|

市場調查報告書

商品編碼

1836694

印度豪華車:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)India Luxury Car - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

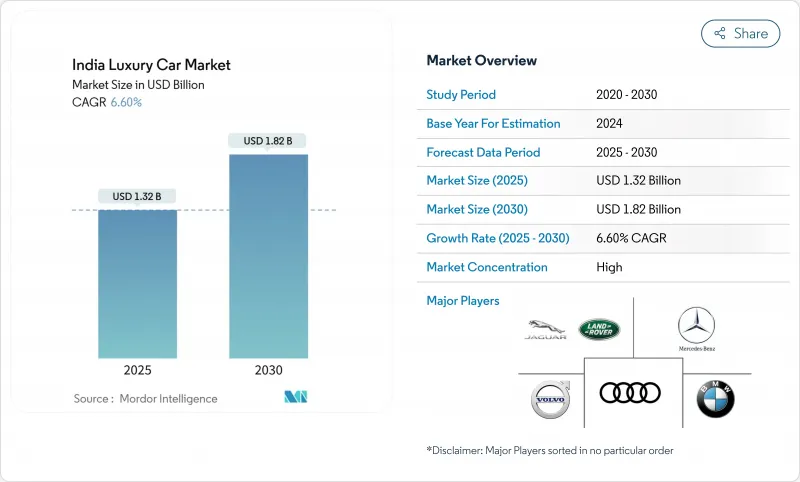

印度豪華車市場預計到 2025 年將達到 13.2 億美元,到 2030 年將達到 18.2 億美元,複合年成長率為 6.60%。

強勁成長的動力源於中上層家庭可支配收入的提高、信貸供應的擴大以及各州差異化的電動車獎勵,這些激勵措施降低了豪華車的總擁有成本。競爭日益激烈,尤其是來自德國本土企業的競爭,帶來了更廣泛的產品選擇和更短的車型週期。在需求方面,進口關稅的降低以及價格維持在5萬至8萬印度盧比範圍內的本地組裝正在推動成長,而來自二線城市的購車者也越來越青睞高階品牌。儘管稅收的複雜性和ADAS服務領域的技能短缺正在抑製成長軌跡,但隨著客戶群的擴大以及原始設備製造商將數位零售之旅融入購買流程中,長期趨勢仍然強勁。

印度豪華車市場趨勢與洞察

中上階層家庭的優質化

預計到 2025 年,年收入 2,000 萬印度盧比或以上的富裕家庭數量將從 1,000 萬人成長到 2,600 萬,這將為印度豪華車市場創造廣闊的基礎。年輕的專業人士和第一代企業家擴大將豪華車視為身份的象徵,並在每次購車時分配更多的預算。梅賽德斯-奔馳報告稱,到 2024 年,80% 的交付將採用融資方式,Star Agility 計劃的滲透率將達到 63%。該品牌在蘇拉特和哥印拜陀等二線樞紐的展示室的訪客數量加倍,標誌著其正在向大都會圈以外的地區擴張。這些人口結構的變化顯著擴大了現有基礎,在宏觀經濟波動中推動了持續成長。

入門車型(CKD)供應增加

本地組裝使原始設備製造商能夠避免對全量生產的車輛徵收進口關稅,並在不影響其豪華價值的情況下使其入門車型具有競爭力。 BMW已實現 50% 的本地化,梅賽德斯 - 奔馳已實現 60%,從而能夠在 20,000-50,000 印度盧比的入門級細分市場中實現戰略定價。長軸距衍生、增強的後座冷卻系統和印度特定的懸吊配置展示了 CKD 營運如何使全球車型適應當地偏好。然而,2024 年預算中的新規定要求在本地組裝關鍵的動力傳動系統總成部件,從而提高了盈虧平衡點並迫使一些小批量車型提價。儘管如此,原始設備製造商仍將 CKD 視為擴大產量、建立供應商生態系統和加快車型更新周期的關鍵,從而增強了 CKD 對市場成長的淨正貢獻。

高消費稅和附加稅結構(最高 50%)

商品及服務稅 (GST) 和附加稅 (Cess)總合可能導致展示室上漲 50%,從而推高購置成本,並抑制整體可尋址需求,儘管人們的生活水準不斷提高。 2024 年預算將價格超過 4 萬美元的高階進口商品關稅減半至 70%,同時引入 40% 的農業基礎設施和發展附加稅,實際上將課稅恢復到 110%。這種波動使 OEM 定價策略變得複雜,通常會鼓勵品牌提供高達 15,000 印度盧比的折扣來清理庫存。雖然對於超高階整車廠 (CBU) 來說,這種懲罰更為嚴厲,但對本地組裝車型的相對保護正在推動 CKD 生產線的持續擴張,即使是小眾車型也是如此。

