|

市場調查報告書

商品編碼

1836709

氟聚合物塗料:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)Fluoropolymer Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

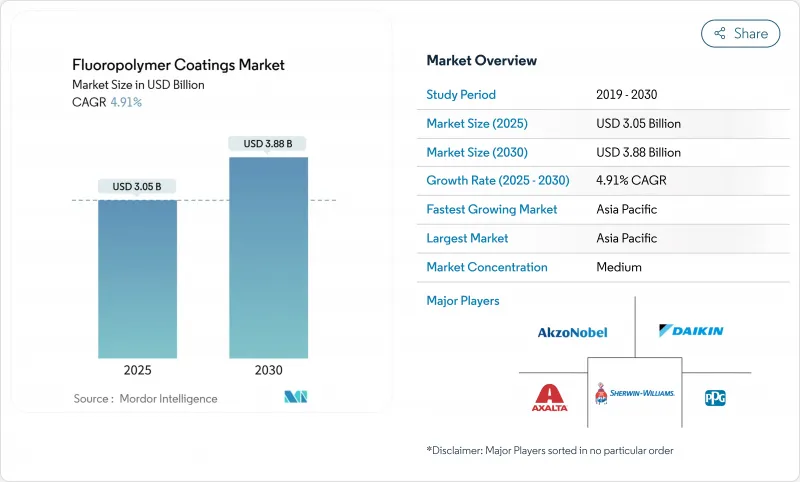

預計氟聚合物塗料市場規模在 2025 年將達到 30.5 億美元,到 2030 年預計將達到 38.8 億美元,預測期內(2025-2030 年)的複合年成長率為 4.91%。

儘管監管機構加強了對全氟和多氟烷基物質 (PFAS) 的審查,但在腐蝕性、高溫和高電氣要求環境下,對高性能表面保護的需求不斷成長,這將繼續支撐其成長。離岸風力發電、電動車動力傳動系統和鋰離子電池超級工廠的投資不斷成長,支撐了中期成長勢頭,而氫氣管道的建設則帶來了長期的量產機會。

全球氟聚合物塗料市場趨勢與洞察

離岸風力發電機塔架防腐塗料的需求不斷增加

離岸風力發電的快速成長推動了對性能的要求,超越了傳統環氧系統。如今,氟聚合物配方採用了有機-無機雜化材料,能夠抵禦海水、鹽霧和積冰等可能導致渦輪機功率輸出降低30%的因素。塗層壽命預計將延長至10-12年,使部署在深水中的下一代浮體式平台的維護窗口翻倍。原型溶膠-凝膠系統可提供強大的金屬附著力,從而降低底漆腐蝕和停機成本,從而幫助營運商實現25年的使用壽命。

低摩擦塗層在電動車動力傳動系統中的應用正在蓬勃發展。

電動車傳動系統的運轉轉速、溫度和電壓都高於內燃機,這會導致摩擦應力增加。氟聚合物塗層可降低表面能,最大程度減少電弧放電,並保護 800V 電橋中的銅導體,從而將傳動系統的整體效率提高 3-5%。領先的原始設備製造商 (OEM) 正在將 PTFE 改質塗層應用於軸承和花鍵齒輪,從而實現更小的潤滑系統,延長零件壽命和續航里程。這些解決方案在中端電動車車型的標準化預計將在 2020 年下半年加速塗層產量的成長。

螢石衍生氫氟酸的供應和定價不穩定

中國控制著全球一半以上的螢石開採量,並收緊了出口配額以維持增值生產,擠壓了外部氟化氫酸生產商。預計2024年現貨價格將再次飆升,促使大型氟聚合物製造商簽訂多年合約並增加庫存。規模較小的氟聚合物製造商面臨利潤率下降、訂單量下降以及交付中斷風險增加等問題,促使企業進行整合,以提高議價能力和供應鏈韌性。

報告中分析的其他促進因素和限制因素

- 智慧烹調器具中高溫不沾塗層的成長

- PVDF內襯鋰離子電池超級工廠擴建

- 嚴格的環境政策和法規

細分分析

PTFE 在 2024 年保持了 44% 的氟聚合物塗料市場佔有率,因為其 260°C 的使用溫度和化學惰性使其可用於半導體蝕刻工具、食品輸送機和化學反應器等重型應用。

PVDF 的複合年成長率最高,達到 5.33%,主要用於鋰離子正極黏合劑、隔膜和半導體潔淨室硬體,這些材料的介電強度和溶劑相容性至關重要。擴大北美和歐洲的產能將確保區域供應穩定,而在地化生產將最大限度地降低碳排放和關稅,從而進一步增強 PVDF 的成長潛力。

