|

市場調查報告書

商品編碼

1844550

食品低溫運輸:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)Food Cold Chain - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

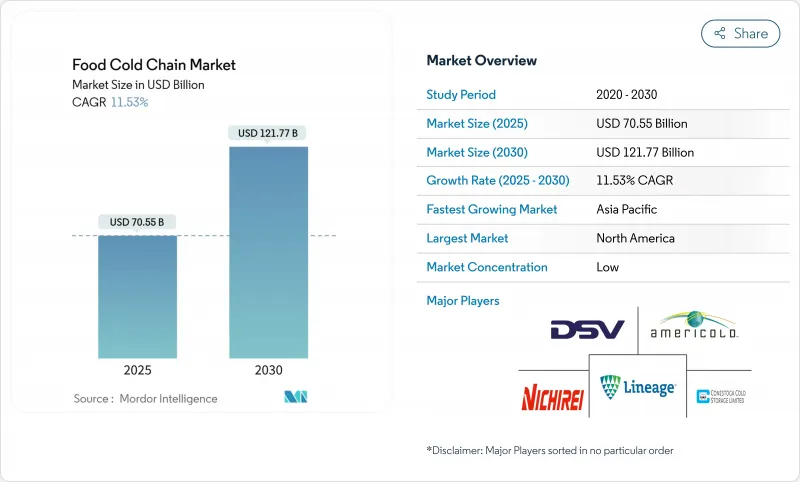

預計 2025 年全球食品低溫運輸市場規模將達到 705.5 億美元,到 2030 年將擴大至 1,217.7 億美元,預測期內複合年成長率將達到 11.53%。

這項加速反映了嚴格的食品安全法規、溫度監控技術的突破以及已烹調簡便食品,這些都要求從農場到餐桌的低溫運輸完整性毫不妥協。消費者食品安全意識的不斷增強、生鮮產品國際貿易的不斷成長以及新興經濟體有組織的零售業的快速發展進一步推動了市場擴張。 FDA 的食品安全現代化法案 (FSMA) 204 要求在 2026 年 1 月對食品可追溯性清單上列出的食品進行全面追溯,促使企業大力投資數位監控基礎設施。該法規尤其影響生鮮食品、乳製品和魚貝類等高風險食品,並要求公司在整個供應鏈中保存關鍵追蹤事件的記錄。這些要求的實施正在推動整個食品低溫運輸產業採用先進的追蹤技術、物聯網感測器和區塊鏈解決方案。

全球食品低溫運輸市場趨勢與洞察

全球對冷凍和生鮮食品的需求不斷增加

冷凍食品消費的成長改變了全球低溫運輸容量需求,尤其對倉庫、運輸和配送網路產生了影響。這種成長對冷藏基礎設施的需求很高,以彌補供需缺口,導致對冷藏倉庫、溫控車輛和先進監控系統的大量投資。疫情期間消費行為的改變使冷凍食品從簡便食品變成了必需品,推動了包括已調理食品、蔬菜、肉類和魚貝類在內的各類購買量的增加,形成了需要永久性擴建基礎設施的長期需求模式。低溫運輸業者強調必須在整個供應鏈(從生產設施到配銷中心和零售店)保持一致的溫度控制。溫度變化會導致產品損失、危及食品安全、引發代價高昂的召回,並導致不合規。溫度控制的複雜性延伸到交付的最後一英里,需要專門的設備和精確的監控通訊協定來保持產品的完整性。

國際食品貿易和跨境食品運輸的成長

跨境食品運輸正演變成一個複雜的溫控物流組織。根據《加強現代商業流通體系建設規劃》,中國商務部計畫在 2027 年實現水果蔬菜低溫運輸配送率達到 25%,肉類低溫運輸配送率達到 45%。這項監管措施反映了國際貿易在糧食安全中的重要作用,尤其是在氣候變遷和地緣政治緊張局勢擾亂傳統供應鏈的背景下。在多個司法管轄區保持溫度完整性的複雜性為專業物流供應商創造了機會,他們可以在確保產品品質的同時滿足各種監管要求。區塊鏈技術和物聯網感測器的整合對於提供進口國所要求的端到端可追溯性至關重要,將跨境食品貿易從物流挑戰轉變為物流支援的競爭優勢。溫控貨櫃運輸已成為關鍵瓶頸,專用冷藏貨櫃因其先進的監控系統而擁有更高的運費。