報告中分析的其他促進因素和限制因素

- 州政府電動車激勵措施

- 城際走廊快速部署150kW以上公共直流充電樁

- 認證二手車網路建置延遲

細分分析

2024年,SUV佔據了印度豪華車市場48.10%的佔有率,這得益於其感知安全性、卓越的道路表現力以及適合混合公路路況的出色離地間隙。寬敞的座艙空間也支援企業CEO們常見的專車接送需求。梅賽德斯-奔馳GLE和寶馬X5繼續領先銷量,而本地組裝的奧迪Q3則拓展了其在高階市場的影響力。原始設備製造商透過「越野」體驗活動進一步刺激了需求,讓首次購買豪華車的消費者對其產品的可靠性更加放心。

轎車正經歷復甦,預計複合年成長率為9.80%,這得益於熱愛駕駛的千禧世代和X世代消費者對其動感的操控和精緻的美學設計所吸引。 2024年,BMWM系銷量飆升250%,梅賽德斯-邁巴赫銷量幾乎加倍,顯示人們對高功率動力傳動系統和後座豪華配置的需求強勁。 BMWi7和梅賽德斯EQS等電動豪華轎車也正在重塑細分市場的認知,它們將性能與永續性性相結合,創造出與無處不在的SUV截然不同的價值提案。以銷售量計算,轎車預計將從2024年的27%成長到2030年的32%,提升所有主要原始設備製造商(OEM)的產品組合多樣性。

這主要歸功於汽油混合動力和動力傳動系統,它們擁有久經考驗的可靠性、快速加油功能以及來自超過275家授權維修廠的全面服務支援。高階純電動車預計將以21.35%的複合年成長率成長。 BMW的iX、i4和i7車型正在為首次購買電動車的消費者帶來超越許多內燃機汽車的先進駕駛輔助功能。

直流快速充電的日益普及,幫助富裕消費者克服了續航里程焦慮的最後障礙,而運行成本的下降和綠色牌照的優惠則提升了便利性的價值。混合動力汽車佔據著一個短暫的市場,吸引著那些熱衷於燃油效率但對其所在城市充電基礎設施不滿意的客戶。特斯拉將於2025年在孟買開設展示室,這可能會加劇競爭,並提高客戶對無線更新、動態軟體功能和直銷透明度的期望。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場狀況

- 市場概況

- 市場促進因素

- 中上階層家庭的優質化

- 入門車型增加(CKD)

- 州政府電動車激勵措施

- 城際走廊快速部署150kW以上公共直流充電樁

- OEM訂購和租賃計劃

- 中國超豪華電動車品牌將印度視為下一個擴張目的地

- 市場限制

- 高消費稅和附加稅結構(最高 50%)

- 整車進口關稅的不確定性

- 認證二手車網路建置延遲

- ADAS 和高壓系統訓練有素的技術人員短缺

- 價值/供應鏈分析

- 監管狀況

- 技術展望

- 波特五力分析

- 買家/消費者的議價能力

- 供應商的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭強度

第5章市場規模與成長預測:價值(美元)

- 按車輛類型

- SUV

- 轎車

- 掀背車

- 按驅動類型

- 內燃機

- 混合

- 電池電動

- 價格分佈

- INR 20 L~50 L

- INR 50 L~80 L

- 80印度盧比或以上

- 按銷售管道

- 直營展示室

- 授權經銷商/專利權

- 線上(直接面對消費者)

- 按地區(印度)

- 北印度

- 西印度群島

- 南印度

- 印度東部和東北部

第6章 競爭態勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Mercedes-Benz AG

- BMW Group

- Audi AG

- Jaguar Land Rover Automotive PLC

- Volvo Car AB

- Lexus

- Porsche AG

- Rolls-Royce Motor Cars India

- Bentley Motors Limited

- Automobili Lamborghini SpA

- Ferrari India

- Maserati SpA

- Aston Martin Lagonda Global Holdings PLC

- Jeep(Stellantis)

第7章 市場機會與未來展望

The India luxury car market size stands at USD 1.32 billion in 2025 and is forecast to reach USD 1.82 billion by 2030, expanding at a 6.60% CAGR.

Robust growth stems from rising disposable income among upper-middle-class households, expanded credit availability, and differentiated state-level EV incentives that compress the total cost of ownership for premium automobiles. Intensifying competitive activity, particularly among German incumbents, continues to widen product choice and shorten model cycles, while accelerating infrastructure roll-outs ease range anxiety for high-performance battery electric vehicles. On the demand side, aspirational buyers from Tier-II cities increasingly favour premium brands, helped by localized assembly that trims import duties and keeps prices within the INR 50-80 lakh bracket. Although taxation complexity and skill shortages in ADAS servicing temper the growth curve, the long-term trajectory remains firmly positive as customer cohorts expand and OEMs embed digital retail journeys into the purchase process.

