|

市場調查報告書

商品編碼

1844502

水性塗料:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)Waterborne Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

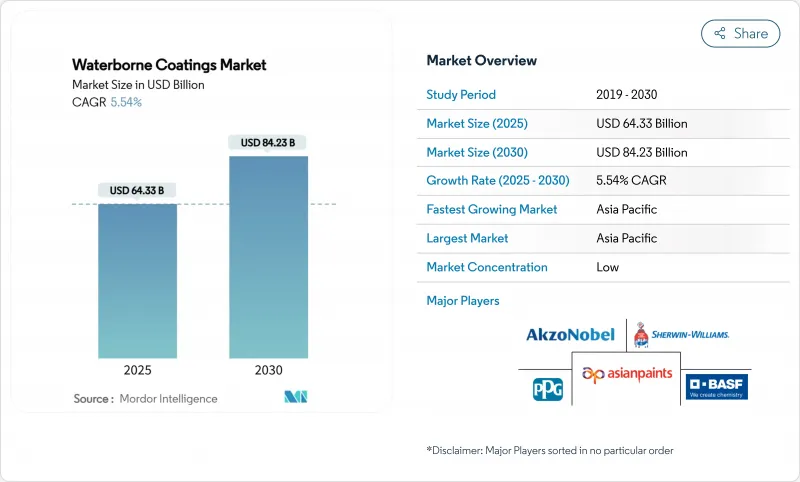

水性塗料市場規模預計在 2025 年為 643.3 億美元,預計到 2030 年將達到 842.3 億美元,預測期內(2025-2030 年)的複合年成長率為 5.54%。

揮發性有機化合物限量收緊、大規模基礎設施項目以及原始設備製造商加速轉向低排放氣體化學品支出,共同支撐了強勁的需求。美國環保署將氣溶膠塗料法規的合規期限延長至2027年1月,顯示生產者在轉向更環保的配方時,必須嚴格遵守監管規定。亞洲建築業的蓬勃發展、汽車修補漆的升級以及生物基樹脂的興起,進一步鞏固了水性塗料市場的長期發展軌跡。競爭策略擴大圍繞著流變學方案(以確保供應安全)、不含PFAS的耐久性增強以及數位色彩平台展開,儘管原料成本波動,但仍為價值獲取開闢了新的途徑。

全球水性塗料市場趨勢與洞察

加強VOC監管和脫碳

加州空氣資源委員會已將工業維護塗料中的 VOC 限制為 50g/L,比聯邦基準值嚴格近 10 倍,迫使配方師開發通過附著力、光澤度和耐久性測試的超低排放氣體配方。加拿大也在推行類似的監管收緊措施,該國將於 2024 年 1 月對 130 個產品類別實施全國性限制,這增加了全球統一 SKU 的跨國公司的合規風險。在歐洲,更新後的 REACH 監管藍圖針對 PVC 添加劑和鄰苯二甲酸酯,縮短了採用不含 PFAS 的多元醇的時間。隨著各國司法管轄區在雄心勃勃的脫碳目標上趨於一致,能夠在各大洲協調單一水性規範的公司可以降低合規開銷並加快市場進入速度,而後進企業則被困在分散的傳統生產線中。

亞洲和非洲基礎設施快速發展

中國經濟獎勵策略推動的工業復甦以及印度的高速公路和地鐵擴建,推動了水性塗料市場以升為單位的最大成長佔有率。在巴林和阿曼,超過45%的新住宅採用快乾、低氣味的水性底漆,隨著該地區承包商追求LEED和Estidama認證,這一比例預計還將成長。亞洲開發銀行的2024年關鍵指標強調,每年1.7兆美元的基礎設施支出必須兼顧氣候適應力,並將室內空氣污染物較低的水性化學品列為採購清單的首位。從印尼到肯亞,在會議上的對話表明,技術顧問擴大向醫院和學校推薦水性環氧樹脂,這證實了人們根深蒂固的偏好,並將支持長期需求成長。

特殊流變添加劑的稀少性和價格波動

流變包裝僅佔原料重量的4%,卻佔其成本的13%,供應緊張影響了整體生產利潤率。圍繞複雜ASE和HASE化合物的製造商整合加劇了價格波動。一次停產可能會使全球每噸成本增加兩位數。帶狀聚矽酸鹽承諾在低劑量下實現pH值穩定的流動,但需要進行大量的兼容性測試,從而將創新週期延長至一年以上。中間庫存緩衝是唯一的對沖手段,可以鎖定可用於資助新研發的資金。

細分分析

到2024年,丙烯酸配方將佔據水性塗料市場的81.20%,這反映了其抗紫外線、保色性和成本效益的優勢,這些優勢使其受到全球建築商和DIY消費者的青睞。在市政重塗計畫和DIY管道擴張的推動下,丙烯酸樹脂水性塗料的市場規模預計將穩定成長。

