|

市場調查報告書

商品編碼

1836716

外骨骼:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)Exoskeleton - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

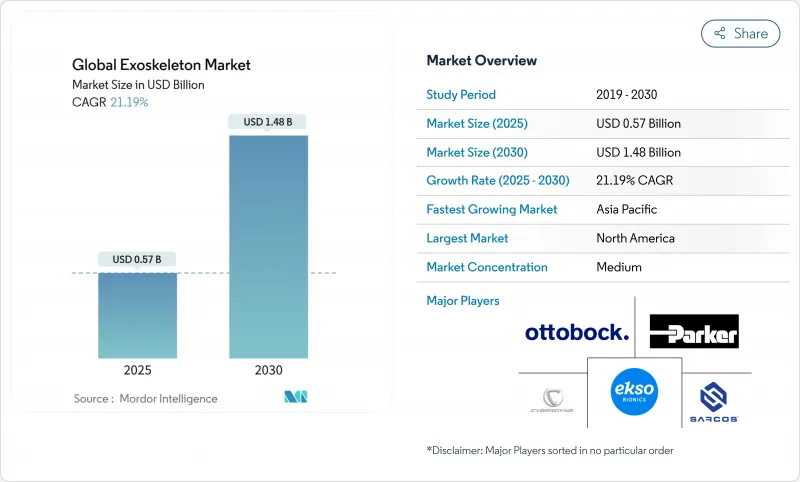

預計 2025 年全球外骨骼市場規模為 5.7 億美元,到 2030 年將達到 14.8 億美元,預測期內(2025-2030 年)的複合年成長率為 21.19%。

從早期的醫療試點到大規模項目,從單線到企業部署的工業人體工學計劃,以及國防機構將原型轉入小規模生產,該技術的應用正在迅速發生。嵌入在控制軟體中的人工智慧 (AI) 重塑了設備的反應能力。同行評審的研究表明,在重複舉重過程中,背部肌肉活動減少了 35%,直接減少了傷害索賠。輕質複合材料、功率重量比致致動器和電池能量密度的同步改進使平均單位質量減少了約 30%,提高了佩戴者的舒適度並延長了使用時間。美國醫療保險於 2024 年 1 月決定將個人外骨骼歸類為有資格享受矯正器具福利的機構,這加速了私人共同支付的引入,並影響了德國、韓國和日本的類似政策。隨著以軟體為中心的參與企業獲得設計勝利,競爭日益激烈。 NVIDIA 決定在 2025 年將 Ekso Bionics 加入其 Connect 計畫中,這表明加速培養運算人才對於持續的差異化至關重要。

全球外骨骼市場趨勢與洞察

需要先進復健解決方案的神經肌肉骨骼疾病迅速增加

同時,預計到2030年,65歲及以上老年人口將佔全球總人口的16%,將增加對助行器的需求。對照臨床試驗表明,與傳統治療相比,早期外骨骼干預可使功能恢復提高高達30%,凸顯了快速部署的臨床意義。醫療系統管理人員開始將機器人治療視為提升醫療效率的工具。這些機器人單元能夠以更少的治療師數量,實現更長、更精準的療程。在中風、多發性硬化症和創傷性腦損傷等多種神經系統疾病領域,已有確鑿證據增強了付款人的信心,並有助於理賠決策的順利進行。

醫療保健領域對機器人復健的需求不斷成長

2025年的一項調查發現,80%的治療師表示,當外骨骼機器人輔助手動操作時,他們的身體壓力減輕,工作效率提高。臨床基準測試表明,在Sheltering Arms Institute,經過12週的結構化機器人治療,脊髓損傷患者的步行速度提高了25-40%;在BSW復健中心,與傳統計畫相比,中風患者的步態對稱性提高了32%。這些結果支持從試點預算轉向多機構採購。汽車工廠和物流設施的工業工程團隊正在加入醫療產業的潮流,採購上肢機器人,以減少肩部損傷和加班成本。