冷藏設施和冷藏運輸車輛的初始資本投資要求高

低溫運輸基礎設施的資本密集度構成了巨大的進入壁壘,專業的建築材料和節能設計導致成本比傳統倉庫高出300-400%。建造冷藏設施需要先進的隔熱系統、專用地板材料以及必須在極端溫度條件下可靠運行的先進製冷設備,不僅推高了初始投資,還增加了持續的維護成本。冷藏運輸車隊也面臨類似的成本壓力,冷藏卡車和拖車的運費需要兩位數的成長才能證明設施擴建的合理性。低溫運輸資產的專業性加劇了資金籌措挑戰,其替代用途有限,並且需要專業的維護專業知識。

細分分析

到2024年,低溫運輸倉儲將佔據最大的市場佔有率,達到55.66%,這反映了所有食品類別對溫控物流基礎設施的需求。此細分市場的主導地位源自於冷藏倉庫的資本密集特性,其中配備先進隔熱材料、自動化貨架系統和節能冷卻技術的專用設施構成了低溫運輸生態系統中最大的成本組成部分。

儘管絕對市佔率較小,但監控組件將呈現最快的成長軌跡,到2030年,其複合年成長率將達到14.45%,這得益於FSMA 204等監管要求以及曲折點:被動溫度記錄正被即時預測分析系統所取代,這些系統可以預測設備故障並最佳化能耗。像Rivercity Innovations這樣的公司已經推出了物聯網自動化溫度監控解決方案,該解決方案具有早期災難性故障檢測(ECFD)功能,可以預測壓縮機故障,從而實現及時維護並防止代價高昂的產品損失。

冷藏溫度範圍 (0-4°C) 將在 2024 年保持市場領先地位,市場佔有率達 60.15%,這反映出其在生鮮食品、乳製品和已調理食品,而這些領域佔據了生鮮食品消費的大部分。然而,受消費者對冷凍簡便食品偏好的轉變以及全球冷凍食品生產能力的擴張推動,冷凍食品 (-18°C) 將呈現更強勁的成長勢頭,到 2030 年複合年成長率將達到 15.49%。

冷凍食品產業的成長軌跡正推動大型零售商投資雙溫區設施,以便在同一營運過程中高效管理冷藏和冷凍食品,從而最佳化空間利用率並降低營運複雜性。 「降溫至-15°C」聯盟由阿拉伯聯合大公國航空貨運部等領先物流供應商支持,是一項全行業共同努力,旨在透過將標準溫度從-18°C調整至-15°C來最佳化冷凍食品運輸,從而在保持產品品質的同時降低消費量。該舉措展示瞭如何透過最佳化溫度範圍來降低營運成本和環境影響,同時保持食品安全標準,從而創造競爭優勢。

區域分析

北美2024年的市佔率為40.46%,這反映了數十年來基礎設施投資和監管發展,打造了全球最成熟的低溫運輸生態系統之一。大型零售商正積極響應,對自動化設施進行策略性投資,沃爾瑪和克羅格正在開發都市區冷藏倉庫,以縮短運輸距離並提高永續性指標。亞太地區受益於成熟的法律規範和消費者願意為品質保證支付溢價的意願,但也面臨基礎設施老化和需要大量資本投資才能滿足現代營運要求的阻力。

預計到 2030 年,亞太低溫運輸市場將以 16.56% 的複合年成長率成長,位居全球首位。這一市場擴張主要得益於政府旨在減少食物廢棄物和簡化供應鏈的支持性政策。中國、印度和印尼等國家的快速都市化推動了對溫控儲存和運輸服務的需求。在印度,截至 2025 年 2 月,Pradhan Mantri Kisan Sampada Yojana 已核准394 個低溫運輸計劃。這些計劃專注於建立綜合低溫運輸設施,包括冷藏運輸、冷藏和加工中心。該計劃透過更好地保存生鮮產品、減少收穫後損失和確保食品安全標準,支持了印度不斷擴大的食品加工產業。該舉措還鼓勵私人投資低溫運輸基礎設施建設,創造更強大、更有效率的食品分銷系統。

