|

市場調查報告書

商品編碼

1844576

汽車玻璃:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)Automotive Glass - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

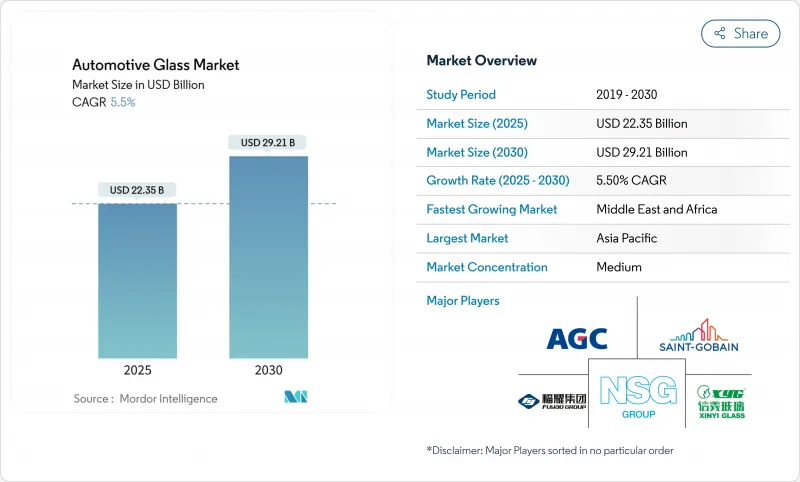

預計汽車玻璃市場規模在 2025 年將達到 223.5 億美元,在 2030 年將達到 292.1 億美元,在預測期內(2025-2030 年)的複合年成長率將達到 5.5%。

儘管原料價格和物流成本波動,但汽車產量的不斷成長、更嚴格的安全法規以及向電動車的轉變仍保持著強勁勢頭。全景天窗、輕質夾層擋風玻璃和電致變色嵌裝玻璃的需求不斷成長,促使製造商拓展專業產品線並深化與原始設備製造商 (OEM) 的夥伴關係。 SUV 車型對更大玻璃表面的重視,加上減少二氧化碳排放的監管壓力,正在加速塗層和多功能產品的採用。這些綜合因素很可能在未來十年推動汽車玻璃市場強勁的技術主導成長。

全球汽車玻璃市場趨勢與洞察

電動車平台轉向全景玻璃

電動車製造商正在採用更大的車頂玻璃來提升車內氛圍和品牌形象。特斯拉的 Cybertruck 和梅賽德斯-奔馳的 Vision V 概念車均配備了可調節色調的電致變色車頂,可將車內溫度降低高達 -5°C,並減少空調負載。預計每輛車的玻璃面積將大幅增加,促使供應商投資寬彎玻璃、低輻射鍍膜和紅外線吸收中間膜。這些高階規格,加上不斷下降的生產成本,預計將逐漸滲透到中等價格分佈的電動車中,從而支持汽車玻璃市場的持續成長。

OEM對輕質夾層玻璃的需求以滿足二氧化碳排放目標

歐洲法規設定了2030年全車平均二氧化碳排放目標,即每公里100克,迫使汽車製造商每行駛一公斤就減少排放。根據美國環保署對2017款福特GT的研究,夾層玻璃對車輛減重30%做出了顯著貢獻。採用離子塑膠中間膜的薄規格夾層玻璃可在不影響抗衝擊性能的情況下,可減輕高達30%的重量。 AGC和聖戈班已將一款兼具輕量化和減震性能的1.6毫米擋風玻璃商業化,增強了汽車玻璃市場的長期前景。

特種中間膜(PVB、離子性塑膠)供應鏈緊縮

KURARAY CO. LTD.的PVB產能擴充未能跟上隔音和HUD級薄膜日益成長的需求,導致前置作業時間延長和限量供應。歐洲貼合機報告稱,供不應求時有發生,迫使他們優先考慮OEM生產,而非售後市場訂單。實驗性生物基中間膜的機械優勢可望達到53.1%,但規模化生產仍面臨挑戰。短期供應壓力可能會在新廠投產前抑制汽車玻璃市場的成長。

細分分析

受成本效益和現有生產設備的推動,到2024年,普通玻璃將佔據汽車玻璃市場的82.70%。夾層玻璃的市場佔有率正在超過強化玻璃,因為它在撞擊時不易破碎,並且符合全球安全標準。這種轉變正在導致特種中間膜的供應趨緊,但隨著原始設備製造商對更薄更輕的結構的需求,夾層玻璃貼合機將獲得更高的價值。智慧玻璃目前仍是少數市場,預計將以12.8%的複合年成長率成長,在豪華車和高階電動車領域佔有一席之地。

