|

市場調查報告書

商品編碼

1836695

堆高機:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)Forklift Trucks - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

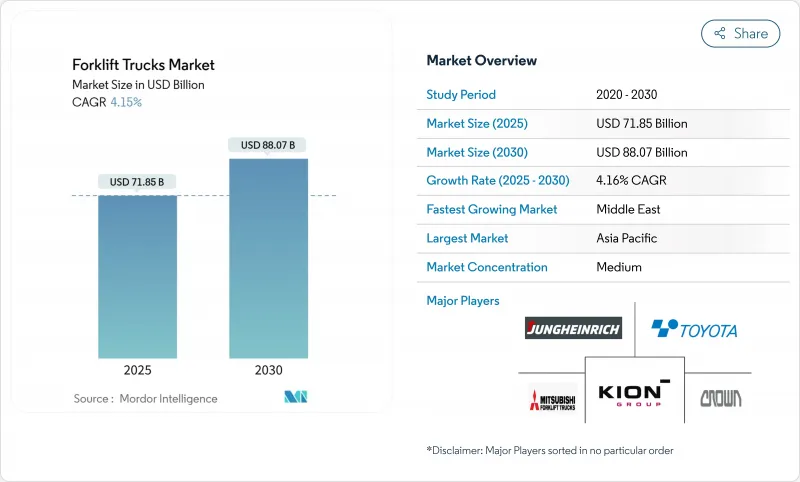

預計2025年堆高機市場規模將達718.5億美元,2030年將達880.7億美元,複合年成長率為4.16%。

儘管宏觀經濟情緒依然喜憂參半,但倉庫自動化方面的穩健資本支出、更嚴格的排放法規以及老舊車隊的穩定更換週期,正在支撐這一進程。從內燃機轉向電動和氫燃料電池車型是堆高機市場最大的結構性變化,因為它再形成了動力傳動系統供應鏈、充電基礎設施和售後服務收益來源。鋰離子電池透過實現無需更換電池的多班次作業,正在加速這一轉變,而氫能技術在快速加氫至關重要的領域也越來越受歡迎。同時,中東和東南亞等高成長地區正在待開發區物流中心採用先進設備,確保堆高機市場在成熟地區經濟成長放緩的情況下仍能保持成長動能。

全球堆高機市場趨勢與洞察

北美自動化電商倉庫的擴張

線上零售的快速成長正刺激美國和加拿大各地倉庫建設創下紀錄。預計2024年,美國電子商務銷售額將達到1.19兆美元,年增8.2%。自動駕駛和半自動卡車的需求成長最快,因為這些設備與倉庫管理軟體整合,提高了處理能力,並緩解了持續的勞動力短缺問題。由此形成的技術主導升級週期,即使在GDP成長放緩的情況下,也能維持出貨量的成長。

歐洲低溫運輸設施中鋰離子堆高機的採用率不斷提高

德國、法國和北歐地區的冷庫營運商正從鉛酸堆高機轉向鋰離子堆高機,因為鋰電池在-30°C下仍能維持95%以上的容量,充電時間縮短至1-2小時,電池壽命也因此增加三倍。低溫運輸食品和飲料產業的複合年成長率已超過4.9%,而限制冷庫內酸性氣體暴露的排放法規也正在強化這項轉變。到2025年,鋰離子堆高機將佔歐洲冷庫新增電動堆高機銷售量的40%。將電池租賃與遠端資訊處理支援捆綁在一起的原始設備製造商將透過展示相對於傳統解決方案的總成本優勢來獲得更高的利潤。

電動式堆高機高機的高初始成本限制了其普及

電動車款的購買價格比同類型內燃機車高出 20-40%。一級電動卡車的平均價格為 36,000 美元,而內燃機卡車的平均價格為 28,000 美元,這限制了其在小型企業中的普及。對於自動駕駛卡車來說,這種價格差異更加明顯,其感測器套件的安裝成本可能超過 10 萬美元。電池租賃、按次付費協議和車隊即服務套餐等替代融資方式正日益普及,但在信貸管道緊張的地區仍處於起步階段。

