|

市場調查報告書

商品編碼

1842544

分析儀器:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)Analytical Instrumentation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

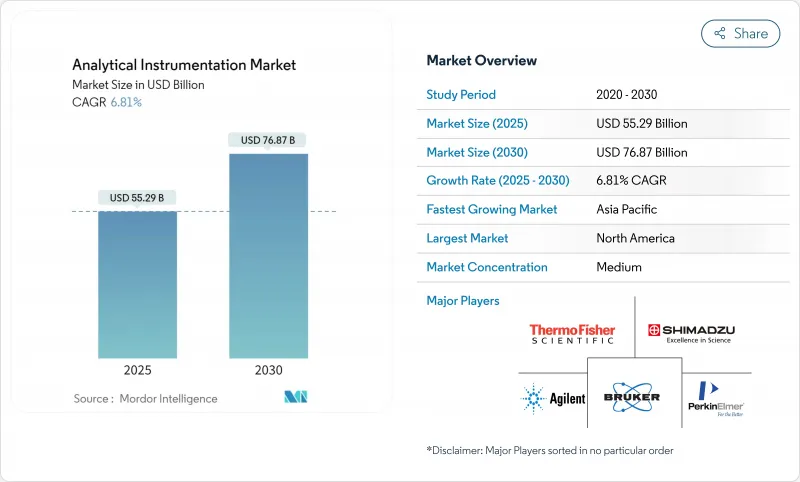

分析儀器市場預計在 2025 年達到 552.9 億美元,在 2030 年達到 768.7 億美元,複合年成長率為 6.81%,顯示高精度測量工具將強勁擴張。

製藥和環境監測領域監管力度的加強、3奈米以下半導體節點的快速擴展以及人工智慧與實驗室硬體的融合,正在推動所有主要終端用戶群體的採用。供應商正在加大對用於連續製藥生產的即時放行檢測解決方案、用於PFAS控制的超痕量光譜平台以及支援生技藥品研發的多組體學質譜儀的投資。同時,氦氣供應的不穩定性正在重塑氣相層析法工作流程,持續的分析化學人才短缺推高了外包成本,並促使買家轉向自動化。這些因素共同作用,使分析設備市場保持價格競爭力,並加速其升級換代。

全球分析儀器市場趨勢與洞察

生技藥品品質保證/品質控制中擴大採用聯用技術

對複雜生技藥品的需求日益成長,促使製造商用聯用液相層析法-質譜平台取代單維方法。目前,近78%的生物製藥廠在其品質營運中至少擁有一個聯用工作流程,高於2023年的水平,從而能夠對關鍵品質屬性進行多屬性監控,並將批次拒收率降低15%。增強的系統整合能夠即時分析轉譯後修飾,加速生產規模擴大和產品發布進度。增強的系統整合能夠即時分析轉譯後修飾,加速生產規模擴大和產品發布進度。這些優勢正在推動資本預算轉向高解析度液相層析串聯質譜(LC-MS/MS),並加強供應商對自動化資料流程的投資。

全球對 PFAS 和微塑膠的監管趨嚴推動超微量分析

歐洲指令中關於兆分之一(PPT)的法規,與2024年美國飲用水法規並行,迫使實驗室添置下一代高解析度質譜儀以及能夠識別小至1微米顆粒的拉曼或傅立葉變換紅外線顯微鏡。隨著超短鏈PFAS檢測成為強制性要求,這一趨勢可能會持續下去。市場領導目前正在捆綁自動化樣品製備,以延長運行間隔並降低檢測閾值,從而增強耗材的經常性收益。

高解析度 MS 的總體擁有成本較高

旗艦質譜儀的價格在50萬美元到150萬美元之間,但由於服務合約、基礎設施維修和專用耗材等因素,五年營運成本往往超過購買價格。由於關稅和本地服務能力有限,新興市場的實驗室面臨的總體擁有成本(TCO)高出30%到45%。即使監管趨嚴,這些障礙也減緩了水質和食品安全領域應用該技術的速度,促使供應商部署精簡的「價值工程」模型和共用服務中心。

