVD reactor supply bottlenecks

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products and Services

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Resin Type

- 5.1.1 Graphene

- 5.1.2 Carbon Nanotubes

- 5.1.3 Nano-TiO2 (Titanium Dioxide)

- 5.1.4 Nano-SiO2 (Silicon Dioxide)

- 5.1.5 Nano-ZnO

- 5.1.6 Nano Silver

- 5.2 By Method

- 5.2.1 Electrospray and Electrospinning

- 5.2.2 Chemical Vapor Deposition (CVD)

- 5.2.3 Physical Vapor Deposition (PVD)

- 5.2.4 Atomic Layer Deposition (ALD)

- 5.2.5 Aerosol Coating

- 5.2.6 Self-Assembly

- 5.2.7 Sol-Gel

- 5.3 By End-User Industry

- 5.3.1 Aerospace and Defense

- 5.3.2 Automotive

- 5.3.3 Electronics and Optics

- 5.3.4 Biomedical

- 5.3.5 Food and Packaging

- 5.3.6 Marine

- 5.3.7 Oil and Gas

- 5.3.8 Other End-user Industries (Energy and Power, Construction and Infrastructure, etc.)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Aculon

- 6.4.2 Artekya Teknoloji

- 6.4.3 BASF

- 6.4.4 Europlasma NV

- 6.4.5 Graphene NanoChem

- 6.4.6 GVD Corporation

- 6.4.7 Henkel AG and Co. KGaA

- 6.4.8 I-CanNano

- 6.4.9 Nanofilm

- 6.4.10 Nanoshine Group Corp

- 6.4.11 Pearl Global Ltd.

- 6.4.12 Pellucere

- 6.4.13 PPG Industries, Inc.

- 6.4.14 SIA Naco Technologies

- 6.4.15 Starshield Technologies Pvt Ltd

- 6.4.16 Tesla NanoCoatings Inc.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

奈米塗層市場:按類型、材料、應用和最終用途產業分類-2026-2032年全球市場預測

奈米塗層市場:按類型、材料、應用和最終用途產業分類-2026-2032年全球市場預測 奈米塗層市場報告:按產品類型、最終用戶和地區分類(2026-2034 年)抗菌奈米塗層市場:2026-2032年全球市場預測(按應用、類型、最終用戶、形態和技術分類)

奈米塗層市場報告:按產品類型、最終用戶和地區分類(2026-2034 年)抗菌奈米塗層市場:2026-2032年全球市場預測(按應用、類型、最終用戶、形態和技術分類) 奈米塗層市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測全球防冰除冰奈米塗層市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

奈米塗層市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測全球防冰除冰奈米塗層市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026年全球奈米塗層市場報告日本奈米塗層市場報告(按產品類型(抗菌、防指紋、防污、易清潔、自清潔)、最終用戶(建築、食品包裝、醫療保健、電子、汽車、船舶及其他)和地區分類,2026-2034年)

2026年全球奈米塗層市場報告日本奈米塗層市場報告(按產品類型(抗菌、防指紋、防污、易清潔、自清潔)、最終用戶(建築、食品包裝、醫療保健、電子、汽車、船舶及其他)和地區分類,2026-2034年) 奈米塗層市場規模、佔有率和成長分析(按類型、基材、應用和地區分類)-2026-2033年產業預測

奈米塗層市場規模、佔有率和成長分析(按類型、基材、應用和地區分類)-2026-2033年產業預測 全球奈米塗層市場:數據報告

全球奈米塗層市場:數據報告 面向工業4.0的智慧表面塗層全球市場:預測至2032年-按塗層類型、功能、技術、最終用戶和地區分類的分析

面向工業4.0的智慧表面塗層全球市場:預測至2032年-按塗層類型、功能、技術、最終用戶和地區分類的分析