隨著汽車製造商和工業維修工程師轉向更小基體、單組分、水性化學品,以縮短噴塗時間並提高耐化學性,聚氨酯市場到2030年將以5.88%的複合年成長率加速成長。環氧樹脂在重防腐蝕應用仍佔有一席之地,但PFAS排放途徑需要同步創新才能維持阻隔指標。受VOC法規的擠壓,醇酸樹脂正透過生物基變體尋求緩解,這些變體用石油基來源的壬二酸替代,從而減少監管審查並保持熟悉的可加工性。

水性塗料報告按樹脂類型(丙烯酸、醇酸樹脂、環氧樹脂、聚氨酯、聚酯、聚偏二氯乙烯等)、終端用戶行業(建築施工、汽車、工業、木材、其他終端用戶行業)和地區(亞太地區、北美、歐洲、南美、中東和非洲)細分。市場預測以美元計算。

區域分析

預計到2024年,亞太地區將佔全球銷售額的42.61%,並預計以6.01%的複合年成長率引領市場,到2030年,亞太地區將牢牢確立其作為水性塗料市場成長引擎的地位。中國的經濟獎勵策略預計將重振工業生產,擴大對一般工業瓷漆的基準需求,而印度混凝土密集型智慧城市的建設預計將吸引彈性屋頂和橋樑防水膜的遠距訂單。

北美擁有成熟的監管體系和技術領先優勢。加州50克/公升的限值迫使全國範圍內的SKU(庫存單位)必須滿足最低VOC限值,從而刺激了分銷鏈上的快速再製造。加拿大的國家VOC規則手冊協調了從魁北克省到不列顛哥倫比亞省的各省限值,簡化了合規水性產品的市場准入流程。

歐洲正透過其「永續性化學品策略」引領永續性趨勢,加速水性塗料在建築、工業和DIY領域的應用。在英國,阿克蘇諾貝爾在BASF的支持下,重新推出了多樂士Easycare系列產品,並承諾將其產品的碳足跡減少至少5%,從而增強其在環保消費者中的品牌影響力。東歐的都市化也推動了塗料銷售的成長,尤其是在歐盟復甦計畫下市政道路和鐵路的維修。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場狀況

- 市場概況

- 市場促進因素

- 加強VOC和脫碳需求

- 亞洲和非洲基礎設施快速發展

- OEM溶劑到水的轉化

- 生物基樹脂(木質素、藻類等)的進展

- 智慧工廠對低溫固化生產線的需求

- 市場限制

- 特殊流變助劑的稀少性和價格波動

- 熱帶地區與濕度有關的乾旱災害

- 極端防腐蝕中不含 PFAS 的性能差距

- 價值鏈分析

- 五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章市場規模及成長預測

- 依樹脂類型

- 丙烯酸纖維

- 醇酸

- 環氧樹脂

- 聚氨酯

- 聚酯纖維

- 聚偏二氯乙烯(PVDC)

- 聚二氟亞乙烯(PVDF)

- 其他樹脂類型

- 按最終用戶產業

- 建築/施工

- 車

- 工業的

- 木頭

- 其他最終用戶產業

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 俄羅斯

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 埃及

- 其他中東和非洲地區

- 亞太地區

第6章 競爭態勢

- 市場集中度

- 策略舉措

- 市佔率分析

- 公司簡介

- Akzo Nobel NV

- Arkema

- Asian Paints Ltd.

- Axalta Coating Systems, LLC

- BASF

- Benjamin Moore & Co.

- Berger Paints India

- Chokwang Paint

- Dow

- Hempel A/S

- Jotun

- Kansai Paint Co., Ltd.

- KCC Corporation

- Masco Corporation

- Nippon Paint Holdings Co., Ltd.

- PPG Industries, Inc.

- RPM International Inc.

- Sika AG

- Teknos Group

- Tenaris

- The Sherwin-Williams Company

- Tikkurila

第7章 市場機會與未來展望

The Waterborne Coatings Market size is estimated at USD 64.33 billion in 2025, and is expected to reach USD 84.23 billion by 2030, at a CAGR of 5.54% during the forecast period (2025-2030).

Robust demand is anchored in tighter volatile-organic-compound caps, large-scale infrastructure programs, and accelerating OEM conversions that together steer spending toward low-emission chemistries. The Environmental Protection Agency's January 2027 compliance date extension under the National Aerosol Coatings Rule illustrates the regulatory tightrope producers must walk as they shift portfolios toward greener formulations. Asian construction booms, automotive refinishing upgrades, and bio-based resin breakthroughs further reinforce the long-term trajectory of the waterborne coatings market. Competitive strategies increasingly revolve around supply-secure rheology packages, PFAS-free durability improvements, and digital color platforms, creating fresh avenues for value capture despite raw-material cost volatility.

