|

市場調查報告書

商品編碼

1844455

汽車空氣懸吊:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)Automotive Air Suspension - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

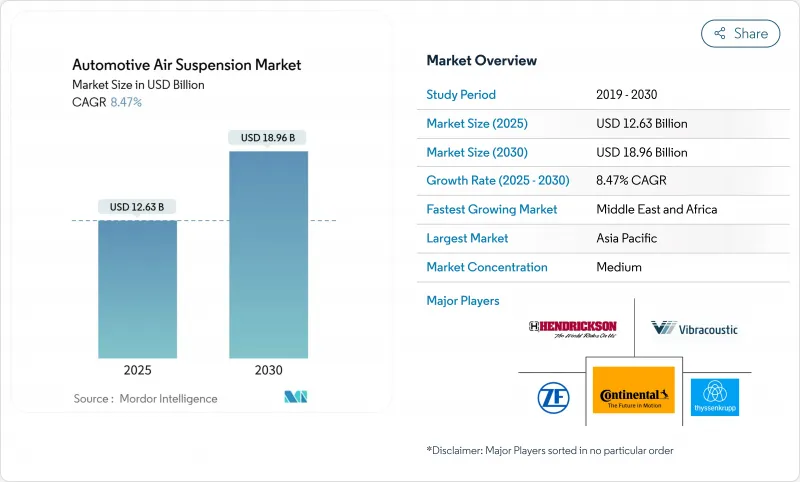

預計 2025 年空氣懸吊系統市場價值將達到 126.3 億美元,到 2030 年將達到 189.6 億美元,複合年成長率為 8.47%。

對高階乘坐舒適性不斷成長的需求、與軟體定義底盤的更深層次整合以及乘用車和商用車的電氣化預計將推動強勁成長。原始設備製造商的平台策略擴大將空氣懸吊定位為自我調整動力學的核心,而一級供應商正在將電子控制、減震和感測技術整合到模組化產品中。雖然乘用車仍然是主要的銷售驅動力,但電動重型卡車和 SUV 正在釋放新的價值池,其中最佳化的重量轉移和預測性車輛高度控制直接轉化為節能。從區域來看,亞太地區依然強勁,得益於中國的高檔汽車銷售和日本的技術創新,而中東和非洲是成長最快的地區,受到基礎設施投資和豪華汽車激增的推動。

全球汽車空氣懸吊市場趨勢與洞察

對乘坐舒適度和乘坐品質的要求不斷提高

在消費者意識和品牌差異化策略的推動下,即使在主流細分市場,人們對高階舒適性的期望也日益強烈。英菲尼迪2025款QX80的電子控制氣壓懸吊體現了這種轉變,它可以動態調整行駛高度,方便上下車、提高越野鉸接性和牽引穩定性。隨著可支配收入的不斷成長,亞洲買家對兼具便利性和身份地位的功能特別敏感。在純電動SUV中,整合式雙腔空氣彈簧(例如探測車探測車導航系統中的eHorizon資訊預先調整減震器設定。總而言之,這些進步強化了空氣懸吊作為全球市場上明顯差異化因素的地位。

亞太地區和歐洲豪華和高檔汽車銷量不斷成長

中國仍然是高階汽車需求中心,國內外廠商都在擴大電子空氣懸吊的應用,以吸引心儀的買家。 BMW的目標是到2024年,電動車在其全球銷量中的佔比達到17.4%,這凸顯了電氣化通常與可選的空氣懸吊套件相輔相成,以實現更低的車內噪音和空氣動力學最佳化的姿態控制。梅賽德斯-奔馳在上海的研發中心擴建正在加速底盤技術的本地化,包括針對當地路況設計的空氣懸吊模組。為了擊敗西方競爭對手,中國高階電動車新興企業正在將節省成本的空氣懸吊系統引入中端價格分佈,加速其區域普及。

中型車輛的系統和整合成本高

電控空氣懸吊的零件成本可能比傳統鋼製彈簧高出數百美元,這阻礙了其在成本敏感的C級車中的應用。複雜的校準需要額外的ECU邏輯和強化的底盤支架,這進一步增加了工程成本。新興市場的OEM廠商更重視低成交價格而非先進的底盤舒適性,減緩了其在大眾市場的普及。小鵬汽車在G9上採用Vibracoustic的雙腔彈簧,同時保持了具有競爭力的價格,這就是降低成本創新的一個例子。

