|

市場調查報告書

商品編碼

1844508

慣性測量單元:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)Inertial Measurement Unit - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

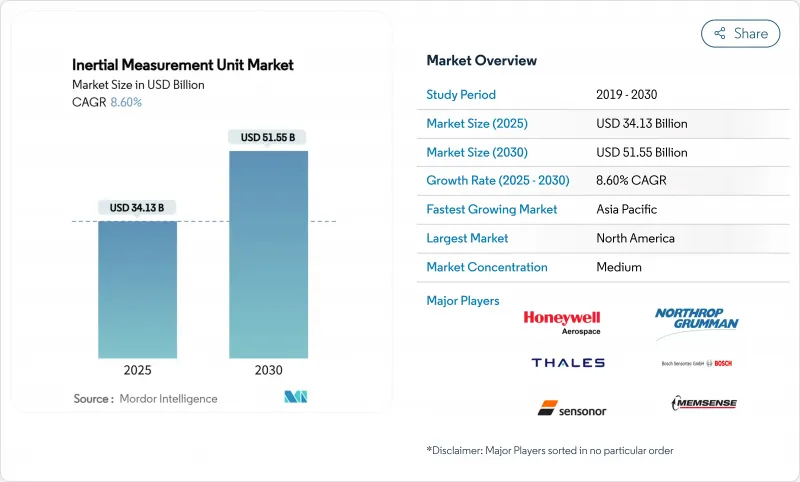

慣性測量單元市場規模預計在 2025 年達到 341.3 億美元,到 2030 年將達到 515.5 億美元,複合年成長率為 8.60%。

混合量子 MEMS 感測器融合推動了需求的成長,它正在重塑飛機、航太和自主平台的精確導航。波音公司 2024 年的量子 IMU 飛行測試透過將無輔助 GPS 導航誤差從數十公里減少到數十公尺證明了這一轉變。地緣政治風險的上升、無人系統的擴散以及量子光電的成熟都加強了慣性測量單元市場的近期成長前景。消費者的吸引力同樣強勁。 2025 年第一季,中國智慧眼鏡出貨量為 494,000 副,年增 116.1%,顯示對平衡精度和電池壽命的經濟型 6 軸感測器的需求達到創紀錄水準。航運、採礦和液化天然氣營運商正在添加戰術級 MEMS IMU,以滿足亞度動態定位公差,從而拓寬了慣性測量單元市場的潛在市場基礎。

全球慣性測量單元市場趨勢與洞察

中東無人機入侵加速反無人機平台部署

在中東部分地區,低成本無人機的表現優於傳統防空系統。北歐防空公司的克魯格 100 攔截飛彈依靠簡化的純慣性測量單元 (IMU) 飛行電腦,速度可達 270 公里/小時,並降低了集群作戰的單位成本。美國選擇了 Epirus 微波系統,該系統將靈活的慣性測量單元 (IMU) 與可停用無人機電子設備的軟體定義發送器相結合。這些措施標誌著採購方向轉向模組化、以軟體為中心的武器,這些武器以慣性核心為核心,而非昂貴的雷達或光學導引。隨著軍隊向大規模反無人機系統 (CMAS) 理論過渡,提供可擴展 IMU 模組和開放 API 的供應商將從中受益。

歐洲液化天然氣油輪擴大採用 MEMS 戰術級 IMU 實現動態定位

歐洲液化天然氣運輸商面臨嚴峻的港口排隊和大西洋的猛烈海浪。 Bourbon 的船舶現已配備基於光纖陀螺儀的 Exail Octans AHRS,以便在起重機操作期間保持橫搖、縱搖和升沈的對準。 MEMS 設計也在船舶改裝應用中取代了環形雷射陀螺儀,以亞度級的精度和一半的購買價格。 Advanced Navigation 的 Hydrus AUV 將海底勘測成本降低了 75%,並消除了團隊潛水任務的需求。這些成本的節省正在推動整個船隊的感測器升級,並擴大商用船舶慣性測量單元的市場。