歐洲維持了穩定的成長,這得益於嚴格的食品安全法規、跨境貿易便利化以及重塑整個歐洲大陸低溫運輸營運的永續發展舉措。該地區對永續性的重視正在加速排放氣體冷藏拖車和先進數位化技術的採用,例如用於即時數據管理的數位孿生系統,可最佳化能源消耗和營運效率。該地區成熟的法規環境以及消費者偏好新鮮本地食品的永續性,並持續推動對先進低溫運輸解決方案的需求,這些解決方案能夠在保持產品品質的同時最大限度地減少環境影響。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場狀況

- 市場概況

- 市場促進因素

- 全球對冷凍和生鮮食品的需求不斷成長

- 國際食品貿易和跨境食品運輸的成長

- 消費者對新鮮、即食的簡便食品的偏好日益成長

- 有組織的零售和餐飲業的擴張

- 冷凍和溫度監測系統的技術進步

- 執行嚴格的食品安全法規和品質標準

- 市場限制

- 冷藏設施和冷藏運輸車輛的初始投資要求高

- 新興市場的電力供應不穩定

- 運輸和儲存過程中的溫度控制挑戰

- 與其他儲存方法的衝突

- 供應鏈分析

- 監管狀況

- 技術展望

- 五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第5章市場規模及成長預測

- 按類型

- 低溫運輸倉儲

- 低溫運輸運輸

- 監控組件

- 按溫度範圍

- 冷藏(0-4 度C)

- 冷凍(-18 度C)

- 深度冷凍/超低溫(-40 度C以下)

- 按運輸方式

- 公路 - 冷藏卡車和拖車

- 海運 - 冷藏貨櫃

- 鐵路 - 冷藏鐵路車輛

- 空運

- 按用途

- 水果和蔬菜

- 肉類和魚貝類

- 乳製品和冷凍甜點

- 烘焙和糖果甜點

- 已調理食品

- 其他用途

- 依技術

- RFID和即時監控

- 支援物聯網的遠端資訊處理

- 自動儲存和搜尋系統

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 北美其他地區

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 西班牙

- 荷蘭

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 其他亞太地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東和非洲地區

- 北美洲

第6章 競爭態勢

- 市場集中度

- 策略舉措

- 市場排名分析

- 公司簡介

- Lineage, Inc.

- Americold Logistics, Inc.

- Nichirei Corporation

- DSV A/S

- Conestoga Cold Storage Limited

- STEF

- RLS Logistics

- NewCold Cooperatief UA

- Burris Logistics

- Congebec Logistics Inc.

- John Swire & Sons(HK)Limited

- Frialsa Frigorificos SA de CV

- XPO, Inc

- China COSCO Shipping Corporation Limited

- AP Moller-Marsk A/S

- Gateway Distriparks Limited

- SCGJWD Logistics Public Company Limited

- Florida Freezer LP

- DP World

- Raben Group

第7章 市場機會與未來展望

The global food cold chain market size reached USD 70.55 billion in 2025 and is projected to expand to USD 121.77 billion by 2030, representing a robust compound annual growth rate (CAGR) of 11.53% during the forecast period.

This acceleration reflects the convergence of stringent food safety regulations, technological disruptions in temperature monitoring, and the explosive growth of ready-to-eat convenience foods that demand uncompromised cold chain integrity from farm to fork. The market expansion is further supported by rising consumer awareness about food safety, growing international trade of perishable goods, and the rapid development of organized retail sectors across emerging economies. Regulatory momentum is reshaping market dynamics as the FDA's Food Safety Modernization Act (FSMA) 204 mandates comprehensive traceability for foods on the Food Traceability List by January 2026, compelling operators to invest heavily in digital monitoring infrastructure . This regulation specifically impacts high-risk foods such as fresh produce, dairy products, and seafood, requiring companies to maintain records of critical tracking events throughout the supply chain. The implementation of these requirements is driving the adoption of advanced tracking technologies, IoT sensors, and blockchain solutions across the food cold chain industry.