報告中分析的其他促進因素和限制因素

- 亞太地區嚴格的排放法規加速電動堆高機的普及

- 疫情後製造業回流將提振美國堆高機需求

- 歐洲和北歐熟練堆駕駛人短缺

細分分析

氫燃料電池車型的擴張速度超過其他動力傳動系統,到2030年,其複合年成長率將達到10.60%。堆高機市場受惠於三分鐘即可完成的加氫,其運作時間與內燃機汽車相當,排放。 局部 Power已在300個地點部署了超過6萬個燃料電池,證明了其商業性可行性。到2024年,電動車將佔據堆高機市場的69.20%,但加州、中國和歐盟的監管期限正在加速電動車隊的轉型。

內燃機製造商正在透過混合動力配置和替代燃料來應對這一挑戰,但事實證明,引擎效率的迭代改進成本過高。電池成本趨勢正在下降,燃料供應商和物流設施營運商之間的氫能發行夥伴關係關係預計將在2027年前降低發行成本。因此,動力傳動系統的多樣化將提升競爭力,使那些與電芯、電堆、充電器和軟體供應商建立合作關係的品牌受益。

三級托盤搬運車在最後一哩交叉轉運網中佔據44.70%的市場佔有率,但這些卡車相對商品化,導致利潤壓力增加。多樣化的需求迫使原始設備製造商管理各種各樣的SKU組合,從用於微型倉配中心的緊湊型三輪電動車到用於貨櫃存放場的18噸重型卡車。因此,跨類別電子設備的標準化已成為降低成本的關鍵策略。

受鋰離子技術推動,I類電動雷射雷達的複合年成長率為4.53%,該技術支援無需更換電池的多班次室內作業。隨著電商設施採用12公尺以上的貨架系統,對堆高機的提升高度和穩定性提出了更高的要求,窄通道II類雷射雷達的堆高機市場規模也不斷擴大。

區域分析

受中國、日本和印度在自動化倉庫和智慧工廠方面大量投資的推動,到2024年,亞太地區堆高機市場收益將佔全球堆高機市場的45.10%。本土品牌正利用成本優勢和政府獎勵,在國內和東南亞地區擴張,加劇了來自美國現有企業的競爭。日本和韓國的成熟堆高機車隊正進入強制更換週期,嚴格的排放法規促使新購車輛轉向鋰離子和氫動力裝置。與區域全面經濟夥伴關係(RCEP)相關的貨運走廊將促進跨境標準化,進一步擴大潛在需求。

中東是成長最快的地區,預計到2030年複合年成長率將達到6.12%。沙烏地阿拉伯、阿拉伯聯合大公國和卡達正根據國家長遠願景,建造港口、鐵路貨場和沙漠物流樞紐。中國和韓國的汽車製造商正利用該地區的自由貿易區在當地組裝汽車,而歐洲品牌則透過售後服務和自動駕駛選項來打造差異化競爭優勢。

北美依然是技術領導者。製造業回流、電商履約以及加州的零排放堆高機法規,正在支撐對電動I類和氫動力V類車輛的需求。美國在遠端資訊處理應用方面也處於領先地位,使車隊管理人員能夠追蹤電池健康狀況、駕駛員行為和維護間隔,從而提高運轉率。加拿大也採取了類似的模式,並得益於不列顛哥倫比亞省和安大略省新建的內陸港口。

在勞動力供應緊張的情況下,歐洲堆高機市場持續轉型為零排放動力傳動系統。超過40萬名持證操作員的技能短缺推動了自動化試點項目,尤其是在北歐地區。德國在鋰離子電池回收和二次利用應用的研發方面處於領先地位,並支持循環設備經濟的發展。隨著汽車和電子產品供應鏈向歐洲大陸核心消費市場轉移,東歐國家的產量成長高於平均值。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場狀況