不到 7 年的設計週期限制了民航機供應商的轉換

認證風險迫使飛機製造商採取保守做法。波音公司對其量子慣性測量單元 (IMU) 進行了四小時的飛行測試,但必須完成數年的認證才能將其用於Line-Fit。Honeywell在火星探勘上飛行的小型IMU凸顯了航太買家更青睞經過驗證、能夠持續數十年可靠性的設計。漫長的檢驗時間會鎖定現有供應商,並減緩單位成本的下降,這限制了商用航空慣性測量單元 (IMU) 市場的成長率。

細分分析

到2024年,陀螺儀將佔慣性測量單元市場收入的40%,並將繼續成為實現死點追蹤精度的基礎。磁力計雖然絕對值較小,但隨著擴增實境開發者將數位羅盤整合到所有頭戴裝置中,其複合年成長率高達10.9%。加速計在振動和ADAS領域保持穩定的市場規模。慣性測量單元市場目前傾向於單封裝感測器融合。意法半導體的LSM6DSV16X增加了一個用於手勢識別的機器學習核心,同時降低了待機功耗並延長了電池壽命。儘管面臨商品化壓力,提供片上分析功能的組件供應商仍可獲得溢價。

加速計正在將陀螺儀、加速計和磁力計資料整合到安全隔離區微控制器中。整合時序消除了感測器之間的延遲,增強了系統抵禦偽造訊號的能力。隨著設計團隊採用這些模組,物料清單 (BOM) 的簡潔性(而非物料成本)正成為主要的選擇因素。儘管出貨量不斷成長,但這種轉變仍支持慣性測量單元市場價格的穩定性。

在智慧型手機和自動駕駛ADAS規模的推動下,商用級設備將在2024年佔據慣性測量單元市場的35%。航太級設備的出貨量雖然規模較小,但預計在低地球軌道(LEO)衛星群的普及推動下,複合年成長率將達到12.4%。諾斯羅普·格魯曼公司的LR-450採用毫米級半球諧振陀螺儀,該陀螺儀已在軌運行超過7000萬小時,無故障運行時間比環形雷射器減少了一半,體積、重量和功率也減少了一半。其可靠性吸引了那些需要發射數百顆相同衛星的衛星群營運商。

隨著商用MEMS精度的提升,等級界限正在變得模糊。汽車零件製造商如今要求戰術級零偏穩定性,而無人機製造商則採購航太級零件以增強輻射抗擾度。擁有靈活生產線、能夠從商用擴展到國防應用的供應商在經濟低迷時期更具韌性,並在慣性測量單元市場中佔據更大的佔有率。

區域分析

2024年,北美佔據慣性測量單元市場收益的38%。美國國防預算資助海軍研究實驗室的量子乾涉測量研究,以延長無漂移導航的運行時間。波音公司的量子IMU飛行檢驗了民航機的使用案例,使本土原始設備製造商能夠超越歐洲競爭對手。 2024年的出口管制改革放寬了對澳洲、加拿大和英國的轉讓,使北美供應商能夠優先參與盟軍的航太計畫。

到2030年,亞太地區的複合年成長率將達到11.8%,位居榜首。在國內補貼的推動下,中國智慧玻璃製造商每季訂購數千萬個六軸MEMS感測器。澳洲的偏遠礦場成為光子慣性測量單元(IMU)的運作平台,鼓勵當地大學衍生出導航新創公司。印度、日本和韓國的新型太空船發射新興企業正在尋求不受《國際武器貿易條例》(ITAR)約束的航太零件,培育本土供應鏈,以在成本敏感型任務領域挑戰美國現有企業。

歐洲在海事、能源和高精度衛星有效載荷領域佔據戰略優勢。歐空局的GENESIS衛星使用冷原子慣性測量單元(IMU)進行厘米級海面監測。 Exile公司贏得了「波旁號」(Bourbon)船舶的光纖陀螺儀動態定位升級契約,體現了該地區在惡劣水域感測器封裝方面的專業技術。Honeywell於2024年斥資2億歐元收購Civitanavi,增強了其歐洲生產基地,確保其飛機項目在跨大西洋貿易緊張局勢下的連續性。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場狀況