細分分析

層析法系統將在 2024 年創造 154.8 億美元的收益,佔分析儀器市場佔有率的 28%。人工智慧校準程序可將吞吐量提高高達 70%,而預測演算法可以指示維護需求並支援 HPLC 和氣相層析的持續升級。在環境實驗室中,對 PFAS 進行分析的需求正在重新激發對先進色譜柱化學和串聯檢測器的需求。同時,質譜儀是成長最快的產品領域,預計到 2030 年將以 7.1% 的複合年成長率成長,因為離子淌度創新(例如具有淌度匹配碎裂的並行累積)可將試樣處理通量提高五倍並突破靈敏度的上限。

質譜分析儀器市場在需要更深入的分子層面洞察的行業中日益成長,例如臨床蛋白質組學、食品真偽鑑定和電池材料。三重四極和Q-TOF配置因其速度和解析度的平衡而佔據了新安裝設備的大多數。供應商的藍圖以超高場Orbitrap和timsTOF架構為中心,將硬體進步與雲端基礎的反捲積平台相結合,以縮短資料處理時間並釋放寶貴的分析師時間。雖然分子光譜仍然是常規品質保證/品質控制的核心收益支柱,但拉曼光譜在製藥連續生產領域正逐漸興起,其中線上探針可以即時檢驗混合均勻性。

高效液相層析和超高效液相層析法系統佔該類別的56%,達到86.7億美元,這得益於其卓越的重現性和基質耐受性,使其成為效價、雜質和穩定性測試的關鍵。人工智慧外掛程式可自動執行梯度設計、流動相選擇和故障預測,使試樣處理通量提高高達70%,同時消除色譜柱浪費。微流體晶片色譜柱正被引入蛋白質組學工作流程,實現與快速掃描質譜儀同步的亞分鐘分離,以支援數據豐富的多組體學研究。

預計到2030年,超臨界流體層析的複合年成長率將達到7.3%,成為成長最快的液相分離技術。使用二氧化碳和少量助溶劑可以實現綠色化學目標,降低單位樣品的溶劑成本,從而在掌性藥物篩檢和雜質分離領域提供極具吸引力的投資回報率。氣相層析法是揮發性物質分析的關鍵,但氦氣短缺推高了營業成本,加速了氫載體和微通道層析法的轉變。隨著監管機構加強對飲用水和工業廢水中離子污染物的限制,離子層析法正重新受到人們的關注。公用事業單位被要求添加自動化線上抑制器系統,以實現全天候監控。

區域分析

2024年,北美市場將達到193.5億美元,佔分析儀器市場的35%。 FDA主導的即時排放檢測、EPA強制執行的兆分之幾PFAS法規,以及520億美元的《晶片法案》(CHIPS Act)——該法案將資助採用亞奈米計量技術的新工廠——將推動需求成長。實驗室正在透過採用氫能氣相層析和低廢物高效液相層析泵來降低氦氣成本和溶劑浪費,展現其對更綠色工作流程的承諾。

亞太地區預計將以7.6%的複合年成長率成長,這反映了中國和印度製藥製造業的規模擴張,以及台灣和韓國先進邏輯和記憶體生產的擴大。地區政府正在加強水質和工業排放標準,鼓勵國有實驗室競標ICP-MS、LC-MS/MS、手持式拉曼光譜儀等設備的多年期採購合約。隨著晶圓代工廠競相開發環柵電晶體和高頻寬記憶體,亞太地區用於半導體品質保證/品質控制的分析設備市場規模預計將超過所有其他垂直領域。

歐洲保持著強而有力的監管主導立場。 《歐洲綠色交易》正在資助全國的PFAS監測、循環經濟研究和無溶劑層析法試點計畫。德國、愛爾蘭和瑞士的製藥中心正在整合包含PAT分析的連續生產線。同時,隨著煉油廠、農產品出口商和礦業公司對實驗室進行現代化升級以滿足國際貿易認證,南美洲和中東/非洲地區正在實現穩定但溫和的成長。由於高昂的TCO仍然是一個障礙,經銷商擴大推廣先租後買和按樣品付費的模式,以降低首次購買者的准入門檻。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場狀況