電致變色車頂正處於早期應用階段,而懸浮顆粒裝置 (SPD) 則具有快速切換和耐用性,正如梅賽德斯-奔馳 Vision V 原型車所展示的那樣。聚合物分散液晶 (PDLC) 車窗旨在實現隱私隔間,而感溫變色薄膜尚未商業化。隨著規模經濟的提升,智慧玻璃將擴展到旗艦車型以外的領域,從而增強汽車玻璃市場。

受強制安裝和ADAS感測器搭載率上升的推動,擋風玻璃將在2024年佔據汽車玻璃市場規模的44.60%。複雜性推高了單位成本,並加劇了供應商和原始設備製造商之間的共同開發週期。然而,隨著SUV車型標配更大的全景天窗,天窗成為成長最快的應用,複合年成長率達到10.2%。

背光玻璃採用隔音層壓板,市場發展勢頭強勁,但保固問題阻礙了其發展。為了滿足防跳法律法規,側燈正在轉向層壓結構,尤其是在歐洲和日本。後視鏡和三角窗正在整合電致變色防眩光塗層,從而增加了無需大面積覆蓋的功能。這些應用組合正在支持汽車玻璃市場的穩定擴張。

區域分析

受中國龐大的產量和強勁的國內需求推動,亞太地區將在2024年佔據汽車玻璃市場的49.20%。政府的獎勵措施在很大程度上維持了工廠產能,而印度的產量成長正成為新的需求驅動力。此次上海會議將重點關注智慧嵌裝玻璃、LiDAR透明度和擴增實境-抬頭顯示器 (AR-HUD) 整合,展示持續的技術創新。日本和韓國為高階汽車製造商 (OEM) 提供先進的夾層和鍍膜產品,在整個汽車玻璃市場中佔據著利潤豐厚的利基市場。

生產商正透過轉向智慧玻璃和永續性項目來應對來自中國進口玻璃的利潤壓力。 AGC 和聖戈班共同開發的 Volta 熔爐代表著降低二氧化碳排放強度的策略性舉措。同時,北美市場正受到 SUV 需求的影響。美國的售後市場正在蓬勃發展,像 Auto Glass Now 這樣的品牌正在擴大在全國的影響力,並抓住更換需求。

預計中東和非洲將成長最快,到2030年的複合年成長率將達到7.1%。沙烏地阿拉伯富含矽的礦床吸引了旨在滿足當地供應的浮法玻璃投資。與更廣泛的行業多元化議程相符的補貼鼓勵了汽車零件的生產,並擴大了該地區在汽車玻璃市場的地位。南美的前景主要與巴西的組裝量有關,而非洲的成長中心是南非相對成熟的汽車玻璃產業。鄰近策略可以幫助全球供應商平衡這些不同地區的運費和準時預期。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場狀況

- 市場概況

- 市場促進因素

- 電動車平台轉向全景嵌裝玻璃

- OEM對輕質夾層玻璃的需求以滿足二氧化碳排放目標

- SUV天窗的快速普及

- 法規要求側窗必須使用安全玻璃

- 高階 OEM 廠商配備 HUD 功能的擋風玻璃數量增加

- 用於 ADAS 功能的嵌入式感測器整合

- 市場限制

- 特殊中間膜(PVB、離子性塑膠)供不應求

- 中國浮法玻璃產能過剩導致利潤率下降,衝擊歐盟市場

- SUV 隔音層壓背光燈的保固成本高昂

- 成熟的售後市場通路更換週期緩慢

- 價值鏈分析

- 五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- OEM和售後市場趨勢分析

第5章市場規模及成長預測

- 按玻璃類型

- 普通玻璃

- 夾層玻璃

- 強化玻璃

- 智慧玻璃

- 電致變色

- 懸浮顆粒物檢測裝置(SPD)

- 聚合物分散液晶(PDLC)

- 感溫變色

- 普通玻璃

- 按用途

- 擋風玻璃

- 背光(後窗)

- 側光

- 天窗

- 後視鏡和側視鏡

- 其他玻璃(四分之一玻璃和通風玻璃)

- 按車輛類型

- 搭乘用車

- 掀背車

- 轎車

- SUV與跨界車

- 奢侈品與運動

- 輕型商用車

- 中大型商用車

- 搭乘用車

- 透過促銷

- 內燃機(ICE)

- 純電動車(BEV)

- 混合動力電動車(HEV/PHEV)

- 燃料電池電動車(FCEV)

- 按銷售管道

- OEM

- 售後市場

- 按地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 紐西蘭

- 其他亞太地區

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 其他中東和非洲地區

- 北美洲

第6章 競爭態勢

- 市場集中度

- 策略舉措

- 市佔率分析

- 公司簡介

- AGC Inc.(Asahi Glass)

- Saint-Gobain SA

- Nippon Sheet Glass Co. Ltd.