63% 的氟聚合物塗料市場是液體,水性塗料可在不損害薄膜完整性的情況下減少 VOC,有助於滿足嚴格的加州和歐盟排放法規。

粉末塗料的 VOC 含量接近零,且過噴可回收,到 2030 年,其複合年成長率將達到 5.5%。 CARC 認證的粉末面漆等發展縮短了施工時間,同時為軍事資產提供了耐化學性,將粉末塗料推向了以前由液體系統主導的航太、航海和重型機械領域。

區域分析

受中國龐大的氟化學產業基礎和大規模可再生能源建設的推動,到2024年,亞太地區將佔據氟聚合物塗料市場佔有率的44%。在印度,刺激電子和太陽能製造業的激勵措施正在創造對防腐工廠設備塗料的持續需求。日本和韓國將保持主導,推動該地區的技術前沿發展,並穩定高階塗料的消費。

北美將受益於製造業回流,將推動PVDF和PTFE的國內生產,保護主要的電池和航太產業免受供應衝擊。聯邦政府的激勵措施將鼓勵需要ETFE內襯輔助設備的氫能計劃,進一步刺激需求。

在歐洲,高環保標準與工業需求並進。德國和英國的離岸風力發電塔建造商正在指定使用壽命氟聚合物層,以最大限度地減少北海昂貴的維護宣傳活動。然而,即將推出的PFAS法規迫使複合材料製造商考慮封閉式回收和低排放製造,以確保長期生存能力。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場狀況

- 市場概況

- 市場促進因素

- 離岸風力發電機塔架防腐塗料的需求不斷增加

- 低摩擦塗層在電動車動力傳動系統部件中快速應用

- 智慧烹調器具中高溫不沾塗層的成長

- 北美和歐洲PVDF內襯鋰離子電池超級工廠的擴建

- 氫氣管道計劃激增推動ETFE和FEP塗層需求

- 市場限制

- 受中國出口配額影響,螢石衍生氫氟酸的供應和價格不穩定

- 來自業界低成本防護塗層的競爭

- 嚴格的環境法規和政策

- 價值鏈分析

- 五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場規模及成長預測(金額)

- 依樹脂類型

- 聚四氟乙烯(PTFE)

- 聚二氟亞乙烯(PVDF)

- 氟化乙丙烯(FEP)

- 乙烯-四氟乙烯(ETFE)

- 全氟烷氧基烷烴(PFA)

- 聚氟乙烯(PVF)

- 其他樹脂類型

- 按塗層技術

- 液體

- 粉末

- 按基材

- 金屬

- 塑膠

- 複合材料

- 按用途

- 產業

- 建築/施工

- 車

- 食品加工

- 航空航太

- 電

- 烹調器具

- 其他用途

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭態勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- AkzoNobel NV

- Arkema SA

- Axalta Coating Systems LLC

- Beckers Group

- Berger Paints India Ltd.

- Daikin Industries, Ltd.

- Dongyue Group Co., Ltd.

- Endura Coatings

- Hempel A/S

- Jiangsu Chenguang Fluoropolymer Co., Ltd.

- Jotun

- NIC Industries Inc.

- PPG Industries, Inc.

- Praxair Surface Technologies, Inc.

- Precision Coating Company, LLC(Integer Holdings Corporation)

- Solvay SA

- The Chemours Company

- The Sherwin-Williams Company

- Tnemec Company Inc.

- Walter Wurdack Inc.

- Whitford Corporation

第7章 市場機會與未來展望

The Fluoropolymer Coatings Market size is estimated at USD 3.05 billion in 2025, and is expected to reach USD 3.88 billion by 2030, at a CAGR of 4.91% during the forecast period (2025-2030).

Rising demand for high-performance surface protection in corrosive, high-temperature, and electrically demanding environments continues to underpin growth even as regulators tighten oversight of per- and polyfluoroalkyl substances (PFAS). Expanded investments in offshore wind farms, electric-vehicle powertrains, and lithium-ion battery gigafactories are anchoring mid-term momentum, while hydrogen pipeline build-outs promise long-term volume opportunities.

Global Fluoropolymer Coatings Market Trends and Insights

Increased Demand for Anti-corrosive Coatings in Offshore Wind Turbine Towers

Surging offshore wind installations are elevating performance requirements beyond conventional epoxy systems. Fluoropolymer formulations now integrate organic-inorganic hybrids that resist seawater, salt spray, and ice accumulation that can cut turbine output by 30%. Coating lifetimes are projected to stretch to 10 - 12 years, doubling the maintenance window for next-generation floating platforms deployed in deeper waters. Prototype sol-gel systems deliver strong metal adhesion, reducing under-film corrosion and cutting downtime expenses for operators who target 25-year service lives.