- 市場概況

- 市場促進因素

- 北美自動化倉庫和電商倉庫的擴張

- 歐洲低溫運輸設施中鋰離子堆高機的採用率不斷提高

- 亞太地區嚴格的排放法規將加速電動堆高機的普及

- 疫情後製造業的重新整合將提振美國堆高機的需求。

- 海灣合作理事會的基礎建設投資打造待開發區物流中心

- 日韓堆高機老化更換週期

- 市場限制

- 電動堆高機的高初始成本限制了其普及

- 歐洲和北歐熟練堆高機司機短缺

- 激烈的租賃車隊競爭對原始設備製造商的利潤帶來壓力

- 供應鏈中斷影響零件可得性

- 價值/供應鏈分析

- 監管和技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭強度

第5章市場規模與成長預測(價值,美元)

- 依動力傳動系統類型

- 內燃機(ICE)

- 電動車

- 鉛酸電池

- 鋰離子

- 氫燃料電池汽車(HFCV)

- 按車輛類別

- I 類(電動駕駛卡車)

- Ⅱ類(電動窄通道)

- III類(電動托盤車)

- IV 類(ICE 緩衝輪胎)

- V 類(ICE 充氣輪胎)

- 負載容量

- 少於5噸

- 5-15噸

- 超過15噸

- 按最終用戶產業

- 製造業

- 物流/倉儲

- 建築和基礎設施

- 零售和批發

- 食品飲料低溫運輸

- 按地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

- 中東

- GCC

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他海灣合作理事會

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 其他非洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 北美洲

第6章 競爭態勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Toyota Industries Corp.

- KION Group AG

- Jungheinrich AG

- Hyster-Yale Materials Handling Inc.

- Mitsubishi Logisnext Co. Ltd.

- Crown Equipment Corp.

- Hangcha Group Co.

- Doosan Industrial Vehicles Co. Ltd.

- Komatsu Ltd.

- Anhui Heli Co. Ltd.

- Clark Material Handling Co.

- Caterpillar Inc.(CAT Lift Trucks)

- Hyundai Material Handling

- Lonking Holdings Ltd.

- Manitou Group

- Godrej & Boyce Mfg. Co.

- EP Equipment Co.

- Liugong Machinery Co.

- UniCarriers Corp.

- SANY Group Co.

第7章 市場機會與未來展望

The forklift trucks market size stands at USD 71.85 billion in 2025 and is forecast to reach USD 88.07 billion by 2030 at a 4.16% CAGR.

Healthy capital spending on warehouse automation, stricter emission rules, and a steady replacement cycle for aging fleets underpin this advance even as macro-economic sentiment remains mixed. Within the forklift trucks market, the pivot from internal-combustion to electric and hydrogen fuel-cell models is the single biggest structural change because it reshapes power-train supply chains, charging infrastructure, and after-sales revenue streams. Lithium-ion batteries are accelerating that shift by delivering multi-shift performance without battery swaps, while hydrogen technology is gaining traction where rapid refueling is critical. In parallel, high-growth geographies such as the Middle East and Southeast Asia are adopting advanced equipment at greenfield logistics hubs, ensuring that the forklift trucks market retains momentum despite slowing economic growth in mature regions.

Global Forklift Trucks Market Trends and Insights

Expansion of Automated & E-commerce Warehouses in North America

Rapid on-line retail growth is fueling record warehouse construction across the United States and Canada. US eCommerce sales stood at $1.19 trillion in 2024, an increase of 8.2% from the previous year Autonomous and semi-autonomous truck demand is rising fastest because these units integrate with warehouse-management software, boost throughput, and mitigate a persistent labor shortage. The result is a technology-led upgrade cycle that keeps unit shipments rising even when headline GDP growth softens.

