|

市場調查報告書

商品編碼

1836720

透明電子產品:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)Transparent Electronics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

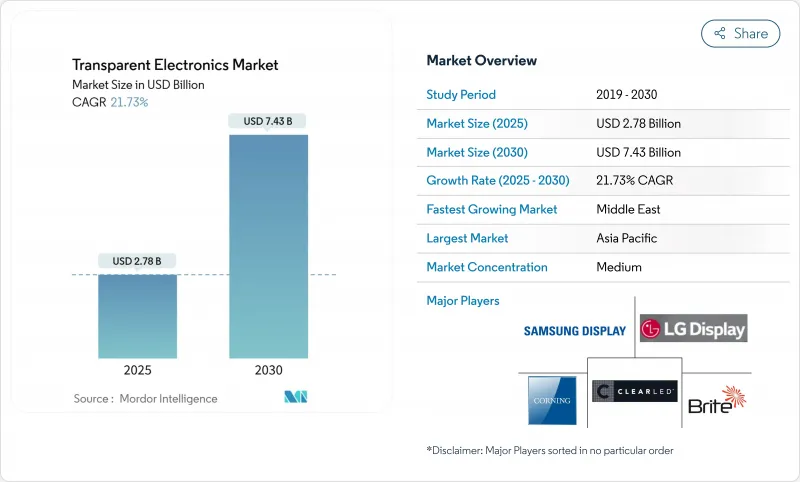

透明電子市場規模預計到2025年將達到27.8億美元,到2030年將擴大到74.3億美元,複合年成長率為21.73%。

將光學透明性與電子功能相結合的產品創新,正在將這項技術從小眾顯示應用推向節能建築、先進汽車駕駛座、身臨其境型零售等領域的主流應用。淨零建築的監管壓力、交通電氣化以及對互動式商業空間日益成長的需求,正在加速資本流入透明光伏、MicroLED 和電致變色平台。競爭優勢日益不僅取決於面板尺寸,還取決於能否獲得軟性材料和高產量比率沉積製程。那些將業務拓展到氧化銦錫 (ITO) 以外的領域,並致力於建築一體化光伏 (BIPV) 和自動駕駛電子產品的製造商,將有望抓住下一波成長浪潮。

全球透明電子產品市場趨勢與洞察

淨零建築規範推動智慧窗戶整合

歐洲立法規定,到2030年所有新建建築的能耗性能將接近零,促使建築師轉向能夠動態調節太陽輻射增益的電致變色嵌裝玻璃。在德國和斯堪地那維亞,試點安裝已顯示製冷節能超過20%,而新型液流電致變色設計現在增加了根據季節調整室內溫度5°C的功能。與建築自動化系統的整合正成為標準,為感測器和控制器製造商以及面板製造商開闢了收益管道。國家維修計畫的資金籌措,確保為外牆維修(包括智慧窗戶)提供專案預算,這為中期成長前景提供了支撐。

透明顯示器在自動駕駛汽車中越來越受歡迎

汽車製造商正在轉向大型透明抬頭顯示器(HUD),將導航、駕駛輔助和資訊娛樂數據直接投射到擋風玻璃上。最近的 MicroLED 原型已實現 85% 的透明度,同時保持 1,000 尼特的亮度,克服了先前在日間光線變化條件下產生的眩光限制。這項性能符合美國、日本和歐盟嚴格的駕駛員分心和安全標準,並有望成為計劃於 2026 年發布的中階電動車的設計標竿。隨著自動駕駛功能向 L3 級的過渡,需要更寬的視野來獲取系統狀態資訊,短期內對 MicroLED 的需求將進一步擴大。

銦供應脆弱性威脅生產穩定性

ITO 仍然是主要的透明導體,但由於超過一半的精煉銦來自同一國家,因此面板製造商每年面臨超過 30% 的現貨價格突然波動。這些價格飆升擠壓了顯示器製造商的淨利率,並推遲了產能擴張決策。材料製造商正在推出奈米銀線替代品,這種替代品可以承受 1,000 次彎曲循環,並且在 90% 的透射率下電阻小於 30 Ω/□。然而,這種轉變需要新的固化溫度和圖形化化學工藝,從而延長了量產的認證週期。