Fast-growing Adoption of Low-Friction Coatings in Electric-Vehicle Powertrains

Electrified drivetrains operate at higher rpm, temperature, and voltage than internal-combustion engines, amplifying tribological stress. Fluoropolymer layers reduce surface energy, minimize arcing, and protect copper conductors in 800 V e-axles, raising overall drivetrain efficiency by 3-5%. Leading OEMs specify PTFE-modified coatings on bearings and spline gears to enable downsized lubrication systems, extending part life and boosting range. Standardization of these solutions across mid-segment EV models will accelerate coating volumes by the latter half of the decade.

Volatile Supply and Pricing of Fluorspar-derived HF Acid

China controls well over half of mined fluorspar and tightens export quotas to retain value-added production, squeezing external producers of HF acid. Spot prices rose sharply again in 2024, prompting larger fluoropolymer makers to lock multi-year contracts and build stockpiles. Smaller coaters face margin erosion, shortened order books, and greater exposure to delivery disruptions, encouraging mergers aimed at negotiating power and supply-chain resilience.

Other drivers and restraints analyzed in the detailed report include:

- Growth of High-temperature Non-stick Coatings in Smart Cookware

- Expansion of PVDF-lined Lithium-ion Battery Gigafactories

- Strict Environmental Policies and Regulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

PTFE maintained 44% of fluoropolymer coatings market share in 2024 because its 260 °C service temperature and chemical inertness serve harsh duties in semiconductor etching tools, food-grade conveyors, and chemical reactors.

PVDF, posting the fastest 5.33% CAGR, is leveraged in lithium-ion cathode binders, separator films, and semiconductor clean-room hardware where its dielectric strength and solvent compatibility are critical. Capacity expansions in North America and Europe lock in regional security of supply, while localized production minimizes carbon footprints and tariffs, further entrenching PVDF's trajectory.

Liquid formulations held 63% of fluoropolymer coatings market size. Waterborne variants that slash VOCs without compromising film integrity are helping manufacturers comply with stringent emission rules in California and the EU.

Powder coatings deliver near-zero VOCs and over-spray recyclability, propelling a 5.5% CAGR through 2030. Developments such as CARC-qualified powder topcoats offer chemical-agent resistance for military assets while cutting application time, broadening powder use into aerospace, maritime, and heavy equipment segments formerly dominated by liquid systems.

The Fluoropolymer Coatings Market Report Segments the Industry by Resin Type (Polytetrafluoroethylene (PTFE), Polyvinylidene Fluoride (PVDF), and More), Coating Technology (Liquid and Powder), Substrate (Metal, Plastic, and Composite and Others), Application (Industrial, Building and Construction, Automotive, Food Processing, Cookware, and More), and Geography (Asia-Pacific, North America, Europe, and More).

Geography Analysis

Asia Pacific accounted for 44% of fluoropolymer coatings market share in 2024, driven by China's extensive fluorochemicals base and massive renewable-energy build-out. India follows with incentives that stimulate electronics and PV manufacturing, creating sustained coating demand for anti-corrosive plant equipment. Japan and South Korea maintain leadership in semiconductors, pushing the region's technology frontier and thereby steadying premium coating consumption.

North America benefits from reshoring that promotes domestic PVDF and PTFE production, insulating battery and aerospace primes from supply shocks. Federal incentives catalyze hydrogen projects that call for ETFE-lined balance-of-plant hardware, further bolstering demand.

Europe balances high environmental standards with industrial necessity. Offshore-wind tower builders in Germany and the United Kingdom specify long-life fluoropolymer layers to minimize expensive North Sea maintenance campaigns. Nevertheless, the looming PFAS restriction forces formulators to examine closed-loop recycling and lower-emission manufacturing to secure long-term viability.

- AkzoNobel N.V.

- Arkema SA

- Axalta Coating Systems LLC

- Beckers Group

- Berger Paints India Ltd.

- Daikin Industries, Ltd.

- Dongyue Group Co., Ltd.

- Endura Coatings

- Hempel A/S

- Jiangsu Chenguang Fluoropolymer Co., Ltd.

- Jotun

- NIC Industries Inc.

- PPG Industries, Inc.

- Praxair Surface Technologies, Inc.

- Precision Coating Company, LLC (Integer Holdings Corporation)

- Solvay SA

- The Chemours Company

- The Sherwin-Williams Company

- Tnemec Company Inc.

- Walter Wurdack Inc.