- 市場概況

- 市場促進因素

- 中東無人機墜毀事件加速反無人機系統平台部署

- 歐洲液化天然氣運輸船擴大採用基於 MEMS 的戰術級 IMU 進行動態定位

- 將冷原子IMU整合到ESA衛星星系中

- 擴展澳洲自動採礦車輛的光子 IMU

- 美國第二代戰鬥機改裝需求激增

- 亞洲XR耳機競爭推動家用電子電器產品IMU訂單激增

- 市場限制

- 七年以上的設計週期限制了民航機供應商的更換

- 《國際武器貿易條例》限制美國向亞太地區新興航太企業出口航太級慣性測量單元

- 在遠距海上航線上,MEMS 陣列的累積偏壓漂移超過每小時 +-0.3°

- 耐輻射 ASIC 短缺導致 LEO 衛星 IMU 的 BOM 成本上升

- 價值/供應鏈分析

- 監管和技術展望

- 技術簡介 - MEMS、FOG、RLG、HRG、冷原子、光子學

- 標準化藍圖(SAE、RTCA/DO-334、NATO STANAG 4671)

- 五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

- 投資與資金籌措分析

第5章市場規模及成長預測

- 按組件

- 陀螺儀

- 加速計

- 磁力儀

- 按年級

- 海洋級

- 導航等級

- 戰術級

- 太空級

- 商業級

- 依技術

- MEMS

- 光纖陀螺儀(FOG)

- 環形雷射陀螺儀(RLG)

- 半球諧振陀螺儀(HRG)

- 機械陀螺儀

- 按最終用戶

- 航太/國防

- 汽車(ADAS 和自動駕駛)

- 工業自動化與機器人

- 消費性電子產品和XR

- 海洋/近海

- 能源(石油和天然氣、風力發電機)

- 地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 其他亞太地區

- 中東

- 以色列

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 埃及

- 其他非洲國家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 北美洲

第6章 競爭態勢

- 市場集中度

- 策略舉措

- 市佔率分析

- 公司簡介

- Honeywell International Inc.

- Northrop Grumman Corp.

- Bosch Sensortec GmbH

- Analog Devices Inc.

- Safran Sensing Technologies

- Thales Group

- STMicroelectronics NV

- ACEINNA Inc.

- Sensonor AS

- Silicon Sensing Systems Ltd.

- KVH Industries Inc.

- Xsens Technologies BV

- VectorNav Technologies LLC

- SBG Systems SAS

- Gladiator Technologies

- Trimble Inc.

- Moog Inc.

- EMCORE Corp.

- TDK-InvenSense

- Murata Manufacturing Co. Ltd.

- Continental AG

- Raytheon Technologies Corp.

第7章 市場機會與未來展望

The inertial measurement unit market size stood at USD 34.13 billion in 2025 and is forecast to reach USD 51.55 billion by 2030, reflecting an 8.60% CAGR.

Demand gains stem from hybrid quantum-MEMS sensor fusion, which is reshaping precision navigation for defines, aerospace, and autonomous platforms. Boeing validated this shift when its 2024 flight test of a quantum IMU cut unaided-GPS navigation error from tens of kilometres to tens of meters. Escalating geopolitical risk, the spread of unmanned systems, and the maturity of quantum photonics all reinforce the near-term growth outlook for the inertial measurement unit market. Consumer pull is equally strong. China shipped 494,000 smart-glass units in Q1 2025, up 116.1% year over year, signalling record demand for low-cost six-axis sensors that balance accuracy and battery life. Maritime, mining, and LNG operators are adding tactical-grade MEMS IMUs to meet sub-degree dynamic-positioning tolerances, widening the addressable base for the inertial measurement unit market.