報告中分析的其他促進因素和限制因素

- 利用透明數位電子看板改變零售業

- 利用建築一體化太陽能發電拓展透明太陽能創新

細分分析

透明顯示器在 2024 年佔據了最大的收入佔有率,為 43.1%,而透明太陽能電池板預計到 2030 年將以 25.5% 的複合年成長率成長,這得益於鼓勵現場發電的建築規範。瑞士企業推出了一款 400W 玻璃狀 BIPV 模組,可融入標準建築幕牆,而不會改變外觀美感。預計到 2030 年,太陽能板的透明電子市場將達到 19 億美元,這反映了它們作為發電和採光錶面的雙重作用。產品多樣化現在擴展到支援觸控感測器和加熱器的透明導電薄膜,以及用於航太屏蔽的耐用透明陶瓷。具有動態著色功能的智慧窗戶單元在商業房地產中繼續受到歡迎,部分原因是營運成本降低,在溫暖的氣候下將投資回收期縮短至五年以內。

透明電子產品市場越來越注重產品類型之間的互通性。新興的串聯太陽能電池與microLED背板共用沉積設備,實現了多用途生產線。嵌入汽車擋風玻璃的透明感測器開始向ADAS(高級駕駛輔助系統)提供居住和環境數據,這表明價值正在從分立元件轉變為整合功能。

預計到2024年,氧化銦錫將佔據透明電子產品市場52.1%的佔有率,並在LCD/TFT和觸控螢幕供應鏈中穩固佔有一席之地。然而,預計銀奈米線複合材料和金屬網將蠶食這一領先地位,到2030年,其複合年成長率將達到22.3%。實驗室設備已證明,在90%的透射率下,薄片電阻為26 Ω/sq,在120%的應變下,電阻漂移僅為10%。應用最佳化指南材料選擇。 PEDOT:PSS等導電聚合物可用於塗覆注塑成型的塑膠基板,從而實現低成本的軟性顯示器,而石墨烯則解決了穿戴式生物感測器中熱性能和訊號均勻性的挑戰。透明陶瓷在惡劣環境下的光學應用中佔據了利基市場,而奈米碳管混合物正在光學透明性至關重要的電磁屏蔽層中嶄露頭角。

區域分析

受大規模顯示器生產工廠和中國全球最大BIPV專案的推動,亞太地區將在2024年佔據全球銷售額的43.1%。在上海和深圳等特大城市,政府將城市空氣品質目標與可再生能源發電量掛鉤的獎勵正在推動透明太陽能建築幕牆的普及。日本和韓國公司在OLED研究領域佔據主導地位,並定期展示樹立透射率和像素密度新標竿的原型產品。

北美在自動駕駛汽車軟體領域處於領先主導,這加速了對透明HUD和感測器豐富的擋風玻璃的需求。各州的建築節能法規各不相同,但電致變色應用正朝著商業維修的方向發展。歐洲嚴格的2030年氣候變遷議程將智慧玻璃和BIPV置於維修資金的核心,從而刺激了建築幕牆建築商和材料專家之間的跨國合作激增。

預計2025年至2030年,中東和非洲的智慧城市投資將以22.6%的複合年成長率成長,數位電子看板、自我調整遮陽和太陽能玻璃將融入地標性計劃中。沙烏地阿拉伯的「2030願景」將撥款數十億美元用於融合透明顯示牆和互動內容的身臨其境型計畫。拉丁美洲代表著一片尚未開發的前沿領域,豐富的太陽照度正推動著透明光伏在城市高層建築建築的應用。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場狀況

- 市場概況

- 市場促進因素

- 淨零建築標準將加速智慧窗戶的採用(歐盟)