- Whitford Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increased Demand for Anti-corrosive Coatings in Offshore Wind Turbine Towers

- 4.2.2 Fast-growing Adoption of Low-Friction Coatings in Electric Vehicle Powertrain Components

- 4.2.3 Growth of High-temperature Non-stick Coatings in Smart Cookware

- 4.2.4 Expansion of PVDF-lined Lithium-ion Battery Gigafactories in the North America and Europe

- 4.2.5 Surge in Hydrogen Pipeline Projects Driving ETFE and FEP Coatings

- 4.3 Market Restraints

- 4.3.1 Volatile Supply and Pricing of Fluorspar-derived HF Acid Due to Chinese Export Quotas

- 4.3.2 Competition from Low-priced Protective Coatings Available in the Industry

- 4.3.3 Strict Environmental Policies and Regulations

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products and Services

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Resin Type

- 5.1.1 Polytetrafluoroethylene (PTFE)

- 5.1.2 Polyvinylidene Fluoride (PVDF)

- 5.1.3 Fluorinated Ethylene Propylene (FEP)

- 5.1.4 Ethylene Tetrafluoroethylene (ETFE)

- 5.1.5 Perfluoroalkoxy Alkanes (PFA)

- 5.1.6 Polyvinyl Fluoride (PVF)

- 5.1.7 Other Resin Types

- 5.2 By Coating Technology

- 5.2.1 Liquid

- 5.2.2 Powder

- 5.3 By Substrate

- 5.3.1 Metal

- 5.3.2 Plastic

- 5.3.3 Composite and Others

- 5.4 By Application

- 5.4.1 Industrial

- 5.4.2 Building and Construction

- 5.4.3 Automotive

- 5.4.4 Food Processing

- 5.4.5 Aviation and Aerospace

- 5.4.6 Electrical

- 5.4.7 Cookware

- 5.4.8 Other Applications

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 Italy

- 5.5.3.4 France

- 5.5.3.5 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (Merger and Acquisition, JV, Capacity Expansions)

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 AkzoNobel N.V.

- 6.4.2 Arkema SA

- 6.4.3 Axalta Coating Systems LLC

- 6.4.4 Beckers Group

- 6.4.5 Berger Paints India Ltd.

- 6.4.6 Daikin Industries, Ltd.

- 6.4.7 Dongyue Group Co., Ltd.

- 6.4.8 Endura Coatings

- 6.4.9 Hempel A/S

- 6.4.10 Jiangsu Chenguang Fluoropolymer Co., Ltd.

- 6.4.11 Jotun

- 6.4.12 NIC Industries Inc.

- 6.4.13 PPG Industries, Inc.

- 6.4.14 Praxair Surface Technologies, Inc.

- 6.4.15 Precision Coating Company, LLC (Integer Holdings Corporation)

- 6.4.16 Solvay SA

- 6.4.17 The Chemours Company

- 6.4.18 The Sherwin-Williams Company

- 6.4.19 Tnemec Company Inc.

- 6.4.20 Walter Wurdack Inc.

- 6.4.21 Whitford Corporation

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

- 7.2 Sustainable and Eco-Friendly Coatings

FEVE氟聚合物塗料市場:2026-2032年全球市場預測(依技術、塗料系統、基材、形態、應用、通路和最終用途分類)

FEVE氟聚合物塗料市場:2026-2032年全球市場預測(依技術、塗料系統、基材、形態、應用、通路和最終用途分類) 2026年全球氟聚合物塗料市場報告氟聚合物塗料市場:按類型、形態、基材和應用分類-2026-2032年全球市場預測防腐蝕氟聚合物塗料市場:2026-2032年全球預測(依樹脂類型、形態、應用及銷售管道)

2026年全球氟聚合物塗料市場報告氟聚合物塗料市場:按類型、形態、基材和應用分類-2026-2032年全球市場預測防腐蝕氟聚合物塗料市場:2026-2032年全球預測(依樹脂類型、形態、應用及銷售管道) FEVE氟聚合物塗料市場-2025-2030年預測

FEVE氟聚合物塗料市場-2025-2030年預測 美國氟聚合物塗料市場規模、佔有率、趨勢分析報告:按產品、最終用途、國家和細分市場預測,2025-2033 年氟聚合物塗料市場規模、佔有率、趨勢分析報告:按產品、最終用途、地區、細分市場預測,2025-2033

美國氟聚合物塗料市場規模、佔有率、趨勢分析報告:按產品、最終用途、國家和細分市場預測,2025-2033 年氟聚合物塗料市場規模、佔有率、趨勢分析報告:按產品、最終用途、地區、細分市場預測,2025-2033 FEVE 氟聚合物塗料市場(全球),2025-2029

FEVE 氟聚合物塗料市場(全球),2025-2029 氟聚合物塗料市場規模、佔有率、成長分析(按樹脂類型、應用和地區分類)- 產業預測,2025-2032 年

氟聚合物塗料市場規模、佔有率、成長分析(按樹脂類型、應用和地區分類)- 產業預測,2025-2032 年