- 市場概況

- 市場促進因素

- 生技藥品品質保證/品質控制中擴大採用聯用技術

- 全球對 PFAS 和微塑膠的監管日益嚴格,推動超微量分析方法的發展

- 藥品生產轉向即時放行測試(RTRT)

- 將半導體節點縮小到 3 奈米以下需要超靈敏的表面分析。

- 擴大可再生航空燃料計劃以促進原料認證

- 透過實驗室分析,電池超級工廠的品質保證快速成長

- 市場限制

- 新興市場高解析度質譜的整體擁有成本較高

- 熟練分析化學家的短缺導致外包成本上升

- 氦氣供應鏈波動影響氣相層析操作

- 受監管領域新分析方法的驗證週期較長

- 產業生態系統分析

- 監理展望

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場規模及成長預測(金額)

- 依產品類型

- 層析法設備

- 氣相層析法(GC)系統

- 高效/超高效液相層析(HPLC/UHPLC)

- 離子層析法(IC)系統

- 超臨界流體層析(SFC)系統

- 分子光譜學

- 紫外可見光譜儀

- 傅立葉轉換紅外線(FT-IR)光譜儀

- 近紅外線(NIR)光譜儀

- 拉曼光譜儀

- 螢光光譜儀

- 元素光譜學

- 原子吸收光譜儀(AAS)

- 電感耦合等離子體發射光譜儀(ICP-OES)

- 電感耦合等離子體質譜儀(ICP-MS)

- X光螢光(XRF)光譜儀

- 質譜法

- 單四極質譜系統

- 四極質譜系統

- 四極飛行時間(Q-TOF) 質譜系統

- Orbitrap 和 FT-MS 系統

- MALDI-TOF質譜系統

- 分析顯微鏡和成像系統

- 掃描電子顯微鏡(SEM)

- 穿透式電子顯微鏡(TEM)

- 原子力顯微鏡(AFM)

- 共聚焦顯微鏡和光學顯微鏡

- 表面、熱和顆粒表徵設備

- X光衍射(XRD)系統

- 熱分析設備(DSC、TGA等)

- 粒度和ZETA電位分析儀

- 耗材及配件

- 資料管理軟體和服務

- 層析法設備

- 按最終用戶產業

- 製藥和生物製藥

- 藥物發現與開發

- 製造品質保證/品質控制

- 臨床和診斷實驗室

- 環境測試實驗室

- 食品和飲料測試

- 化工/石化

- 石油和天然氣(上游、中游、下游)

- 材料科學/冶金學

- 半導體和電子

- 學術和政府研究機構

- 取證與安全

- 用水和污水業務

- 製藥和生物製藥

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 北歐的

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 東南亞

- 澳洲

- 其他亞太地區

- 南美洲

- 巴西

- 南美洲其他地區

- 中東和非洲

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 其他中東地區

- 非洲

- 南非

- 其他非洲國家

- 北美洲

第6章 競爭態勢

- 市場集中度

- 策略性舉措(併購、合作、資金籌措)

- 市佔率分析

- 公司簡介

- Agilent Technologies, Inc.

- Thermo Fisher Scientific Inc.

- Shimadzu Corporation

- Danaher Corporation(SCIEX, Leica Microsystems)

- Bruker Corporation

- Waters Corporation

- PerkinElmer Inc.

- Metrohm AG

- Mettler Toledo International Inc.

- Malvern Panalytical Ltd.(Spectris)

- Hitachi High-Tech Corporation

- HORIBA, Ltd.

- JEOL Ltd.

- Anton Paar GmbH

- Bio-Rad Laboratories, Inc.

- ZEISS Group

- Oxford Instruments plc

- Nikon Instruments Inc.