高昂的資本投入和維護成本阻礙了商業性應用

標價從5萬美元到15萬美元不等,服務合約每年增加5000美元到1萬美元。投資報酬率取決於預防工傷和減少住院時間,但新興市場(公共資金是主要驅動力)受到限制和部署有限的限制。此後,供應商已收費按使用付費租賃和機器人即服務模式,儘管這些模式在北美以外的地區仍處於起步階段。

報告中分析的其他促進因素和限制因素

- 機器人技術的發展

- 新興醫療市場出現有利的報銷框架

- 由於安全指南不明確,使用外骨骼有風險

細分分析

到 2024 年,動力類產品的收入將成長 84.22%,這得益於複雜行走、爬樓梯和負重的機動輔助。這構成了大多數復健通訊協定和防禦原型的支柱。然而,隨著物流公司在物流中心部署數百個被動矯正器具,例如可減輕下背部壓力的彈簧矯正器具,到 2030 年的複合年成長率將達到 22.82%。到 2025 年,被動腰椎外骨骼將被納入職業健康預算,此前同行評審的研究證實,它們可以在搬運紙箱時將背部伸肌活動減少 35%。動力髖關節和被動脊椎支撐的結合可以同時減少能源需求和零件數量。

成本差異仍然很大,被動式產品的零售價僅為動力產品的三分之一。透過利用先進的複合材料和彈性扭轉元件,製造商在保持輔助扭矩的同時減輕了重量,使被動式產品能夠滿足嚴格的採購限制。透過將感測器直接嵌入支撐框架,被動式產品開始為企業儀表板提供人體工學分析,從而縮小了與動力式產品之間的數據差距。即使動力系統在高強度治療中仍然保持效用,被動式產品也有望從注重預算的買家那裡搶佔越來越大的市場佔有率。

2024年,移動外骨骼將佔全球銷售額的68.34%,這反映了它們能夠適應各種地形,並適應獨立的日常生活、倉庫工作和步兵機動。電池創新使其運行時間達到6至8小時,比之前的型號延長40%,可支援完整的臨床輪班或連續的生產週期。患者認為,與患者視線水平的互動具有心理益處,有助於提高居家環境中患者的依從性。固定式系統雖然目前規模較小,但由於其能夠在有限的運動學習階段提供高度重複的訓練,到2030年,其複合年成長率將達到24.23%。在醫療中心,這些系統安裝在龍門架上,治療師可以使用擴增實境(AR) 疊加技術微調患者的步態運動,加速神經可塑性介入。

可互換模組允許單一機殼在跑步機安裝和地面安裝之間切換,模糊了移動和固定之間的界限。這種靈活性對於希望在各種患者群體中分攤資本的中型康復連鎖機構來說極具吸引力。供應商正在提供即插即用的附加元件組件,例如扶手、安全帶和跑步機踏板。

區域分析

由於成熟的支付生態系統和充足的創業投資資金,北美將在2024年佔據外骨骼市場收益的40.33%。聯邦醫療保險(Medicare)91,032美元的固定報銷率大大提高了脊髓損傷患者的負擔能力,並增加了向退伍軍人健康管理局中心和一級創傷醫院的設備出貨量。在美國,包括汽車組裝和宅配物流公司在內的工業雇主正在試行上身服裝,以減少與傷害相關的停工時間,這些計劃正在逐步轉為框架合約。加拿大也走在類似的道路上,每個州的工人賠償委員會都在進行試點項目,以評估索賠減少和生產力提高的效果。

歐洲的銷售額排名第二,其中德國、法國和北歐國家領先。德國的 BARMER 覆蓋範圍涵蓋 850 萬名受益人,為近一半的法定受保人提供報銷服務。由 Horizon Europe津貼的研究合作正在蓬勃發展,將亞琛、蘇黎世和熱那亞的機器人研究所與臨床用戶聯繫起來。巴伐利亞汽車製造商正在將肩部支撐外骨骼引入其生產線,以符合肌肉骨骼暴露閾值。不斷發展的 ExosCE 認證路徑將醫療和機械指令合併為一個文件並縮短核准時間,從而促進了產品部署。