細分分析

到2024年,NECAS解決方案將佔據空氣懸吊系統市場55.75%的佔有率。該領域在靜態負載平衡已足夠滿足需求的客車、拖車和基本款皮卡車型中依然受歡迎。另一方面,隨著原始設備製造商轉向以軟體為中心的架構,ECAS正以9.42%的複合年成長率快速擴張。 ECAS單元使用來自加速計、相機和地圖服務的數據來預測懸吊設置,從而提升舒適性和行駛操控性。 ECAS還能實現可變行駛高度,以最佳化電動車的空氣動力學性能,這對於即將推出的高階跨界車至關重要。

軟體定義汽車專注於無線校準和功能解鎖,這些是 ECAS 獨有的功能。採埃孚 (ZF) 的 sMOTION 和大陸集團的 E-Level 系列支援售後更新,例如微調彈簧曲線或添加越野模式。 NECAS 在改裝和成本敏感領域仍然很重要。然而,隨著 ECAS 成為中型豪華轎車、高性能 SUV 和電動送貨車的標配,其佔有率預計會下降。閥門和壓力感測器價格的持續下降可能會加速各個價值領域向 ECAS 的轉變。

以高階轎車和SUV為主導的乘用車市場,其舒適性提升是其賣點,到2024年將佔據空氣懸吊系統65.45%的市場佔有率。同時,中重型卡車的複合年成長率將達到8.32%,在所有車型中最高。電動傳動系統透過實現自動負載平衡和車身高度控制,進一步提升了空氣懸吊的價值,從而延長了續航里程並保護了電池組。輕型商用貨車和長途客車正在分別採用該技術來提高城市配送效率和乘客舒適度,但其成長速度落後於中重型卡車。

8級電動曳引機的空氣懸吊技術透過分配軸荷並保持在法定重量限制範圍內,減輕了電池重量帶來的負擔。雖然乘用車將繼續在銷售方面保持領先,但商用車領域將推動創新週期,影響零件的耐用性和預測性維護能力,並最終將影響零售車型。

由於整合複雜性以及懸吊調校與碰撞安全性和ADAS合規性之間的協調,到2024年,原廠配件將佔據空氣懸吊系統市場佔有率的74.23%。隨著車輛老化以及車迷對舒適性和車身姿態的追求,售後市場將以7.72%的複合年成長率擴張。 Arnott Industries(現已被MidOcean Partners收購)正在積極擴展其針對歐洲SUV和美國肌肉車的多品牌替換套件,這表明其有意在售後市場進行整合。

當原廠氣壓彈簧達到使用壽命時,消費者會轉向售後市場套件。即插即用型 ECAS 替換模組的日益普及,縮短了安裝時間,並擴大了吸引力。 OEM 頻道對於初始安裝仍然至關重要,因為保固範圍、認證和整合診斷至關重要。售後市場從老舊車隊、性能愛好者以及尋求可調離地間隙的利基越野社區中獲取增量收益。

區域分析

2024年,亞太地區將以39.26%的市佔率引領氣壓懸吊系統市場。中國對豪華車和電動車的需求將推動大部分銷量,而日本品牌將繼續完善其舒適性技術。梅賽德斯-奔馳正在利用全球一級供應商的本地化研發和製造能力,縮短其供應鏈,並根據不同地區的乘坐舒適性偏好調整規格。政府對新能源汽車的支持也提高了先進底盤整合的標準。

隨著基礎建設計劃和富裕消費群的融合,到2030年,中東和非洲的複合年成長率將達到7.25%,成為最快的地區。高階SUV和皮卡將佔據主導地位,買家優先考慮高度可調的懸架,以便在沙漠地形中靈活行駛。歐洲保持著較高的滲透率,因為嚴格的車輛二氧化碳排放法規推動了輕量化空氣彈簧和基於高度的空氣動力效率策略的發展。