Rising Adoption of Lithium-ion Forklifts in European Cold-Chain Facilities

Cold-store operators across Germany, France, and the Nordics are switching from lead-acid to lithium-ion powered trucks because lithium cells retain more than 95% capacity at -30 °C, cut charging hours to 1-2, and triple battery life. The cold-chain food & beverage segment already tops 4.9% CAGR, and emissions rules limiting acid-gas exposure inside chilled warehouses are reinforcing the shift. By 2025 lithium-ion units represent 40% of new electric forklift sales in European cold rooms as operators prioritize uptime and reduced battery maintenance . OEMs that bundle battery leasing and telematics support capture higher margins by proving total-cost advantages over legacy solutions.

High Upfront Cost of Electric Forklifts Is Restraining Adoption

Electric models carry a 20-40% purchase premium over comparable ICE units. A Class I electric truck averages USD 36,000 versus USD 28,000 for ICE, limiting take-up among small enterprises . The price gap is steeper in autonomous variants, whose sensor suites can lift installed cost above USD 100,000. Alternative financing, such as battery leasing, pay-per-use contracts, and fleet-as-a-service packages, is gaining traction but remains nascent in regions where credit access is tight.

Other drivers and restraints analyzed in the detailed report include:

- Stringent APAC Emission Mandates Accelerating Electric Forklift Uptake

- Post-pandemic Reshoring of Manufacturing Boosting United States Forklift Demand

- Shortage of Skilled Forklift Operators in Europe & Nordics

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hydrogen fuel-cell models are scaling more rapidly than any other power-train, expanding at 10.60% CAGR through 2030. The forklift trucks market benefits because hydrogen refueling takes 3 minutes, matching ICE uptime while offering zero localized emissions. Plug Power has deployed over 60,000 fuel cells across 300 sites, proving commercial viability. Although the 69.20% electric share still dominates the forklift trucks market in 2024, regulatory deadlines in California, China, and the EU accelerate the pivot to electrified fleets.

ICE manufacturers respond with hybrid configurations and alternative fuels, but achieving repeated engine efficiency gains is proving to be cost-prohibitive. Battery cost curves are trending downward, and hydrogen distribution partnerships between fuel suppliers and logistics park operators promise lower dispensing costs by 2027. Consequently, power-train diversification enhances competitive intensity, rewarding brands that secure supplier alliances for cells, stacks, chargers, and software.

Class III pallet movers dominate with 44.70% market share due to last-mile cross-dock networks, but margin pressure is intensifying because these trucks are relatively commoditized. Demand diversification forces OEMs to manage a broad SKU mix ranging from compact three-wheel electrics for micro-fulfilment centers to heavy 18-ton rigs for container yards. Electronics standardization across classes is therefore a key cost-reduction strategy.

Class I electric riders book 4.53% CAGR, propelled by lithium-ion technology that supports multi-shift indoor operations without battery swaps. The forklift trucks market size for narrow-aisle Class II units is also expanding as e-commerce facilities adopt racking systems above 12 m high, demanding trucks with enhanced lift height and stability.

The Forklift Trucks Market Report is Segmented by Power-Train Type (Internal Combustion Engine, Electric and More), Vehicle Class (Class I, Class II and More), Load Capacity (Less Than 5 Tons, 5-15 Tons and More), End-User Industry (Manufacturing, Logistics and Warehousing and More), and Geography. The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific held 45.10% of the forklift trucks market revenue in 2024 as China, Japan, and India invested heavily in automated warehousing and smart factories. Domestic brands leverage cost advantages and government incentives to expand at home and Southeast Asia, heightening competition for European and U.S. incumbents. Mature fleets in Japan and South Korea are entering mandatory replacement cycles, and strict emission caps tilt new purchases toward lithium-ion or hydrogen units. Freight corridors linked to the Regional Comprehensive Economic Partnership foster cross-border standardization that further enlarges addressable demand.

The Middle East is the fastest-growing region, projected at 6.12% CAGR to 2030, as Saudi Arabia, UAE, and Qatar build ports, rail yards, and desert distribution hubs under long-range national visions. Chinese and Korean OEMs use regional free-trade zones to assemble units locally, while European brands differentiate on after-sales service and autonomous options.