Global Food Cold Chain Market Trends and Insights

Rising Demand for Frozen and Perishable Food Products Globally

The increase in frozen food consumption has changed cold chain capacity requirements globally, with particular impact on warehousing, transportation, and distribution networks. This growth has created high demand for cold storage infrastructure to address supply-demand gaps, leading to significant investments in refrigerated warehouses, temperature-controlled vehicles, and advanced monitoring systems. Consumer behavior changes during the pandemic transformed frozen foods from convenience items to essential products, driving increased purchases across categories including ready meals, vegetables, meat, and seafood, thereby establishing long-term demand patterns that necessitate permanent infrastructure expansion. Cold chain operators emphasize that maintaining consistent temperature controls throughout the supply chain is essential, from production facilities through distribution centers to retail locations, as temperature variations can cause product losses, compromise food safety, trigger costly recalls, and result in regulatory non-compliance. The complexity of temperature management extends to last-mile delivery, where maintaining product integrity requires specialized equipment and precise monitoring protocols.

Growth in International Food Trade and Cross-Border Food Transportation

Cross-border food transportation has evolved into a sophisticated orchestration of temperature-controlled logistics, with China's Ministry of Commerce targeting 25% cold chain circulation rates for fruits and vegetables and 45% for meat by 2027 under its modern commercial circulation system enhancement plan . This regulatory push reflects the critical role of international trade in food security, particularly as climate change and geopolitical tensions disrupt traditional supply chains. The complexity of maintaining temperature integrity across multiple jurisdictions has created opportunities for specialized logistics providers who can navigate varying regulatory requirements while ensuring product quality. The integration of blockchain technology and IoT sensors has become essential for providing end-to-end traceability required by importing countries, transforming cross-border food trade from a logistics challenge into a technology-enabled competitive advantage. Temperature-controlled container shipping has emerged as a critical bottleneck, with specialized reefer containers commanding premium rates due to their sophisticated monitoring and control systems.

High Initial Capital Investment Requirements for Cold Storage Facilities and Refrigerated Transport Vehicles

The capital intensity of cold chain infrastructure creates significant barriers to entry, with specialized construction materials and energy-efficient designs commanding premium costs that can exceed conventional warehousing by 300-400%. The construction of cold facilities requires sophisticated insulation systems, specialized flooring, and advanced refrigeration equipment that must operate reliably in extreme temperature conditions, driving up both initial investment and ongoing maintenance costs. Refrigerated transport vehicles face similar cost pressures, with reefer trucks and trailers requiring double-digit rate increases to justify equipment expansion. The financing challenge is compounded by the specialized nature of cold chain assets, which have limited alternative uses and require specialized maintenance expertise.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Consumer Preference for Fresh and Ready-to-Eat Convenience Foods

- Expansion of Organized Retail and Food Service Sectors

- Competition from Alternative Preservation Methods

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cold-chain storage commands the largest market share at 55.66% in 2024, reflecting the fundamental infrastructure requirements for temperature-controlled logistics across all food categories. The segment's dominance stems from the capital-intensive nature of refrigerated warehousing, where specialized facilities with advanced insulation, automated racking systems, and energy-efficient cooling technologies represent the largest cost component in the cold chain ecosystem.

Monitoring components, despite representing a smaller absolute market share, exhibit the fastest growth trajectory at 14.45% CAGR through 2030, driven by regulatory mandates such as FSMA 204 and the increasing sophistication of IoT-enabled temperature tracking systems. The monitoring components segment's rapid expansion reflects a technological inflection point where passive temperature logging is being replaced by real-time, predictive analytics systems that can anticipate equipment failures and optimize energy consumption. Companies like Rivercity Innovations have introduced IoT automated temperature monitoring solutions featuring Early Catastrophic Failure Detection (ECFD) capabilities that predict compressor failures, allowing for timely maintenance and preventing costly product losses.

The chilled temperature range (0-4°C) maintains market leadership with a 60.15% share in 2024, reflecting the broad applicability of this temperature zone across fresh produce, dairy products, and prepared foods that constitute the majority of perishable food consumption. However, the frozen segment (-18°C) demonstrates superior growth momentum with a 15.49% CAGR through 2030, driven by changing consumer preferences toward frozen convenience foods and the expansion of frozen food manufacturing capacity globally.

The frozen segment's growth trajectory has prompted major retailers to invest in dual-temperature facilities that can efficiently manage both chilled and frozen products within the same operation, optimizing space utilization and reducing operational complexity. The Move to -15°C coalition, supported by Emirates SkyCargo and other major logistics providers, represents an industry-wide effort to optimize frozen food transportation by adjusting standard temperatures from -18°C to -15°C, potentially reducing energy consumption while maintaining product quality. This initiative demonstrates how temperature range optimization can create competitive advantages through reduced operational costs and environmental impact, while maintaining food safety standards.