北美市場以皮卡和重型卡車為主。 Stellantis 和其他底特律三巨頭製造商正在圍繞空氣懸吊模組重組其車身框架平台,以滿足純電動車的牽引穩定性和空氣動力學性能。南美雖然仍是一個新興市場,但受節能零件進口關稅降低的推動,巴西的高階 SUV組裝正在成長。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場狀況

- 市場概況

- 市場促進因素

- 對乘坐和座艙舒適度的需求不斷增加

- 擴大亞太和歐洲豪華及高級汽車的銷售

- ECAS 與 ADAS 和底盤網域控制站的整合

- 電動重型卡車的燃油節省(報告不足)

- 預測性維護數位孿生降低物流的整體擁有成本(未充分通報)

- 加強對振動敏感貨物(漏報)的監管

- 市場限制

- 中階車輛的系統和整合成本高

- 對可靠性和維護複雜性的擔憂

- ECU 連線 ECAS 中未充分報告的網路安全風險

- 彈性體和複合材料價格波動(未報告)

- 價值/供應鏈分析

- 監管狀況

- 技術展望

- 轉向 48V 和軟體定義底盤

- 輕質複合材料空氣彈簧波紋管

- 波特五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭強度

第5章市場規模及成長預測

- 按控制類型

- 電子控制空氣懸吊(ECAS)

- 非電子控制空氣懸吊(NECAS)

- 按車輛類型

- 搭乘用車

- 輕型商用車

- 中型和大型卡車

- 公車和長途客車

- 按最終用戶

- OEM

- 售後市場

- 按組件

- 空氣彈簧

- 壓縮機和儲液器

- 電控系統

- 車輛高度和壓力感測器

- 避震器

- 透過促銷

- 內燃機汽車

- 純電動車

- 按懸掛結構

- 被動式空氣懸吊

- 半自我調整氣壓懸吊

- 全主動氣壓懸吊

- 按銷售管道

- 直接銷售給原始設備製造商

- 一級/模組供應商

- 按地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 其他亞太地區

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 奈及利亞

- 其他中東和非洲地區

- 北美洲

第6章 競爭態勢

- 市場集中度

- 策略舉措

- 市佔率分析

- 公司簡介

- Continental AG

- ZF Friedrichshafen AG

- Hendrickson International

- Thyssenkrupp Bilstein

- Vibracoustic SE

- Firestone Industrial Products

- Hitachi Astemo

- Mando Corporation

- SAF-Holland SE

- Meritor(Cummins)

- AccuAir Suspension

- Air Lift Company

- Arnott Industries

- BWI Group

- KYB Corporation

- Komman Air Suspension

- Guangzhou Guomat Air Spring

- Dunlop Systems & Components

- Tenneco Inc.

第7章 市場機會與未來展望

The Air Suspension Systems Market is valued at USD 12.63 billion in 2025 and is forecast to reach USD 18.96 billion by 2030, expanding at an 8.47% CAGR.

Rising demand for premium ride quality, deeper integration with software-defined chassis, and the electrification of both passenger and commercial vehicles create a strong growth runway. OEM platform strategies increasingly position air suspension as a core enabler for adaptive dynamics, while tier-1 suppliers consolidate electronic control, damping, and sensing technologies into modular offerings. Passenger cars still anchor volume, yet electrified heavy trucks and SUVs are unlocking new value pools where optimized weight transfer and predictive height control translate directly into energy savings. Regional momentum remains strongest in Asia-Pacific, buoyed by Chinese luxury sales and Japanese innovation, whereas the Middle East and Africa are emerging as the fastest-growing arena on the back of infrastructure investment and premium vehicle uptake

Global Automotive Air Suspension Market Trends and Insights

Rising Demand for Ride Quality and Cabin Comfort

Premium comfort expectations are now evident even in mainstream segments, driven by consumer awareness and brand differentiation strategies. INFINITI's 2025 QX80 illustrates this shift with an Electronic Air Suspension that adjusts dynamic height for easy ingress, off-road articulation, and towing stability. Asian buyers, supported by rising disposable incomes, are particularly responsive to features that marry convenience with perceived status. In battery-electric SUVs, integrating two-chamber air springs, such as Vibracoustic's system for XPeng's G9, allows simultaneous ride compliance and battery thermal management. Predictive algorithms using road-surface data further enhance comfort and handling; Land Rover's latest Range Rover employs navigation-fed eHorizon information to pre-condition damper settings. Collectively, these advances reinforce air suspension as a tangible differentiator across global markets.