India Luxury Car Market Trends and Insights

Premiumization of Upper-middle-class Households

Affluent households earning over INR 20 lakh annually are forecast to increase from 10 million to 26 million by 2025, laying a broad foundation for the Indian luxury car market. Younger professionals and first-generation entrepreneurs increasingly view premium vehicles as status symbols, driving higher budget allocations per purchase. OEM finance programmes reinforce the trend; Mercedes-Benz notes that 80% of deliveries were financed in 2024 and that its Star Agility scheme grew 63% in penetration. Brand showrooms in Tier-II hubs such as Surat and Coimbatore are now seeing double the footfall, signaling diffusion beyond metropolitan areas. This demographic shift materially enlarges the addressable base, propelling consistent growth even amid macro volatility.

Rising Availability of Entry-level Models (CKD)

Localized assembly enables OEMs to bypass steep import duties on completely built units, positioning entry variants competitively without eroding luxury cachet. BMW has achieved 50% localization, while Mercedes-Benz has reached 60%, allowing strategic pricing in the INR 20-50 lakh gateway segment. Tailored long-wheelbase derivatives, enhanced rear-seat cooling, and India-specific suspension setups showcase how CKD operations adapt global models to local preferences. New 2024 Budget rules, however, require domestic assembly of critical powertrain components, raising breakeven thresholds and pushing some low-volume nameplates toward price hikes. Even so, OEMs regard CKD as indispensable for volume scale, supplier ecosystem development, and faster model refresh cycles, reinforcing its net positive contribution to market growth.

High GST & Cess Structure (up to 50%)

Combined GST and cess charges can lift ex-showroom prices by 50%, inflating acquisition costs and constricting total addressable demand despite rising affluence. While the 2024 Budget halved customs duty on premium imports above USD 40,000 to 70%, it introduced a 40% Agriculture Infrastructure and Development Cess, returning the effective levy to 110% . This volatility complicates OEM pricing strategies and nudges brands toward discounting, often up to INR 15 lakh, to clear inventory. The penalty is more acute for ultra-luxury CBUs, whereas locally assembled variants remain relatively sheltered, driving continuous expansion of CKD lines even for niche models.

Other drivers and restraints analyzed in the detailed report include:

- EV Incentives by State Governments

- Rapid Rollout of 150 kW+ Public DC Chargers on Inter-city Corridors

- Slow Build-out of Certified Pre-owned Luxury Networks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

SUVs captured 48.10% of India's luxury car market share in 2024 on the back of perceived safety, commanding road presence, and superior ground clearance suited to mixed highway conditions. Larger cabin volume also supports chauffeur-driven use cases common among corporate principals. Mercedes-Benz GLE and BMW X5 remained volume anchors, while locally assembled Audi Q3 extended reach into aspirational cohorts. OEMs further amplified demand through 'off-road' experiential events that reassured first-time luxury buyers about product robustness.

Sedans are resurging with a forecast 9.80% CAGR as driving-enthusiast millennials and Gen-X consumers gravitate toward dynamic handling and sleek aesthetics. BMW M series deliveries soared 250% in 2024, and Mercedes-Maybach nearly doubled volumes, indicating a robust appetite for high-output powertrains and rear-seat luxury. Electrified limousines such as the BMW i7 and Mercedes EQS also reset segment perception by combining performance with sustainability, creating a differentiated value proposition against omnipresent SUVs. In volume terms, sedans are expected to lift their contribution from 27% in 2024 to 32% by 2030, boosting portfolio diversity for all major OEMs.

Internal combustion platforms still underpin 75.20% of deliveries, largely because petrol hybrids and diesel powertrains offer proven reliability, quick refuelling, and extensive service support across 275+ authorized workshops. However, electrification momentum is unmistakable: luxury BEVs are expected to register a 21.35% CAGR. BMW's iX, i4, and i7 models are introducing first-time EV buyers to advanced driver-assist features that surpass many ICE counterparts.

Widening DC-fast-charge availability pushes affluent consumers over the last range-anxiety hurdle, while lower running costs and green-number-plate privileges add material convenience value. Hybrids occupy a transitory segment, absorbing customers keen on fuel efficiency but unconvinced about charging infrastructure in their city. Tesla's Mumbai showroom opening in 2025 is likely to intensify competition and elevate customer expectations for over-the-air updates, dynamic software features, and direct sales transparency.