Global Inertial Measurement Unit Market Trends and Insights

Accelerated deployment of counter-UAS platforms amid Middle East drone incursions

Low-cost drones now outnumber legacy air defenses across several Middle East theatres. Nordic Air Defence's Kreuger 100 interceptor relies on a simplified IMU-only flight computer, reaches 270 km/h, and cuts unit costs for swarm engagements. The U.S. Marine Corps selected Epirus microwave systems that couple agile IMUs with software-defined emitters to disable drone electronics. These moves signal a procurement pivot toward modular, software-centric weapons built around inertial cores rather than expensive radar or optical guidance. Suppliers that offer scalable IMU modules and open APIs stand to gain as militaries transition to volume-deployment counter-UAS doctrine.

Rising adoption of MEMS tactical-grade IMUs in European LNG tankers for dynamic positioning

European LNG shippers face tighter port queues and harsher Atlantic swells. Bourbon vessels now carry Exail Octans AHRS, based on fiber-optic gyros, to maintain roll, pitch, and heave integrity during crane operations. MEMS designs are also displacing ring-laser gyros on retrofit jobs because they slash purchase price by half while meeting sub-degree accuracy. Advanced Navigation's Hydrus AUV lowered subsea survey costs 75% and removed the need for team-based diving missions. Such savings encourage fleet-wide sensor upgrades, expanding the inertial measurement unit market across commercial shipping.

Design-in cycles less than 7 years limiting supplier switch-over in commercial aircraft

Certification risk makes air-framers conservative. Boeing flight-tested quantum IMUs for four hours but must still complete multi-year qualification before line-fit adoption. Honeywell's miniature IMU that flew on Mars probes underscores how aerospace buyers favour proven designs that demonstrate multi-decade reliability. Lengthy validation locks in incumbent vendors and slows unit-price erosion, tempering the inertial measurement unit market growth rate in commercial aviation.

Other drivers and restraints analyzed in the detailed report include:

- Integration of cold-atom IMUs in ESA small-satellite constellations

- Expansion of photonic IMUs for autonomous mining vehicles in Australia

- ITAR restrictions curtailing U.S. space-grade IMU exports to APAC new-space players

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Gyroscopes contributed 40% of inertial measurement unit market revenue in 2024 and remain foundational for dead-reckoning accuracy. Magnetometers, though smaller in absolute value, compound at 10.9% CAGR as augmented-reality developers embed digital compasses inside every headset. Accelerometers maintain consistent volume in vibration and ADAS roles. The inertial measurement unit market now leans toward single-package sensor fusion. STMicroelectronics' LSM6DSV16X adds a machine-learning core that recognizes gestures while lowering standby power to extend battery life. Component vendors that offer on-chip analytics can charge premiums despite commoditization pressure.

Emerging packages combine gyro, accelerometer, and magnetometer data inside secure enclave micro-controllers. Integrated timing eliminates inter-sensor latency and hardens systems against spoof signals. As design teams adopt these modules, bill-of-materials simplicity overtakes raw component cost as the main selection factor. That transition supports steady pricing in the inertial measurement unit market despite rising shipment volumes.

Commercial-grade devices captured 35% of inertial measurement unit market size in 2024 thanks to smartphone and auto-ADAS scale. Space-grade shipments, though smaller, are projected to climb 12.4% CAGR on the back of proliferated low-Earth-orbit (LEO) constellations. Northrop Grumman's LR-450 uses milli-HRG gyros that log more than 70 million fault-free hours in orbit while halving size, weight, and power over ring-laser counterparts. That reliability attracts constellation operators who must launch hundreds of identical satellites.

Grade boundaries blur as commercial MEMS precision improves. Automotive suppliers now request tactical-grade bias stability, while drone makers procure space-qualified parts for radiation robustness. Vendors that master flexible production lines able to pivot from consumer to defense volumes gain resilience during sector downturns, reinforcing their share within the inertial measurement unit market.