- Fuyao Glass Industry Group Co. Ltd.

- Xinyi Glass Holdings Ltd.

- Guardian Automotive(Koch Industries)

- Webasto SE

- Carlex Glass America LLC

- Magna International Inc.

- Vitro Automotive

- Corning Incorporated

- Sisecam Automotive

- Shanghai Yaohua Pilkington Glass

- Gentex Corporation

- AGP Group

第7章 市場機會與未來展望

The automotive glass market size stands at USD 22.35 billion in 2025 and is projected to reach USD 29.21 billion by 2030, reflecting a steady 5.5% CAGR during the forecast period (2025-2030).

Rising vehicle production, stricter safety mandates, and the shift toward electric mobility are sustaining momentum even as raw-material prices and logistics costs fluctuate. Growing demand for panoramic roofs, lightweight laminated windshields, and electrochromic glazing is encouraging manufacturers to scale specialized lines and deepen partnerships with OEMs. The emphasis on larger glass surfaces in SUVs, coupled with regulatory pressure to cut CO2 emissions, is accelerating the adoption of coated and multi-functional products. Together, these forces position the automotive glass market for resilient, technology-led growth through the decade.

Global Automotive Glass Market Trends and Insights

Shift Toward Panoramic Glazing In EV Platforms

Electric-vehicle makers are installing larger roof panes to enhance cabin ambience and brand identity. Tesla's Cybertruck and Mercedes-Benz's Vision V concept integrate electrochromic roofs that modulate tint levels, cutting cabin temperatures by up to 18°F and lowering HVAC loads. Glass area per vehicle is forecast to surge, prompting suppliers to invest in wide-format bending, low-E coatings, and infrared-absorbing interlayers. This premium specification is expected to permeate mid-priced EVs as production costs fall, supporting sustained growth in the automotive glass market.

OEM Demand For Lightweight Laminated Glass To Meet CO2 Targets

European regulations set a 100 g/km fleet-average CO2 goal for 2030, pushing automakers to shave every kilogram. EPA studies of the 2017 Ford GT show laminated glazing contributed materially to a 30% mass drop. Thin-gauge laminates using ionoplast interlayers now trim weight by up to 30% without compromising impact performance. AGC and Saint-Gobain are commercializing 1.6-mm windshield constructions that pair weight savings with acoustic damping, reinforcing long-term prospects for the automotive glass market.

Supply-Chain Crunch Of Specialty Interlayers (PVB, Ionoplast)

Kuraray's PVB capacity expansions have not kept pace with rising demand for acoustic and HUD-grade films, extending lead times and forcing allocation programs. European laminators report spot shortages, compelling them to prioritize OEM production over aftermarket orders. Experimental bio-based interlayers deliver promising mechanical gains of 53.1% but remain years from scale. Short-term supply stress may temper automotive glass market growth until new plants start up.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Sunroof Penetration In SUVs

- Regulation-Led Mandatory Safety Glazing For Side Windows

- Margin Erosion From Chinese Float-Glass Overcapacity Flooding EU Market

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Regular glass commanded 82.70% of the automotive glass market share in 2024, thanks to cost efficiency and entrenched production assets. Laminated variants are gaining against tempered formats because they keep shards intact on impact, satisfying global safety norms. The shift tightens the supply of specialty interlayers, yet it positions laminators for higher value capture as OEMs demand thinner, lighter constructions. Smart glass, though only a minority today, is projected to post a 12.8% CAGR, carving out niches in luxury vehicles and high-end EVs.

Electrochromic roofs dominate early adoption; suspended particle devices (SPD) deliver faster switching and durability, as shown in Mercedes-Benz's Vision V prototype. Polymer-dispersed liquid crystal (PDLC) windows target privacy partitions, while thermochromic films remain pre-commercial. As economies of scale improve, smart glass will expand beyond flagships, bolstering the automotive glass market.