Global Waterborne Coatings Market Trends and Insights

Stricter VOC and Decarbonization Mandates

California's Air Resources Board restricts industrial-maintenance VOCs to 50 g/L, nearly a ten-fold tightening against federal thresholds, forcing formulators to engineer ultra-low emission blends that still pass adhesion, gloss, and durability tests. Similar tightening unfolds across Canada, where national limits on 130 product classes took effect in January 2024 and extend compliance risk for multinationals with globally harmonized SKUs. In Europe, the updated REACH Restrictions Roadmap targets PVC additives and ortho-phthalates, compressing the adoption window for PFAS-free polyols. As jurisdictions converge on ambitious decarbonization metrics, companies able to harmonize one waterborne specification across continents will lower compliance overhead and speed market entry, leaving laggards boxed into fragmented legacy lines.

Rapid Infrastructure Buildouts in Asia and Africa

China's stimulus-driven industrial revival and India's highway and metro expansions underpin the largest share of incremental liters for the waterborne coatings market. GCC construction pipelines add a climatic angle: quick-drying, low-odor waterborne primers now coat more than 45% of new residential stock in Bahrain and Oman, a share expected to widen as regional contractors chase LEED and Estidama credentials. The Asian Development Bank's 2024 Key Indicators emphasize that USD 1.7 trillion annual infrastructure spending must integrate climate resilience, thrusting waterborne chemistries with minimal indoor-air pollutants to the top of procurement lists. Conference dialogues from Indonesia to Kenya indicate that technical consultants increasingly recommend water-based epoxies for hospitals and schools, confirming an entrenched preference that raises the floor for long-run demand growth.

Scarcity and Price Volatility of Specialty Rheology Additives

Rheology packages, barely 4% by weight yet 13% of raw-material spend, swing overall production margins when supply tightens. Producer consolidation around complex ASE and HASE chemistries magnifies price shocks; a single outage can inflate global quarti-ton costs by double digits. Ribbon polysilicates promise pH-stable flow at lower dosages but need extensive compatibility trials, stretching innovation timelines to one year or more. Interim stock buffers remain the only hedge, locking capital that could fund new research and development.

Other drivers and restraints analyzed in the detailed report include:

- OEM One-Component Conversion from Solvent to Water Systems

- Bio-Based Resin Breakthroughs

- PFAS-Free Performance Gap for Extreme Anticorrosion

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Acrylic formulations anchored 81.20% of the waterborne coatings market in 2024, reflecting a time-tested blend of UV resistance, color retention, and cost efficiency that builders and DIY consumers favor worldwide. The waterborne coatings market size for acrylic resins is projected to expand steadily, supported by municipal repaint programs and widening do-it-yourself channels.

Polyurethane, though a smaller base, is accelerating at 5.88% CAGR to 2030 as vehicle makers and industrial-maintenance engineers shift to one-component waterborne chemistries that cut booth times and raise chemical resistance. Epoxies retain their foothold in heavy anticorrosive service, though PFAS exit paths demand parallel innovation to sustain barrier metrics. Alkyds, squeezed by VOC levies, find reprieve in bio-sourced variants that swap azelaic acid for petroleum feedstocks, easing regulatory scrutiny while keeping familiar workability.

The Waterborne Coatings Report is Segmented by Resin Type (Acrylic, Alkyd, Epoxy, Polyurethane, Polyester, Polyvinylidene Chloride, and More), End-User Industry (Building and Construction, Automotive, Industrial, Wood, and Other End-User Industries), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific commanded 42.61% of global revenue in 2024 and is on track for a market-leading 6.01% CAGR to 2030, cementing its position as the growth engine for the waterborne coatings market. China's stimulus packages revive industrial output, expanding baseline demand for general-industrial enamels, while India's concrete-intensive smart-city corridors open long-haul orders for elastomeric roof and bridge membranes.

North America reflects regulatory maturity mixed with technology leadership. California's 50 g/L cap forces nationwide SKUs to align at the lowest permissible VOC, rippling through distribution chains and spurring rapid reformulation. Canada's national VOC rulebook harmonizes provincial limits, smoothing market access for compliant waterborne lines from Quebec to British Columbia.

Europe remains a sustainability trend-setter through the Chemicals Strategy for Sustainability, accelerating waterborne adoption across architectural, industrial, and DIY shelves. AkzoNobel's BASF-enabled Dulux Easycare relaunch in the UK advances its pledge to cut product carbon by 5% minimum, strengthening brand pull among eco-conscious shoppers. Eastern-European urbanization also drives incremental liters, especially in municipal road and rail renovations funded by EU recovery programs.