- 抬頭顯示器在自動駕駛汽車和電動車駕駛座中的快速應用(北美)

- 支持 AR 的透明零售指示牌在亞洲一線城市激增

- 隨著建築一體化太陽能發電成為強制性要求,透明太陽能板發展勢頭強勁(中國)

- 穿戴式醫療感測器需要軟性透明導體

- 市場限制

- 銦價格波動及供應集中度

- 低產量比率大面積透明OLED面板

- 歐洲電子垃圾重金屬氧化膜法規

- 磁控濺鍍及ALD設備的資本投資高

- 生態系分析

- 技術展望

- 波特五力分析

- 新進入者的威脅

- 購買者和消費者的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭強度

第5章 市場規模及成長預測(金額)

- 按產品

- 透明顯示器

- 透明太陽能板

- 智慧窗戶/智慧玻璃

- 透明導電膜

- 透明陶瓷和鋁

- 透明感測器等

- 依材料類型

- 氧化銦錫(ITO)

- 替代 TCO(AZO、FTO)

- 奈米銀線和金屬網

- 碳基奈米材料(石墨烯、CNT)

- 導電聚合物(PEDOT:PSS)

- 依技術

- LCD/TFT

- OLED和微型OLED

- 量子點微型LED

- 薄膜太陽能電池(CIGS、鈣鈦礦)

- 電致變色和SPD

- 按最終用戶使用

- 消費性電子產品

- 汽車和運輸設備

- 架構和基礎設施

- 能源和公共產業(BIPV、農業光伏)

- 航太/國防

- 醫療保健和穿戴式設備

- 零售/數位電子看板

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 北歐國家(丹麥、瑞典、挪威、芬蘭)

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 東南亞

- 澳洲

- 其他亞太地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美

- 中東

- 波灣合作理事會成員國

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 其他非洲國家

- 北美洲

第6章 競爭態勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- BOE Technology Group Co., Ltd.

- LG Display Co., Ltd.

- Samsung Display Co., Ltd.

- Corning Incorporated

- AGC Inc.

- NSG Group(Pilkington)

- Saint-Gobain SA

- Ubiquitous Energy Inc.

- Brite Solar Inc.

- ClearLED Ltd.

- Panasonic Holdings Corp.

- Cambrios Technology Corp.

- Surmet Corporation

- 3M Company

- DuPont de Nemours Inc.

- PPG Industries Inc.

- Guardian Industries Holdings

- Shenzhen Nexnovo Technology Co., Ltd.

- Shenzhen AuroLED Technology Co., Ltd.

- Street Communication Inc.

- Apple Inc.(Transparent AR Glass R&D)

- JX Nippon Mining and Metals Corp.

- Heraeus Holding GmbH

- American Elements Corp.

第7章 市場機會與未來展望

The transparent electronics market size reached USD 2.78 billion in 2025 and is forecast to expand to USD 7.43 billion by 2030, registering a 21.73% CAGR.

Product innovation that merges optical clarity with electronic functionality is shifting the technology from niche display uses toward mainstream roles in energy-smart buildings, advanced vehicle cockpits, and immersive retail. Regulatory pressure for net-zero construction, the electrification of transport, and rising demand for interactive commercial spaces are accelerating capital flows into transparent photovoltaic, micro-LED, and electrochromic platforms. Competitive advantage is increasingly determined by access to flexible materials and high-yield deposition processes rather than panel size alone. Manufacturers that diversify beyond indium tin oxide (ITO) and align with building-integrated photovoltaics (BIPV) or autonomous-vehicle electronics are positioned to capture the next wave of growth.

Global Transparent Electronics Market Trends and Insights

Net-zero building codes driving smart-window integration

European legislation that mandates nearly zero-energy performance for all new structures by 2030 is pushing architects toward electrochromic glazing that dynamically modulates solar gain. Pilot installations across Germany and Scandinavia have shown cooling-energy cuts exceeding 20%, and newer liquid-flow electrochromic designs added the ability to shift interior temperatures 5 °C seasonally. Integration with building-automation systems is becoming standard, opening revenue streams for sensor and controls suppliers alongside panel manufacturers. Medium-term growth prospects are reinforced by funding under national renovation programs, which reserve dedicated budgets for envelope upgrades that include smart windows.