Growing Luxury and Premium Vehicle Sales in Asia-Pacific and Europe

China remains the epicenter of premium demand, with domestic and imported marques expanding electronic air suspension fitment to secure aspirational buyers. BMW achieved a 17.4% EV mix in 2024 global deliveries, underscoring how electrification often coincides with optional air suspension packages for cabin tranquility and aero-optimized stance control. Mercedes-Benz's enlarged R&D footprint in Shanghai accelerates the localization of chassis technologies, including air suspension modules designed for local road conditions. Chinese premium EV startups, keen to undercut Western rivals, are bringing cost-controlled air systems to mid-tier price points, quickening regional adoption.

High System and Integration Cost for Mid-Segment Vehicles

The electronic air suspension bill of material can exceed conventional steel springs by several hundred USD, discouraging inclusion in cost-sensitive C-segment cars. Complex calibration work added ECU logic and reinforced chassis mounts, further inflating engineering spending. Emerging-market OEMs prioritize lower transaction prices over advanced chassis comfort, delaying penetration in mass segments. Nonetheless, localized sourcing in China and leaner component designs are narrowing the gap; XPeng's decision to deploy Vibracoustic's two-chamber springs while keeping the G9's price competitive exemplifies cost-down innovation.

Other drivers and restraints analyzed in the detailed report include:

- Integration of ECAS with ADAS and Chassis Domain Controllers

- Fleet Fuel-Saving Benefits for Electric Heavy-Duty Trucks

- Reliability & Maintenance Complexity Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

NECAS Solutions retained a 55.75% share of the air suspension systems market in 2024, mainly because fleet buyers value proven simplicity and lower acquisition costs. The segment remains prevalent in buses, trailers, and basic pickup models where static load leveling suffices. In contrast, ECAS is scaling fast at a 9.42% CAGR as OEMs migrate toward software-centric architectures. ECAS units harvest data from accelerometers, cameras, and map services to predict suspension settings, improving both comfort and handling on the fly. ECAS also supports variable ride height for EV aero optimization, making it indispensable for forthcoming premium crossovers.

Software-defined vehicles emphasize over-the-air calibration and feature unlocks, capabilities inherent to ECAS. ZF's sMOTION and Continental's E-Level families allow post-sale updates that fine-tune spring curves or add off-road modes. NECAS remains relevant in retrofit and cost-driven regions. Yet, its share is projected to decline as ECAS becomes standard on mid-size luxury sedans, performance SUVs, and electric delivery vans. The ongoing price erosion of valves and pressure sensors will accelerate the pivot toward ECAS across value segments.

Passenger cars captured 65.45% of the air suspension systems market share in 2024 through luxury sedans and SUVs, where heightened comfort is a selling point. Medium and Heavy trucks, however, are on track for an 8.32% CAGR, the highest among all vehicle categories. Electrified drivelines amplify the value of air suspension by enabling automated load balancing and ride-height control that extend the range and protect battery packs. Light commercial vans and coaches adopt the technology for urban delivery efficiency and passenger comfort, respectively, although their growth profile lags medium and heavy trucks.

Air suspension technology in Class 8 electric tractors mitigates battery mass penalties by distributing axle loads while preserving legal weight limits. Passenger cars will keep leading in volume terms, yet commercial segments drive innovation cycles, influencing component durability and predictive maintenance capabilities that later cascade into retail models

OEM fitment accounted for 74.23% of the air suspension systems market share in 2024 revenue because of integration complexity and the need to align suspension tuning with crash safety and ADAS calibration. The aftermarket expands at 7.72% CAGR as vehicle parc ages and enthusiasts seek comfort or stance upgrades. Arnott Industries, now under MidOcean Partners, is aggressively expanding multi-brand replacement kits for European SUVs and American muscle cars, signaling consolidation intent within the retrofit domain.

Consumers turn to aftermarket kits when factory air springs reach end-of-life, often after eight years. Increased availability of plug-and-play ECAS replacement modules reduces installation time, broadening appeal. OEM channels remain indispensable for first-fitment, where warranty coverage, homologation, and integrated diagnostics are paramount. The aftermarket will capture incremental revenue from aging fleets, performance enthusiasts, and niche off-road communities seeking adjustable ground clearance.