- Akzo Nobel N.V.

- Arkema

- Asian Paints Ltd.

- Axalta Coating Systems, LLC

- BASF

- Benjamin Moore & Co.

- Berger Paints India

- Chokwang Paint

- Dow

- Hempel A/S

- Jotun

- Kansai Paint Co., Ltd.

- KCC Corporation

- Masco Corporation

- Nippon Paint Holdings Co., Ltd.

- PPG Industries, Inc.

- RPM International Inc.

- Sika AG

- Teknos Group

- Tenaris

- The Sherwin-Williams Company

- Tikkurila

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stricter VOC and Decarbonization Mandates

- 4.2.2 Rapid Infrastructure Buildouts in Asia and Africa

- 4.2.3 OEM One-Component Conversion from Solvent to Water Systems

- 4.2.4 Bio-Based Resin Breakthroughs (eg, Lignin, Algae)

- 4.2.5 Smart Factory Demand for Low-Temperature Cure Lines

- 4.3 Market Restraints

- 4.3.1 Scarcity and Price Volatility of Specialty Rheology Additives

- 4.3.2 Humidity-Related Drying Defects in Tropical Regions

- 4.3.3 PFAS-Free Performance Gap for Extreme Anticorrosion

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Resin Type

- 5.1.1 Acrylic

- 5.1.2 Alkyd

- 5.1.3 Epoxy

- 5.1.4 Polyurethane

- 5.1.5 Polyester

- 5.1.6 Polyvinylidene Chloride (PVDC)

- 5.1.7 Polyvinylidene Fluoride (PVDF)

- 5.1.8 Other Resin Types

- 5.2 By End-user Industry

- 5.2.1 Building and Construction

- 5.2.2 Automotive

- 5.2.3 Industrial

- 5.2.4 Wood

- 5.2.5 Other End-user Industries

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Southeast Asia

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Russia

- 5.3.3.6 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 South Africa

- 5.3.5.4 Egypt

- 5.3.5.5 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Akzo Nobel N.V.

- 6.4.2 Arkema

- 6.4.3 Asian Paints Ltd.

- 6.4.4 Axalta Coating Systems, LLC

- 6.4.5 BASF

- 6.4.6 Benjamin Moore & Co.

- 6.4.7 Berger Paints India

- 6.4.8 Chokwang Paint

- 6.4.9 Dow

- 6.4.10 Hempel A/S

- 6.4.11 Jotun

- 6.4.12 Kansai Paint Co., Ltd.

- 6.4.13 KCC Corporation

- 6.4.14 Masco Corporation

- 6.4.15 Nippon Paint Holdings Co., Ltd.

- 6.4.16 PPG Industries, Inc.

- 6.4.17 RPM International Inc.

- 6.4.18 Sika AG

- 6.4.19 Teknos Group

- 6.4.20 Tenaris

- 6.4.21 The Sherwin-Williams Company

- 6.4.22 Tikkurila

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

水性塗料市場分析及預測(至2035年):按類型、產品類型、應用、技術、成分、最終用戶和功能分類

水性塗料市場分析及預測(至2035年):按類型、產品類型、應用、技術、成分、最終用戶和功能分類 全球水性塗料市場規模、佔有率、趨勢及成長分析報告(2026-2034)

全球水性塗料市場規模、佔有率、趨勢及成長分析報告(2026-2034) 2026年全球水性塗料市場報告

2026年全球水性塗料市場報告 ACE低溫水性塗料市場依樹脂類型、應用及通路-2026-2032年全球預測

ACE低溫水性塗料市場依樹脂類型、應用及通路-2026-2032年全球預測 水性塗料市場規模、佔有率及成長分析(按樹脂類型、應用和地區分類)-2026-2033年產業預測水性被覆劑市場:2025-2032年全球預測(按樹脂類型、基材、應用方法和分銷管道分類)

水性塗料市場規模、佔有率及成長分析(按樹脂類型、應用和地區分類)-2026-2033年產業預測水性被覆劑市場:2025-2032年全球預測(按樹脂類型、基材、應用方法和分銷管道分類) 水性塗料市場-全球產業規模、佔有率、趨勢、機會及預測,按樹脂類型、應用、地區及競爭情況細分,2020-2030 年全球水性塗料市場規模(按樹脂類型、最終用戶、地區、範圍和預測)

水性塗料市場-全球產業規模、佔有率、趨勢、機會及預測,按樹脂類型、應用、地區及競爭情況細分,2020-2030 年全球水性塗料市場規模(按樹脂類型、最終用戶、地區、範圍和預測)