The Food Cold Chain Market Report Segments the Industry Into Type (Cold-Chain Storage, and More), Temperature Range (Chilled (0-4 °C), and More), Transport Mode (Road - Reefer Trucks and Trailers, Sea - Reefer Containers, and More), Application (Fruits and Vegetables, Meat and Seafood, and More), Technology (RFID and Real-Time Monitoring, and More) and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America's 40.46% market share in 2024 reflects decades of infrastructure investment and regulatory development that created the world's most sophisticated cold chain ecosystem, yet the region now confronts modernization challenges as legacy facilities struggle with e-commerce demands and sustainability requirements. Major retailers are responding with strategic investments in automated facilities, exemplified by Walmart and Kroger's development of urban-centric cold storage facilities that reduce transportation distances and improve sustainability metrics. The region benefits from established regulatory frameworks and consumer willingness to pay premium prices for quality assurance, yet faces headwinds from aging infrastructure and the need for substantial capital investment to meet modern operational requirements.

The Asia-Pacific cold chain market is projected to grow at a CAGR of 16.56% through 2030, representing the highest growth rate globally. This expansion is primarily driven by supportive government policies aimed at reducing food waste and improving supply chain efficiency. The rapid urbanization across countries like China, India, and Indonesia has increased demand for temperature-controlled storage and transportation services. In India, the Pradhan Mantri Kisan Sampada Yojana has approved 394 cold chain projects as of February 2025. These projects focus on establishing integrated cold chain facilities, including refrigerated transportation, cold storage units, and processing centers. The initiative supports India's expanding food processing industry by enabling better preservation of perishable goods, reducing post-harvest losses, and ensuring food safety standards. The program also promotes private sector investment in cold chain infrastructure development, creating a more robust and efficient food distribution system.

Europe maintains steady growth supported by stringent food safety regulations, cross-border trade facilitation, and sustainability initiatives that are reshaping cold chain operations across the continent. The region's focus on sustainability has accelerated the adoption of emission-free refrigerated trailers and advanced digitalization technologies, including digital twin systems for real-time data management that optimize energy consumption and operational efficiency. The region's mature regulatory environment and consumer preferences for fresh, locally sourced foods continue to drive demand for sophisticated cold chain solutions that can maintain product quality while minimizing environmental impact.

- Lineage, Inc.

- Americold Logistics, Inc.

- Nichirei Corporation

- DSV A/S

- Conestoga Cold Storage Limited

- STEF

- RLS Logistics

- NewCold Cooperatief UA

- Burris Logistics

- Congebec Logistics Inc.

- John Swire & Sons (H.K.) Limited

- Frialsa Frigorificos S.A. de C.V.

- XPO, Inc

- China COSCO Shipping Corporation Limited

- A.P. Moller - Marsk A/S

- Gateway Distriparks Limited

- SCGJWD Logistics Public Company Limited

- Florida Freezer LP

- DP World

- Raben Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for frozen and perishable food products globally

- 4.2.2 Growth in international food trade and cross-border food transportation

- 4.2.3 Increasing consumer preference for fresh and ready-to-eat convenience foods

- 4.2.4 Expansion of organized retail and food service sectors

- 4.2.5 Technological advancements in refrigeration and temperature monitoring systems

- 4.2.6 Implementation of strict food safety regulations and quality standards

- 4.3 Market Restraints

- 4.3.1 High initial capital investment requirements for cold storage facilities and refrigerated transport vehicles

- 4.3.2 Power-supply volatility in emerging markets

- 4.3.3 Temperature control challenges during transportation and storage transitions

- 4.3.4 Competition from alternative preservation methods

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Cold-chain Storage

- 5.1.2 Cold-chain Transport

- 5.1.3 Monitoring Components

- 5.2 By Temperature Range

- 5.2.1 Chilled (0-4 °C)

- 5.2.2 Frozen (-18 °C)

- 5.2.3 Deep-Frozen/Ultra-low (<-40 °C)