Inertial Measurement Unit Market Report is Segmented by Component (Gyroscopes, Accelerometers, and More), Grade (Marine, Navigation and More), Technology (MEMS, FOG, and More), End User (Aerospace & Defense, Automotive, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America commanded 38% of inertial measurement unit market revenue in 2024. U.S. defense budgets fund quantum interferometer research at the Naval Research Laboratory, extending navigation run-time without drift. Boeing's quantum-IMU flight validated commercial-aviation use cases and keeps local OEMs ahead of European rivals. Export-control reforms in 2024 eased transfers to Australia, Canada, and the United Kingdom, giving North American vendors privileged access to allied aerospace programs.

Asia-Pacific posts the strongest 11.8% CAGR through 2030. Chinese smart-glass makers, buoyed by domestic subsidies, order tens of millions of six-axis MEMS sensors each quarter. Australia's remote mines serve as live testbeds for photonic IMU trucks, encouraging regional universities to spin out navigation start-ups. New-space launch firms across India, Japan, and South Korea seek ITAR-free space-grade parts, fostering indigenous supply chains that challenge U.S. incumbents in cost-sensitive missions.

Europe retains strategic niches in marine, energy, and high-precision satellite payloads. The ESA GENESIS satellite will use cold-atom IMUs to underpin centimeter-level sea-level monitoring. Exail won Bourbon vessel contracts for fiber-optic gyro dynamic-positioning upgrades, reflecting regional expertise in harsh-sea sensor packaging. Honeywell's EUR 200 million purchase of Civitanavi in 2024 gives the firm a deep European production base, ensuring continuity for aircraft programs even amid trans-Atlantic trade frictions.

- Honeywell International Inc.

- Northrop Grumman Corp.

- Bosch Sensortec GmbH

- Analog Devices Inc.

- Safran Sensing Technologies

- Thales Group

- STMicroelectronics N.V.

- ACEINNA Inc.

- Sensonor AS

- Silicon Sensing Systems Ltd.

- KVH Industries Inc.

- Xsens Technologies B.V.

- VectorNav Technologies LLC

- SBG Systems SAS

- Gladiator Technologies

- Trimble Inc.

- Moog Inc.

- EMCORE Corp.

- TDK-InvenSense

- Murata Manufacturing Co. Ltd.

- Continental AG

- Raytheon Technologies Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated Deployment of Counter-UAS Platforms amid Middle-East Drone Incursions

- 4.2.2 Rising Adoption of MEMS-based Tactical-Grade IMUs in European LNG Tankers for Dynamic Positioning

- 4.2.3 Integration of Cold-Atom IMUs in ESA Small-Satellite Constellations

- 4.2.4 Expansion of Photonic IMUs for Autonomous Mining Vehicles in Australia

- 4.2.5 Demand Spike for Retrofit Navigation Upgrades in U.S. Gen-II Fighter Fleet

- 4.2.6 High-volume Consumer-Electronics IMU Orders Driven by Asia's XR Headset Race

- 4.3 Market Restraints

- 4.3.1 Design-in Cycles >7 Years Limiting Supplier Switch-Over in Commercial Aircraft

- 4.3.2 ITAR Restrictions Curtailing U.S. Space-grade IMU Exports to APAC New-Space Players

- 4.3.3 Cumulative Bias Drift in MEMS Arrays Exceeding +-0.3°/hr for Long-haul Maritime Routes

- 4.3.4 Scarcity of Radiation-Hardened ASICs Raising BOM Costs in LEO Satellite IMUs

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory and Technological Outlook

- 4.5.1 Technology Snapshot - MEMS, FOG, RLG, HRG, Cold-Atom, Photonic

- 4.5.2 Standardization Roadmap (SAE, RTCA/DO-334, NATO STANAG 4671)

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Investment and Funding Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Gyroscopes

- 5.1.2 Accelerometers

- 5.1.3 Magnetometers

- 5.2 By Grade

- 5.2.1 Marine Grade

- 5.2.2 Navigation Grade

- 5.2.3 Tactical Grade

- 5.2.4 Space Grade

- 5.2.5 Commercial Grade

- 5.3 By Technology

- 5.3.1 MEMS

- 5.3.2 Fiber-Optic Gyro (FOG)