North America remains a technology bellwether. Manufacturing reshoring, e-commerce fulfillment, and California's zero-emission forklift regulation combine to sustain demand for electric Class I and hydrogen Class V machines. The United States also leads telematics adoption, with fleet managers tracking battery health, operator behavior, and maintenance intervals to boost utilization. Canada follows similar patterns, helped by new inland ports in British Columbia and Ontario.

Europe's forklift trucks market continues to transition to zero-emission power-trains amid tight labor availability. Skill shortages exceeding 400,000 certified operators drive automation pilots, especially in the Nordics. Germany leads R&D on lithium-ion battery recycling and second-life applications, supporting a circular equipment economy. Eastern European member states exhibit above-average unit growth as automotive and electronics supply chains migrate closer to the continent's core consumer markets.

- Toyota Industries Corp.

- KION Group AG

- Jungheinrich AG

- Hyster-Yale Materials Handling Inc.

- Mitsubishi Logisnext Co. Ltd.

- Crown Equipment Corp.

- Hangcha Group Co.

- Doosan Industrial Vehicles Co. Ltd.

- Komatsu Ltd.

- Anhui Heli Co. Ltd.

- Clark Material Handling Co.

- Caterpillar Inc. (CAT Lift Trucks)

- Hyundai Material Handling

- Lonking Holdings Ltd.

- Manitou Group

- Godrej & Boyce Mfg. Co.

- EP Equipment Co.

- Liugong Machinery Co.

- UniCarriers Corp.

- SANY Group Co.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of Automated & E-commerce Warehouses in North America

- 4.2.2 Rising Adoption of Lithium-ion Forklifts in European Cold-Chain Facilities

- 4.2.3 Stringent APAC Emission Mandates Accelerating Electric Forklift Uptake

- 4.2.4 Post-pandemic Reshoring of Manufacturing Boosting U.S. Forklift Demand

- 4.2.5 Infrastructure Investments Across GCC Creating Greenfield Logistics Hubs

- 4.2.6 Aging Forklift Fleet Replacement Cycle in Japan & South Korea

- 4.3 Market Restraints

- 4.3.1 High Upfront Cost of Electric Forklift Is Restraining Adoption

- 4.3.2 Shortage of Skilled Forklift Operators in Europe & Nordics

- 4.3.3 Intense Rental-Fleet Competition Compressing OEM Margins

- 4.3.4 Supply Chain Disruptions Affecting Component Availability

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory & Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Power-train Type

- 5.1.1 Internal Combustion Engine (ICE)

- 5.1.2 Electric

- 5.1.2.1 Lead-acid

- 5.1.2.2 Li-ion

- 5.1.3 Hydrogen Fuel-cell Vehicle (HFCV)

- 5.2 By Vehicle Class

- 5.2.1 Class I (Electric Rider Trucks)

- 5.2.2 Class II (Electric Narrow-Aisle)

- 5.2.3 Class III (Electric Pallet)

- 5.2.4 Class IV (ICE Cushion-Tire)

- 5.2.5 Class V (ICE Pneumatic-Tire)

- 5.3 By Load Capacity

- 5.3.1 Less than 5 Tons

- 5.3.2 5-15 Tons

- 5.3.3 Above 15 Tons

- 5.4 By End-user Industry

- 5.4.1 Manufacturing

- 5.4.2 Logistics & Warehousing

- 5.4.3 Construction & Infrastructure

- 5.4.4 Retail & Wholesale

- 5.4.5 Food & Beverage Cold-Chain

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Middle East

- 5.5.4.1 GCC

- 5.5.4.1.1 Saudi Arabia

- 5.5.4.1.2 United Arab Emirates

- 5.5.4.1.3 Rest of GCC

- 5.5.4.2 Turkey

- 5.5.4.3 Rest of Middle East

- 5.5.5 Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Rest of Africa

- 5.5.6 Asia Pacific

- 5.5.6.1 China

- 5.5.6.2 India

- 5.5.6.3 Japan

- 5.5.6.4 South Korea

- 5.5.6.5 Rest of Asia Pacific

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, JVs, Product Launches)

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Toyota Industries Corp.