- 5.3 By Transport Mode

- 5.3.1 Road - Reefer Trucks and Trailers

- 5.3.2 Sea - Reefer Containers

- 5.3.3 Rail - Refrigerated Railcars

- 5.3.4 Air Cargo

- 5.4 By Application

- 5.4.1 Fruits and Vegetables

- 5.4.2 Meat and Seafood

- 5.4.3 Dairy and Frozen Dessert

- 5.4.4 Bakery and Confectionery

- 5.4.5 Ready-to-Eat Meals

- 5.4.6 Other Applications

- 5.5 By Technology

- 5.5.1 RFID and Real-time Monitoring

- 5.5.2 IoT-Enabled Telematics

- 5.5.3 Automated Storage and Retrieval Systems

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.1.4 Rest of North America

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 Italy

- 5.6.2.4 France

- 5.6.2.5 Spain

- 5.6.2.6 Netherlands

- 5.6.2.7 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 South Africa

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 United Arab Emirates

- 5.6.5.4 Rest of Middle East and Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Ranking Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Lineage, Inc.

- 6.4.2 Americold Logistics, Inc.

- 6.4.3 Nichirei Corporation

- 6.4.4 DSV A/S

- 6.4.5 Conestoga Cold Storage Limited

- 6.4.6 STEF

- 6.4.7 RLS Logistics

- 6.4.8 NewCold Cooperatief UA

- 6.4.9 Burris Logistics

- 6.4.10 Congebec Logistics Inc.

- 6.4.11 John Swire & Sons (H.K.) Limited

- 6.4.12 Frialsa Frigorificos S.A. de C.V.

- 6.4.13 XPO, Inc

- 6.4.14 China COSCO Shipping Corporation Limited

- 6.4.15 A.P. Moller - Marsk A/S

- 6.4.16 Gateway Distriparks Limited

- 6.4.17 SCGJWD Logistics Public Company Limited

- 6.4.18 Florida Freezer LP

- 6.4.19 DP World

- 6.4.20 Raben Group

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

食品物流市場:依運輸方式、溫度控制、產品類型、服務類型及最終用戶分類-2026-2032年全球市場預測

食品物流市場:依運輸方式、溫度控制、產品類型、服務類型及最終用戶分類-2026-2032年全球市場預測 食品物流市場規模、佔有率、趨勢和預測:按運輸方式、產品類型、服務類型、細分市場和地區分類,2026-2034年

食品物流市場規模、佔有率、趨勢和預測:按運輸方式、產品類型、服務類型、細分市場和地區分類,2026-2034年 2026年全球食品低溫運輸市場報告2026年全球智慧食品物流市場報告全球食品冷藏物流服務市場(依運輸方式、附加價值服務、倉儲配送及運輸分類)預測(2026-2032年)食品冷藏和冷凍供應鏈物流市場:按倉儲、包裝和標籤、訂單履行和運輸分類,全球預測,2026-2032年日本食品物流市場規模、佔有率、趨勢及預測(依運輸方式、產品類型、服務類型、細分市場及地區分類),2026-2034年

2026年全球食品低溫運輸市場報告2026年全球智慧食品物流市場報告全球食品冷藏物流服務市場(依運輸方式、附加價值服務、倉儲配送及運輸分類)預測(2026-2032年)食品冷藏和冷凍供應鏈物流市場:按倉儲、包裝和標籤、訂單履行和運輸分類,全球預測,2026-2032年日本食品物流市場規模、佔有率、趨勢及預測(依運輸方式、產品類型、服務類型、細分市場及地區分類),2026-2034年 食品物流市場規模、佔有率及成長分析(依運輸方式、服務、產品、倉儲設施及地區分類)-2026-2033年產業預測

食品物流市場規模、佔有率及成長分析(依運輸方式、服務、產品、倉儲設施及地區分類)-2026-2033年產業預測 食品低溫運輸市場規模、佔有率和趨勢分析報告:按類型、建設類型、應用、地區和細分市場預測,2025-2033 年

食品低溫運輸市場規模、佔有率和趨勢分析報告:按類型、建設類型、應用、地區和細分市場預測,2025-2033 年 食品冷鏈物流市場-全球產業規模、佔有率、趨勢、機會及預測(依產品類型、應用、建築類型、地區及競爭情況分類,2020-2030 年)

食品冷鏈物流市場-全球產業規模、佔有率、趨勢、機會及預測(依產品類型、應用、建築類型、地區及競爭情況分類,2020-2030 年)