- Rigaku Corporation

- LECO Corporation

- Sartorius AG

- Merck KGaA(MilliporeSigma)

第7章 市場機會與未來展望

The analytical instrumentation market is valued at USD 55.29 billion in 2025 and is projected to reach USD 76.87 billion by 2030, reflecting a 6.81% CAGR and signaling robust expansion in high-precision measurement tools.

Increasing regulatory oversight in pharmaceuticals and environmental monitoring, rapid semiconductor node shrinkage below 3 nm, and the convergence of artificial intelligence with laboratory hardware are boosting adoption across every major end-user group. Vendors are intensifying investments in real-time release testing solutions for continuous pharmaceutical manufacturing, ultra-trace spectrometry platforms for PFAS control, and multi-omics mass spectrometry to support biologics pipelines. Simultaneously, helium supply volatility is reshaping gas chromatography workflows, while persistent talent shortages in analytical chemistry elevate outsourcing costs and nudge buyers toward automation. Together, these forces are sustaining pricing power and fueling incremental upgrades in the analytical instrumentation market.

Global Analytical Instrumentation Market Trends and Insights

Rising Adoption of Hyphenated Techniques for Biologics QA/QC

Growing demand for complex biologics is encouraging manufacturers to replace single-dimension methods with hyphenated liquid chromatography-mass spectrometry platforms. Nearly 78% of biopharmaceutical plants now deploy at least one hyphenated workflow in quality operations, up from 2023 levels, enabling multi-attribute monitoring of critical quality attributes and trimming batch rejection rates by 15%.Enhanced system integration allows real-time profiling of post-translational modifications, accelerating scale-up and release schedules. These gains are pushing capital budgets toward high-resolution LC-MS/MS and reinforcing supplier investments in automated data pipelines.

Stringent Global Limits on PFAS and Micro-plastics Boosting Ultra-Trace Spectrometry

Parts-per-trillion limits in the 2024 U.S. drinking-water rule and parallel European directives are forcing laboratories to add next-generation high-resolution mass spectrometers and Raman or FTIR microscopes capable of identifying particles down to 1 µm. Environmental labs increased capital outlays for such systems by 34% in 2024 alone, a trend likely to continue as ultrashort-chain PFAS detection becomes compulsory.Market leaders now bundle automated sample preparation that extends run-time intervals and lowers detection thresholds, thereby strengthening recurring consumables revenue.

High Total Cost of Ownership for High-Resolution MS

Pricing for flagship mass spectrometers ranges between USD 500,000 and USD 1.5 million, yet five-year operating expenses often exceed purchase price because of service contracts, infrastructure retrofits, and specialized consumables. Emerging-market labs face 30% to 45% higher TCO due to tariffs and limited local service capacity. These barriers delay adoption in water-quality and food-safety settings even as regulations tighten, prompting vendors to roll out streamlined "value-engineered" models and shared-service hubs.

Other drivers and restraints analyzed in the detailed report include:

- Shift Toward Real-Time Release Testing in Pharma Production

- Semiconductor Node Shrinkage Less than 3 nm Requiring Ultra-Sensitive Surface Analysis

- Shortage of Skilled Analytical Chemists Elevating Outsourcing Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Chromatography systems generated USD 15.48 billion in revenue and commanded 28% of analytical instrumentation market share in 2024. AI-enabled calibration routines now boost throughput by up to 70% while predictive algorithms flag maintenance needs, supporting sustained upgrades in both HPLC and gas chromatograph. In environmental labs, the need to profile PFAS has revived demand for advanced column chemistries and tandem detectors. Mass spectrometry, meanwhile, represents the fastest-expanding product family, slated for 7.1% CAGR through 2030 as ion-mobility innovations such as parallel accumulation with mobility-aligned fragmentation quintuple sample throughput and push sensitivity ceilings .

The analytical instrumentation market size for mass spectrometers is benefiting from cross-industry uptake-clinical proteomics, food authenticity, and battery materials all require deeper molecular insight. Triple-quadrupole and Q-TOF configurations account for the bulk of new installations owing to their balance between speed and resolution. Supplier roadmaps center on ultrahigh-field Orbitrap and timsTOF architectures that couple hardware advances with cloud-based deconvolution platforms, trimming data-processing times and freeing scarce analyst hours. Molecular spectroscopy remains a core revenue pillar for routine QA/QC, though Raman is gaining ground in pharmaceutical continuous manufacturing, where in-line probes verify blend uniformity in real time.