亞太地區是成長最快的叢集,到2030年的複合年成長率將達到23.78%。根據mobihealthnews.com報道,韓國製造商WIRobotics將於2025年在美國推出其WIM步行輔助機器人,凸顯了該地區的出口野心。中國的「中國製造2025」計畫為復健機器人工廠提供津貼獎勵,而日本的老齡化社會則將公共研發重點轉向輔助行動領域。儘管醫療報銷存在不確定性,但電子和造船行業的工業客戶正在批量採購腰部支撐服,以減少責任索賠。新加坡和澳洲之間的官民合作關係關係正專注於一項將外骨骼與智慧家庭生態系統結合的城市老化舉措。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場狀況

- 市場概況

- 市場促進因素

- 需要先進復健解決方案的神經肌肉骨骼疾病數量迅速增加

- 醫療保健產業對機器人復健的需求不斷成長

- 機器人技術的進步

- 新興醫療市場出現有利的報銷框架

- 將人工智慧整合到控制系統中

- 更輕的材料和更高的電池效率

- 市場限制

- 高昂的資本投入和維護成本阻礙了商業性應用

- 由於安全指南不明確,使用外骨骼有風險

- 長期有效性的臨床證據有限,影響付款人和臨床醫生的接受度

- 新興市場的保險覆蓋範圍有限

- 技術展望

- 波特五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第5章市場規模及成長預測(單位:美元)

- 依技術

- 有源/主動

- 被動的

- 透過移動

- 移動的

- 固定式

- 按部分

- 上肢

- 手外骨骼

- 手臂外骨骼

- 下肢

- 腰部

- 膝蓋

- 腳踝和腳

- 全身

- 上肢

- 按組件

- 硬體

- 軟體

- 服務

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 其他亞太地區

- 中東和非洲

- GCC

- 南非

- 其他中東和非洲地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美

- 北美洲

第6章 競爭態勢

- 市場集中度

- 市佔率分析

- 公司簡介

- CYBERDYNE Inc.

- Ekso Bionics Holdings Inc.

- Ottobock SE & Co. KGaA

- Parker Hannifin Corp.

- Sarcos Technology & Robotics Corp.

- ReWalk Robotics Ltd.

- BIONIK Laboratories Corp.

- Bioservo Technologies AB

- Gogoa Mobility Robots

- Rehab-Robotics Co. Ltd.

- Bioness Inc.(Bioventus)

- B-Temia Inc.

- Myomo Inc.

- Lockheed Martin Corp.

- Seismic Powered Clothing

- RB3D SAS

- Wearable Robotics SRL

- Fourier Intelligence

- Panasonic Corp.(Atoun)

第7章 市場機會與未來展望

- 閒置頻段和未滿足需求評估

The Global Exoskeleton Market size is estimated at USD 0.57 billion in 2025, and is expected to reach USD 1.48 billion by 2030, at a CAGR of 21.19% during the forecast period (2025-2030).

Rapid adoption is unfolding as early medical pilots convert into scaled programs, industrial ergonomics projects expand from single lines to enterprise roll-outs, and defense agencies move prototypes into limited-rate production. Artificial intelligence (AI) embedded within control software is reshaping device responsiveness, with peer-reviewed studies showing up to a 35% cut in back muscle activity during repetitive lifts, a jump that directly lowers injury claims. Parallel gains in lightweight composites, power-to-weight actuators, and battery energy density have trimmed average unit mass by roughly 30%, improving wearer comfort and session duration. The reimbursement breakthrough in the United States Medicare's January 2024 decision to classify personal exoskeletons under the brace benefit has triggered private-payer adoption and influenced similar policy moves in Germany, South Korea, and Japan. Competitive intensity is climbing as software-centric entrants secure design wins; NVIDIA's 2025 decision to place Ekso Bionics in its Connect program signaled that accelerated computing talent is now indispensable for sustained differentiation.