Autonomous vehicles accelerating transparent display adoption

Automakers are turning to large-format transparent head-up displays (HUDs) that project navigation, driver-assist, and infotainment data directly onto windshields. Recent micro-LED prototypes have achieved 85% transparency while retaining 1,000-nit brightness, overcoming prior glare limitations in variable daylight. This capability satisfies stringent driver-distraction and safety norms in the United States, Japan, and the EU, triggering design wins in mid-segment electric vehicles slated for 2026 release. Short-term demand is amplified by the transition to autonomous Level 3 functions, which require larger visual fields for system-status information.

Indium supply vulnerabilities threatening production stability

ITO remains the workhorse transparent conductor, yet more than half of refined indium originates from a single country, exposing panel producers to sudden spot-price swings above 30% per annum. These spikes compress display-maker margins and delay capacity-expansion decisions. Materials firms are responding with silver-nanowire alternatives that exhibit sub-30 Ω/sq resistance at 90% transmittance while tolerating 1,000 bending cycles. The transition, however, requires new curing temperatures and patterning chemistries, prolonging qualification cycles for high-volume production.

Other drivers and restraints analyzed in the detailed report include:

- Retail transformation through transparent digital signage

- Building-integrated photovoltaics expanding transparent solar innovation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Transparent displays generated the largest revenue share in 2024 at 43.1%, yet transparent solar panels are projected to grow at a 25.5% CAGR to 2030, propelled by building codes that reward on-site generation. A Swiss venture introduced a 400 W glass-like BIPV module that blends into standard facades without altering exterior aesthetics. The transparent electronics market size for solar panels is forecast to reach USD 1.9 billion by 2030, reflecting their dual role as power generators and daylighting surfaces. Product diversification now extends to transparent conductive films that underpin touch sensors and heaters, as well as rugged transparent ceramics for aerospace shielding. Smart-window units equipped with dynamic tinting continue to gain traction in commercial real estate, aided by operating-cost reductions that shorten payback periods to under five years in warm climates.

The transparent electronics market increasingly values interoperability between product categories. Emerging tandem solar cells share deposition tools with micro-LED backplanes, enabling multi-purpose manufacturing lines. Transparent sensors embedded in vehicle windshields are beginning to feed occupancy and environment data into advanced driver-assistance systems, illustrating how value migrates from stand-alone components to integrated functions.

Indium tin oxide accounted for 52.1% of transparent electronics market share in 2024, underscoring its entrenched position across LCD/TFT and touch-panel supply chains. Nevertheless, silver-nanowire composites and metal meshes are expected to erode this lead, climbing at 22.3% CAGR through 2030. Lab devices have demonstrated 26 Ω/sq sheet resistance at 90% transmittance, with only 10% resistance drift under 120% strain, making them viable for foldable phones and e-skin patches. Application-specific optimisation guides material choice. Conductive polymers such as PEDOT:PSS now coat injection-moulded plastic substrates for low-cost, flexible displays, while graphene manages heat and signal-uniformity challenges in wearable biosensors. Transparent ceramics secure niche demand in harsh-environment optics, and carbon-nanotube hybrids are emerging in electromagnetic-shielding layers where optical transparency is non-negotiable.

The Transparent Electronics Market Report is Segmented by Product (Transparent Displays, Transparent Solar Panels, Smart, and More), Material Type (Indium Tin Oxide (ITO), Alternative TCOs (AZO, FTO), and More), Technology (LCD/TFT, and More), End-User Application (Consumer Electronics, Automotive and Transportation, Aerospace and Defense, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific commanded 43.1% of 2024 revenue, anchored by high-volume fabs for displays and the world's largest BIPV programme in China. Government incentives that link urban air-quality targets to renewable-energy capacity fuel adoption of transparent solar facades in megacities such as Shanghai and Shenzhen. Japanese and South Korean firms dominate OLED research, regularly showcasing prototypes that set new benchmarks in transmittance and pixel density.