Windshields held 44.60% of the automotive glass market size in 2024, underpinned by mandatory fitment and rising ADAS sensor content. Complexity drives up unit value, reinforcing supplier-OEM co-development cycles. Sunroofs, however, are the fastest-growing application at 10.2% CAGR as SUVs standardize large openings for panoramic vistas.

Backlites see modest traction from acoustic laminates, though warranty issues temper speed. Sidelites transition to laminated construction to meet ejection-prevention laws, especially in Europe and Japan. Rear-view mirrors and quarter windows integrate electrochromic anti-glare coatings, adding feature content without large area demand. Collectively, the application mix underpins steady expansion in the automotive glass market.

The Automotive Glass Market Report is Segmented by Glass Type (Regular Glass and Smart Glass), Application (Windshield, Sunroof and More), Vehicle Type (Passenger Cars, and More), Propulsion (Internal Combustion Engine, Battery Electric Vehicle (BEV), and More), Sales Channel (OEM, and Aftermarket), and Geography. The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific dominated the automotive glass market, with 49.20% of the revenue in 2024, anchored by China's vast output and rapid domestic uptake. Government incentives have kept plants near capacity, while India's production climb adds a fresh demand axis. Conferences in Shanghai spotlight intelligent glazing, LiDAR transparency, and AR-HUD integration, showcasing continual innovation. Japan and South Korea supply advanced laminated and coated products for premium OEMs, preserving high-margin niches as part of the broader automotive glass market.

Producers combat margin squeeze from Chinese imports by pivoting into smart glass and sustainability programs. AGC and Saint-Gobain's joint Volta furnace evidences a strategic move to slash CO2 intensity. Meanwhile, North America remains influential due to the demand for SUVs. The United States features vibrant aftermarket activity; brands such as Auto Glass Now scale national footprints to capture replacement revenue.

The Middle East and Africa are expected to be the fastest climbers at 7.1% CAGR through 2030. Saudi Arabia's silica-rich deposits attract float-glass investments intended to localize supply. Subsidies aligned with broader industrial-diversification agendas incentivize auto-component production, broadening the region's stake in the automotive glass market. South America's outlook is tied chiefly to Brazilian assembly volumes, while Africa's growth centers on South Africa's relatively mature sector. Proximity production strategies help global suppliers balance freight costs and just-in-time expectations across these varied geographies.

- AGC Inc. (Asahi Glass)

- Saint-Gobain S.A.

- Nippon Sheet Glass Co. Ltd.

- Fuyao Glass Industry Group Co. Ltd.

- Xinyi Glass Holdings Ltd.

- Guardian Automotive (Koch Industries)

- Webasto SE

- Carlex Glass America LLC

- Magna International Inc.

- Vitro Automotive

- Corning Incorporated

- Sisecam Automotive

- Shanghai Yaohua Pilkington Glass

- Gentex Corporation

- AGP Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Shift Toward Panoramic Glazing In EV Platforms

- 4.2.2 OEM Demand For Lightweight Laminated Glass To Meet CO2 Targets

- 4.2.3 Rapid Sunroof Penetration In SUVs

- 4.2.4 Regulation-Led Mandatory Safety Glazing For Side Windows

- 4.2.5 Growing Retrofit Of HUD-Compatible Windshields By Premium OEMs

- 4.2.6 Integration Of Embedded Sensors For ADAS Functionality

- 4.3 Market Restraints

- 4.3.1 Supply-Chain Crunch Of Specialty Interlayers (PVB, Ionoplast)

- 4.3.2 Margin Erosion From Chinese Float-Glass Overcapacity Flooding EU Market

- 4.3.3 High Warranty Costs Linked To Acoustic Laminated Backlights In SUVs

- 4.3.4 Slow Replacement Cycles In Mature Aftermarket Channels

- 4.4 Value-Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 OEM vs. Aftermarket Trend Analysis

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By Glass Type

- 5.1.1 Regular Glass

- 5.1.1.1 Laminated Glass

- 5.1.1.2 Tempered Glass

- 5.1.2 Smart Glass

- 5.1.2.1 Electrochromic

- 5.1.2.2 Suspended Particle Device (SPD)

- 5.1.2.3 Polymer Dispersed Liquid Crystal (PDLC)

- 5.1.2.4 Thermochromic

- 5.1.1 Regular Glass

- 5.2 By Application

- 5.2.1 Windshield

- 5.2.2 Backlite (Rear Window)