Global Exoskeleton Market Trends and Insights

Accelerating Prevalence of Neuro-Musculoskeletal Disorders Requiring Advanced Assistive Rehabilitation Solutions

Spinal cord injuries affect 294,000 individuals in the United States, with 17,000 new cases added annually, creating a sizeable candidate pool for robotic gait systems, while the share of people aged >= 65 is projected to reach 16% of the global population by 2030, elevating demand for mobility aids.Controlled clinical trials show that early exoskeleton intervention can lift functional recovery by up to 30% versus traditional therapy, underscoring the clinical rationale for rapid roll-out. Health-system administrators are starting to view robotic therapy as a throughput tool: units permit longer, more task-specific sessions with fewer therapists, an outcome that directly expands revenue capacity without proportionate head-count growth. Robust evidence across multiple neurological conditions stroke, multiple sclerosis, traumatic brain injury reinforces payer confidence, smoothing the path toward coverage decisions.

Growing Demand from Healthcare Sector for Robotic Rehabilitation

Hospital groups face chronic staffing gaps as rehabilitation workloads climb; surveys from 2025 show 80% of therapists reporting reduced physical strain and higher throughput when exoskeletons supplement manual assistance. Clinical benchmarking demonstrates 25-40% boosts in post-SCI walking speed after 12 weeks of structured robotic therapy at Sheltering Arms Institute, while stroke patients at BSW Rehabilitation enjoyed 32% better gait symmetry compared with conventional programs. These outcomes support a shift from pilot budgeting to multi-site procurement. Industrial engineering teams in automobile and logistics facilities are piggy-backing on medical proof points, sourcing upper-body units to curb shoulder injuries and overtime payments.

High Capital Expenditure and Maintenance Costs Limiting Widespread Commercial Adoption

List prices range between USD 50,000-150,000, with service contracts adding USD 5,000-10,000 yearly, figures that strain smaller hospitals and mid-sized factories. The return-on-investment case hinges on preventing workplace injuries and shortening inpatient stays; however, constraints in emerging markets, where public budgets dominate spend, suppress unit volumes. Vendors are subsequently pivoting to leasing and robotics-as-a-service models that charge per usage hour, but these schemes remain nascent outside North America.

Other drivers and restraints analyzed in the detailed report include:

- Advancement in Robotic Technologies

- Favorable Reimbursement Frameworks Emerging in Developed Healthcare Markets

- Risks Involved with Using Exoskeletons Due to Vague Safety Guidelines

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The powered category captured 84.22% revenue in 2024, benefitting from motor-driven assistance that supports complex gait, stair ascent, and load carriage. It forms the backbone of most rehabilitation protocols and defense prototypes. However, passive devices, such as spring-based braces that offload lower-back strain, are recording a 22.82% CAGR to 2030 as logistics firms deploy hundreds of units in distribution centers. In 2025, peer-reviewed trials confirmed passive lumbar exoskeletons could cut back-extensor activity by 35% during carton handling, bringing them into occupational health budgets. Hybrid designs are emerging: powered hip joints paired with passive spinal supports lower both energy demand and component count, pointing to a mid-term convergence of the two classes.

The cost delta remains pronounced, with passive models retailing for one-third of powered alternatives. Manufacturers leverage advanced composites and elastomeric torsion elements to maintain assistance torque while trimming weight, placing passive lines within stringent procurement caps. As sensors embed directly onto brace frames, passive units are starting to feed ergonomic analytics to enterprise dashboards, closing the data gap with their powered counterparts. These uptake catalysts position the passive cohort to absorb incremental share from budget-sensitive buyers, even as powered systems sustain utility in high-acuity therapy.

Mobile exoskeletons held 68.34% of 2024 global revenue, reflecting their ability to traverse varied terrain and therefore address daily-living independence, warehouse tasks, and infantry maneuvers. Battery innovations lifted operating time to 6-8 hours, 40% longer than older models, supporting full clinic shifts and continuous production cycles. Users cite psychological benefits from eye-level interaction, a factor boosting adherence in home settings. Stationary systems, although smaller today, clock a 24.23% CAGR through 2030 because they deliver high-repeatability training in constrained motor-learning phases. Medical centers position them on gantry frames where therapists fine-tune gait kinematics via augmented-reality overlays, a configuration that accelerates neuroplasticity interventions.