High-performance and ultra-high-performance liquid chromatography systems commanded 56% of this category, valued at USD 8.67 billion, as their reproducibility and matrix tolerance make them indispensable for potency, impurity, and stability testing. Artificial-intelligence plug-ins now automate gradient design, mobile-phase selection, and fault prediction, boosting sample throughput by up to 70% while reducing column waste. Microfluidic chip columns are entering proteomic workflows, delivering sub-minute separations that synchronize with fast-scanning mass spectrometers and support data-rich multi-omics studies.

Supercritical-fluid chromatography is projected to advance at 7.3% CAGR through 2030, the quickest cadence within liquid-phase separations. Its use of CO2 and minimal co-solvent meets green-chemistry targets and lowers per-sample solvent cost, creating attractive payback in chiral drug screening and impurity isolation. Gas chromatography remains vital for volatile analyses, yet helium scarcity elevates operating expenses, accelerating migration to hydrogen carriers and micro-channel alternatives. Ion chromatography is back in focus as regulators tighten ionic-contaminant limits in drinking water and industrial effluent, prompting utilities to add automated inline suppressor systems that can handle 24/7 monitoring.

The Analytical Instrumentation Market Report is Segmented by Product Type (Chromatography Instruments, Molecular Spectroscopy, Elemental Spectroscopy, Mass Spectrometry, and More), End-User Industry (Pharmaceuticals and Biopharmaceuticals, Clinical and Diagnostics Laboratories, Environmental Testing Laboratories, Chemical and Petrochemical, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated USD 19.35 billion in 2024, equivalent to 35% of the analytical instrumentation market. Demand is anchored in FDA-driven real-time release testing, EPA-mandated parts-per-trillion PFAS limits, and a USD 52 billion CHIPS Act outlay that funds new fabs, each specifying sub-nanometer metrology. Laboratories adopt hydrogen-ready gas chromatographs and low-dead-volume HPLC pumps to mitigate helium costs and solvent waste, illustrating an appetite for greener workflows.

Asia-Pacific is forecast to deliver a 7.6% CAGR, reflecting pharmaceutical manufacturing scale-ups in China and India, plus advanced logic and memory production in Taiwan and South Korea. Regional governments tighten water-quality and industrial-emission standards, encouraging state-owned labs to tender multi-year procurement contracts for ICP-MS, LC-MS/MS, and handheld Raman. The analytical instrumentation market size allocated to semiconductor QA/QC in Asia-Pacific is projected to outgrow every other vertical as foundries race for gate-all-around transistors and high-bandwidth memory.

Europe maintains a robust, regulation-driven posture. The European Green Deal funds nationwide PFAS monitoring, circular-economy research, and solvent-free chromatography pilots. Pharmaceutical hubs in Germany, Ireland, and Switzerland integrate continuous-manufacturing lines that embed PAT analytics. Meanwhile, South America and the Middle East and Africa record steady but smaller gains as refineries, agro-exporters, and mining firms modernize labs to meet international trade certifications. High TCO remains a hurdle, so distributors increasingly promote lease-to-own and pay-per-sample schemes that lower entry barriers for first-time buyers.

- Agilent Technologies, Inc.

- Thermo Fisher Scientific Inc.

- Shimadzu Corporation

- Danaher Corporation (SCIEX, Leica Microsystems)

- Bruker Corporation

- Waters Corporation

- PerkinElmer Inc.

- Metrohm AG

- Mettler Toledo International Inc.

- Malvern Panalytical Ltd. (Spectris)

- Hitachi High-Tech Corporation

- HORIBA, Ltd.

- JEOL Ltd.

- Anton Paar GmbH

- Bio-Rad Laboratories, Inc.

- ZEISS Group

- Oxford Instruments plc

- Nikon Instruments Inc.