- 5.3.3 Ring-Laser Gyro (RLG)

- 5.3.4 Hemispherical Resonator Gyro (HRG)

- 5.3.5 Mechanical Gyro

- 5.4 By End User

- 5.4.1 Aerospace and Defense

- 5.4.2 Automotive (ADAS and Autonomous)

- 5.4.3 Industrial Automation and Robotics

- 5.4.4 Consumer Electronics and XR

- 5.4.5 Marine and Offshore

- 5.4.6 Energy (Oil and Gas, Wind Turbines)

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 Middle East

- 5.5.4.1 Israel

- 5.5.4.2 Saudi Arabia

- 5.5.4.3 United Arab Emirates

- 5.5.4.4 Turkey

- 5.5.4.5 Rest of Middle East

- 5.5.5 Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Egypt

- 5.5.5.3 Rest of Africa

- 5.5.6 South America

- 5.5.6.1 Brazil

- 5.5.6.2 Argentina

- 5.5.6.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Honeywell International Inc.

- 6.4.2 Northrop Grumman Corp.

- 6.4.3 Bosch Sensortec GmbH

- 6.4.4 Analog Devices Inc.

- 6.4.5 Safran Sensing Technologies

- 6.4.6 Thales Group

- 6.4.7 STMicroelectronics N.V.

- 6.4.8 ACEINNA Inc.

- 6.4.9 Sensonor AS

- 6.4.10 Silicon Sensing Systems Ltd.

- 6.4.11 KVH Industries Inc.

- 6.4.12 Xsens Technologies B.V.

- 6.4.13 VectorNav Technologies LLC

- 6.4.14 SBG Systems SAS

- 6.4.15 Gladiator Technologies

- 6.4.16 Trimble Inc.

- 6.4.17 Moog Inc.

- 6.4.18 EMCORE Corp.

- 6.4.19 TDK-InvenSense

- 6.4.20 Murata Manufacturing Co. Ltd.

- 6.4.21 Continental AG

- 6.4.22 Raytheon Technologies Corp.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

慣性測量單元市場報告:按組件、等級、技術、最終用途行業和地區分類(2026-2034 年)

慣性測量單元市場報告:按組件、等級、技術、最終用途行業和地區分類(2026-2034 年) 慣性測量單元 (IMU) 市場:按技術、組件、軸、銷售管道和應用分類-2026-2032 年全球市場預測

慣性測量單元 (IMU) 市場:按技術、組件、軸、銷售管道和應用分類-2026-2032 年全球市場預測 2026年全球火箭慣性測量單元市場報告2026年全球慣性測量單元市場報告

2026年全球火箭慣性測量單元市場報告2026年全球慣性測量單元市場報告 慣性測量單元 (IMU) 市場規模、佔有率和成長分析(按組件、等級、技術、應用和地區分類)—2026-2033 年行業預測

慣性測量單元 (IMU) 市場規模、佔有率和成長分析(按組件、等級、技術、應用和地區分類)—2026-2033 年行業預測 慣性測量單元市場,按等級、按組件、按平台、按技術、按最終用戶、按國家和地區 - 2025 年至 2032 年全球行業分析、市場規模、市場佔有率和預測

慣性測量單元市場,按等級、按組件、按平台、按技術、按最終用戶、按國家和地區 - 2025 年至 2032 年全球行業分析、市場規模、市場佔有率和預測 到 2030 年慣性測量裝置市場預測:按平台、等級、組件、技術、應用、最終用戶和地區進行的全球分析

到 2030 年慣性測量裝置市場預測:按平台、等級、組件、技術、應用、最終用戶和地區進行的全球分析 慣性測量單元市場規模、佔有率、趨勢分析報告:按組件、按技術、按應用、按地區、細分市場預測,2024-2030

慣性測量單元市場規模、佔有率、趨勢分析報告:按組件、按技術、按應用、按地區、細分市場預測,2024-2030