North America leverages its leadership in autonomous-vehicle software to accelerate demand for transparent HUDs and sensor-rich windshields. Building-energy rules vary by state, yet collectively favour electrochromic adoption in commercial retrofits. Europe's strict 2030 climate agenda places smart glass and BIPV at the centre of renovation funding, driving a surge of cross-border partnerships between facade contractors and materials specialists.

The Middle East and Africa is forecast to grow at 22.6% CAGR from 2025 to 2030 as smart-city investments integrate digital signage, adaptive shading and solar glass in landmark projects. Saudi Arabia's Vision 2030 allocates multi-billion-dollar budgets to immersive heritage sites that blend transparent display walls with interactive content. Latin America represents an untapped frontier where abundant solar irradiance aligns with transparent PV adoption in urban high-rise developments, although supply-chain hurdles and financing costs temper near-term uptake.

- BOE Technology Group Co., Ltd.

- LG Display Co., Ltd.

- Samsung Display Co., Ltd.

- Corning Incorporated

- AGC Inc.

- NSG Group (Pilkington)

- Saint-Gobain SA

- Ubiquitous Energy Inc.

- Brite Solar Inc.

- ClearLED Ltd.

- Panasonic Holdings Corp.

- Cambrios Technology Corp.

- Surmet Corporation

- 3M Company

- DuPont de Nemours Inc.

- PPG Industries Inc.

- Guardian Industries Holdings

- Shenzhen Nexnovo Technology Co., Ltd.

- Shenzhen AuroLED Technology Co., Ltd.

- Street Communication Inc.

- Apple Inc. (Transparent AR Glass R&D)

- JX Nippon Mining and Metals Corp.

- Heraeus Holding GmbH

- American Elements Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Net-Zero Building Codes Accelerating Smart-Window Adoption in EU

- 4.2.2 Rapid Uptake of Head-Up Displays in Autonomous and EV Cockpits (North America)

- 4.2.3 AR-Enabled Transparent Retail Signage Surge in Asia's Tier-1 Cities

- 4.2.4 Building-Integrated PV Mandates Spurring Transparent Solar Panels in China

- 4.2.5 Wearable Medical Sensors Requiring Flexible Transparent Conductors

- 4.3 Market Restraints

- 4.3.1 Indium Price Volatility and Supply Concentration

- 4.3.2 Low Yield Scaling Large-Area Transparent OLED Panels

- 4.3.3 E-waste Rules on Heavy-Metal Oxide Films in Europe

- 4.3.4 High CapEx for Magnetron Sputtering and ALD Equipment

- 4.4 Industry Ecosystem Analysis

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Product

- 5.1.1 Transparent Displays

- 5.1.2 Transparent Solar Panels

- 5.1.3 Smart Windows/Smart Glass

- 5.1.4 Transparent Conductive Films

- 5.1.5 Transparent Ceramics and Aluminum

- 5.1.6 Transparent Sensors and Others

- 5.2 By Material Type

- 5.2.1 Indium Tin Oxide (ITO)

- 5.2.2 Alternative TCOs (AZO, FTO)

- 5.2.3 Silver Nanowire and Metal Mesh

- 5.2.4 Carbon-Based Nanomaterials (Graphene, CNT)

- 5.2.5 Conductive Polymers (PEDOT:PSS)

- 5.3 By Technology

- 5.3.1 LCD/TFT

- 5.3.2 OLED and micro-OLED

- 5.3.3 Quantum-Dot and micro-LED

- 5.3.4 Thin-Film Photovoltaic (CIGS, Perovskite)