- Rigaku Corporation

- LECO Corporation

- Sartorius AG

- Merck KGaA (MilliporeSigma)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Adoption of Hyphenated Techniques for Biologics QA/QC

- 4.2.2 Stringent Global Limits on PFAS and Micro-plastics Boosting Ultra-Trace Spectrometry

- 4.2.3 Shift Toward Real-Time Release Testing (RTRT) in Pharma Production

- 4.2.4 Semiconductor Node Shrinkage < 3 nm Requiring Ultra-Sensitive Surface Analysis

- 4.2.5 Expansion of Renewable Aviation Fuel Programs Driving Feedstock Certification

- 4.2.6 In-Lab Analytics Surge for Battery Gigafactory Quality Assurance

- 4.3 Market Restraints

- 4.3.1 High Total Cost of Ownership of High-Resolution MS in Emerging Markets

- 4.3.2 Shortage of Skilled Analytical Chemists Elevating Outsourcing Costs

- 4.3.3 Helium Supply-Chain Volatility Impacting GC Operations

- 4.3.4 Lengthy Validation Cycles for Novel Analytical Methods in Regulated Sectors

- 4.4 Industry Ecosystem Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Degree of Competition

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Product Type

- 5.1.1 Chromatography Instruments

- 5.1.1.1 Gas Chromatography (GC) Systems

- 5.1.1.2 High-/Ultra-High-Performance Liquid Chromatography (HPLC/UHPLC)

- 5.1.1.3 Ion Chromatography (IC) Systems

- 5.1.1.4 Supercritical Fluid Chromatography (SFC) Systems

- 5.1.2 Molecular Spectroscopy

- 5.1.2.1 UV-Visible Spectrometers

- 5.1.2.2 Fourier Transform Infrared (FT-IR) Spectrometers

- 5.1.2.3 Near-Infrared (NIR) Spectrometers

- 5.1.2.4 Raman Spectrometers

- 5.1.2.5 Fluorescence Spectrometers

- 5.1.3 Elemental Spectroscopy

- 5.1.3.1 Atomic Absorption Spectrometers (AAS)

- 5.1.3.2 ICP-Optical Emission Spectrometers (ICP-OES)

- 5.1.3.3 ICP-Mass Spectrometers (ICP-MS)

- 5.1.3.4 X-Ray Fluorescence (XRF) Spectrometers

- 5.1.4 Mass Spectrometry

- 5.1.4.1 Single Quadrupole MS Systems

- 5.1.4.2 Triple Quadrupole MS Systems

- 5.1.4.3 Quadrupole-Time-of-Flight (Q-TOF) MS Systems

- 5.1.4.4 Orbitrap and FT-MS Systems

- 5.1.4.5 MALDI-TOF MS Systems

- 5.1.5 Analytical Microscopes and Imaging Systems

- 5.1.5.1 Scanning Electron Microscopes (SEM)

- 5.1.5.2 Transmission Electron Microscopes (TEM)

- 5.1.5.3 Atomic Force Microscopes (AFM)

- 5.1.5.4 Confocal and Optical Microscopes

- 5.1.6 Surface, Thermal and Particle Characterisation Instruments

- 5.1.6.1 X-Ray Diffraction (XRD) Systems

- 5.1.6.2 Thermal Analysis Instruments (DSC, TGA, etc.)

- 5.1.6.3 Particle Size and Zeta Potential Analysers

- 5.1.7 Consumables and Accessories

- 5.1.8 Data Management Software and Services

- 5.1.1 Chromatography Instruments

- 5.2 By End-User Industry

- 5.2.1 Pharmaceuticals and Biopharmaceuticals

- 5.2.1.1 Drug Discovery and Development

- 5.2.1.2 Manufacturing QA/QC

- 5.2.2 Clinical and Diagnostics Laboratories

- 5.2.3 Environmental Testing Laboratories

- 5.2.4 Food and Beverage Testing

- 5.2.5 Chemical and Petrochemical

- 5.2.6 Oil and Gas (Upstream, Midstream, Downstream)