Interchangeable modules allow a single chassis to switch between treadmill-mounted and overground modes, blurring the mobile-stationary divide. This flexibility appeals to mid-sized rehabilitation chains seeking to amortize capital across varied patient cohorts. Vendors are consequently shipping plug-and-play add-ons, such as handrails, harnesses, and treadmill plates, that install without specialist tooling, reducing downtime.

The Exoskeleton Market Report is Segmented by Technology (Powered / Active and Passive), Mobility (Mobile and Stationary), Body Part (Upper Limb, Lower Limb, and Full Body), Component (Hardware, Software and Services), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America captured 40.33% of 2024 exoskeleton market revenue, supported by a mature payer ecosystem and deep venture funding. Medicare's fixed reimbursement rate of USD 91,032 dramatically improved affordability for spinal cord injury patients, lifting device shipments to Veterans Health Administration centers and Level I trauma hospitals. U.S. industrial employers-including automotive assemblers and parcel logistics firms pilot upper-body exosuits to stem injury downtime, and these projects are progressively converting into framework agreements. Canada follows similar trajectories, with provincial workers' compensation boards underwriting pilot programs that assess claims reduction and productivity gains.

Europe ranks second in revenue, anchored by Germany, France, and the Nordics. Germany's BARMER coverage decision encompassed 8.5 million beneficiaries, bringing reimbursed access to nearly half of statutory-insured citizens. Research collaborations thrive under Horizon Europe grants, linking robotics labs in Aachen, Zurich, and Genoa with clinical partners. Industrial uptake is buoyed by strict ergonomic directives; automotive OEMs in Bavaria deploy shoulder-support exoskeletons on production lines to comply with musculoskeletal exposure thresholds. The evolving ExosCE certification path eases product rollout by combining medical and machinery directives into one dossier, shortening approval timelines.

Asia-Pacific is the fastest-growing cluster at 23.78% CAGR through 2030. South Korean manufacturer WIRobotics launched the WIM gait-assist robot in the United States in 2025, highlighting the region's export ambitions mobihealthnews.com. China's Made-in-China 2025 agenda attaches grant incentives to rehabilitation robotics factories, while Japan's ageing demographics funnel public R&D to assistive mobility. Despite pockets of reimbursement uncertainty, industrial customers in electronics and shipbuilding sectors procure lumbar-support suits en masse to curb compensation claims. Public-private partnerships in Singapore and Australia focus on urban ageing initiatives that integrate exoskeletons with smart-home ecosystems.

- CYBERDYNE Inc.

- Ekso Bionics

- Ottobock

- Parker Hannifin

- Sarcos Technology & Robotics Corp.

- ReWalk Robotics

- BIONIK Laboratories Corp.

- Bioservo Technologies

- Gogoa Mobility Robots

- Rehab-Robotics Co. Ltd.

- Bioness Inc. (Bioventus)

- B-Temia

- Myomo Inc.

- Lockheed Martin Corp.

- Seismic Powered Clothing

- RB3D SAS

- Wearable Robotics SRL

- Fourier Intelligence

- Panasonic Corp. (Atoun)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating Prevalence of Neuro-Musculoskeletal Disorders Requiring Advanced Assistive Rehabilitation Solutions

- 4.2.2 Growing Demand from Healthcare Sector for Robotic Rehabilitation

- 4.2.3 Advancement in Robotic Technologies

- 4.2.4 Favorable Reimbursement Frameworks Emerging in Developed Healthcare Markets

- 4.2.5 AI Integration in Control Systems

- 4.2.6 Lightweight Materials and Battery Efficiency Gains

- 4.3 Market Restraints

- 4.3.1 High Capital Expenditure and Maintenance Costs Limiting Widespread Commercial Adoption

- 4.3.2 Risks Involved with Using Exoskeletons Due to Vague Safety Guidelines

- 4.3.3 Limited Clinical Evidence on Long-Term Efficacy Affecting Payer & Clinician Acceptance