The India Luxury Car Market Report is Segmented by Vehicle Type (SUV, Sedan and More), Drive Type (IC Engine, Hybrid and More), Price Range (INR 20 L- 50 L, INR 50 L - 80 L and More), Sales Channel (Company-Owned Showrooms, Authorized Dealerships/Franchise and More) and Region. The Market Sizes and Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Mercedes-Benz AG

- BMW Group

- Audi AG

- Jaguar Land Rover Automotive PLC

- Volvo Car AB

- Lexus

- Porsche AG

- Rolls-Royce Motor Cars India

- Bentley Motors Limited

- Automobili Lamborghini S.p.A.

- Ferrari India

- Maserati S.p.A

- Aston Martin Lagonda Global Holdings PLC

- Jeep (Stellantis)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Premiumization of Upper-middle-class households

- 4.2.2 Rising availability of entry-level models (CKD)

- 4.2.3 EV incentives by state governments

- 4.2.4 Rapid rollout of 150 kW+ public DC chargers on inter-city corridors

- 4.2.5 OEM-financed subscription & leasing schemes

- 4.2.6 Chinese ultra-luxury EV brands eyeing India as next launch pad

- 4.3 Market Restraints

- 4.3.1 High GST & Cess structure (up to 50 %)

- 4.3.2 Import duty uncertainty on CBUs

- 4.3.3 Slow build-out of certified pre-owned luxury networks

- 4.3.4 Scarcity of trained technicians for ADAS & high-voltage systems

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers/Consumers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By Vehicle Type

- 5.1.1 SUV

- 5.1.2 Sedan

- 5.1.3 Hatchback

- 5.2 By Drive Type

- 5.2.1 IC Engine

- 5.2.2 Hybrid

- 5.2.3 Battery Electric

- 5.3 By Price Range

- 5.3.1 INR 20 L to 50 L

- 5.3.2 INR 50 L to 80 L

- 5.3.3 Above INR 80 L

- 5.4 By Sales Channel

- 5.4.1 Company-owned Showrooms

- 5.4.2 Authorized Dealerships / Franchise

- 5.4.3 Online (Direct-to-Consumer)

- 5.5 By Region (India)

- 5.5.1 North India

- 5.5.2 West India

- 5.5.3 South India

- 5.5.4 East & North-East India

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Mercedes-Benz AG

- 6.4.2 BMW Group

- 6.4.3 Audi AG

- 6.4.4 Jaguar Land Rover Automotive PLC

- 6.4.5 Volvo Car AB

- 6.4.6 Lexus

- 6.4.7 Porsche AG

- 6.4.8 Rolls-Royce Motor Cars India

- 6.4.9 Bentley Motors Limited

- 6.4.10 Automobili Lamborghini S.p.A.

- 6.4.11 Ferrari India

- 6.4.12 Maserati S.p.A

- 6.4.13 Aston Martin Lagonda Global Holdings PLC

- 6.4.14 Jeep (Stellantis)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

2026年全球豪華車市場報告

2026年全球豪華車市場報告 豪華車市場規模、佔有率、趨勢及報告:按車型、燃料類型、價格範圍和地區分類(2026-2034 年)

豪華車市場規模、佔有率、趨勢及報告:按車型、燃料類型、價格範圍和地區分類(2026-2034 年) 豪華車市場分析及預測(至2035年):依類型、產品類型、服務、技術、零件、應用、材質、最終用戶、安裝類型、解決方案分類

豪華車市場分析及預測(至2035年):依類型、產品類型、服務、技術、零件、應用、材質、最終用戶、安裝類型、解決方案分類 中國豪華車市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲豪華車市場-佔有率分析、產業趨勢、統計和成長預測(2026-2031)

中國豪華車市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲豪華車市場-佔有率分析、產業趨勢、統計和成長預測(2026-2031) 2026-2034年全球豪華車市場規模、佔有率、趨勢及成長分析報告豪華車:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

2026-2034年全球豪華車市場規模、佔有率、趨勢及成長分析報告豪華車:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 豪華車市場機會、成長要素、產業趨勢分析及預測(2026-2035)日本豪華車市場報告:按車輛類型、燃料類型、價格範圍和地區分類(2026-2034 年)

豪華車市場機會、成長要素、產業趨勢分析及預測(2026-2035)日本豪華車市場報告:按車輛類型、燃料類型、價格範圍和地區分類(2026-2034 年) 豪華車市場規模、佔有率及成長分析(依動力系統、車輛類型、燃料類型、零件和地區分類)-2026-2033年產業預測

豪華車市場規模、佔有率及成長分析(依動力系統、車輛類型、燃料類型、零件和地區分類)-2026-2033年產業預測