- 5.2.7 Materials Science and Metallurgy

- 5.2.8 Semiconductor and Electronics

- 5.2.9 Academic and Government Research Institutes

- 5.2.10 Forensic and Security

- 5.2.11 Water and Wastewater Utilities

- 5.2.1 Pharmaceuticals and Biopharmaceuticals

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Nordics

- 5.3.2.7 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 South Korea

- 5.3.3.4 India

- 5.3.3.5 South East Asia

- 5.3.3.6 Australia

- 5.3.3.7 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Middle East

- 5.3.5.1.1 United Arab Emirates

- 5.3.5.1.2 Saudi Arabia

- 5.3.5.1.3 Rest of Middle East

- 5.3.5.2 Africa

- 5.3.5.2.1 South Africa

- 5.3.5.2.2 Rest of Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, Funding)

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Agilent Technologies, Inc.

- 6.4.2 Thermo Fisher Scientific Inc.

- 6.4.3 Shimadzu Corporation

- 6.4.4 Danaher Corporation (SCIEX, Leica Microsystems)

- 6.4.5 Bruker Corporation

- 6.4.6 Waters Corporation

- 6.4.7 PerkinElmer Inc.

- 6.4.8 Metrohm AG

- 6.4.9 Mettler Toledo International Inc.

- 6.4.10 Malvern Panalytical Ltd. (Spectris)

- 6.4.11 Hitachi High-Tech Corporation

- 6.4.12 HORIBA, Ltd.

- 6.4.13 JEOL Ltd.

- 6.4.14 Anton Paar GmbH

- 6.4.15 Bio-Rad Laboratories, Inc.

- 6.4.16 ZEISS Group

- 6.4.17 Oxford Instruments plc

- 6.4.18 Nikon Instruments Inc.

- 6.4.19 Rigaku Corporation

- 6.4.20 LECO Corporation

- 6.4.21 Sartorius AG

- 6.4.22 Merck KGaA (MilliporeSigma)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

X光繞射儀市場:2026-2032年全球預測(按儀器類型、最終用戶、應用和銷售管道)

X光繞射儀市場:2026-2032年全球預測(按儀器類型、最終用戶、應用和銷售管道) 分析儀器市場規模、佔有率和成長分析(按產品、技術、應用、最終用途和地區分類)-2026-2033年產業預測

分析儀器市場規模、佔有率和成長分析(按產品、技術、應用、最終用途和地區分類)-2026-2033年產業預測 分析儀器市場機會、成長促進因素、產業趨勢分析及預測(2026-2035年)分析儀器市場按技術、產品類型、最終用戶、應用和部署方式分類-2025-2032年全球預測

分析儀器市場機會、成長促進因素、產業趨勢分析及預測(2026-2035年)分析儀器市場按技術、產品類型、最終用戶、應用和部署方式分類-2025-2032年全球預測 美國分析儀器市場:市場規模、佔有率和趨勢分析(按產品、技術和應用分類),細分市場預測(2025-2033 年)催化劑篩檢合成設備市場(按產品類型、催化劑類型、操作、應用和最終用戶分類)—全球預測 2025-2030流程分析儀器市場(按儀器類型、分析類型、測量參數、最終用戶和部署類型)—2025-2030 年全球預測食品檢測和分析設備市場(按產品類型、食品類型、應用和最終用戶分類)—2025-2030 年全球預測

美國分析儀器市場:市場規模、佔有率和趨勢分析(按產品、技術和應用分類),細分市場預測(2025-2033 年)催化劑篩檢合成設備市場(按產品類型、催化劑類型、操作、應用和最終用戶分類)—全球預測 2025-2030流程分析儀器市場(按儀器類型、分析類型、測量參數、最終用戶和部署類型)—2025-2030 年全球預測食品檢測和分析設備市場(按產品類型、食品類型、應用和最終用戶分類)—2025-2030 年全球預測 全球分析儀器市場

全球分析儀器市場 2025年全球燃料特性分析儀市場報告

2025年全球燃料特性分析儀市場報告