- 6.4.2 KION Group AG

- 6.4.3 Jungheinrich AG

- 6.4.4 Hyster-Yale Materials Handling Inc.

- 6.4.5 Mitsubishi Logisnext Co. Ltd.

- 6.4.6 Crown Equipment Corp.

- 6.4.7 Hangcha Group Co.

- 6.4.8 Doosan Industrial Vehicles Co. Ltd.

- 6.4.9 Komatsu Ltd.

- 6.4.10 Anhui Heli Co. Ltd.

- 6.4.11 Clark Material Handling Co.

- 6.4.12 Caterpillar Inc. (CAT Lift Trucks)

- 6.4.13 Hyundai Material Handling

- 6.4.14 Lonking Holdings Ltd.

- 6.4.15 Manitou Group

- 6.4.16 Godrej & Boyce Mfg. Co.

- 6.4.17 EP Equipment Co.

- 6.4.18 Liugong Machinery Co.

- 6.4.19 UniCarriers Corp.

- 6.4.20 SANY Group Co.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

堆高機市場:動力來源、等級、負載容量、技術、最終用戶和應用分類-2026-2032年全球市場預測堆高機變速箱市場:依負載能力、動力來源及終端用戶產業分類-2026-2032年全球市場預測

堆高機市場:動力來源、等級、負載容量、技術、最終用戶和應用分類-2026-2032年全球市場預測堆高機變速箱市場:依負載能力、動力來源及終端用戶產業分類-2026-2032年全球市場預測 堆高機市場規模、佔有率、趨勢和預測:按產品類型、技術、等級、應用和地區分類,2026-2034年超窄巷道堆高機市場:依產品類型、負載能力、作業範圍類型、應用、最終用戶產業、通路分類,全球預測(2026-2032年)

堆高機市場規模、佔有率、趨勢和預測:按產品類型、技術、等級、應用和地區分類,2026-2034年超窄巷道堆高機市場:依產品類型、負載能力、作業範圍類型、應用、最終用戶產業、通路分類,全球預測(2026-2032年) 港口堆高機市場規模、佔有率和成長分析:按產品類型、載重能力、應用、最終用戶產業、分銷管道、地區和產業預測分類,2026-2033年

港口堆高機市場規模、佔有率和成長分析:按產品類型、載重能力、應用、最終用戶產業、分銷管道、地區和產業預測分類,2026-2033年 倉庫堆高機市場規模、佔有率和成長分析:按堆高機類型、載重能力、終端用戶產業、動力來源和地區分類-2026-2033年產業預測

倉庫堆高機市場規模、佔有率和成長分析:按堆高機類型、載重能力、終端用戶產業、動力來源和地區分類-2026-2033年產業預測 多向堆高機市場規模、佔有率和成長分析:按堆高機類型、燃料類型、載重能力、應用、終端用戶產業、地區和產業預測分類,2026-2033年

多向堆高機市場規模、佔有率和成長分析:按堆高機類型、燃料類型、載重能力、應用、終端用戶產業、地區和產業預測分類,2026-2033年 堆高機延伸臂市場規模、佔有率和成長分析:按延伸臂類型、應用、材質、最終用戶和地區分類-2026-2033年產業預測

堆高機延伸臂市場規模、佔有率和成長分析:按延伸臂類型、應用、材質、最終用戶和地區分類-2026-2033年產業預測 全球堆高機市場規模、佔有率、趨勢和成長分析報告(2026-2034)日本堆高機市場規模、佔有率、趨勢和預測:按類型、動力來源、載重能力、電池、最終用戶和地區分類,2026-2034年

全球堆高機市場規模、佔有率、趨勢和成長分析報告(2026-2034)日本堆高機市場規模、佔有率、趨勢和預測:按類型、動力來源、載重能力、電池、最終用戶和地區分類,2026-2034年