- 4.3.4 Limited Insurance Coverage in Emerging Markets

- 4.4 Technological Outlook

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Technology

- 5.1.1 Powered / Active

- 5.1.2 Passive

- 5.2 By Mobility

- 5.2.1 Mobile

- 5.2.2 Stationary

- 5.3 By Body Part

- 5.3.1 Upper Limb

- 5.3.1.1 Hand Exoskeleton

- 5.3.1.2 Arm Exoskeleton

- 5.3.2 Lower Limb

- 5.3.2.1 Hip

- 5.3.2.2 Knee

- 5.3.2.3 Ankle & Foot

- 5.3.3 Full Body

- 5.3.1 Upper Limb

- 5.4 By Component

- 5.4.1 Hardware

- 5.4.2 Software

- 5.4.3 Services

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 CYBERDYNE Inc.

- 6.3.2 Ekso Bionics Holdings Inc.

- 6.3.3 Ottobock SE & Co. KGaA

- 6.3.4 Parker Hannifin Corp.

- 6.3.5 Sarcos Technology & Robotics Corp.

- 6.3.6 ReWalk Robotics Ltd.

- 6.3.7 BIONIK Laboratories Corp.

- 6.3.8 Bioservo Technologies AB

- 6.3.9 Gogoa Mobility Robots

- 6.3.10 Rehab-Robotics Co. Ltd.

- 6.3.11 Bioness Inc. (Bioventus)

- 6.3.12 B-Temia Inc.

- 6.3.13 Myomo Inc.

- 6.3.14 Lockheed Martin Corp.

- 6.3.15 Seismic Powered Clothing

- 6.3.16 RB3D SAS

- 6.3.17 Wearable Robotics SRL

- 6.3.18 Fourier Intelligence

- 6.3.19 Panasonic Corp. (Atoun)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

外骨骼機器人:全球市場佔有率和排名、總收入和需求預測(2025-2031年)

外骨骼機器人:全球市場佔有率和排名、總收入和需求預測(2025-2031年) 外骨骼市場(按產品類型、材料類型和應用)—2025-2032 年全球預測外骨骼機器人市場按產品類型、應用、最終用戶、技術和操作模式分類—2025-2032年全球預測建築外骨骼市場依產品類型、身體部位、應用、動力來源及通路分類-2025-2032年全球預測

外骨骼市場(按產品類型、材料類型和應用)—2025-2032 年全球預測外骨骼機器人市場按產品類型、應用、最終用戶、技術和操作模式分類—2025-2032年全球預測建築外骨骼市場依產品類型、身體部位、應用、動力來源及通路分類-2025-2032年全球預測 智慧外骨骼市場-全球產業規模、佔有率、趨勢、機會和預測,按組件、類型、產品類型、身體部位、應用、地區和競爭細分,2020 年至 2030 年

智慧外骨骼市場-全球產業規模、佔有率、趨勢、機會和預測,按組件、類型、產品類型、身體部位、應用、地區和競爭細分,2020 年至 2030 年 外骨骼系統市場報告,按組件(硬體、軟體)、類型(動力、被動)、移動性(固定式、移動式)、身體部位(下半身、上半身、全身)、最終用途領域(醫療保健、國防、工業及其他)和地區分類,2025 年至 2033 年

外骨骼系統市場報告,按組件(硬體、軟體)、類型(動力、被動)、移動性(固定式、移動式)、身體部位(下半身、上半身、全身)、最終用途領域(醫療保健、國防、工業及其他)和地區分類,2025 年至 2033 年 2025年全球建築外骨骼市場報告2025年穿戴式機器人技術全球市場報告

2025年全球建築外骨骼市場報告2025年穿戴式機器人技術全球市場報告 全球智慧外骨骼市場

全球智慧外骨骼市場 外骨骼市場:按材料、按結構、按移動性、按身體部位、按組件、按類型、按行業垂直和按地區分類 - 預測至 2030 年

外骨骼市場:按材料、按結構、按移動性、按身體部位、按組件、按類型、按行業垂直和按地區分類 - 預測至 2030 年