Automotive Air Suspension Market Report is Segmented by Control Type (ECAS and NECAS), Vehicle Type (Passenger Cars and More), End User (OEM and Aftermarket), Component (Air Springs and More), Propulsion (ICE and BEV), Suspension Architecture (Passive Air Suspension and More), Sales Channel (Direct To OEM and More) and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Geography Analysis

Asia-Pacific led the air suspension systems market with a 39.26% share in 2024. Chinese luxury and electric vehicle demand fuels most of the volume, while Japanese brands continue to refine comfort technologies. Mercedes-Benz's localized R&D and manufacturing footprints by global tier-1 suppliers shorten supply chains and adapt specifications for regional ride-comfort preferences. Government support for new energy vehicles also raises the ceiling for advanced chassis integration.

As infrastructure projects and affluent consumer bases converge, the Middle East and Africa will deliver the fastest CAGR at 7.25% through 2030. Premium SUVs and pickups dominate the mix, and buyers value height-adjustable suspensions for desert terrain versatility. Europe retains high penetration because stringent fleet CO2 limits encourage lightweight air springs and height-based aero efficiency strategies.

North America's dynamics hinge on pickup and heavy-truck adoption. Stellantis and other Detroit-Three manufacturers are reorganizing body-on-frame platforms around air suspension modules to satisfy towing stability and BEV aerodynamics. South America remains emergent but shows rising uptake in Brazilian premium SUV assembly, aided by import-duty reductions on components that enhance fuel economy.

- Continental AG

- ZF Friedrichshafen AG

- Hendrickson International

- Thyssenkrupp Bilstein

- Vibracoustic SE

- Firestone Industrial Products

- Hitachi Astemo

- Mando Corporation

- SAF-Holland SE

- Meritor (Cummins)

- AccuAir Suspension

- Air Lift Company

- Arnott Industries

- BWI Group

- KYB Corporation

- Komman Air Suspension

- Guangzhou Guomat Air Spring

- Dunlop Systems & Components

- Tenneco Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for ride quality & cabin comfort

- 4.2.2 Growing luxury & premium vehicle sales in Asia-Pacific & Europe

- 4.2.3 Integration of ECAS with ADAS & chassis domain controllers

- 4.2.4 Fleet fuel-saving benefits for electric heavy-duty trucks (under-reported)

- 4.2.5 Predictive-maintenance digital twins lowering TCO for logistics fleets (under-reported)

- 4.2.6 Vibration-sensitive cargo regulations tightening (under-reported)

- 4.3 Market Restraints

- 4.3.1 High system & integration cost for mid-segment vehicles

- 4.3.2 Reliability & maintenance complexity concerns

- 4.3.3 Cyber-security risks in ECU-connected ECAS (under-reported)

- 4.3.4 Elastomer & composite price volatility (under-reported)

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.6.1 Transition to 48-V & software-defined chassis

- 4.6.2 Lightweight composite air-spring bellows

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Control Type

- 5.1.1 Electronically Controlled Air Suspension (ECAS)

- 5.1.2 Non-Electronically Controlled Air Suspension (NECAS)