- 5.3.5 Electrochromic and SPD

- 5.4 By End-user Application

- 5.4.1 Consumer Electronics

- 5.4.2 Automotive and Transportation

- 5.4.3 Building and Infrastructure

- 5.4.4 Energy and Utilities (BIPV, Agrivoltaics)

- 5.4.5 Aerospace and Defense

- 5.4.6 Healthcare and Wearables

- 5.4.7 Retail and Digital Signage

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Nordics (Denmark, Sweden, Norway, Finland)

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 South Korea

- 5.5.3.4 India

- 5.5.3.5 Southeast Asia

- 5.5.3.6 Australia

- 5.5.3.7 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East

- 5.5.5.1 Gulf Cooperation Council Countries

- 5.5.5.2 Turkey

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 BOE Technology Group Co., Ltd.

- 6.4.2 LG Display Co., Ltd.

- 6.4.3 Samsung Display Co., Ltd.

- 6.4.4 Corning Incorporated

- 6.4.5 AGC Inc.

- 6.4.6 NSG Group (Pilkington)

- 6.4.7 Saint-Gobain SA

- 6.4.8 Ubiquitous Energy Inc.

- 6.4.9 Brite Solar Inc.

- 6.4.10 ClearLED Ltd.

- 6.4.11 Panasonic Holdings Corp.

- 6.4.12 Cambrios Technology Corp.

- 6.4.13 Surmet Corporation

- 6.4.14 3M Company

- 6.4.15 DuPont de Nemours Inc.

- 6.4.16 PPG Industries Inc.

- 6.4.17 Guardian Industries Holdings

- 6.4.18 Shenzhen Nexnovo Technology Co., Ltd.

- 6.4.19 Shenzhen AuroLED Technology Co., Ltd.

- 6.4.20 Street Communication Inc.

- 6.4.21 Apple Inc. (Transparent AR Glass R&D)

- 6.4.22 JX Nippon Mining and Metals Corp.

- 6.4.23 Heraeus Holding GmbH

- 6.4.24 American Elements Corp.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

2026年全球透明電子產品市場報告2026年全球電氣和電子材料市場報告

2026年全球透明電子產品市場報告2026年全球電氣和電子材料市場報告 奈米銀透明導電薄膜市場:按應用、終端用戶產業、產品類型、製造技術和薄膜形態分類-2026-2032年全球預測透明電子產品市場按產品類型、材料、終端用戶產業、應用和技術分類,全球預測(2026-2032年)

奈米銀透明導電薄膜市場:按應用、終端用戶產業、產品類型、製造技術和薄膜形態分類-2026-2032年全球預測透明電子產品市場按產品類型、材料、終端用戶產業、應用和技術分類,全球預測(2026-2032年) 透明電子產品市場規模、佔有率及成長分析(按材料、裝置類型、外形規格、應用和地區分類)-2026-2033年產業預測

透明電子產品市場規模、佔有率及成長分析(按材料、裝置類型、外形規格、應用和地區分類)-2026-2033年產業預測 2025 年至 2033 年透明電子產品市場報告(按產品類型、應用和地區)

2025 年至 2033 年透明電子產品市場報告(按產品類型、應用和地區) 透明電子市場,按產品類型、按材料、按泡沫係數、按最終用戶、按國家和地區 - 2025 年至 2032 年全球行業分析、市場規模、市場佔有率和預測

透明電子市場,按產品類型、按材料、按泡沫係數、按最終用戶、按國家和地區 - 2025 年至 2032 年全球行業分析、市場規模、市場佔有率和預測 全球透明電子市場

全球透明電子市場 透明電子市場,按類型(透明顯示器、透明太陽能電池板、透明窗戶)、最終用途(消費電子產品、汽車、建築、醫療保健、軍事與國防、安全系統)和預測,2024 - 2032

透明電子市場,按類型(透明顯示器、透明太陽能電池板、透明窗戶)、最終用途(消費電子產品、汽車、建築、醫療保健、軍事與國防、安全系統)和預測,2024 - 2032