- 5.2.3 Sidelite (Side Windows)

- 5.2.4 Sunroof

- 5.2.5 Rear-view & Side-view Mirrors

- 5.2.6 Other Glazing (Quarter & Vent)

- 5.3 By Vehicle Type

- 5.3.1 Passenger Cars

- 5.3.1.1 Hatchback

- 5.3.1.2 Sedan

- 5.3.1.3 SUV & Crossover

- 5.3.1.4 Luxury & Sports

- 5.3.2 Light Commercial Vehicles

- 5.3.3 Medium and Heavy Commercial Vehicles

- 5.3.1 Passenger Cars

- 5.4 By Propulsion

- 5.4.1 Internal Combustion Engine (ICE)

- 5.4.2 Battery Electric Vehicle (BEV)

- 5.4.3 Hybrid Electric Vehicle (HEV/PHEV)

- 5.4.4 Fuel Cell Electric Vehicles (FCEV)

- 5.5 By Sales Channel

- 5.5.1 OEM

- 5.5.2 Aftermarket

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Spain

- 5.6.3.5 Italy

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 Australia

- 5.6.4.6 New Zealand

- 5.6.4.7 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 South Africa

- 5.6.5.4 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 AGC Inc. (Asahi Glass)

- 6.4.2 Saint-Gobain S.A.

- 6.4.3 Nippon Sheet Glass Co. Ltd.

- 6.4.4 Fuyao Glass Industry Group Co. Ltd.

- 6.4.5 Xinyi Glass Holdings Ltd.

- 6.4.6 Guardian Automotive (Koch Industries)

- 6.4.7 Webasto SE

- 6.4.8 Carlex Glass America LLC

- 6.4.9 Magna International Inc.

- 6.4.10 Vitro Automotive

- 6.4.11 Corning Incorporated

- 6.4.12 Sisecam Automotive

- 6.4.13 Shanghai Yaohua Pilkington Glass

- 6.4.14 Gentex Corporation

- 6.4.15 AGP Group

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

日本汽車玻璃市場報告(按玻璃類型、材料類型、車輛類型、技術、應用、最終用戶和地區分類,2026-2034)

日本汽車玻璃市場報告(按玻璃類型、材料類型、車輛類型、技術、應用、最終用戶和地區分類,2026-2034) 汽車用智慧玻璃的全球市場,各技術,各用途,控制機構,各車輛,各地區,機會,預測,2018年~2032年

汽車用智慧玻璃的全球市場,各技術,各用途,控制機構,各車輛,各地區,機會,預測,2018年~2032年 汽車玻璃/智慧玻璃(2025)

汽車玻璃/智慧玻璃(2025) 汽車玻璃蓋板 - 全球市場佔有率和排名、總銷售量和需求預測(2025-2031 年)

汽車玻璃蓋板 - 全球市場佔有率和排名、總銷售量和需求預測(2025-2031 年) 汽車全景擋風玻璃市場按分銷管道、車輛類型、產品類型和技術分類-全球預測,2025-2032年汽車玻璃市場依產品類型、玻璃類型、中階材料、車輛類型和安裝方式分類-2025-2032年全球預測汽車防眩光玻璃市場:依玻璃類型、應用、車輛類型、通路和眩光減少等級分類-2025-2032年全球預測

汽車全景擋風玻璃市場按分銷管道、車輛類型、產品類型和技術分類-全球預測,2025-2032年汽車玻璃市場依產品類型、玻璃類型、中階材料、車輛類型和安裝方式分類-2025-2032年全球預測汽車防眩光玻璃市場:依玻璃類型、應用、車輛類型、通路和眩光減少等級分類-2025-2032年全球預測 汽車用玻璃市場:產業趨勢·全球預測 (~2035年):產品類型·技術·用途·車輛類型·流通類型·企業規模·各主要地區全球汽車智慧玻璃市場按技術類型、材料類型、功能、安裝類型、應用、銷售管道和車輛類型分類 - 預測至 2025 年至 2030 年

汽車用玻璃市場:產業趨勢·全球預測 (~2035年):產品類型·技術·用途·車輛類型·流通類型·企業規模·各主要地區全球汽車智慧玻璃市場按技術類型、材料類型、功能、安裝類型、應用、銷售管道和車輛類型分類 - 預測至 2025 年至 2030 年 2025-2029年全球汽車玻璃市場

2025-2029年全球汽車玻璃市場