- 5.2 By Vehicle Type

- 5.2.1 Passenger Cars

- 5.2.2 Light Commercial Vehicles

- 5.2.3 Medium and Heavy Trucks

- 5.2.4 Buses & Coaches

- 5.3 By End User

- 5.3.1 OEM

- 5.3.2 Aftermarket

- 5.4 By Component

- 5.4.1 Air Springs

- 5.4.2 Compressors and Reservoirs

- 5.4.3 Electronic Control Units

- 5.4.4 Height & Pressure Sensors

- 5.4.5 Shock Dampers

- 5.5 By Propulsion

- 5.5.1 ICE Vehicles

- 5.5.2 Battery-Electric Vehicles

- 5.6 By Suspension Architecture

- 5.6.1 Passive Air Suspension

- 5.6.2 Semi-Active / Adaptive Air Suspension

- 5.6.3 Fully Active Air Suspension

- 5.7 By Sales Channel

- 5.7.1 Direct to OEM

- 5.7.2 Tier-1 / Module Supplier

- 5.8 By Geography

- 5.8.1 North America

- 5.8.1.1 United States

- 5.8.1.2 Canada

- 5.8.1.3 Rest of North America

- 5.8.2 South America

- 5.8.2.1 Brazil

- 5.8.2.2 Argentina

- 5.8.2.3 Rest of South America

- 5.8.3 Europe

- 5.8.3.1 Germany

- 5.8.3.2 United Kingdom

- 5.8.3.3 France

- 5.8.3.4 Italy

- 5.8.3.5 Spain

- 5.8.3.6 Rest of Europe

- 5.8.4 Asia-Pacific

- 5.8.4.1 China

- 5.8.4.2 Japan

- 5.8.4.3 India

- 5.8.4.4 South Korea

- 5.8.4.5 Rest of Asia-Pacific

- 5.8.5 Middle East and Africa

- 5.8.5.1 Saudi Arabia

- 5.8.5.2 United Arab Emirates

- 5.8.5.3 South Africa

- 5.8.5.4 Nigeria

- 5.8.5.5 Rest of Middle East and Africa

- 5.8.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Continental AG

- 6.4.2 ZF Friedrichshafen AG

- 6.4.3 Hendrickson International

- 6.4.4 Thyssenkrupp Bilstein

- 6.4.5 Vibracoustic SE

- 6.4.6 Firestone Industrial Products

- 6.4.7 Hitachi Astemo

- 6.4.8 Mando Corporation

- 6.4.9 SAF-Holland SE

- 6.4.10 Meritor (Cummins)

- 6.4.11 AccuAir Suspension

- 6.4.12 Air Lift Company

- 6.4.13 Arnott Industries

- 6.4.14 BWI Group

- 6.4.15 KYB Corporation

- 6.4.16 Komman Air Suspension

- 6.4.17 Guangzhou Guomat Air Spring

- 6.4.18 Dunlop Systems & Components

- 6.4.19 Tenneco Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

電子控制氣壓懸吊系統市場:按零件、車輛類型、銷售管道和分銷管道分類 - 全球預測 2025-2032氣壓懸吊市場按組件、系統類型、車輛類型、銷售管道和最終用戶分類-2025-2030 年全球預測空氣彈簧市場按類型、組件、材料、銷售管道、應用和最終用戶產業分類-2025-2030 年全球預測

電子控制氣壓懸吊系統市場:按零件、車輛類型、銷售管道和分銷管道分類 - 全球預測 2025-2032氣壓懸吊市場按組件、系統類型、車輛類型、銷售管道和最終用戶分類-2025-2030 年全球預測空氣彈簧市場按類型、組件、材料、銷售管道、應用和最終用戶產業分類-2025-2030 年全球預測 氣壓懸吊座椅市場-全球產業規模、佔有率、趨勢、機會和預測,按應用、類型、地區和競爭細分,2020-2030 年

氣壓懸吊座椅市場-全球產業規模、佔有率、趨勢、機會和預測,按應用、類型、地區和競爭細分,2020-2030 年 汽車空氣懸吊市場規模、佔有率、成長分析(按組件、按類型、按推進器、按車輛類型、按地區)- 2025 年至 2032 年行業預測

汽車空氣懸吊市場規模、佔有率、成長分析(按組件、按類型、按推進器、按車輛類型、按地區)- 2025 年至 2032 年行業預測 汽車空氣彈簧市場(2026-2032):按類型、應用和地區分類

汽車空氣彈簧市場(2026-2032):按類型、應用和地區分類 按車型、技術類型、銷售通路、地區、機會和預測對全球汽車空氣懸吊市場進行評估(2018 年至 2032 年)全球氣壓懸吊市場規模(按技術、應用、產品、地區和預測)

按車型、技術類型、銷售通路、地區、機會和預測對全球汽車空氣懸吊市場進行評估(2018 年至 2032 年)全球氣壓懸吊市場規模(按技術、應用、產品、地區和預測) 2025年全球氣壓懸吊市場報告2025年全球汽車空氣懸吊市場報告

2025年全球氣壓懸吊市場報告2025年全球汽車空氣懸吊市場報告